KIKILOMBO/iStock via Getty Images

By Silvia Kitchener

Global inflation concerns, rising interest rates in the U.S., the Russia-Ukraine war and political uncertainty with new governments in Chile, Peru and, most recently, Colombia have finally caught up with the region. In addition, Brazil, the largest market in Latin America, will be holding presidential elections this year, contributing to further uncertainty.

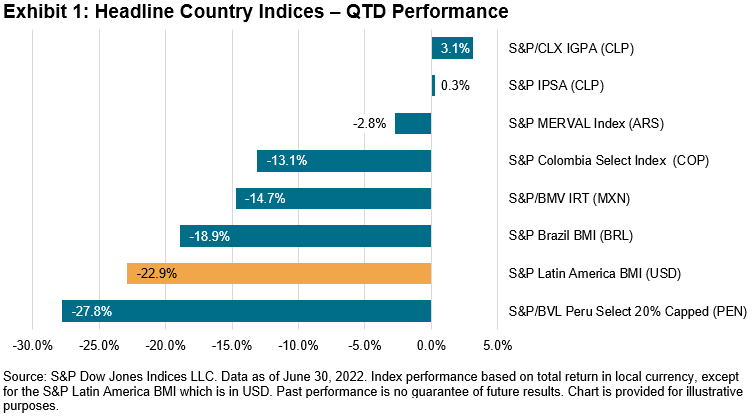

From a country perspective, Chile had the best returns in Q2, with the flagship S&P IPSA gaining nearly 0.30% in CLP. The broader Chilean index, the S&P/CLX IGPA, did better with a 3.1% return for the same period. All other markets, in local currency, had negative returns for Q2 (see Exhibit 1).

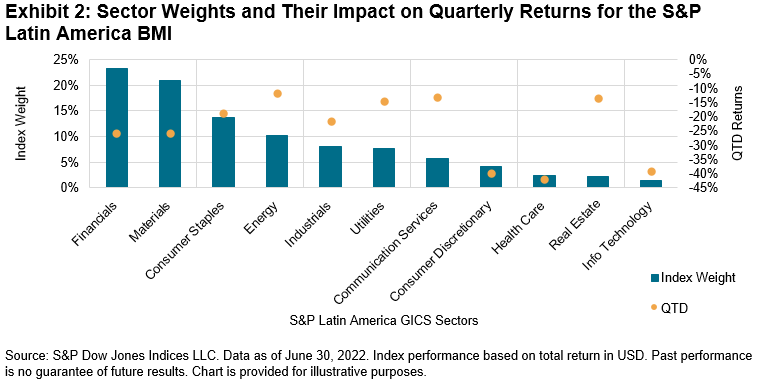

No sector was unscathed in Q2. It is interesting to note that while Health Care (-42.1%), Consumer Discretionary (-40.0%) and I.T. (-39.1%) were the worst performers, they were not necessarily the main contributors to the quarterly losses. Exhibit 2 shows that it’s more likely that sectors with large representation in the region, such as Financials, Materials and even Consumer Staples, which were down 25.3%, 21.0% and 13.8%, respectively, had the most significant impact on the downturn of the equity market.

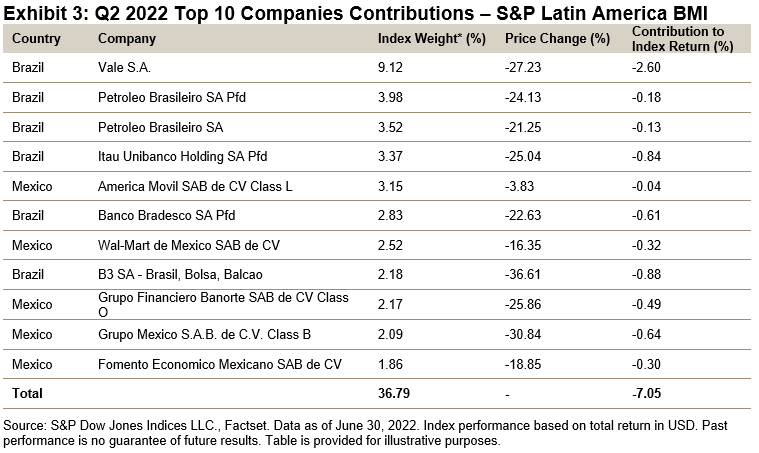

Similarly, most of the losses were driven by Brazilian and Mexican companies, which together represent about 88% of the S&P Latin America BMI. Exhibit 3 shows how the top 10 index constituents accounted for nearly one-third of the Q2 index decline. Brazilian companies Vale S.A., B3 S.A. and Itau Unibanco had the most significant impact on the index.

Though it is perhaps not surprising that the markets have taken a turn for the worse given the local political turmoil, rising inflation, the Russia-Ukraine war and the lingering effects of COVID-19, it is still disappointing to see the markets drop this sharply. While there is no telling where the bottom may be, volatility is likely to continue. Let’s hope the next turn will be an upswing.

Disclosure: Copyright © 2022 S&P Dow Jones Indices LLC, a division of S&P Global. All rights reserved. This material is reproduced with the prior written consent of S&P DJI. For more information on S&P DJI please visit www.spdji.com. For full terms of use and disclosures please visit Terms of Use.

Editor’s Note: The summary bullets for this article were chosen by Seeking Alpha editors.

Be the first to comment