Tim Boyle

Today is the day when Kimberly-Clark (NYSE:KMB) commented on its previous three months’ performance. We have already published two analyses this year and we recommend to our readers to check up on our previous articles:

Q2 Results

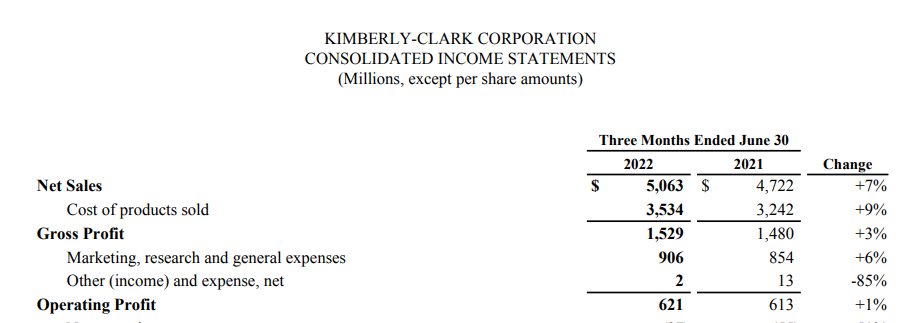

Kimberly’s second-quarter performances were not great. There was a strong price increase action resulting in 7% growth on the revenue line that was offset by currency effect but more importantly was not sufficient to cover cost pressure at the COGS level. Going down to the bottom line, we also see increased costs for marketing and higher SG&A expenses. We are not surprised and we have already anticipated more pass-through action in the second half of the year.

Kimberly-Clark Q2 financial snap

Source: Kimberly-Clark Q2 press release

Mare Evidence Lab’s conclusion was also supported by the CEO’s words – Kimberly’s “result also reflects ongoing market volatility and significant input cost inflation. We continue to be thoughtful with our response to inflation, focusing on providing value to our consumers while leveraging price and cost discipline to mitigate macro headwinds for margin improvement over time.”

We should also note that the CEO increased the company’s guidance on organic sales growth. They are currently in a range between 5%-7% versus the previous estimate of 4%-6%. At the same time, operating profit margin and EPS were downgraded, now they are expected to be at the lower end of the company’s range.

Kimberly-Clark 2022 guidance

Source: Goldman Sachs Global Staples Forum

Why are we more positive about Essity (OTCPK:ESSYY; OTCPK:ETTYF)?

- Essity delivered 17.8% of organic sales growth, much higher than its American counterparts;

- Contrary to Kimberly’s performance, volume grew by 3.7%. This was also coupled with a strong price/mix resulting in a plus 14.1% compared to a plus 1% achieved by Kimberly;

- Looking at the Essity performance, we also note a decline in margin due to the cost pressure, the quarter was supported by lower tax (same for Kimberly) and lower minorities. In Kimberly, we note lower working capital requirements;

- The European capacity utilization rate is suffering (there are many small players), and Essity is taking full advantage;

- We appreciated the bolt-on acquisitions that Essity is currently pursuing. The latest M&A was concluded in Canada. Essity acquired 80% of Knix Wear Inc., a leading supplier of leakproof apparel for incontinence and periods.

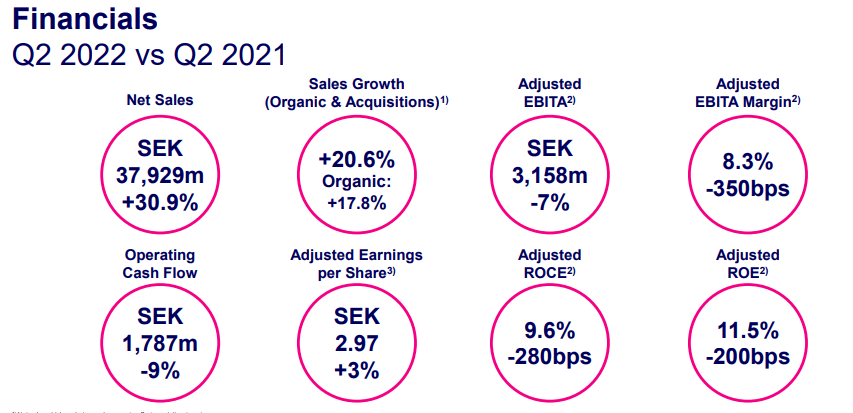

Essity Q2 financial snap

Source: Essity Q2 Results

Conclusion and Valuation

Aside from the financial consideration and the latest results, Essity is currently trading at a 2023 P/E of 13x compared to 19x of its closest peer. We believe that this discount is totally not justified. Once again, we reaffirm our neutral rating on Kimberly-Clark and a buy rating on Essity, this is based on a 16x P/E, which derives a target price of SEK 300.

Be the first to comment