kynny

General Overview

Lithium’s importance in the development of a growing battery electric vehicle industry is key. As governments jump on the green energy bandwagon, pledging notable changes in energy consumption and a safeguarding of the environment, mineral resource output has become critical.

So much so that Chinese lithium chemical producers, such as world class Gangfeng Lithium, have been scouring the world looking for new sources of supply.

It’s the story of Leo Lithium (OTCPK:LLLAF) which is a marriage of cash and technical nous between Australian miners and Chinese financiers. Its prolific Mali based Goulamina project a few hours South of capital Bamako promises secured supply for several years to come.

Accordingly, its deep pocketed Chinese backers have secured offtake agreements, port capacity and logistics firepower to get battery minerals from the Mali bush to Chinese industrial hubs in a bid to quench an unwavering thirst for electric vehicles.

My outlook for Leo Lithium remains bullish. Notwithstanding, close scrutiny of lithium prices and trends in BEV sales needs monitoring, particularly as the global economy moves into recession.

Trading Economics

Despite a post SARS-Cov2 lithium boom, prices have tended to moderate as the impact of an oncoming global recession and a cooling of BEV automotive sales have arisen.

Lithium carbonate prices have moderated to CNY 485K/t at the start of the year, the lowest level since mid-2022. That is 20% off the all-time high of CNY 600K/t hit in November on boosted supply and signs of dwindling demand.

Capacity improvements boosted Chinese domestic production by 89% year-on-year despite some output cuts. A ~30% increase in capacity is forecast which, coupled with a decline in electric vehicle sales in China, may see a cooling of prices.

Company Introduction

Leo Lithium is a pure play Chinese backed lithium firm presently developing the world class Goulamina lithium project in Mali. The company will be West Africa’s first mover in spodumene production when the project comes online in 2024, supplying the booming lithium-ion battery industry. Leo Lithium is dual listed on both the Australian stock exchange and Frankfurt stock exchange.

Leo Lithium

Goulamina is a prolific lithium play touting >100 Mt of mineral resources.

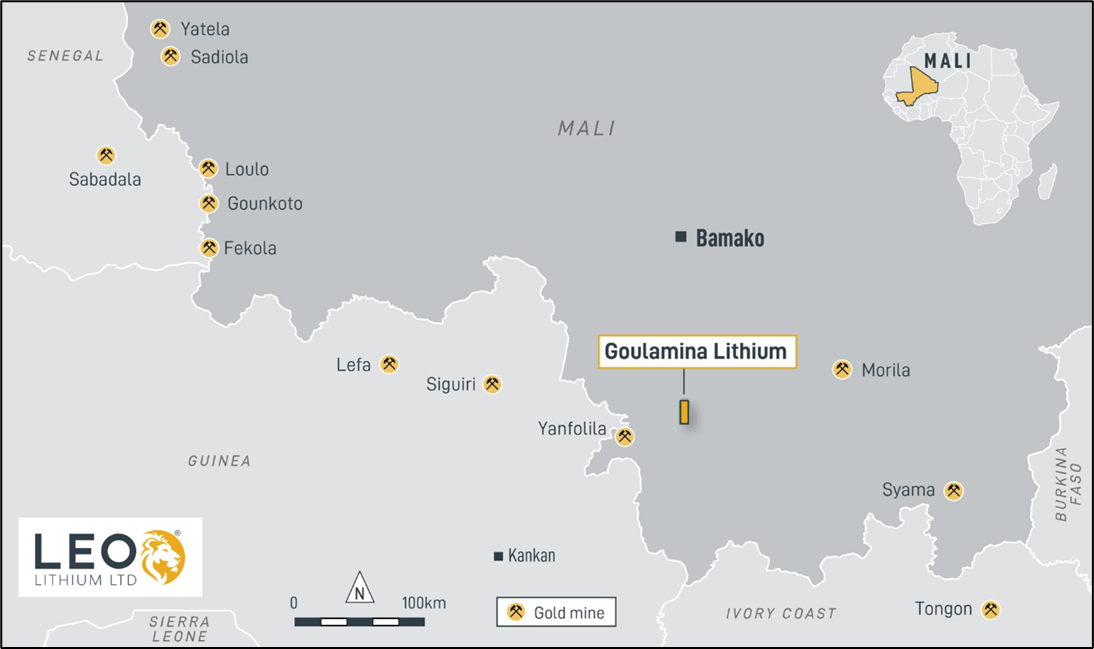

Goulamina Project

The Goulamina Project is a first-class prolific West African lithium play. Its mission to become West Africa’s first spodumene producer is a tribute to the resources and funding thrown at the project to bring it online in 2024. It will supply the automotive industry’s unabated thirst for lithium-ion batteries.

Direct shipping ore will provide project cash flow fast-tracking, as several production milestones are navigated. The open pit ore reserve estimate for proven mineral resource is 8.1Mt at 1.55% Li2O. Probable reserve range is an additional 44Mt. All in, the project has 785k contained tons of Li2O.

Leo Lithium

The Goulamina Lithium Project lies a few hours drive from Bamako, outside the provincial town of Bougouni.

Drilling results demonstrate an increased level of confidence in the scale and potential of the Goulamina resource. The Danaya domain has predominantly been completed, with further high-grade pegmatite intercepts being detected.

The North Eastern Domain has seen roughly 80% of its drilling program completed. Additional drilling operations will be completed into 2023. In summary, an updated mineral resource estimate for Danaya is penned in for early 2023 with a comprehensive update for the entire project a little later.

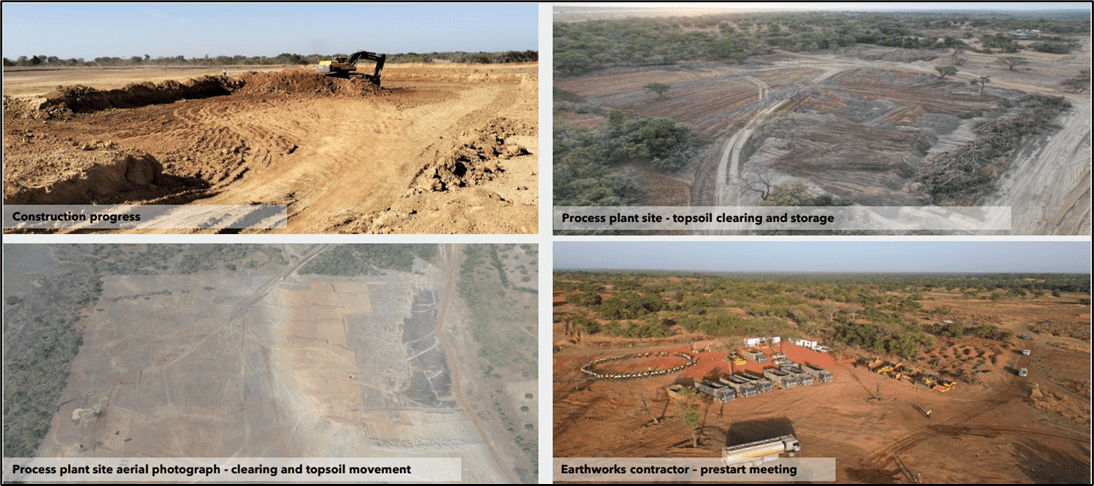

The project remains on schedule – 48% of scheduled activities have been completed. Procurement activities have been realized and approximately 30% of project expenditure has now been committed to.

Long lead time items such as the ball mill are due for delivery early 2023 while civil works take place. 200 staff and contractors have been mobilized and bulk earthworks packages are in process of being completed. The concrete batch plant is the next item on the project critical path. Overall, the project remains within budget.

Leo Lithium

Project construction is progressing well as the mine prepares for first spodumene in 2024.

Naturally production output will be staged. Stage 1 production targets include 2.3Mtpa of ore throughput to produce Spodumene concentrate of 506Ktpa. Capital expenditure will total about US $255M for phase 1. Stage 2 will witness an increase in output to 4.0Mtpa. This phase will also see more than a 50% increase in capacity, to 831Ktpa and capital expenditure of approximately US $70M.

Fast track shipments of export spodumene before full completion of the plant are being considered, with Chinese JV partner Ganfeng supportive of the idea and the Mali government presently under consultation. This provides the advantage of early revenue generation, proof testing project logistics capabilities, and improving project treasury. Presently 2 shipments of 30Kmt each are being considered of ore graded at 1.2% to 1.5% of Li2O likely.

Project financing has been derived from multiple sources – The US $255M capex pre-production is being bank rolled with a mix of debt and equity. US $130M in equity funding from Chinese JV partner Gangfeng will be drawn down initially. Following this, US $40M of Gangfeng debt will be accessed. Leo Lithium will subsequently fund US $43M of the remainder from corporate cash with Gangfeng matching the amount.

Direct shipping ore provides an option to fast-track cash inflows with indicative financials of US $260-$300/t FOB Abidjan. Sea freight costs to China will be circa US $47.50/wmt China main port.

Project Transport & Logistics

Transport & logistics will be critical to project success and presents a critical risk factor. A 10-year agreement has been secured at Abidjan, Cote d’Ivoire for a minimum 250Ktpa concentrate storage and export.

A secondary shipping option is now being studied with either Dakar, Senegal or San Pedro, Cote d’Ivoire being likely contenders. 3rd party truck and logistics port contractors will be used minimizing capex for Leo Lithium.

Leo Lithium

With the project being developed in landlocked Mali, best-in-class logistics are critical to success.

Key Financials

The project has Chinese backers with deep pockets. Gangfeng Lithium is one of the world’s largest lithium chemicals producers and is ploughing hundreds of millions of dollars in debt and equity to secure spodumene supplies for its Chinese chemical plants.

100% of stage 1 offtake will find its way to Gangfeng lithium processing plants in China with pricing based on lithium chemicals, spot and quarterly prices. 50% of stage 2 offtake has also been secured by Gangfeng. Leo Lithium is currently engaging 3rd parties to market the remaining capacity.

As the company is in pre-stages of its project, there is not a lot to show on the income statement. The balance sheet, however, is another story. The company holds ~ $59.3M in cash and marketable securities deployable to finance project funding needs. $72.4M in long term investments linked to Goulamina has been committed to. US $69.1M in issuance of common stock over the last 12 months has been a major source of financing.

Risk Factors

Despite presenting some compelling project characteristics, the Goulamina project is not without risk. Mali remains a country reputed for widespread political instability, military coups, and violence. While Bougouni is some ways away from conflict areas in the North, it cannot be discounted that the political environment impact project schedules.

China’s heavy involvement in the project provides additional risk, particularly if geo-political tensions between the West and China escalated. The shuttering of Russian business following the onset of the conflict in Ukraine provide some indications of what possibly could come, should similar sanctions face China.

Firefinch’s 17.6% holding in the firm is also worth noting. Its failed Morila gold play in Mali has left the company reeling and looking for sources of cash. Despite being downplayed by Leo Lithium management, a fire sale of the 17.6% holding to raise funds could put significant pressure on the stock price.

Lithium prices are evolving too. It’s the perfect storm, a lagging but ever-growing amount of capacity coming online at a time when consumer discretionary and specifically the global automotive industry is starting to roll over.

Tesla (TSLA) has started to offer discounts in numerous countries as it struggles to maintain its growth engine. All in, this provides for telling times for the industry and perhaps signs of lasting change.

Key Takeaways

For investors looking for exposure to the growing BEV industry, Leo Lithium makes for an interesting pitch. It shows promise of being West Africa’s pioneering battery minerals play. With plentiful reserves, wealthy Chinese backers, and Australian technical nous, it’s geared to fuel the Chinese battery chemical industry into the next decade.

Only a sapping of demand, Mali political unrest, Chinese economic sanctions, a tanking of lithium prices or complicated logistics issues could possibly throw a spanner in the works.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Be the first to comment