HomoCosmicos

Just over two months ago, I wrote on K92 Mining (OTCQX:KNTNF), noting that any pullbacks into the US$4.50 – US$4.90 zone would provide a low-risk area to start a position in the stock. After a sharp leg down into this zone in early November, the stock has recovered nicely, up 28% from its lows, and it even managed to eke out a positive gain for the year. Although this might not be what investors were hoping for heading into 2022, this represents meaningful outperformance vs. its benchmark and the major market averages and can be attributed to K92’s continued exploration success and ability to deliver on promises consistently. Let’s take a look at its Q3 results and at notable recent developments below:

Judd Mineralization (Company Presentation)

Q3 Results

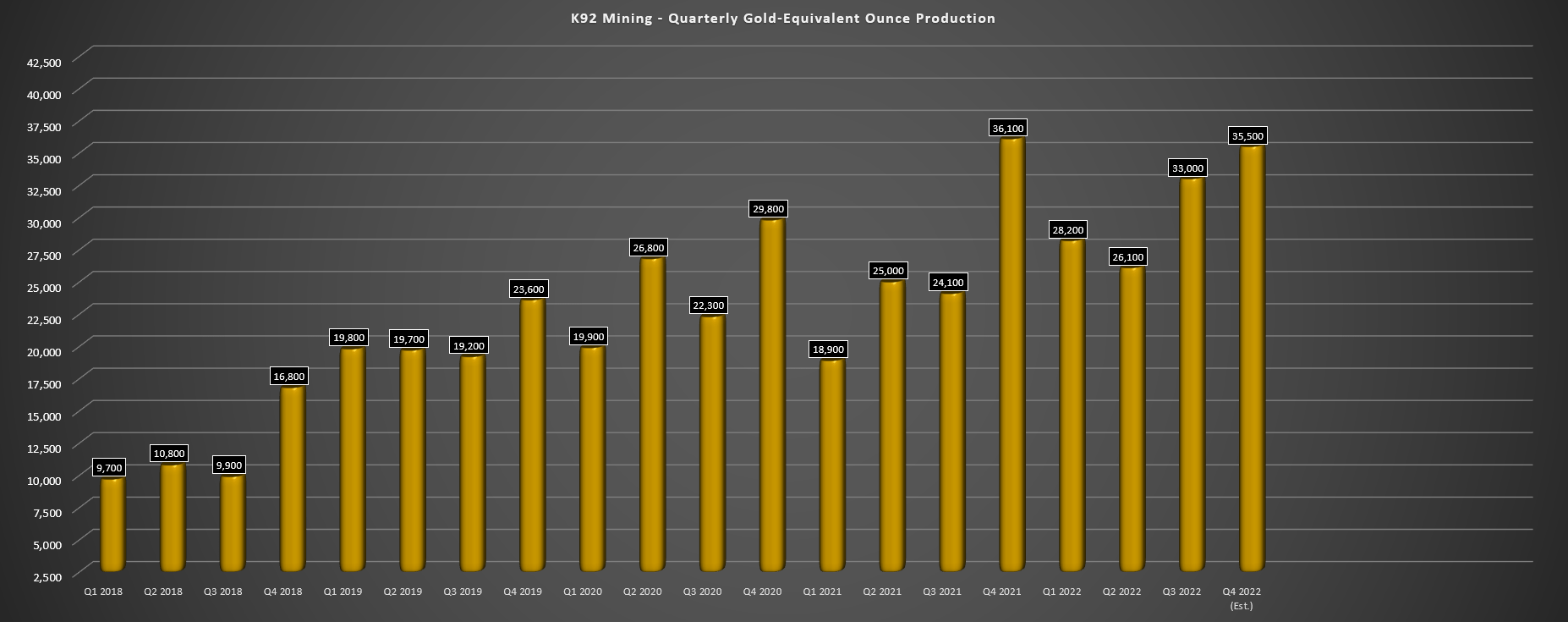

K92 Mining released its Q3 results in mid-November, reporting a 37% increase in quarterly production to ~33,000 gold-equivalent ounces. This impressive performance was driven by record tonnes mined (~122,000 tonnes) and record tonnes processed of ~117,900, offset by a slight decrease in grades vs. Q3 2021 levels. The result was that despite the weaker average realized gold price in the period ($1,663/oz) and fewer ounces sold than produced in the period (~25,300 ounces of gold sold vs. ~29,300 ounces produced), K92 Mining was able to post an increase in revenue and cash flow from operations. The latter came in at $11.5 million, an improvement from $7.0 million in Q3 2021.

K92 Mining – Quarterly Production (Company Filings, Author’s Chart)

Some investors might be slightly disappointed at the relatively low revenue and margins despite the strong production quarter. Still, it’s important to note that this was primarily related to selling fewer ounces than it produced, with gold concentrate and dore inventory of ~6,800 ounces at quarter-end. Additionally, the softness in the gold price certainly didn’t help, with K92’s average selling price sliding nearly 3% to $1,663/oz. Fortunately, the gold price has rebounded sharply since Q3, and it is back above the psychological $1,800/oz level, setting up a very strong Q4, given that K92 Mining should see another strong quarter of production with processing throughput near the 120,000-tonne mark.

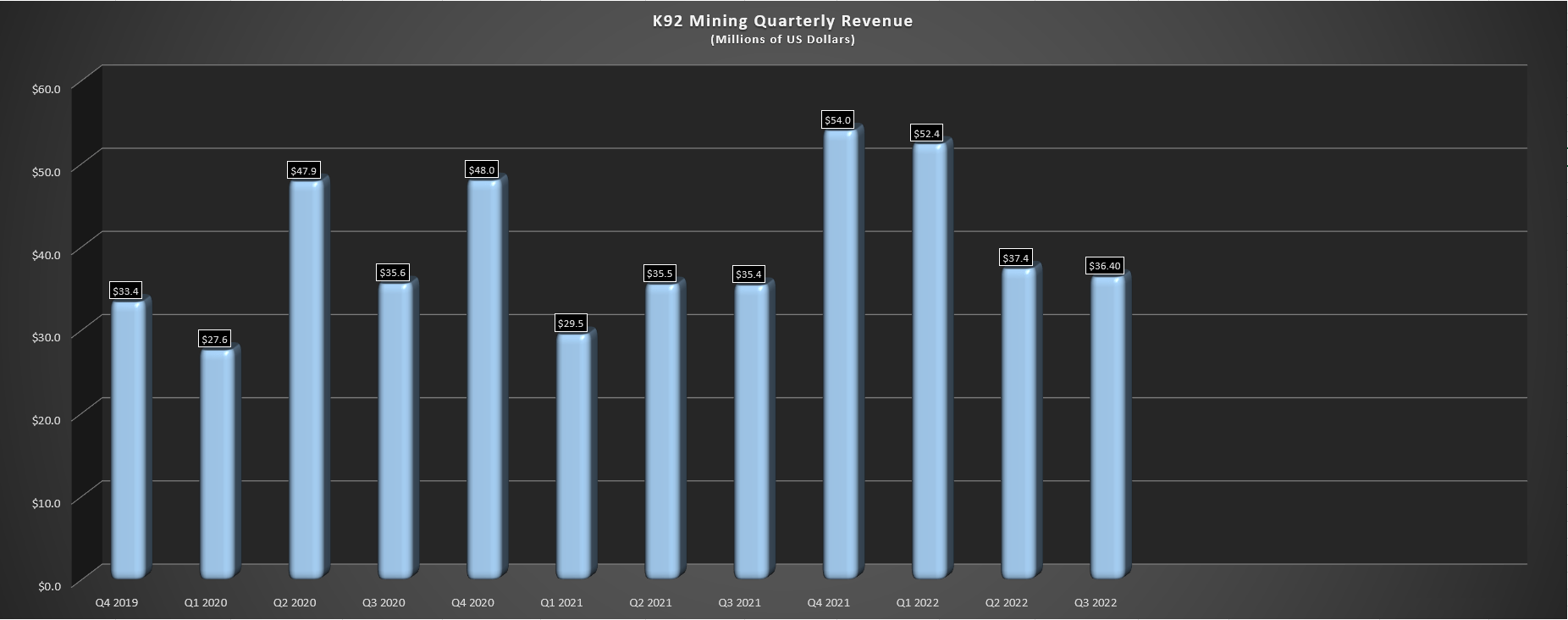

K92 Mining – Quarterly Revenue (Company Filings, Author’s Chart)

Meanwhile, digging into margins, cash costs and cash operating margins actually improved considerably on a year-over-year basis ($503/oz vs. $596/oz), a deviation from K92’s peer group, with the sector impacted by inflationary pressures and weaker gold prices. K92 Mining managed to buck this trend as it benefited from economies of scale (Stage 2 Expansion and imminent Stage 2A Expansion). However, we did see a drag on all-in-sustaining cost [AISC] margins, with increased AISC ($909/oz vs. $752/oz) and a lower gold price. This was related to a sharp increase in sustaining capital in Q3, higher G&A (increased corporate hires and higher management fees/wages), fewer ounces sold than produced, and a lower gold price.

K92 Mining – Gold Price, AISC, AISC Margins (Company Filings, Author’s Chart)

Fortunately, while AISC margins dipped in Q3, they were still above the industry average at $754/oz. Plus, full-year all-in-sustaining costs are set to come in below K92 Mining’s guidance mid-point of $930/oz, assuming we see a strong finish to the year. Plus, if we step back and look at the big picture, K92 Mining should enjoy sub $700/oz all-in-sustaining costs post-2024 with its Stage 3 Expansion or sub $650/oz costs in its Stage 4 Expansion scenario (1.7 million tonnes per annum). Hence, if costs are a little higher over the next several quarters as it sees increased spending for its major expansion, I don’t see this as that material to investment case here, which is owning a 300,000-ounce plus per annum producer with $1,000/oz plus AISC margins.

Recent Developments

Moving over to recent developments, there were several, with the three major ones being the following:

- the Stage 2A Expansion run rate looks beatable, with it already achieved on an annualized basis with August throughput rates

- the recent extension to its mining lease [ML 150] to June 2034, reducing any uncertainty that might have stemmed from Barrick’s (GOLD) situation at Porgera, also in Papua New Guinea

- continued exploration success, which looks to be uncovering a much larger mineralized footprint at its Kainantu Mine

Beginning with the Stage 2A Expansion, investors might recall that K92 Mining chose to go ahead with a Stage 2A Expansion (500,000 tonnes per annum vs. 400,000 tonnes per annum) to take advantage of its higher mining rates and to aid in funding the planned Stage 3 Expansion. As of August, the company has already reached its planned Stage 2A Expansion rate on an annualized basis (1,373 tonnes per day), which suggests that, like the Stage 2 Expansion, the Stage 2A Expansion may also outperform nameplate capacity. K92 Mining noted that the flotation expansion is planned for Q1 2023, and this is also expected to boost metallurgical recoveries. So, with a lift in recoveries in 2023 and a possible ~540,000 tonne per annum throughput rate, we could see a ~150,000 GEO year from K92 Mining (a 22% increase from FY2022 estimates of 123,000 GEOs).

On the mining lease front, this is a huge positive for the company, given that there might have been some anxiety that terms might be renegotiated after the difficult time that Barrick has had with its Porgera Mine. Instead, we’ve seen a meaningful extension to K92’s mining lease more than 18 months ahead of the original expiry date, suggesting clear support for this mine by the PNG Government. This is undoubtedly solid news for a company undertaking a very large expansion that had to get approved to justify its premium valuation. In addition, it could lead to some expansion in K92 Mining’s multiple, given that investors can breathe a sigh of fresh air and don’t have any major worries from a permitting standpoint over the next decade.

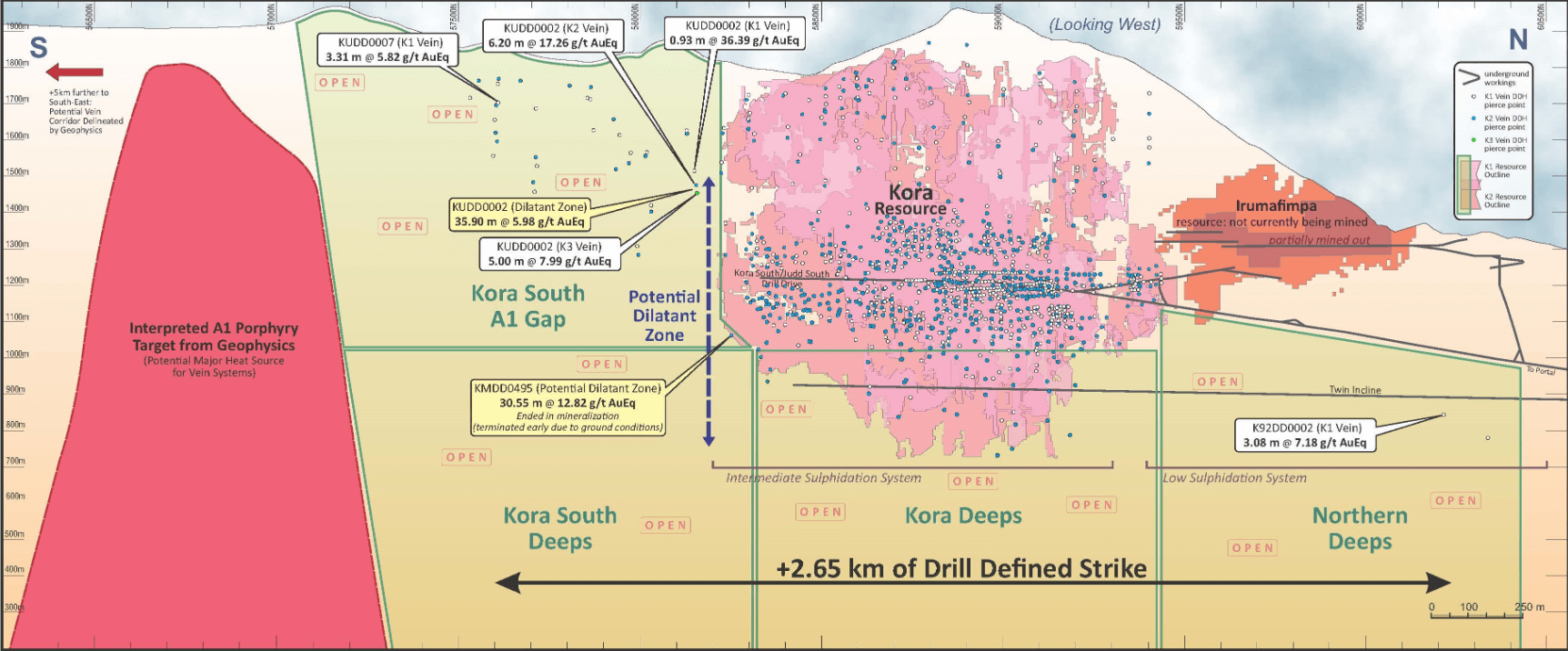

Kora Resource & Expansion Drilling (Company Website)

Finally, on the exploration front, K92 Mining reported several phenomenal intercepts from Kora, Kora South, Judd, and Judd South. It also reported a significant step-out north of its Kora resource base and below Irumafimpa. Beginning with Kora South, the highlight hole of 30.55 meters at 12.82 grams per tonne gold-equivalent (11.50-meter true width) is above the average resource grade and ended in mineralization, suggesting the potential to grow this resource further to the south, with this being its southern-most hole drilled at depth. Meanwhile, closer to the surface, K92 Mining hit multiple solid intercepts, which could potentially extend Kora 600 meters to the south, representing a 60% increase in the strike since the Q4 2021 resource update.

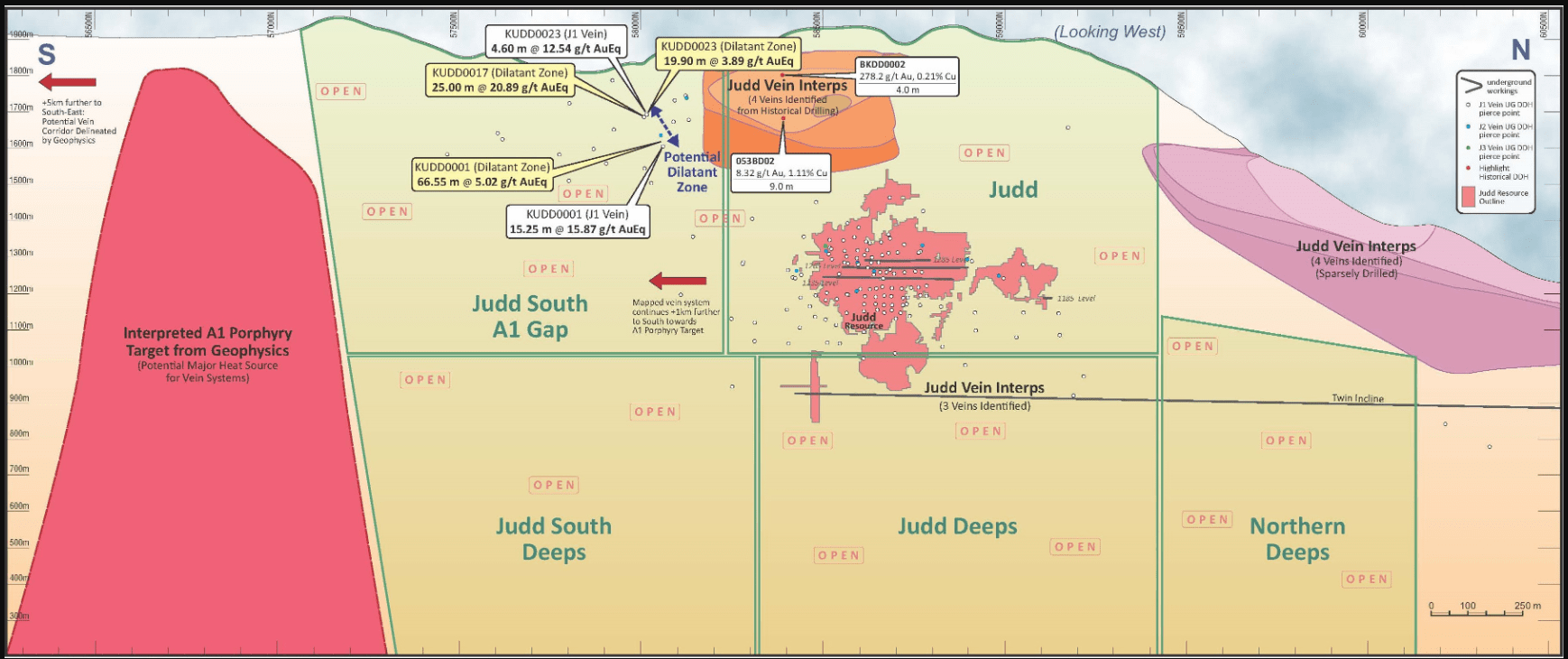

Judd Resource & Expansion Drilling (Company Website)

As for Judd, its resource is much smaller than Kora, but K92 Mining has had similar success stepping out to the south. The highlight hole was 25.00 meters at 20.89 grams per tonne gold equivalent, double the average resource grade over a true width of 17.69 meters. This incredible intercept confirmed additional mineralization up-dip from the thick intercept of 66.55 meters at 5.02 grams per tonne gold-equivalent, and additional drilling near-surface has extended the strike by up to 600 meters to the south here as well. When it comes to the future of Jud and based on the success of drilling to date (high hit rate at solid grades) and the fact that mineralization remains open in several directions, it’s looking like the resource base here is set to grow considerably in time for the major expansion post-2025.

Valuation

Based on ~242 million fully diluted shares and a share price of US$5.70, K92 Mining trades at a market cap of ~$1.38 billion and an enterprise value of $1.27 billion. Comparing this figure to an estimated fair value of ~$1.68 billion at $1,700/oz gold with $350 million assigned to exploration upside and $130 million in corporate G&A leaves K92 Mining trading at a P/NAV multiple of 0.82. I would normally consider this a steep valuation for a single-asset producer in a non-Tier-1 jurisdiction. However, with an industry-leading growth profile, an orebody that continues to surprise to the upside, and the positive news with an extension to its mining lease, I think K92 Mining can easily command a multiple of 1.0x – 1.2x P/NAV.

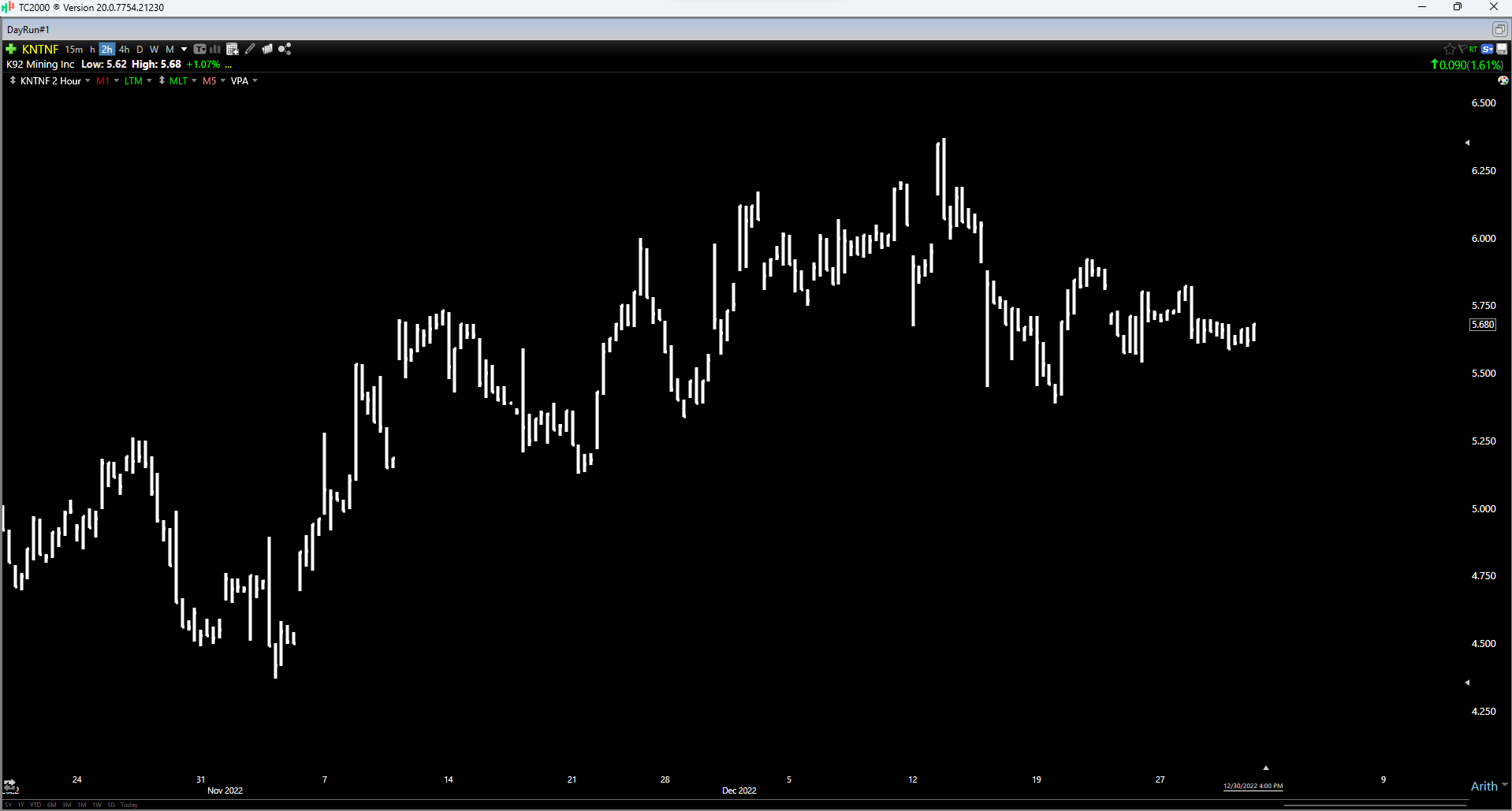

Using a 1.10x P/NAV multiple, I see a fair value for K92 Mining of ~$1.83 billion [US$7.56], which translates to a 33% upside from current levels. That said, I prefer a minimum 30% discount but, ideally, a 35% discount to fair value to justify buying single-asset producers. At a share price of US$5.70, KNTNF doesn’t quite meet this criterion with an ideal buy zone of US$4.90 or lower. So, while I see K92 Mining as a very solid buy-the-dip candidate and a top-3 growth story, I don’t see the stock in a low-risk buy zone, and it’s hard to entirely rule out the stock filling its gap at US$4.60 before making a sustainable bottom on its chart.

KNTNF Daily Chart (TC2000.com)

Summary

K92 Mining is one of the few producers that has continued to fire on all cylinders. Not only is it meeting its promises and consistently hitting new records, but it looks to be in a position to finance a massive growth plan with limited share dilution (just a single capital raise done last year) due to its Stage 2A Expansion which will boost cash flow to fund the expansion. If K92 Mining is successful, we could see production grow from ~123,000 GEOs in 2022 to 400,000+ GEOs in FY2026, translating to a ~35% compound annual production growth rate, with this nearly unrivaled within its peer group. In fact, the only company with a similar profile is i-80 Gold (IAUX) at a ~51% CAGR, but it is benefiting from starting from a lower base than K92 Mining.

Given this impressive growth profile combined with meaningful margin expansion and that K92 Mining is arguably one of the top exploration stories sector-wide with consistent resource additions, I continue to see the stock as a top-12 producer. However, the goal is to invest in great companies when they’re hated. And while K92 Mining is certainly less loved after the stock has consolidated for two years, I continue to see more attractive bets elsewhere in the sector from a valuation standpoint. That said, if K92 Mining were to dip below US$4.90, I would strongly consider starting an initial position in the stock.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Be the first to comment