Brankospejs/iStock via Getty Images

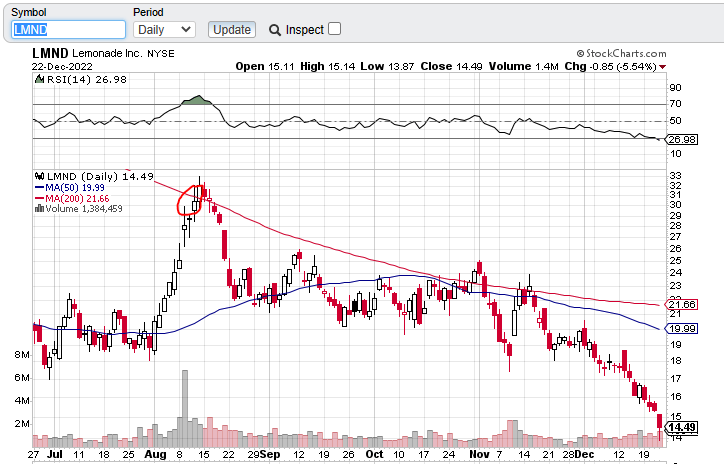

When we last covered Lemonade, Inc. (NYSE:LMND), we gave it a Sell rating as the stock was perfectly setup to get clobbered. A “Sell” is the equivalent of a “Short Sell” to us. While we pan a wide variety of stocks and those are easy to find in this market, a “Sell” is only given when we think the stock has good, immediate downside. It has to marry bad fundamentals with overbought technicals. In other words, the crowd has to be chasing the company with poor fundamentals. That is exactly the setup we had on Lemonade in early August as the company outlined a plan for profitability. The short squeeze had driven the company back to the 200-day moving average, and we saw it as a good opportunity to push the Sell call.

Stock Charts

With the stock down almost 50%, three things have changed, and that gets us to our upgrade reason today.

Reason 1:

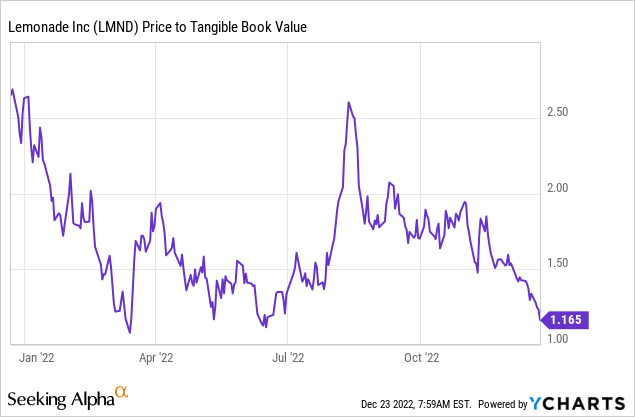

Insurance stocks are always a tangible book value story first. What we mean by that is all valuation starts off at how much tangible equity is available for every shareholder. Mind you, this is not the same as saying “It has X amount of net cash, and it is a fast-growing company”. No. That is about the silliest statement you can make about an insurance company. All companies in this sector need that tangible equity to write policies off of it. It is the backing to pay insurance or reinsurance claims. Most of them have very low leverage as the policy writing is the real leverage risk. That said, a stock near tangible equity is a better value than one trading higher.

Lemonade’s stock price has now moved very close to its tangible book value per share.

So at a 20,000-foot level, conventional metrics finally support the price around this level. This of course is very little comfort to people who got swept in the hype and bought it at $185, but Ce La Vie.

Reason 2:

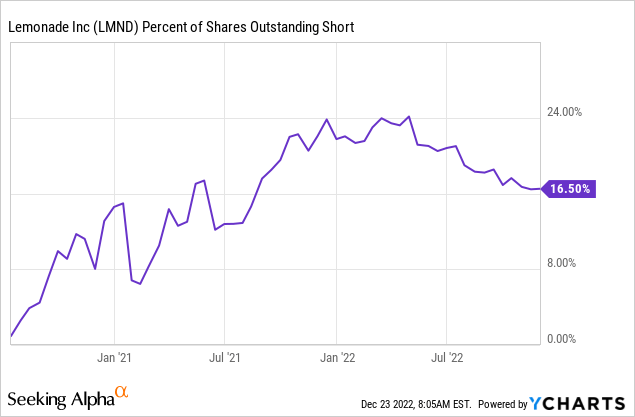

Lemonade is extremely oversold as the drop from the August high has gotten it way under its 50-day moving average. This, of course, has been driven by the poor fundamentals and likely, a heavy dose of tax loss selling. As tax loss selling winds up, and we settle into the low volume holiday season, Lemonade could become a target for a short squeeze. The short float numbers are not extremely high, but respectable and not worth risking moving against.

Reason 3:

Lemonade for all its flaws and a complete lack of profits could be bought out. From an acquirer’s standpoint, the company is now trading close to tangible equity and if they feel they can rapidly turn around the loss-making policies, a bid could be placed. We give this low odds at present, but with every tick lower, the odds do increase. The Lemonade brand has become quite popular, and it is growing rapidly in multiple markets. Even if there was a rumor about it, we could see a good short squeeze from such oversold levels. Why hang around at this point? The next point to Short Sell would be a bounce similar to August.

Verdict – Why We Are Not Going For A Buy

We generally move in incremental steps, and a double upgrade would be quite out of character. So, you will generally not get a Buy rating after a Sell, unless something fundamentally changes. In the case of Lemonade, the only thing that has changed is that it is no longer a good short sale. Everything else remains in the dumps. Rapid growth in policy writing has not brought with it a semblance of profits. The outlook for the next two years is heavily negative, and we don’t see much changing that.

Seeking Alpha

The company will get some interest income, especially if you benchmark against early 2022, in the coming years. But with $900 million of tangible equity, we don’t think it will be a game changer. At best that gets you $36-$45 million in interest income versus a loss run rate over $240 million a year.

In fact, our base outlook here is that Lemonade will have to do a very big equity raise to prevent the stock from going to zero within three years. The company is on the clock to turn things around, and it has a lot of wood to chop.

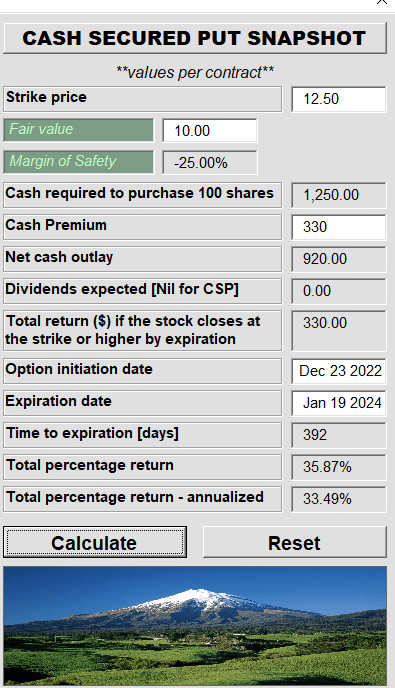

So whichever way it plays out, a long case is impossible to make. If you still buy the bull here, and we strongly suggest you reconsider, then options make more sense. One way would be to sell the $12.50 Cash Secured Puts for January 2024.

Author’s App

This defensive option would create a 35.87% total return if Lemonade managed to levitate over $12.50 for one year. It also has a breakeven point of $9.20. This defensive way is far better than a direct long position. For our part, we are staying out as there are far better quality insurance and reinsurance plays to be bothering with a long position here.

Please note that this is not financial advice. It may seem like it, sound like it, but surprisingly, it is not. Investors are expected to do their own due diligence and consult with a professional who knows their objectives and constraints.

Be the first to comment