Mario Tama

Altria Group, Inc. (NYSE:MO) investors were likely assured that the company’s ability to weather a more pronounced macroeconomic slowdown was understated, as it posted a double beat on net revenue and profitability at its recent earnings release.

In addition, the company demonstrated its confidence in its free cash flow (FCF) generation by announcing a new $1B stock repurchase program after exhausting its previous $1.8B authorization. Despite that, an analyst on the conference call had anticipated a more significant repurchase program.

However, management reminded investors that MO still pays a substantial dividend (NTM dividend yield: 8.2%) as part of its overall capital allocation strategy. As such, income investors were likely not perturbed by the “smaller” new authorization, as MO has proved its market-beating performance over the past year (1Y total return: 1.87%).

Despite that, investors should consider that Altria’s FY23 outlook probably didn’t inspire the same level of confidence in Wall Street analysts (consensus rating: Neutral). An analyst on the call highlighted that Altria’s “2023 earnings guidance reflects a slightly lower growth rate compared to (its) 4% to 7% guidance over the last several years.”

Accordingly, Altria guided an adjusted EPS growth of 3% to 6% for FY23. However, it was still better than the more pessimistic consensus projections of 3.7%, suggesting Wall Street was concerned with the macroeconomic impact on its premium positioning in the market.

Does it make sense? Well, Altria did highlight the impact of consumers trading down, as the discounted segment gained share (1.4 share points) due to higher inflation, macroeconomic concerns, and heightened competition. However, Marlboro also raised its share of the premium segment to 58.2%, corroborating its brand and market leadership in the more profitable segment.

As such, we believe Altria remains in a pole position to leverage a potential economic recovery in H2’23 or 2024 if the job market remains strong, bolstering consumer spending.

We urged investors in our previous article to pay close attention to the macroeconomic headwinds that could affect Altria’s ability to maintain its momentum to transit to reduced-risk products.

However, our concerns could have been overstated, as management’s confidence to drive solid adjusted EPS growth in a highly uncertain year is constructive.

Still, investors need to consider the more intense competitive headwinds that could affect the company’s transition from its legacy tobacco business. The company acknowledged higher promotional spending in its smokeless categories to compete for market share. However, management also articulated that it has curtailed its promo spending to lift its margins, closing “the price gap with competitors.”

We believe the execution risks in the company’s transition and the success of its JV with Japan Tobacco (OTCPK:JAPAF) on heated tobacco stick products will be closely scrutinized by investors.

Therefore, the structural risks of its transformation journey could hamper the re-rating potential of MO, as Wall Street analysts are likely looking for more evidence of a sustained improvement moving ahead.

With that in mind, investors will need to consider whether the current opportunity in MO is attractive enough, given its relatively attractive valuation?

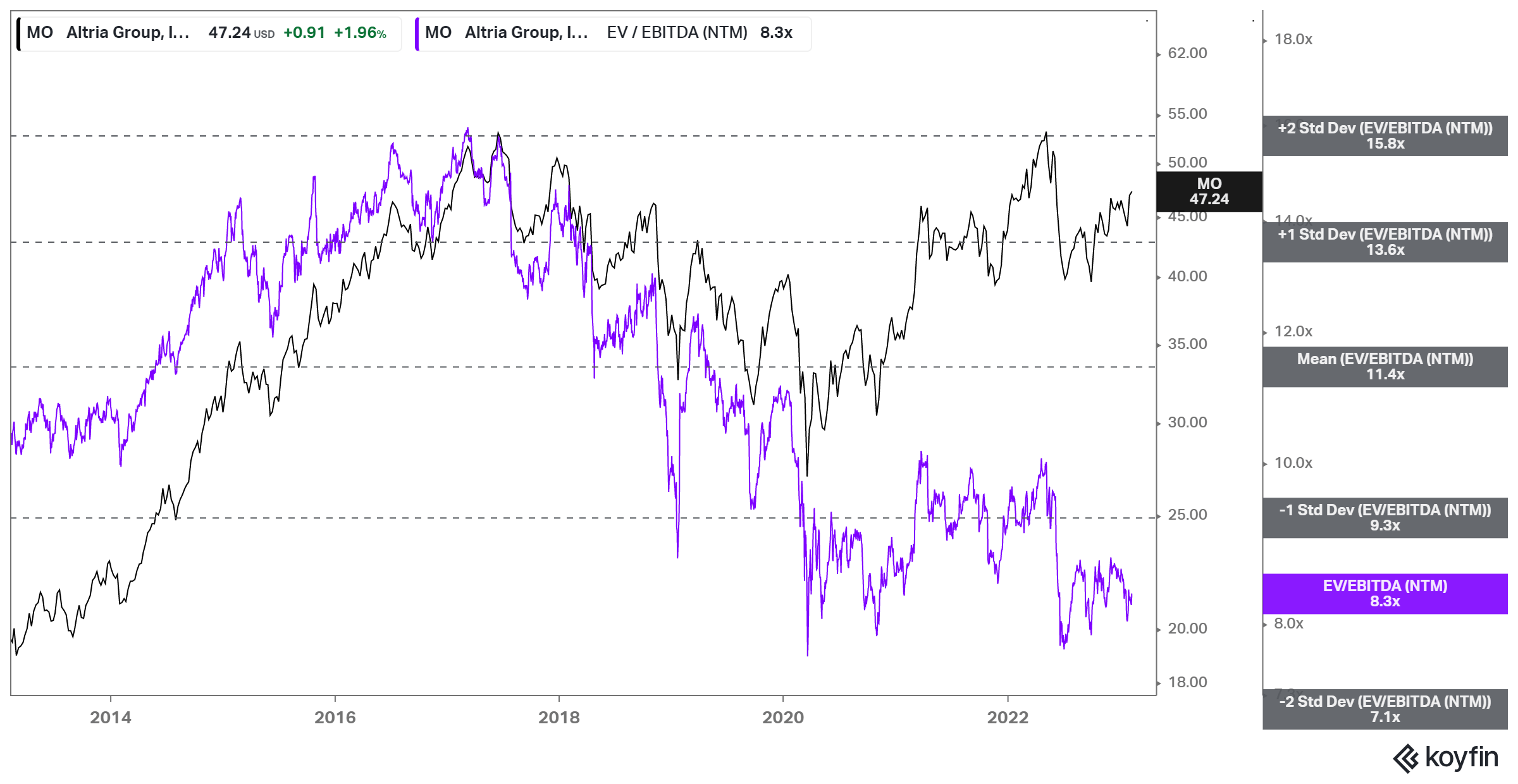

MO NTM EBITDA valuation trend (koyfin)

MO last traded at an NTM EBITDA of 8.3x, well below its 10Y average of 11.4x. However, it’s still ahead of its peers’ median of 6.5x (according to S&P Cap IQ data).

Therefore, the market has likely de-risked MO and its peers as they execute their transition away from their legacy categories, given the secular decline in the total shipment volume of combustible products, which fell 7.8% in FY22.

Therefore, the onus is on Altria to outperform the market’s tepid optimism, which investors will need to consider for a potential uplift in its valuation prospects.

Despite that, MO’s bottoming process in September 2022 remains robust. Therefore, income investors should find the current levels attractive to add more positions.

Rating: Buy (Reiterated).

Be the first to comment