SeanPavonePhoto

Thesis

The Kroger Co. (NYSE:KR) is the second-largest grocer in the country, with the potential to rival Walmart (WMT) as the top dog. Kroger’s stock price has performed quite well from lows in mid-2019, however, the stock still appears to offer good value at current price levels. Kroger’s merger with Albertsons Companies, Inc. (ACI) will offer investors a ton of value so long as the FTC allows it. Additionally, Kroger has been posting strong results in tandem with improved guidance. Kroger has proven to be a great investment in uncertain markets and the company appears undervalued based on my discounted cash flow analysis. Let’s take a look.

Kroger-Albertsons merger

Kroger and Albertsons agreed to a merger in which Kroger will acquire all outstanding ACI shares for $24.6 billion, or $34.10 per share. This reflects a 28.5% premium from current share prices when not including the special dividend payment of $6.85 per share. A finalized deal still offers quite a bit of value for those interested in Albertsons stock. Kroger received a second request from the FTC regarding the merger, which is expected to delay the merger by months. While antitrust issues merit much concern, Kroger believes they have a clear path to approval by 2024.

The FTC is concerned the Kroger-Albertsons merger will harm local grocers and lead to higher prices for consumers. Kroger believes spinning off roughly 100 – 375 stores into SpinCo will help achieve FTC approval. Regardless, the merger would solidify Kroger as the second—if not largest—grocery chain in the country. Together, Kroger and Albertsons operate 4,996 stores, 66 distribution centers, 52 manufacturing plants, 3,972 pharmacies, and 2,015 fuel centers across 48 states and the District of Columbia. Depending on potential divestitures, Kroger could surpass Walmart as the country’s largest grocer by storefronts, as Walmart held 4,742 storefronts in 2022. Kroger and Albertsons delivered $210 billion in revenue, $3.3 billion in net income, and $11.6 billion in EBITDA in FY21. While Kroger and Albertsons revenue generation falls quite short of Walmart’s, the dynamic duo would undoubtedly be its top competitor in the grocery space.

Kroger is producing strong results and improved guidance

Kroger’s operational performance has been quite impressive as of recent. The company has invested heavily in its digital initiatives, is driving ID sales growth with Kroger Fresh and Our Brands business and is on track for $1 billion in cost savings for a fifth consecutive year. Kroger’s digital sales are up over 10%, ID sales are up over 6.9%, and the company expanded its Fresh initiatives to 1,252 stores (all data for 3Q22).

Kroger’s success can be seen in its FY22 full-year guidance:

- Full-year guidance on ID sales went from 4.0% – 4.5% to 5.1% – 5.3%.

- Full-year guidance on EPS went from $3.95 – $4.05 to $4.05 – $4.15.

- Full-year guidance on operating profit went from $4.6B – $4.7B to $4.8B – $4.9B.

- Full-year guidance on CAPEX went from $3.4B – $3.6B to $3.2 B- $3.4B.

Kroger’s guidance on ID sales, earnings, operating profit, and CAPEX all saw positive revisions from 3Q22 guidance to updated guidance in December of 2022. Considering the nature of the current economic climate, it’s relieving to see a company forecasting for the better.

Kroger’s a strong investment in a weak market

The broader market and economy have been plagued with numerous headwinds, from rising rates, high inflation, and supply chain disruptions all immediately following a grueling pandemic. The only positive to look at is the strong labor market, which conversely doesn’t help the regression of the elevated inflation levels. That said, grocers have always been a solid investment avenue to turn to during times of high inflation and a struggling market. While consumers may hold off on new cars, cell phones, and luxury apparel items as budgets tighten, they still have to eat. The business of selling necessities is a great business, and that’s Kroger’s business.

I’m sure everyone reading this has seen a spike in their grocery bills. Kroger is not immune to rising costs, however, like many other businesses, a large majority of those are passed down to the consumer. The difference, again, is that consumers will buy food regardless of the price hikes. In fact, the current economic environment has likely helped Kroger drive the impressive growth in its Our Brands business (up 10.4% in 3Q22), as Kroger’s in-house products are generally cheaper than larger name brands. Let’s look at Kroger’s stock performance during some recent times of economic turmoil.

- The .com Bubble (2000 – 2002): Kroger’s stock price—$8.78 – $10.28.

- The Housing Crisis (2007 – 2008): Kroger’s stock price—$11.80 – $12.65.

- The Covid-19 Pandemic (2020 – 2022): Kroger’s stock price—$30.71 – $44.24.

Kroger’s stock has managed to fare quite well during times of economic turmoil. While interest rates may be close to peaking and inflation has been tapering down, there are still fears that more trouble is ahead. Regardless, Kroger has proven to be a solid investment during times of market uncertainty.

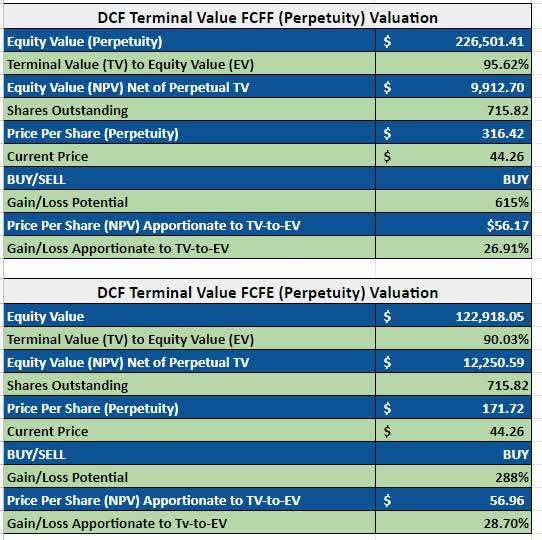

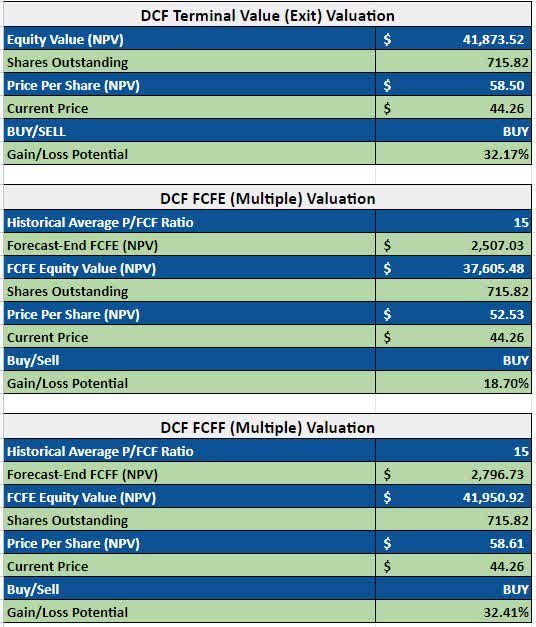

My DCF results on Kroger

I ran a discounted cash flow (“DCF”) on Kroger using TTM data starting in FY19 to FY22 and forecast for five years. I take income statement, balance sheet, and cash flow line items as a percentage of revenue in order to get my forecasted figures, and used analyst revenue growth forecasts to get my forecasted revenue figures. I forecasted free cash flow to firm (FCFF), free cash flow to equity (FCFE), and EBITDA. I use the perpetuity approach utilizing terminal value for my FCFF and FCFE valuations, and use the exit approach for EBITDA. I also take Kroger’s historical average P/FCF ratios and apply them to the company’s forecast-end discounted cash flows to get two more additional exit strategy values for an average. Below are some notes regarding the DCF:

- I take terminal-to-equity value percentage to account for the present value of equity.

- I use the weighted average cost of capital (WACC) as my discount rate for FCFF.

- I use the cost of equity (CAPM) as my discount rate for FCFE.

- My average rate of return is the average of Kroger’s 5-yr CAGR, NI/MC, and average market return.

- I’m using Kroger’s 5-yr monthly beta of 0.51.

- My terminal growth rate is 3.00%.

- My risk-free rate is 2.5% considering the current would technically be negative.

- EBITDA exit multiple is 4.5. P/FCF multiple is 15 for both FCFF and FCFE.

Here are my results:

DCF FCFF & FCFE (Perpetuity) (Dalton Hicks)

DCF EBITDA (Exit) & FCFF/FCFE Avg. P/FCF Multiple (Dalton Hicks)

I take the average of the net present value upside for each respective valuation method and get an average net present value upside of 27.78%. Both perpetuity and exit strategy approaches utilizing DCF analysis point to Kroger being undervalued.

Risks to consider with a Kroger investment

In all, I don’t find Kroger to be a risky investment. That said, I find the potential that the FTC could prevent the Kroger-Albertsons merger, industry competition/ecommerce, and lack of international presence to be Kroger’s biggest threats.

Should Kroger’s merger with Albertsons get shutdown by the FTC, we may see heightened volatility in the stock price. It’s likely investors are quite excited about the merger, indicating poor news on this front may lead to selloffs. It’s quite unclear how the merger is going to play out considering the FTC is thoroughly reviewing its potential impact on local markets and how it will affect grocery prices. Several Senators have also voiced opposition to the merger. It’s hard to say how the FTC declining the merger would affect Kroger’s stock, but it’s certainly worth keeping an eye on.

The retail grocery sector is highly competitive as there are many storefronts to shop at and being competitive with pricing is difficult. In short, is extremely hard to hold a significantly competitive edge in the grocery space. Additionally, Amazon’s (AMZN) massive ecommerce presence poses quite a threat. Over 70% of Americans are shopping online on a daily basis. Consumers can get same day deliveries for similar prices while saving time by not having to go to the store. Amazon’s Whole Foods is producing double-digit sales growth, indicating they’re making ground in the grocery space. While I do believe the majority of consumers like to shop in-store for their groceries, everything is trending towards online sales.

That said, Kroger has produced impressive growth with its digital initiatives and has a far greater physical presence than Amazon does in the retail grocery space. Investors should continually monitor sales trends and Kroger’s digital sales growth to make sure the company is keeping up with consumer grocery shopping trends.

While I don’t think Kroger’s lack of international presence is a threat to its operational performance, I do think it may hinder its attractiveness as an investment. With Walmart across the globe, it’s able to generate far more revenue and cash flow than the likes of Kroger. Investors may view Kroger as a company with limited potential as its presence in the U.S. continues to become progressively more saturated. Additionally, international expansion initiatives will come with a hefty price tag, one that would be taking a hefty bite out of bottom-line figures. Lack of international presence may not be directly harming Kroger, but it’s certainly not helping it.

Conclusion:

In all, I find The Kroger Co. to be an attractive investment at current price levels. Kroger has produced double-digit growth in online sales and is driving strong ID sales growth with its Fresh initiatives. The improved guidance across the board is a reflection of Kroger’s strong operational performance. Furthermore, Kroger has historically performed well in uncertain markets, which we are currently in now. Based on my discounted cash flow analysis of Kroger analyzing multiple valuation strategies, Kroger stock appears quite undervalued. That said, I recommend shares of The Kroger Co. as a solid investment option in the current market.

If you liked this article, follow me to get notified when I post new analysis and insights on various stocks in the market.

Be the first to comment