Kaiser Aluminum Corporation (NASDAQ:NASDAQ:KALU) recently signed a large acquisition, and reported more than double digit sales growth. In my view, further research and development and the use of lean manufacturing would imply higher stock valuations. Besides, assuming expectations from management about the company’s EBITDA margin and some small acquisitions, my DCF model resulted in an even higher target price. Yes, I obviously see risks from the current amount of debt and new environmental regulations. With that, I believe that Kaiser Aluminum could be a beneficial long-term play.

Kaiser Aluminum: Meaningful Acquisitions And An Ambitious Target

Founded in 1946 and previously part of Kaiser Aluminum and Chemicals Corporation, Kaiser Aluminum is an aluminum producer based in the United States. The company manufactures and sells general engineering products or GE products, beverage and food packaging products, and aerospace and high strength products among other products.

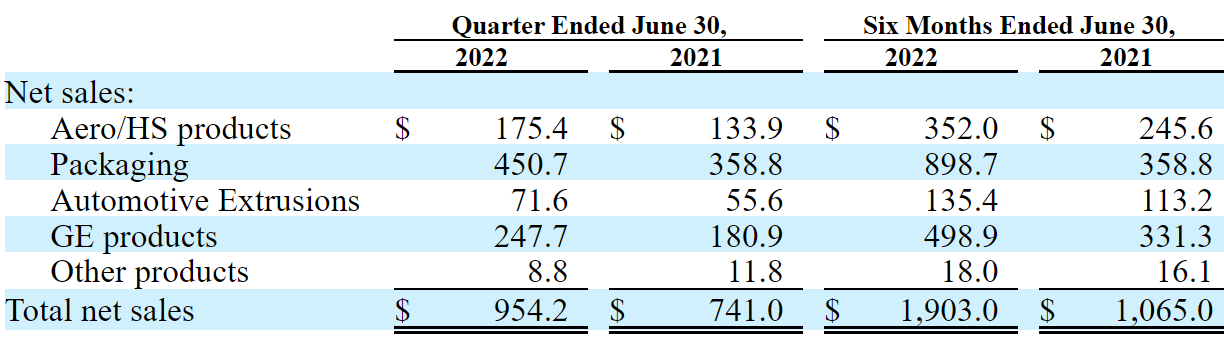

In 2021, management executed M&A operations, which led to a double digit sales growth in 2022. Management appears to be conducting several new searches of supplies, which may soon help improve revenue growth.

Source: 10-Q

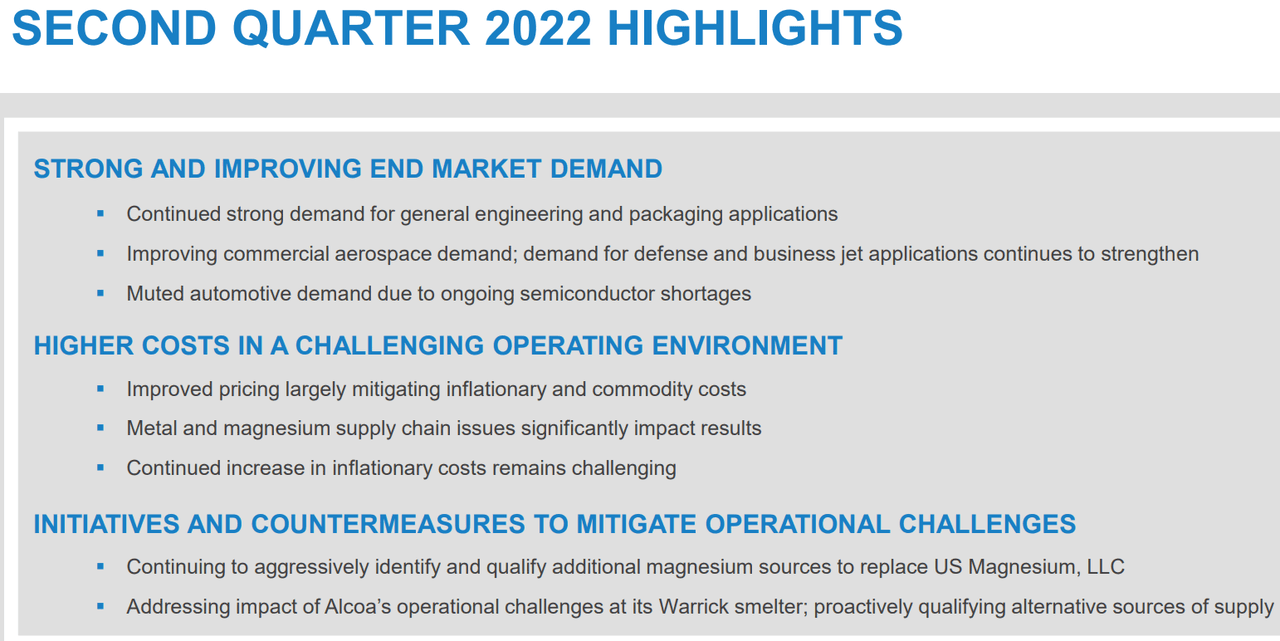

In the last quarterly report, Kaiser Aluminum noted strong demand for GE products and packaging products. The company also appears to successfully navigate inflationary pressures by successfully increasing prices. Clients don’t seem to reduce their demand for products, which is quite beneficial. In my view, if Kaiser successfully finds new sources of supply, and operational challenges don’t affect future free cash flow, I would expect stock price increases.

Presentation

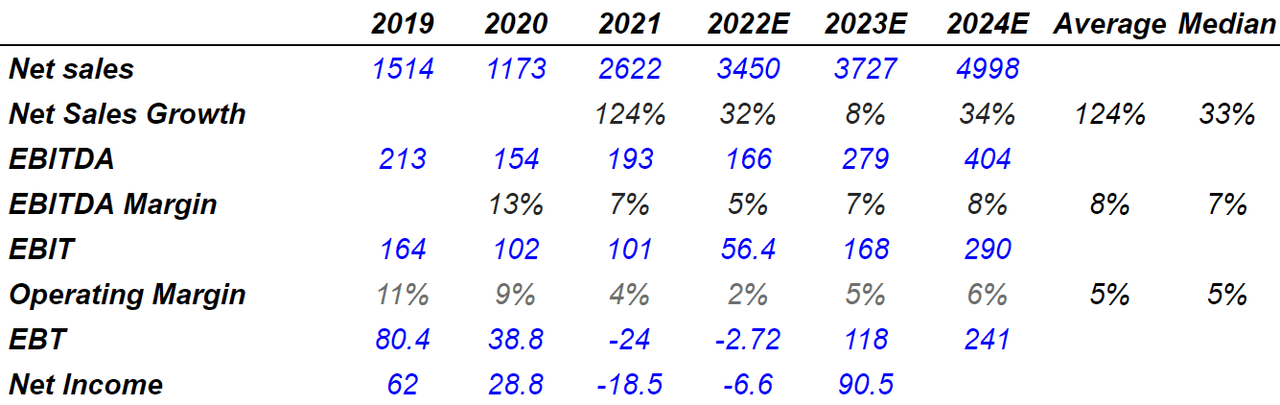

With that about the state of the company’s operations, Kaiser Aluminum reported an interesting long-term target. Management believes that the EBITDA margin could stand at 20%, which is more than two times what the company is currently reporting.

Presentation

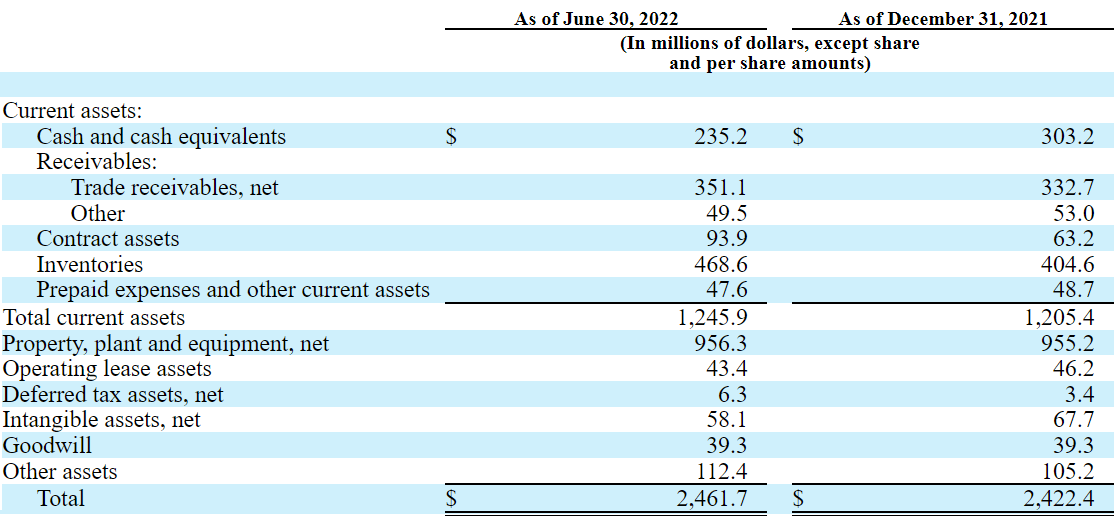

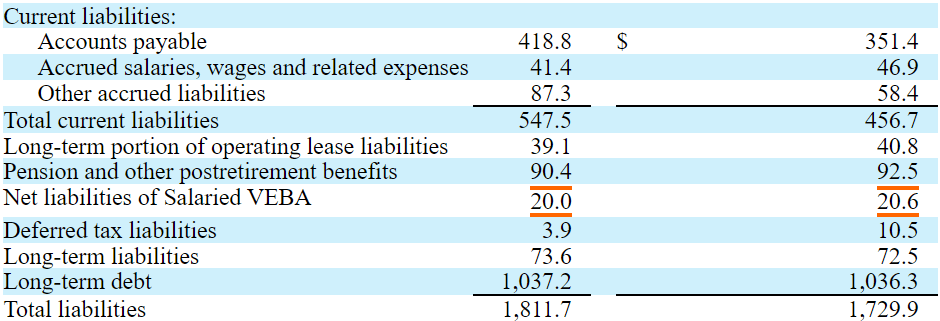

Balance Sheet: $1 Billion In Long Term Debt, But Healthy Asset/Liability Ratio

As of June 30, 2022, Kaiser reported $235 million in cash, total assets of $2.4 billion, and $1.8 billion in total liabilities. The asset/liability ratio remains healthy. However, investors may want to have a look at the company’s total amount of debt.

10-Q

Long-term debt stands at $1 billion, and Kaiser also reports pension obligations worth $90 million. In my view, Kaiser’s business model shows stable EBITDA margins, and it is easy to make forecasts. With that, in my view, if management successfully reduces its total amount of debt, the cost of capital may decline, which may lead to stock appreciation. Let’s note that certain investors may, in my view, not invest in Kaiser Aluminum because of its net debt/ EBITDA ratio.

10-Q

Forecasts From The Investment Community Are Beneficial

In my view, the forecasts made by analysts about Kaiser Aluminum are beneficial. Investors are expecting sales growth of 32% in 2022 and 34% in 2024. The EBITDA margin is also expected to be close to 8%-7%, with positive net income from 2023.

Source: Marketscreener.com

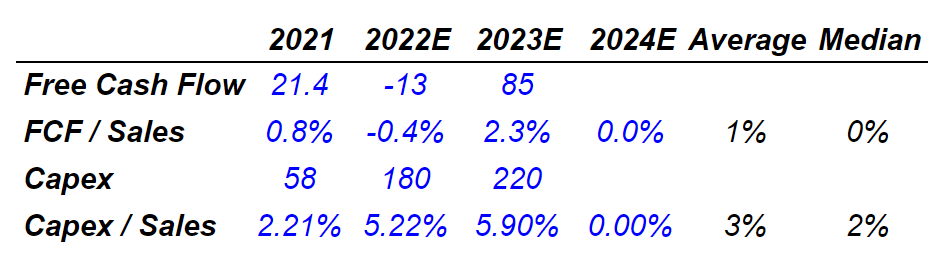

It is also worth noting that investors are expecting a significant jump in the free cash flow from 2023, which would stand at close to $85 million. Finally, let’s note that the investment community does not expect relevant capital expenditures from 2022. The capex/sales ratio is expected to be close to 3%.

Source: Marketscreener.com

Under Conservative and Standard Conditions, I Obtained A Fair Price Of $77 Per Share

Under normal circumstances, I would expect that Kaiser’s Lean Manufacturing, Six Sigma, and Total Productive Manufacturing tools will enhance the EBITDA margin. The company provided a significant amount of information about how it intends to become a low cost producer in the market:

Our strategy to be the supplier of choice and a low cost producer is enabled by a culture of continuous improvement that is facilitated by the Kaiser Production System, an integrated application of tools such as Lean Manufacturing, Six Sigma and Total Productive Manufacturing. Using KPS, we seek to continuously reduce our own manufacturing costs and eliminate waste throughout the value chain. Source: 10-k

Under this case scenario, I also expect that R&D efforts will enhance future quality, reduce costs, and improve product attributes. Let’s note that we are talking about a company that invests close to $10 million in R&D per year:

Research and development costs for 2021, 2020 and 2019 were $9.3 million, $9.1 million and $10.5 million, respectively.

Our Centers for Excellence, dedicated research and development centers devoted to product performance enhancement and process development within our production operations, are focused on: 1) controlling the manufacturing process; 2) maximizing the use of recycled aluminum; 3) improving product quality; and 4) ensuring consistency and enhanced product attributes. Source: 10-k

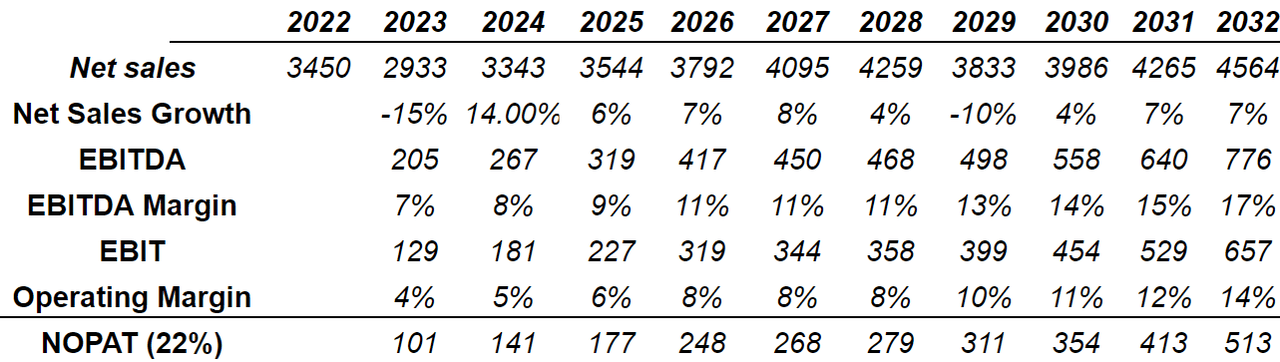

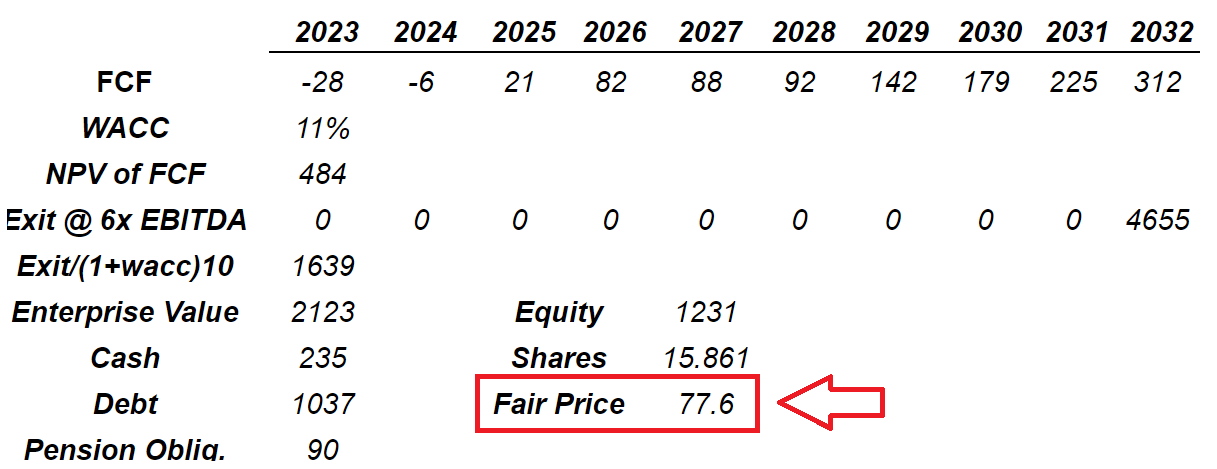

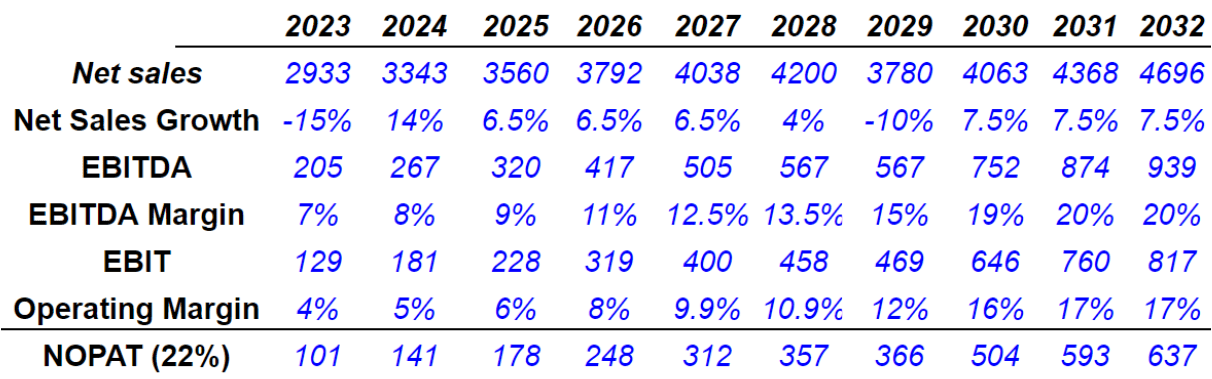

Under the previous conditions, I included -15% sales growth in 2023 and sales growth around 14% and -10% from 2024 to 2032. I also believe that Kaiser’s EBITDA margin will likely increase, but a bit less than what management predicted. In my view, an EBITDA margin around 11% and 17% from 2026 to 2032 could happen. If we also include a conservative effective tax of 22%, 2032 NOPAT would likely stand at around $513 million.

Arie’s DCF Model

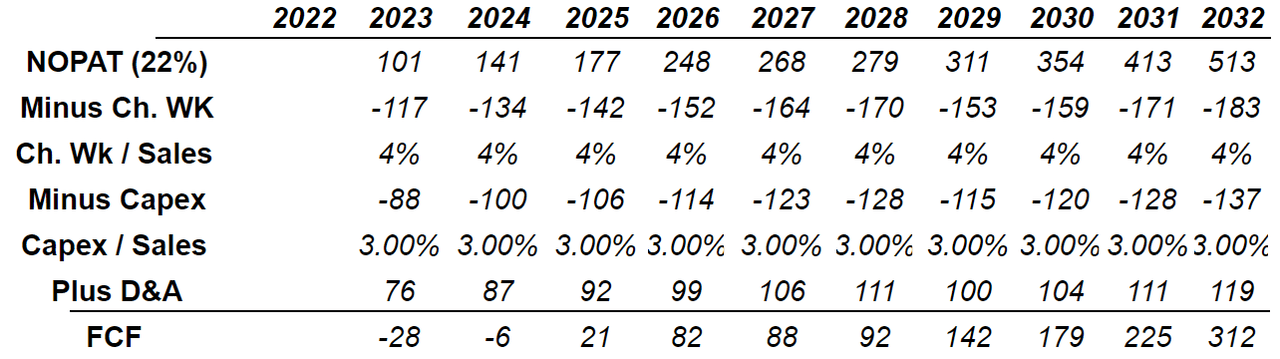

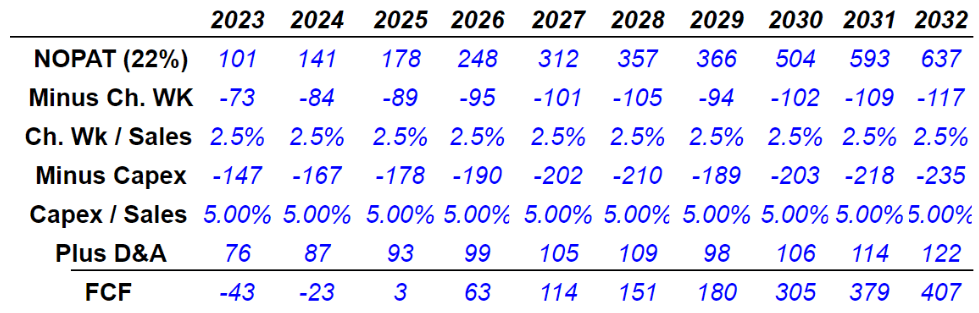

I also included changes in working capital close to $117 million and $183 million as well as capital expenditures around $89 million and $137 million. The results include positive free cash flow from 2025 and 2032 FCF of $312 million. I believe that these figures are quite conservative.

Arie’s DCF Model

If we use a discount of 11% like other investment advisors, the NPV of the free cash flow from 2023 to 2032 would stand at $484 million. With an exit multiple of 6x EBITDA used in 2032, I obtained a net present value of $1.63 billion. Summing everything I obtained an enterprise value of $2.1 billion. Finally, adjusting with the net debt, the equity value would be equal to $1.2 billion, and the fair price would be $77 per share.

Arie’s DCF Model

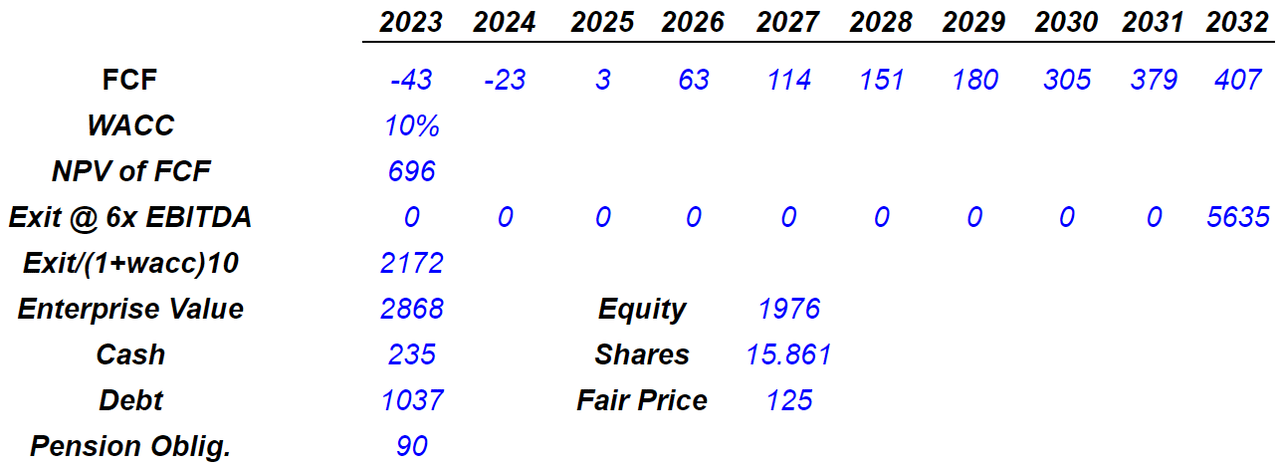

The Best Case Scenario Would Result In A Valuation Of $125 Per Share

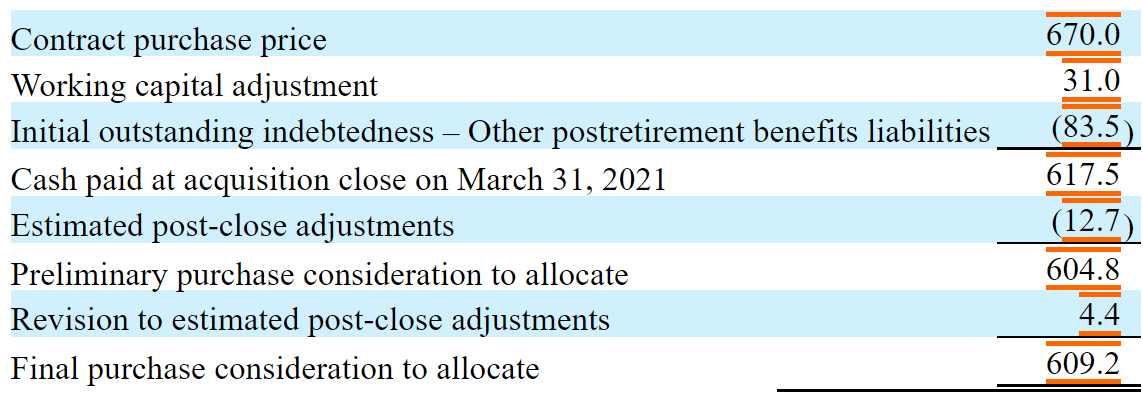

My best case scenario would include successful integration of Alcoa Warrick LLC and further acquisitions in the long-term. Let’s note that Kaiser Aluminum is not currently in a position to acquire other companies. The total amount of debt is significant. However, once the free cash flow commences to accelerate, and expected synergies are realized, perhaps the debt would decrease. As a result, Kaiser Aluminum may acquire new targets, which would likely bring higher EBITDA margin.

On March 31, 2021, we acquired Alcoa Warrick LLC and certain assets comprising the aluminum casting and rolling mill facility located in Warrick County, Indiana for a purchase price of $670.0 million. Warrick is a leading producer of bare and coated aluminum coil used for can stock applications in the beverage and food packaging industry in North America. Source: 10-k

10-k

Under these extraordinary circumstances, I believe that a sales growth around -15% and 14% from 2023 to 2032 makes sense. I also included an EBITDA margin close to 20% in 2032 as well as 2032 operating margin of 17%.

Arie’s DCF Model

With changes in working capital/sales of 2.5% and capex/sales of 5%, I obtained a free cash flow around $3 million and around $400 million. Note that in this case, I also used an effective tax of 22%.

Arie’s DCF Model

With a discount of 10% and an exit multiple of 6x EBITDA, the enterprise value would stand at close to $2.85 billion. Finally, the equity would stand at $1.9 billion, and the fair price would be close to $125 per share.

Arie’s DCF Model

Worst Case Scenario

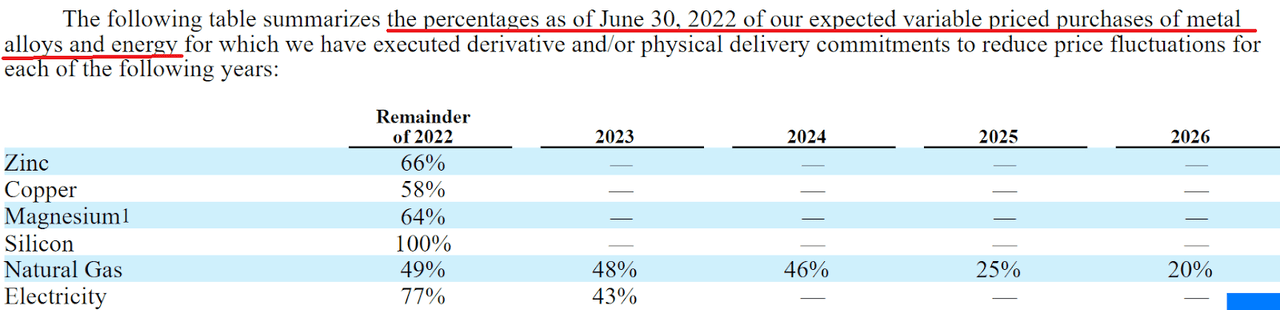

Certain changes in metal prices and mainly changes in the aluminum price could be a disaster for the company. Besides, Kaiser also depends on the prices of natural gas and electricity. If these two variables increase, I would say that management may have to increase the prices of its products. Customers may not be willing to accept the price increase, which would hurt revenue growth. If management decides not to increase prices, I would say that the free cash flow margin would decline. Finally, let’s note that the company executed hedging transactions to cover risks, which usually never covers 100% of the risks:

In conducting our business, we enter into derivative transactions, including forward contracts and options, to limit our exposure to: 1) metal price risk related to our sale of fabricated aluminum products and the purchase of metal, including primary and scrap, or recycled, aluminum, our main raw material, and certain alloys used as raw material for our fabrication operations; 2) energy price risk relating to fluctuating prices of natural gas and electricity used in our production processes. Source: 10-Q

10-Q

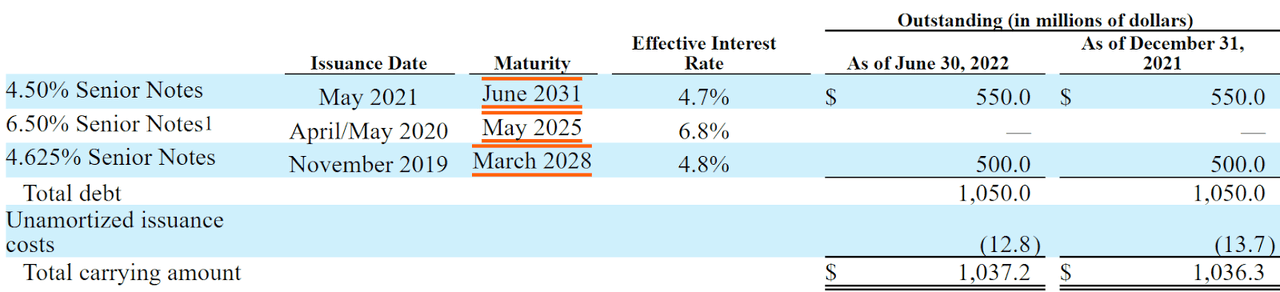

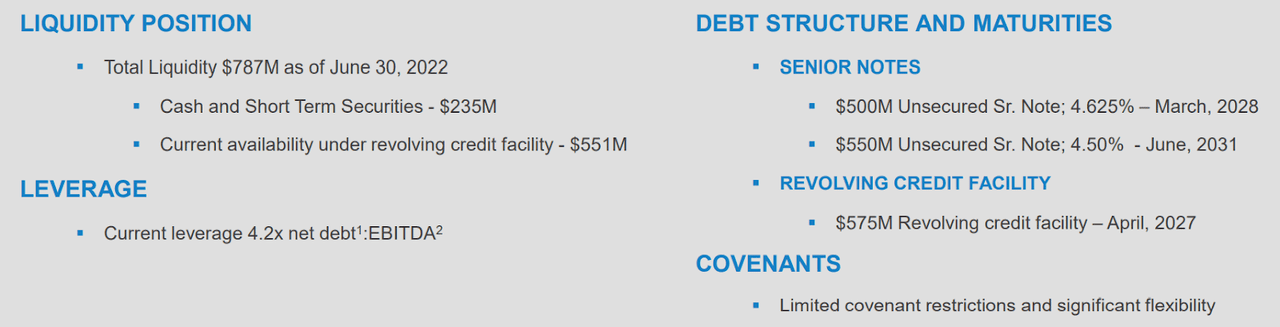

I am not concerned about the company’s debt obligations because most of the debt is payable in 2028 and 2031. With that, if Kaiser Aluminum does not reduce its debt or generates sufficient FCF per year to justify its current value, investors may be afraid. If many equity investors believe that Kaiser Aluminum will not be able to pay its debt, they may dump their shares. As a result, we may see an increase in the cost of equity and a reduction in the fair price.

10-Q

Source: Presentation

Source: Presentation

I am also deeply concerned about potential risks coming from new regulatory changes. Also, investigations about the operations of Kaiser could lead to fines, which may damage the company’s free cash flow margins. As an example, let’s note that the company is currently being investigated by the Ohio Environmental Protection Agency:

Pursuant to a consent agreement with the Ohio Environmental Protection Agency, we initiated an investigational study of our Newark, Ohio facility related to historical on-site waste disposal. During the quarter ended December 31, 2018, we submitted our remedial investigation study to the OEPA for review and approval. The final remedial investigation report was approved by the OEPA during the quarter ended December 31, 2020. We are currently preparing the required feasibility study, which we expect to submit to the OEPA for review during the quarter ending December 31, 2022. Source: 10-Q

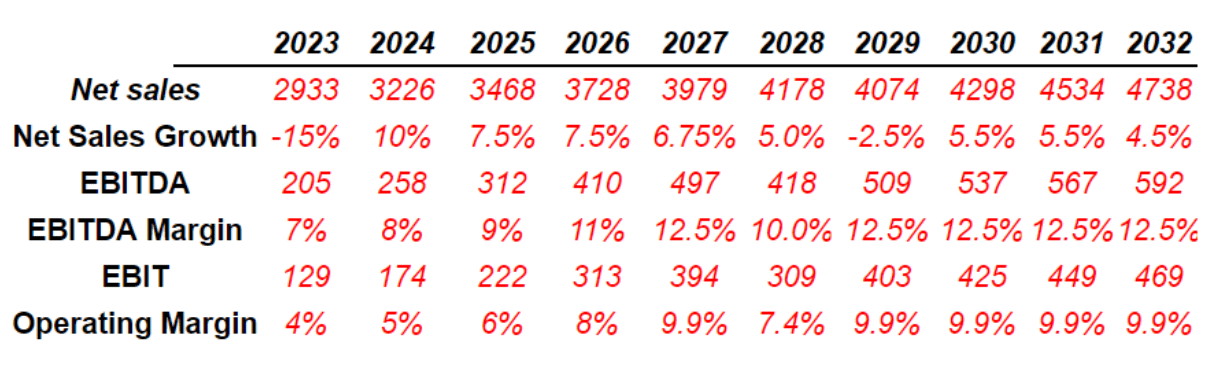

Under these conditions, I assumed sales growth of -15% in 2023 and 2032 net sales of around $4.5-$4.7 billion. I also assumed 2028 EBITDA margin of 10% and EBITDA margin close to 12.5% from 2029 to 2032.

Arie’s DCF Model

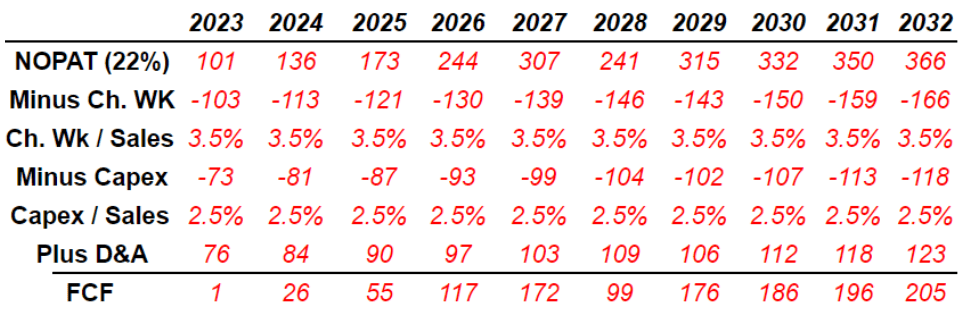

With changes in working capital/sales of 3.5% and capex/sales of 2.5%, I obtained 2032 free cash flow of $205 million. I believe that these numbers are less optimistic than that of most investors.

Arie’s DCF Model

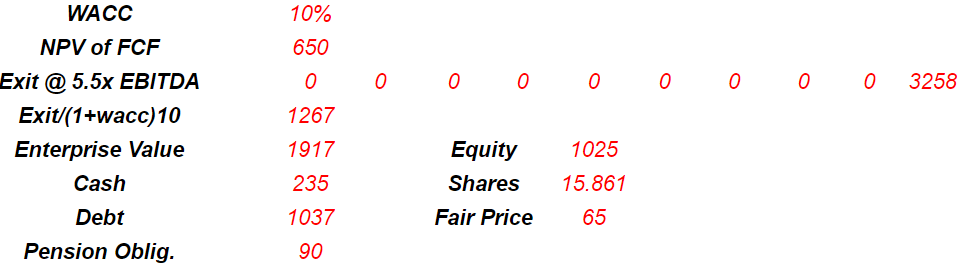

With a discount of 10%, the NPV of future free cash flow would be equal to $650 million. Besides, with an exit multiple of 5.5x EBITDA, the NPV of terminal value would be close to 1.25 billion. Finally, the fair price would stand at $65 per share.

Arie’s DCF Model

Takeaway

Kaiser Aluminum Corporation is an old player in the aluminum industry, and recently signed an acquisition, which may lead to many changes inside the organization. The company believes that an EBITDA margin of 20% is achievable in the long-term. Under my own DCF model, by including such EBITDA margin, I obtained a fair price that is significantly higher than the current market valuation. In my view, further research and development, some small acquisitions, and a favorable metals market could lead to a share price of $125. Yes, there are obviously risks from the current amount of debt and regulatory changes. However, at the current market price, I believe that Kaiser is a company to be followed carefully.

Please note that foreign exchange and other leveraged trading involves significant risk of loss. It is not suitable for all investors and you should make sure you understand the risks involved, seeking independent advice if necessary.

Be the first to comment