Fahroni/iStock via Getty Images

Welcome to the September 2022 edition of the lithium miner news. The past month saw lithium carbonate and spodumene spot prices achieve new record price highs (in CNY) as demand outstrips supply.

We also saw the European Commission discussing their Critical Raw Materials Act, following on from the U.S. Inflation Reduction Act (US$369b for climate change policies).

The lithium producers are making record revenues and profits buoyed by record lithium prices. The funded near-term lithium producers (AGY, LAC, CXO, SGML) are all set to start production in the next 1-6 months at a perfect time when lithium is desperately needed.

Lithium price news

Asian Metal reported during the past 30 days, 99.5% China lithium carbonate spot prices were up 1.1% and China lithium hydroxide prices were up 0.89%. Lithium Iron Phosphate (Li 3.9% min) prices were up 1.6%. Spodumene (6% min) prices were up 4.1% over the past 30 days.

Metal.com reported lithium spodumene concentrate (6%, CIF China) price of CNY 36,358 (~USD 5,100/mt), as of September 23, 2022.

On September 19 BNN Bloomberg reported:

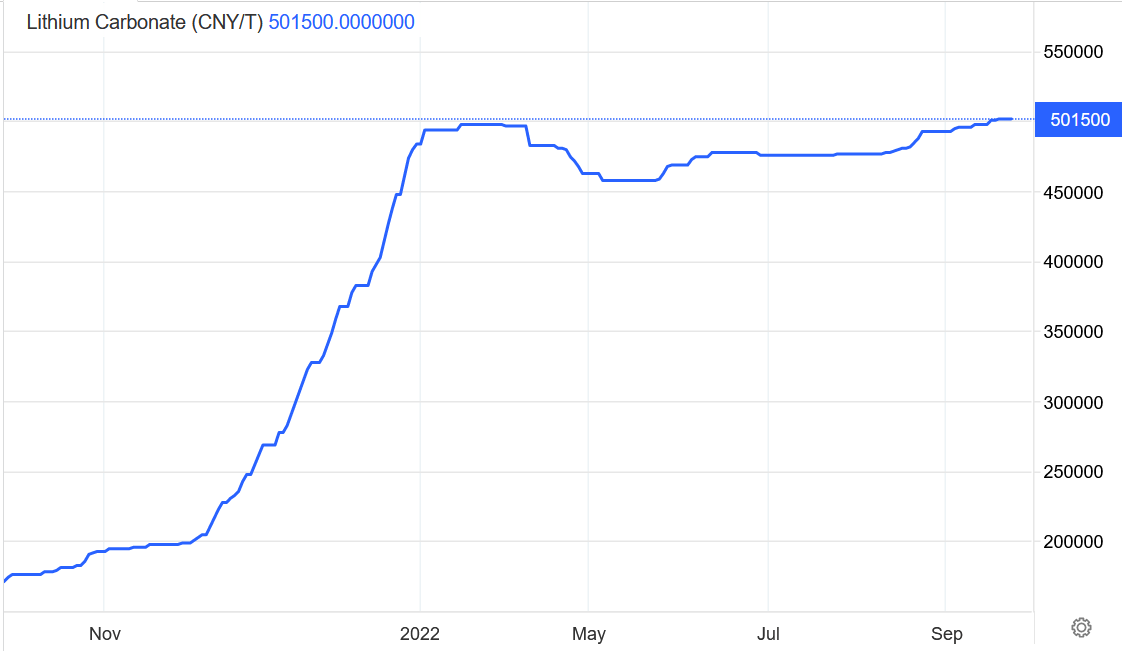

Lithium resumes insane gains to add pressure on automakers… Lithium carbonate jumped to a new record Friday of 500,500 yuan ($71,315) a ton in China, according to data from Asian Metal Inc. The battery material has roughly tripled in the past year, and is more than 1,150% higher than a pandemic low touched in July 2020. Prices of lithium hydroxide are also gaining and closing in on an all-time high set in April.

On September 20 Pilbara Minerals reported (a new record):

Pilbara Minerals intends to accept the highest bid of US$6,988/dmt (SC5.5, FOB Port Hedland basis) which on a pro rata basis for lithia content (and adjusted to be inclusive of freight costs) equates to a price of ~US$7,708/dmt (SC6.0, CIF China basis).

Note: Bold emphasis in the above two news by the author.

China Lithium carbonate spot price – CNY 501,500 (~USD 70,352)

Trading Economics

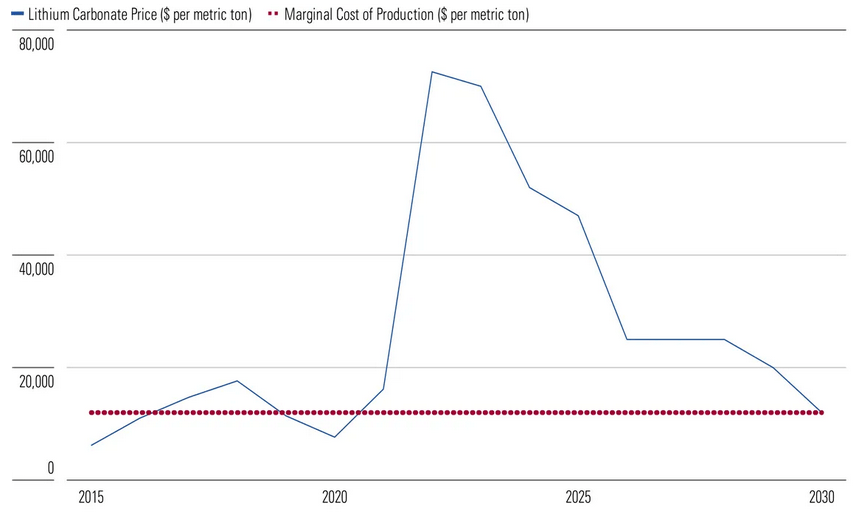

Morningstar’s lithium price forecast 2022 to 2030 (as of mid 2022)

Morningstar

Lithium demand versus supply outlook

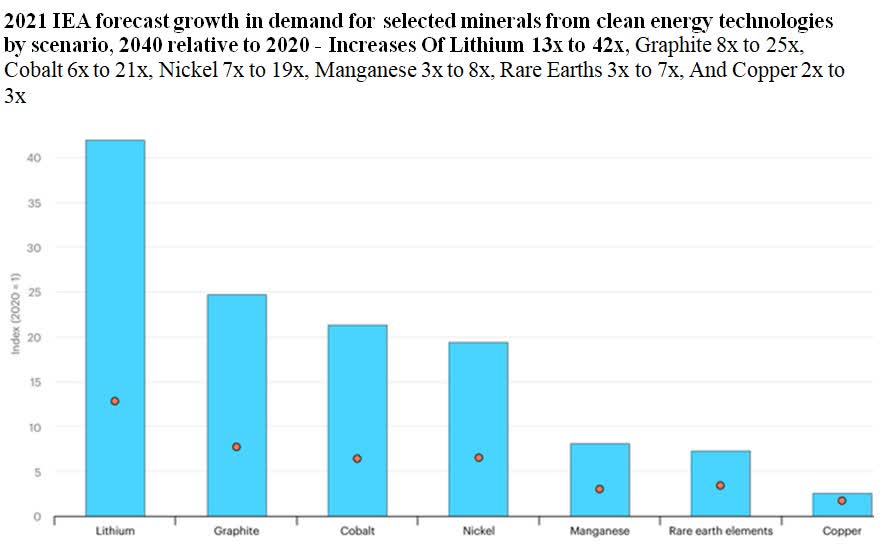

2021 IEA forecast growth in demand for selected minerals from clean energy technologies by scenario, 2040 relative to 2020 – Increases Of Lithium 13x to 42x, Graphite 8x to 25x, Cobalt 6x to 21x, Nickel 7x to 19x, Manganese 3x to 8x, Rare Earths 3x to 7x, and Copper 2x to 3x.

IEA

UBS’s EV metals demand forecast (from Nov. 2020)

UBS

Rio Tinto’s lithium emerging supply gap chart (October 2021)

Rio Tinto

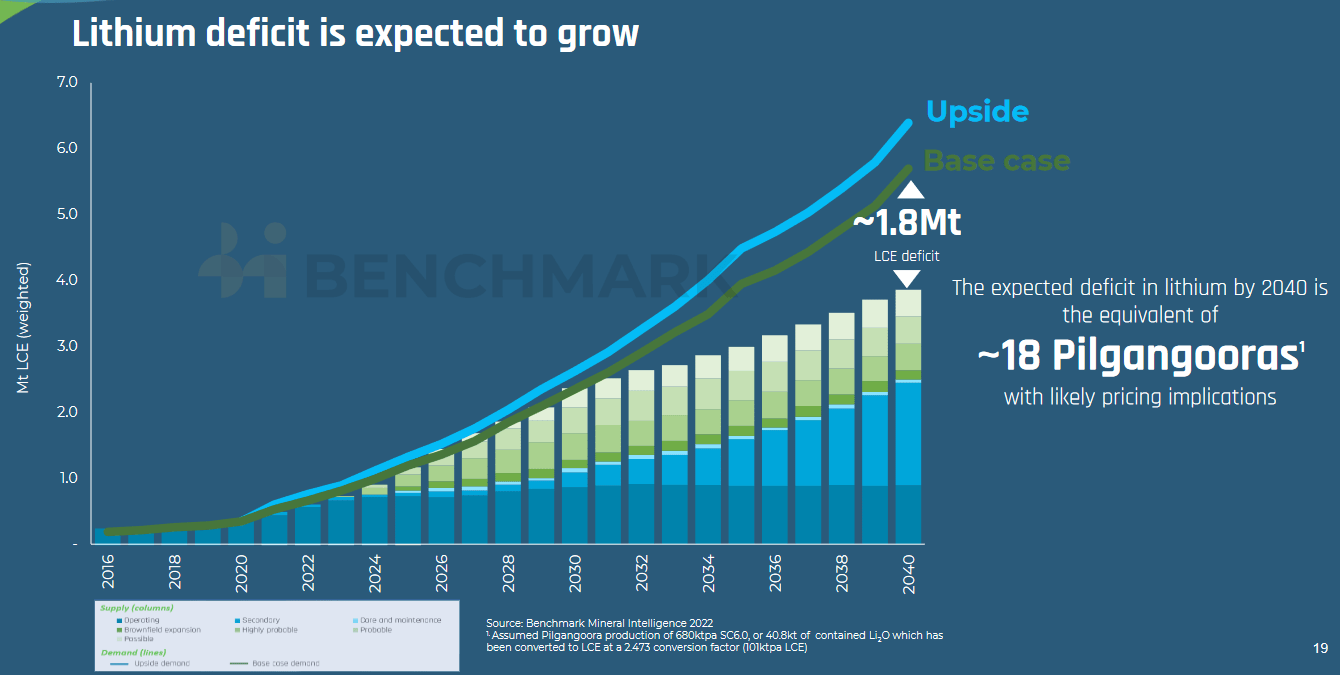

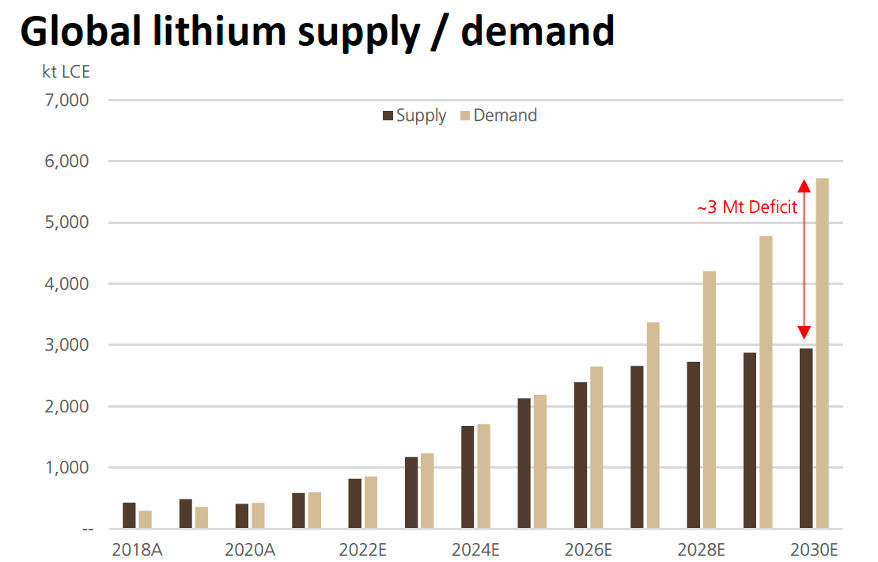

Lithium demand vs. supply forecast by Benchmark Mineral Intelligence (from mid-2022)

BMI

If supply can be rapidly ramped in future years, it can come close to meeting surging demand

BMI

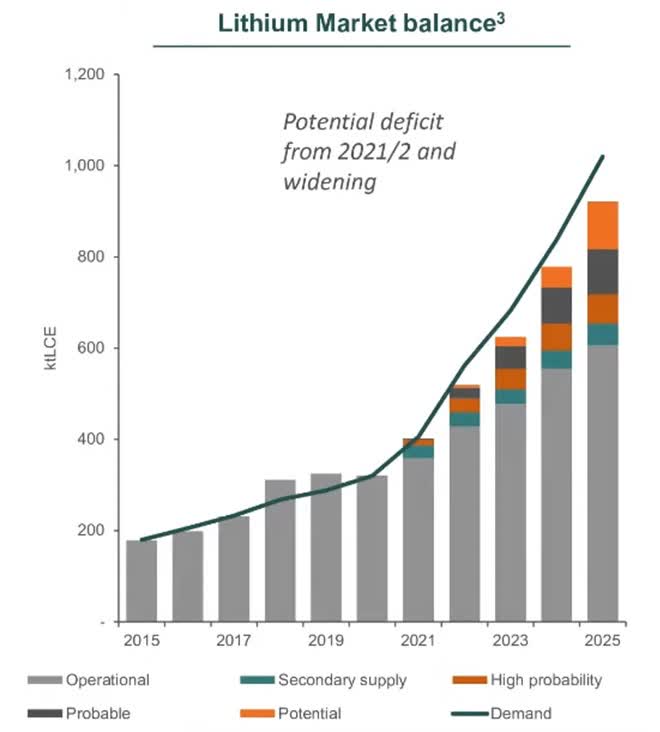

UBS forecasts Year battery metals go into deficit (chart from 2021)

UBS

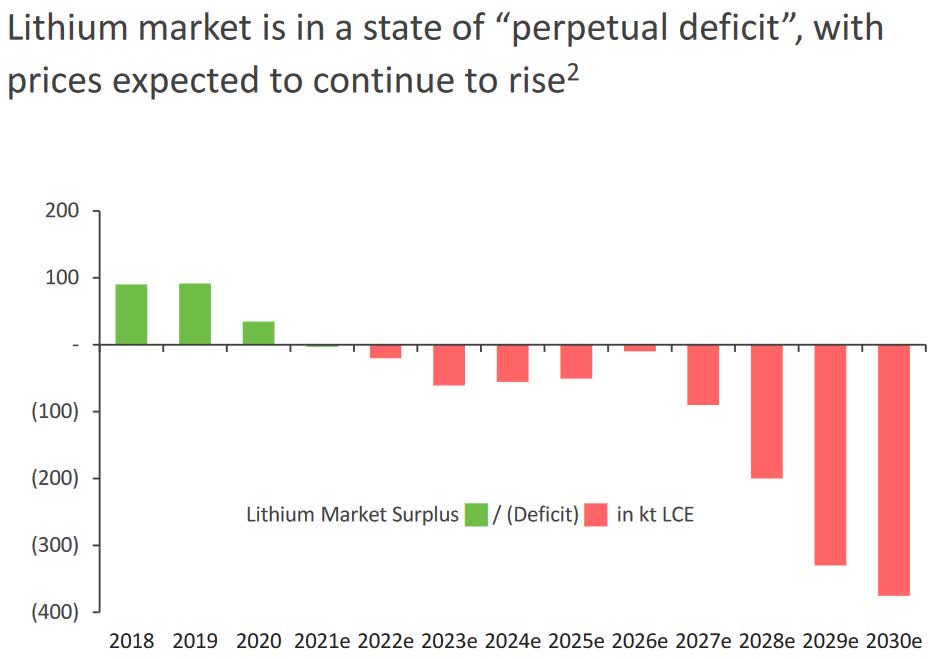

Macquarie’s lithium demand vs. supply forecast (July 2021) – Deficits from 2022 growing bigger from 2027

Macquarie

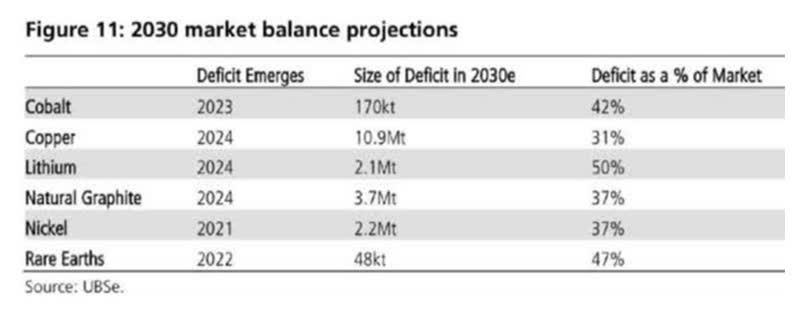

UBS lithium demand vs. supply forecast to 2030

UBS

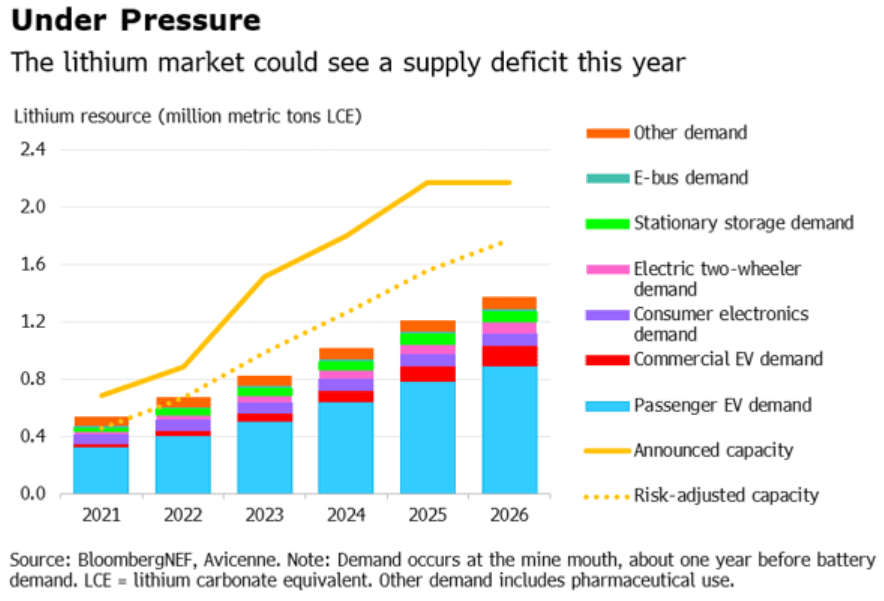

BloombergNEF lithium demand vs. supply forecast (as of mid-2022)

BloombergNEF

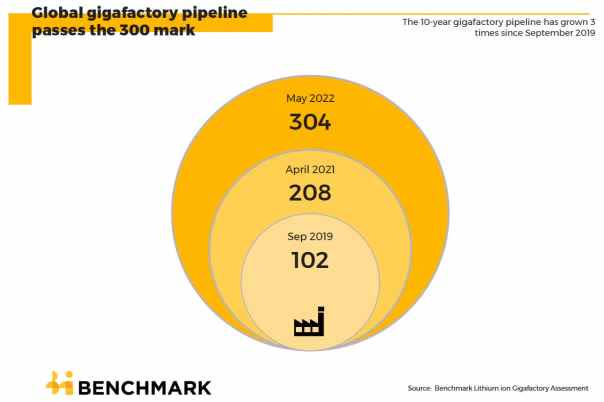

Global lithium-ion battery gigafactory pipeline – now at 304 and 6,387.6 GWh as of May 2022

BMI BMI

BMI forecasts Li-ion battery cell capacity to grow at a CAGR of 47% from 2021 to 2032 (as of mid 2022)

BMI

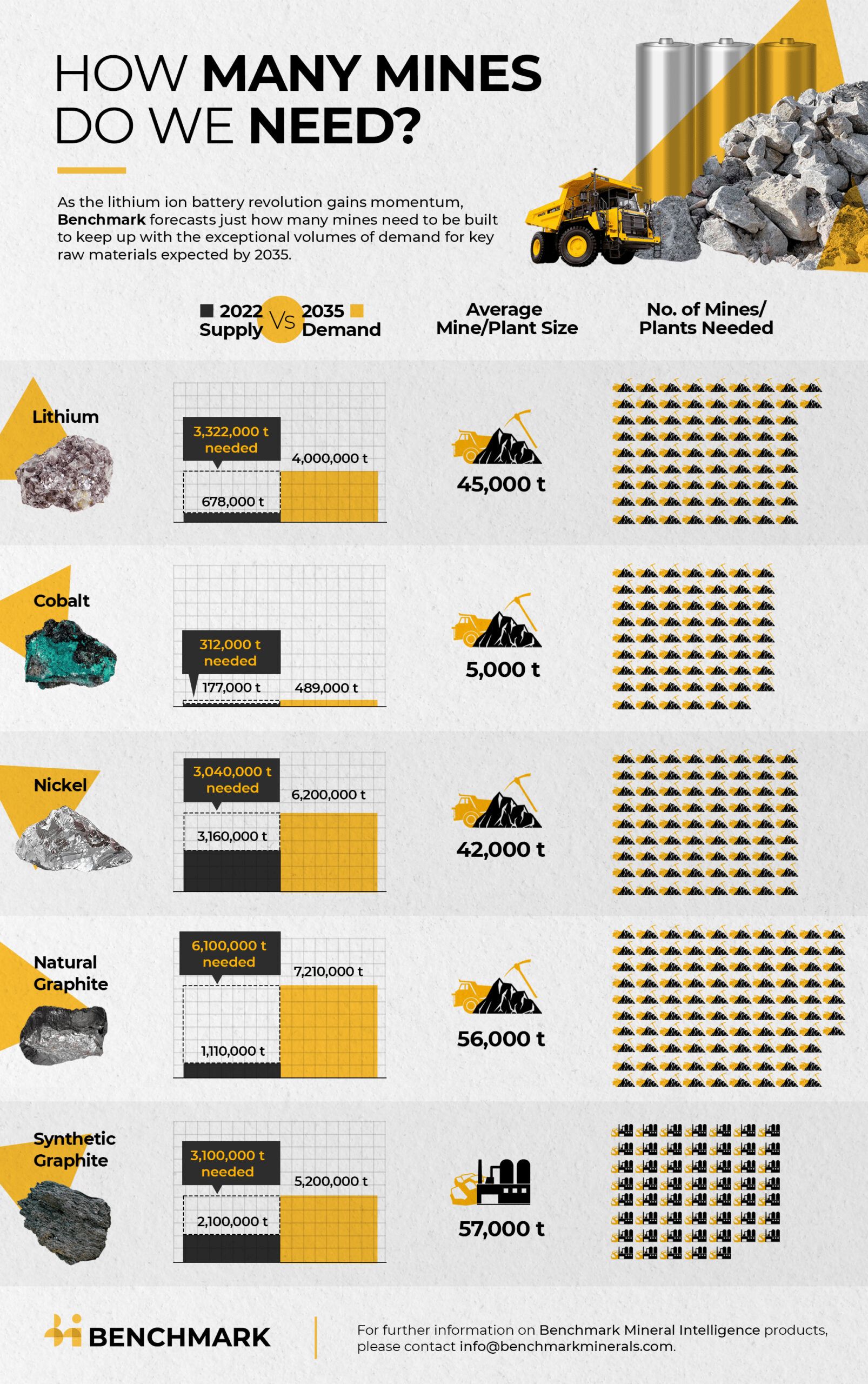

We need 330+ new EV metal mines from 2022 to 2035 to meet surging demand – 74 new 45,000tpa LCE lithium mines (59 if include recycling)

BMI

Lithium market and battery news

On August 16 Electrive reported: “BYD announces plans for lithium mine and battery production in Yichun.”

On August 23 Reuters reported:

VW aims to take stakes in Canadian mines, mine operators – Handelsblatt…”We are not opening any mines of our own, but we want to acquire stakes in Canadian mines and mine operators,” Thomas Schmall told the daily on Tuesday.

On August 25 Mining.com reported:

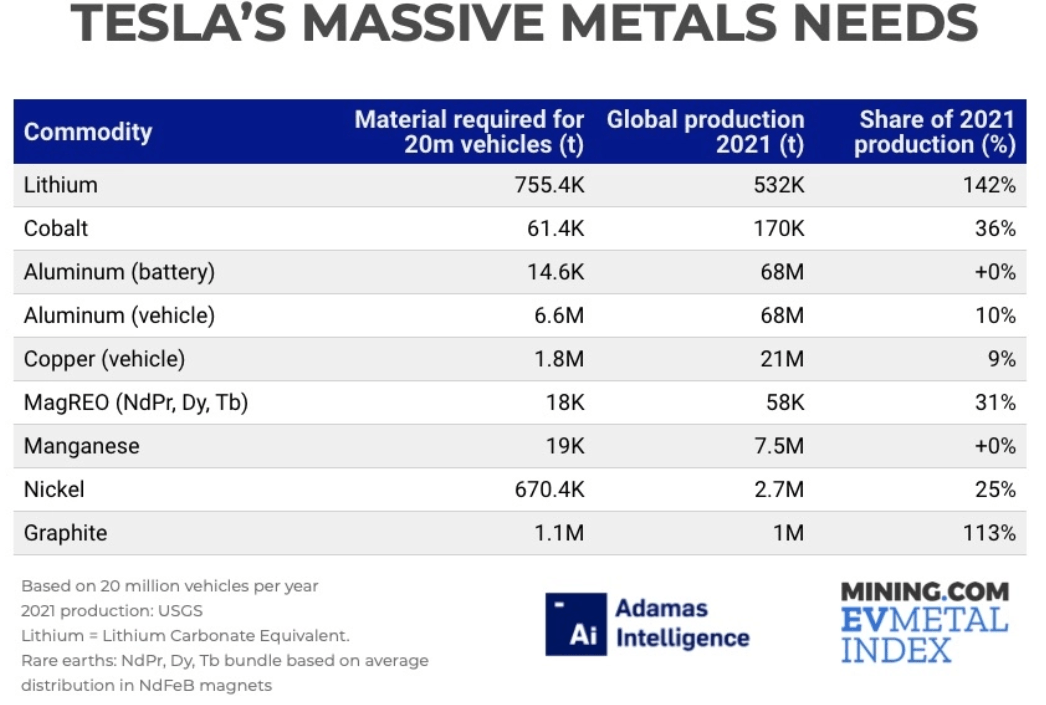

Tesla’s battery metals bill balloons to $100 billion… At today’s price Tesla is on the hook for a bit over $100 billion for the 11.1 million tonnes of raw materials it needs to build 20m cars… As automakers (and the renewable energy sector) scramble for lithium, nickel, cobalt, graphite, rare earths, aluminium, manganese and copper securing supply may ultimately be a bigger issue than costs… To produce 20m vehicles Tesla alone needs more than the total volume of lithium and natural graphite produced last year, almost a third of the magnet rare earths, 36% of the cobalt, and so on.

Note: Bold emphasis by the author.

Lithium and natural graphite are forecast to have the greatest demand increase by Tesla as they move towards producing 20m EVs pa (right column forecasts what would be Tesla’s % increase needed on 2021 ‘total’ global production)

Miningdotcom courtesy Adamas Intelligence

On August 26 Bloomberg reported:

Panasonic in talks for $4 billion battery plant in US: WSJ. Facility would be on top of another plant planned for Kansas. Oklahoma is a likely location for the new plant, although there are no guarantees an agreement will be reached, according to the report. Any new facility would be on top of another $4 billion EV battery factory that Panasonic said in July it plans to build in Kansas…Korean battery makers also have a slew of plans for battery plants in the US, constructing four for General Motors Co., two for Stellantis NV and three for Ford Motor Co.

On August 28 CNBC PRO reported: “UBS upgrades lithium sector as supply struggles to keep pace with demand, favors these stocks.”

On August 31 Benchmark Mineral Intelligence reported:

$15 BILLION US GIGAFACTORY PUSH ACCELERATES NORTH AMERICAN CAPACITY GROWTH. A total of $15 billion could be invested into US gigafactories from announcements in the last two months, enough to build more than the entire current production capacity in the country, according to Benchmark. The announcements from Tesla supplier Panasonic, Honda and LG Energy Solution, as well as Toyota, could result in an additional 157 gigawatt-hours of annual production capacity by mid-decade, including a reported second Panasonic plant in the US, according to Benchmark.

On September 1, Kallanish reported: “Ford urges Biden administration to expedite battery metals mining in US.”

On September 1 Seeking Alpha reported:

Tesla appears to be ramping up interest in manufacturing in Canada. Tesla is continuing to look at potential advanced manufacturing sites in Canada, according to filings related to lobbying activities.

On September 2 ABC news reported:

Port Hedland proposed lithium refinery could reduce exposure to iron ore prices. Plans for a billion-dollar lithium plant for Western Australia’s Pilbara…British chemical company Alkemy Capital Investments has announced plans to build a four-train lithium sulphate (LSM) refinery in Port Hedland…Under the plans, the company would refine 180,000 tonnes of concentrate into lithium sulphate before further processing takes place off shore. Longer term, 720,000 tonnes of spodumene concentrate processed each year at the Port Hedland site would produce 96,000 tonnes of lithium hydroxide – all to supply Europe’s fast-growing electric battery market.

On September 5 Seeking Alpha reported: “Chile’s copper, lithium industries seen winning from constitution rejection.”

On September 5 Mining.com reported:

EV battery maker ProLogium considers UK for $8 billion factory… The solid-state battery startup is evaluating 90 sites across countries including France, Germany, the Netherlands, Poland and the UK…Other locations in the US, China and Southeast Asia are also being contemplated.

On September 6 Benchmark Mineral Intelligence reported:

…More than 300 new mines could need to be built over the next decade to meet the demand for electric vehicle and energy storage batteries, according to a Benchmark forecast. At least 384 new mines for graphite, lithium, nickel and cobalt are required to meet demand by 2035, based on average mine sizes in each industry, according to Benchmark. Taking into account recycling of raw materials, the number is around 336 mines…To meet the world’s lithium requirements would require 74 new lithium mines with an average size of 45,000 tonnes by 2035, according to Benchmark. Including forecast volumes from recycled lithium, however, it’s around 59 mines.

Note: Bold emphasis by the author. See also BMI chart above market news.

On September 14 The European Commission reported:

Critical Raw Materials Act: securing the new gas & oil at the heart of our economy I Blog of Commissioner Thierry Breton. “Lithium and rare earths will soon be more important than oil and gas. Our demand for rare earths alone will increase fivefold by 2030. […] We must avoid becoming dependent again, as we did with oil and gas. […] We will identify strategic projects all along the supply chain, from extraction to refining, from processing to recycling. And we will build up strategic reserves where supply is at risk. This is why today I am announcing a European Critical Raw Materials Act.”…To frame the ambition, objectives could be introduced in the legislation. For example, a target could be set that at least 30% of the EU’s demand for refined lithium should originate from the EU by 2030, or to recover at least 20% of the rare earth elements present in relevant waste streams by 2030…

- Jan. 2022 Trend Investing article – “European Junior Lithium Miners To Consider.“

On September 20 Financial Times reported:

Europe lags China in race for electric car supply chain. Lithium from hard rock for batteries and rare earths for magnets and motors underscore main Asian competitor’s dominance.

On September 21 Seeking Alpha reported:

FREYR Battery jumps to post-SPAC high after Morgan Stanley points to huge upside…Morgan Stanley called the electric vehicle stock its top overall sector pick…Morgan Stanley updated estimates on FREY and boosted the price target to $26 from $18. The bull case price target was hiked to $60 from $34.

Lithium miner news

Albemarle (NYSE:ALB)

On August 29, Albemarle announced: “Albemarle concludes strategic review of catalysts business.”

On August 30, Albemarle announced: “Albemarle announces new global business unit alignment.” Highlights include:

Albemarle’s two core global business units will become:

- “Albemarle Specialties: This GBU will include the current Bromine business as well as the Lithium Specialties business in the current Lithium business…

- Albemarle Energy Storage: This GBU will include the Hydroxide, Carbonate, Battery Grade Metal, and Advanced Energy Storage businesses in the current Lithium business…”

Upcoming catalysts:

- Q3 2022 – Wodgina Lithium Mine (60% ALB: 40% MIN) Train 2 restart. Note the non-binding agreement will (if completes) move Wodgina to a 50% ALB: 50% MIN JV.

NB: The Greenbushes Mine in WA is owned by Albemarle 49%, Tianqi Lithium Corporation ~25%, and IGO Limited ~25%. Wodgina Lithium Mine is a JV (50% ALB: 50% MIN). Kemerton Lithium Hydroxide Plant is a JV (60% ALB: 40% MIN).

Kemerton Lithium Hydroxide Plant (60% ALB: 40% MIN) in WA

Albemarle Albemarle

Sociedad Quimica y Minera S.A. (NYSE:SQM), Wesfarmers [ASX:WES] (OTCPK:WFAFY), Covalent Lithium (SQM/WES JV)

On August 29 The West Australian reported:

Wesfarmers looking ‘far and wide’ for new battery minerals investments…Wesfarmers and its Chilean partner SQM are looking to begin production of value-adding lithium hydroxide from a new plant being built within the WA’s large chemicals production complex at Kwinana in the second half of 2024. However, the duo’s Covalent Lithium joint venture is now planning to take advantage of elevated prices for spodumene concentrate by selling that product into the market as soon as the Mt Holland mine, near Southern Cross, is finished rather than wait for the completion of the Kwinana plant. The mine concentrator is now more than 40 per cent complete, with most of the civil works for the refinery near completed.

Upcoming catalysts:

? late 2023/early 2024 – Mt Holland plans to start ‘spodumene’ production and sales early.

H2 2024 – Mt. Holland production to begin (SQM/Wesfarmers JV) as well as their lithium hydroxide [LiOH] refinery.

Investors can read SQM’s latest presentation here or the latest Trend Investing article on SQM here.

Jiangxi Ganfeng Lithium [SHE:002460] [HK: 1772] (OTC:GNENF) (OTCPK:GNENY)

On September 2, aastocks reported:

Ganfeng Lithium mulls to partner with Fulin precision on integrated lithium dihydrogen phosphate project. Ganfeng Lithium announced that it had recently inked a “project investment cooperation agreement” with Mianyang Fulin Precision Co., Ltd., pursuant to which the two parties will jointly invest in a joint venture company to develop an integrated lithium dihydrogen phosphate project which has an annual production output of 200,000 tonnes.

On September 19, Jangxi Ganfeng Lithium announced: “Financial statements/ESG Information – [Interim/Half-Year Report].”

Investors can read the latest Trend Investing article on Ganfeng Lithium here.

(Chengdu) Tianqi Lithium Industries Inc. [SHE:002466], Tianqi Lithium Energy Australia (TLEA) is a JV with Tianqi Lithium (51%) and IGO Limited (49%). TLEA owns the Kwinana lithium hydroxide facility in WA

On August 26, Market Screener reported:

Tianqi Lithium Corporation reports earnings results for the half year ended June 30, 2022…For the half year, the company reported sales was CNY 14,295.57 million compared to CNY 2,351.04 million a year ago. Net income was CNY 10,327.59 million compared to CNY 85.8 million a year ago.

On August 30, Market Screener reported:

Tianqi Lithium Corporation announces an equity buyback for CNY 200 million worth of its shares. Tianqi Lithium Corporation (SZSE:002466) announces a share repurchase program. Under the program, the company will repurchase up to CNY 200 million worth of class A shares. The shares will be repurchased at a price of not more than CNY 150 per share.

On August 31, Market Screener reported: “Tianqi Lithium swings to profit as revenue surges six-fold; Shares down 3% in Shenzhen.”

On September 19, Market Screener reported: “Tianqi Lithium Corporation (XSEC:002466) added to FTSE All-World Index.”

You can watch a good Tainqi Lithium CEO video interview here, where he discusses lithium market demand and supply issues.

Kwinana lithium refinery JV (51% Tianqi: 49% IGO) in Western Australia

IGO Limited

Pilbara Minerals [ASX:PLS] (OTC:PILBF)

On September 20, Pilbara Minerals announced:

Results of the 9th BMX auction. Implied price of us$7,708/dmt (SC6.0, CIF China). Pilbara Minerals Limited (“Pilbara Minerals” or the “Company”: ASX: PLS) is pleased to announce the results of its latest spodumene concentrate auction, held via its digital Battery Material Exchange (“BMX”) platform, earlier this afternoon. A cargo of 5,000dmt at a target grade of ~5.5% lithia was presented for sale on the digital platform, with delivery expected from mid October 2022.

Upcoming catalysts:

Late 2023 – Plan to commission production of POSCO/Pilbara Minerals (18%, option to increase to 30%) JV LiOH facility in Korea.

Mineral Resources [ASX:MIN] (OTCPK:MALRF)

Mt Marion Mine (50% MIN: 50% Ganfeng). Wodgina Lithium Mine (60% ALB: 40% MIN) restarted in mid-2022. (Note the non-binding agreement will (if completes) move Wodgina to a 50% ALB: 50% MIN JV). The 50ktpa Kemerton Lithium Hydroxide refinery (60% ALB: 40% MIN) is due for first sales in H2, 2022.

On August 29, Mineral Resources announced: “FY22 full year result.” Highlights include:

Fy22 Underlying Profit and Loss:

- “Revenue of $3.4bn down 8% on pcp and Underlying EBITDA of $1.0bn down 46% on pcp.

- FY22 Revenue and Underlying EBITDA driven by: Record iron ore exports offset by lower realised prices. Higher lithium prices and initial lithium hydroxide earnings. Record Mining Services volumes. Costs maintained within guidance despite significant pressure.

- Depreciation and amortisation increased due to higher production across Mining Services, Iron Ore and Lithium.”

FY22 Cash Flow:

- “Working capital reflects first time impacts of Wodgina spodumene sales and lithium hydroxide sales from Mt Marion. Lithium price increase over the period also impacts receivables balance.

- Timing on lithium hydroxide reflective of tolling agreement and while there may be some ongoing fluctuation, lithia recoveries are not in question.

- Tax paid of $203M of which $159M relates to FY21.

- Capex of $800M in FY22.

- Dividends paid of $324M following a record FY21 result.

- Investments and acquisitions primarily comprise of $200M of RHIOJV tenements acquired for the Onslow Iron project.

- Divestment of Pilbara Minerals (ASX: PLS) shareholding, net of $65M tax paid.

- Net change in borrowings reflect proceeds from completion of US$1.25bn Senior Unsecured Notes Offering in FY22.”

FY22 Capex of $800M includes:

- “Lithium growth capex on the restart and ramp up of 2 trains at Wodgina.”

FY22 Summary Balance Sheet:

- “Closing cash of $2.4bn and borrowings of $3.1bn, reflecting completion of US$1.25bn Notes offering in March 2022…”

On August 31, Mineral Resources announced:

MinRes’ Vision to power up in WA. MinRes has announced plans to further support the world’s renewable energy future by becoming Australia’s first battery cell manufacturer…

On September 8, the AFR reported:

MinRes mulls mega lithium spin-off, JPMorgan digs up structures. Australian miner Mineral Resources is considering spinning off and listing its growing lithium arm in the United States, in a bid to create billions of dollars of value for investors.

On September 12, Mineral Resources announced: “Initial results from Norseman Lithium JV.” Highlights include:

The drilling has confirmed the presence of lithium bearing pegmatites with significant results returned including:

- “9 m @ 1.26% Li₂O and 151ppm Ta₂O₅ from 30 m.

- 8 m @ 1.10% Li₂O and 118 ppm Ta₂O₅ from 53 m…”

On September 15, Mineral Resources announced: “Mineral Resources Limited increases GL1 shareholding…”

Investors can read the latest Trend Investing article on Mineral Resources here.

Livent Corp. (LTHM)[GR:8LV]

No news for the month.

You can read the Trend Investing Livent article here when Livent was trading at US$7.26.

Allkem [ASX:AKE] [TSX:AKE] (OTCPK:OROCF)(formerly Orocobre)

No news for the month.

Upcoming catalysts include:

- Early Q4, 2022 – Naraha lithium hydroxide plant (10ktpa) commissioning (ORE share is 75%) has completed, first production expected in early Q4.

- Late 2022 – Olaroz Stage 2 expansion commissioning followed by a 2 year ramp to 25ktpa. When combined with Stage 1 total capacity will be 42.5ktpa.

- H2 2023 – Sal De Vida Stage 1 production targeted to begin and ramp to 15ktpa. SDV Stage 2&3 combined will begin about 2025 and ramp to an additional 30ktpa. Total combined when completed will be 45ktpa.

You can read the latest investor presentation here. You can read the latest Trend Investing Allkem article here.

AMG Advanced Metallurgical Group NV [NA:AMG] [GR:ADG] (OTCPK:AMVMF)

On September 6, AMG announced:

AMG Lithium signs binding multiyear agreement to supply battery-grade lithium hydroxide with EcoPro, the Holding Company of cathode materials manufacturer EcoPro BM. Under the Agreement, AMG Lithium will deliver a minimum of 5,000 tonnes per annum (“tpa”) of battery-grade lithium hydroxide to EcoPro BM’s cathode materials production plant in Debrecen, Hungary. The contract includes an option for additional volumes. Initial quantities for qualification purposes are scheduled to be delivered in late 2023 – with regular quantities to follow in 2024…

Upcoming catalysts:

- Q4, 2022 – Lithium-vanadium battery (“LIVA”) for the energy storage market to be ready.

- End Q4, 2022 – New vanadium spent catalyst recycling facility in Zanesville, Ohio to be commissioned.

- Q2, 2023 – Stage 2 production at Mibra Lithium-Tantalum mine (additional 40ktpa) forecast to begin, bringing total production capacity to 130ktpa.

- Q3, 2023 – Lithium hydroxide facility in Bitterfeld-Wolfen Germany to be commissioned. First module to be 20,000tpa LiOH.

- 2023 – Saudi Arabia vanadium Projects JV with Shell & Aramco.

- 2025-2028 – German LiOH facility expansion with Modules 2-5 (100,00tpa LiOH.

You can view the latest company presentation here or the very recent Trend Investing article here.

Lithium Americas [TSX:LAC] (LAC)

On September 20, Lithium Americas announced: “Lithium Americas enters strategic collaboration agreement with Green Technology Metals.” Highlights include:

- “Collaboration Agreement executed with GT1, a North American focused lithium exploration and development company with hard rock spodumene assets in north-west Ontario, Canada.

- Builds upon Lithium Americas’ previous strategic equity investment in GT1 of US$10 million and established collaboration framework.

- Provides non-exclusive rights to undertake collaborative activities between the two parties.

- Establishes a Strategic Management Committee for further joint exploration and development opportunities with focus on Canada and the U.S.”

Upcoming catalysts:

- H2 2022 – Thacker Pass FS and early construction works planned to commence.

- H2 2022 – Cauchari-Olaroz lithium production to commence and ramp to 40ktpa. From 2025 a Stage 2 20ktpa+ expansion is planned.

- 2023 – Possible lithium clay producer from Thacker Pass Nevada (full ramp by 2026).

NB: Ganfeng Lithium (51%) and Lithium Americas (49%) own the JV company Minera Exar S.A., which owns 91.5% interest and is entitled to 100% of the production from the Cauchari-Olaroz Project. The 8.5% interest is owned by Jujuy Energia y Mineria Sociedad del Estado (“JEMSE”) (a company owned by the Government of Jujuy province).

Argosy Minerals [ASX:AGY][GR:AM1] (OTCPK:ARYMF)

Argosy has an interest in the Rincon Lithium Project in Argentina, targeting a fast-track development strategy. Argosy is now producing at a small scale and ramping to 2,000tpa lithium carbonate starting June 2022.

On September 1, Argosy Minerals announced: “Rincon 2,000tpa Li2CO3 operational update.” Highlights include:

- “95% of total development works now complete – first battery quality Li2CO3 product targeted during next month.

- Commercial lithium carbonate production operations scheduled during next quarter…

- The Company remains on budget and is targeting to achieve first battery quality lithium carbonate product next month.”

On September 2, Argosy Minerals announced: “S&P Dow Jones Indices announces September 2022 quarterly rebalance of the S&P/ASX Indices.” Argosy joined the ASX300.

On September 8, Argosy Minerals announced: “Interim financial report for the half-year ended 30 June 2022.”

On September 23 Listcorp reported:

Positive drilling progress at Rincon Lithium Project… The Company is encouraged with the extended depths of the production well drilling and lithium brine pumping test works conducted to date, which may enhance the outcomes and provide scope for improved results for the next stage estimation and feasibility works.

Upcoming catalysts:

- Oct. 2022 – Rincon Lithium Project commissioning.

Investors can view the company’s latest investor presentation here, and the latest Trend Investing Argosy Minerals article here.

Core Lithium Ltd. [ASX:CXO] [GR:7CX] (OTC:CORX)(OTCPK:CXOXF)

Core 100% own the Finniss Lithium Project (Grants Resource) in Northern Territory Australia. Significantly they already have an off-take partner with China’s Yahua (large market cap, large lithium producer), who has signed a supply deal with Tesla (TSLA). The Company states they have a “high potential for additional resources from 500km2 covering 100s of pegmatites.” Fully funded and starting mining with a planned Q4 2022 production start.

On August 29, Core Lithium announced:

Core and Tesla extend Offtake Term Sheet Australia’s next lithium producer, Core Lithium Ltd (Core or Company) (ASX: CXO), advises that is has mutually agreed with Tesla, Inc. (“Tesla”) to extend the termination date for its binding offtake term sheet (“Offtake Term Sheet”) with Tesla to 26 October 2022. The extension allows Core and Tesla to complete negotiations for the definitive full form binding offtake agreement. The Offtake Term Sheet with electric vehicle manufacturer Tesla is for the supply of up to 110,000 dry metric tonnes of lithium spodumene concentrate produced at Core’s Finnis Lithium Project expected to commence in 2023 (refer to ASX Announcement 2 March 2022).

Investors can read a company presentation here, or the Trend Investing article when Core Lithium was back at A$0.055 here.

Catalysts include:

- Late 2022 – Lithium spodumene production at Finniss targeted to begin.

Sigma Lithium Resources [TSXV:SGML](SGMLF) (SGML)

Sigma is developing a world-class lithium hard rock deposit with exceptional mineralogy at its Grota do Cirilo Project in Brazil.

No significant news for the month.

Catalysts include:

- Late 2022 – Production targeted to begin at the Grota do Cirilo Project in Brazil and ramp to 531,000tpa spodumene (Stage 1 and 2 combined).

Investors can read the latest company presentation here or the Trend Investing article here back when Sigma was trading at C$5.00.

Lithium miner ETFs

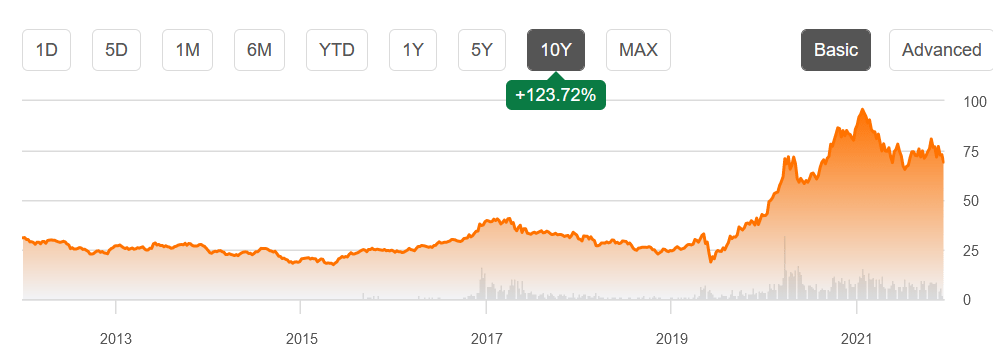

Global X Lithium & Battery Tech ETF (NYSEARCA:LIT) – Price = US$69.13

The LIT fund was down significantly in September. The current P/E is 18.04.

Our model forecast is for lithium demand to increase 5.3x between end 2020 and end 2025 to ~1.8m tpa, and 13x this decade to reach ~4.5 m tpa by end 2029 (assumes electric car market share of 32% by end 2025 and 70% by end 2029).

Note: A Nov. 2020 UBS forecast is for “lithium demand to lift 11-fold from ~400kt in 2021 through to 2030.”

Global X Lithium & Battery Tech ETF 10-year price chart

Seeking Alpha

The Amplify Lithium & Battery Technology ETF (BATT)

BATT is currently on a P/E of 12.62. It is a well diversified fund. On their website they state: “BATT is a portfolio of companies generating significant revenue from the development, production and use of lithium battery technology, including: 1) battery storage solutions, 2) battery metals & materials, and 3) electric vehicles. BATT seeks investment results that correspond generally to the EQM Lithium & Battery Technology Index (BATTIDX).”

Conclusion

September saw record lithium prices.

Highlights for the month were:

- Lithium resumes insane gains to add pressure on automakers. Lithium carbonate jumped to a new record Friday of 500,500 yuan ($71,315) a ton.

- Adamas Intelligence: Lithium and natural graphite are forecast to have the greatest demand increase by Tesla as they move towards producing 20m EVs pa.

- Panasonic in talks for $4 billion battery plant in US.

- VW aims to take stakes in Canadian mines, mine operators.

- UBS upgrades lithium sector as supply struggles to keep pace with demand.

- BMI: US$15B U.S. gigafactory push accelerates North America capacity growth.

- British chemical company Alkemy Capital Investments has announced plans to build a four-train lithium sulphate (LSM) refinery in Port Hedland, WA.

- Tesla appears to be ramping up interest in manufacturing in Canada.

- Chile’s copper, lithium industries seen winning from constitution rejection.

- BMI – More than 300 new mines could need to be built over the next decade to meet the demand for EVs and energy storage batteries. We need 74 new 45,000tpa LCE lithium mines (59 if include recycling) by 2035.

- European Commission – Critical Raw Materials Act – “Lithium and rare earths will soon be more important than oil and gas.”

- FREYR Battery (FREY) jumps to post-SPAC high after Morgan Stanley points to huge upside. Boosts the price target to $26 from $18.

- Covalent Lithium (SQM/Wesfarmers JV at Mt Holland) plans to start ‘spodumene’ production and sales early to take advantage of strong prices.

- Ganfeng Lithium mulls to partner with Fulin precision on integrated lithium dihydrogen phosphate project. (A precursor for LFP batteries)

- Tianqi Lithium net income surges to CNY 10,327.59m from CNY 85.8m a year ago. Announces an equity buyback worth CNY 200m.

- Pilbara Minerals achieves a record spodumene spot price in September at their BMX Auction. Implied price of US$7,708/dmt (SC6.0, CIF China).

- Mineral Resources plans to become Australia’s first battery cell manufacturer. Mulls mega lithium spin-off with a USA listing.

- AMG Lithium signs binding multiyear agreement to supply battery-grade lithium hydroxide with EcoPro.

- Argosy Minerals Rincon Lithium Project – 95% of total development works now complete. Targeting to achieve first battery quality lithium carbonate product next month (October).

- Core and Tesla extend Offtake Term Sheet Australia’s next lithium producer.

As usual all comments are welcome.

Be the first to comment