RiverNorthPhotography

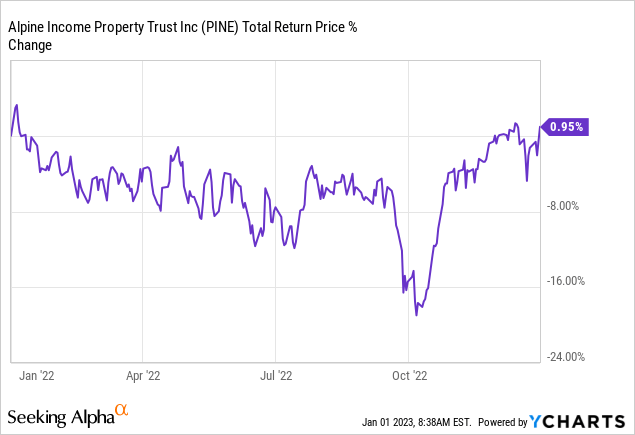

Volatility is the word I’ll pick to describe how I think 2023 will turn out to be for most stock market investors as the core macroeconomic themes that drove the performance of the stock market in 2022 all come to head this year. The Fed is set to increase rates to 5% to 5.25% with a series of 25 basis points hikes, inflation will likely experience a marked decline and all the currently lagging economic indicators of a recession will no longer be lagging. Making a pivot to REITs and income investing more specifically helps smooth out expected volatility by bringing in a calculable level of return before an investment is made.

Alpine Income Property (NYSE:PINE) is a micro-cap triple-net lease REIT with a diversified portfolio of single-tenant occupiers across retail properties. The company counts 7-Eleven, Lowe’s (LOW), and Walmart (WMT) as tenants. The portfolio is large with 149 properties spread across 35 states and with its total portfolio square feet at 3.7 million. Further, occupancy is currently running high at 100% as 53% of its total annualized base rent of $41.8 million comes from investment-grade rated tenants.

A High Yielder For A Possibly Tumultuous Year

REITs have to return 90% of their taxable income to investors in the form of dividends, hence, they employ a lot of leverage to scale their targeted return rate across as many properties as they can so their taxable income base can grow year-over-year. This drives the increases in dividends income investors crave. At the core, this requires the REIT to employ leverage at a cheaper base than its overall income. Hence, most REITs suffered in 2022 as interest rates were hiked to new highs to create an environment where variable debt became more expensive and the returns on new acquisitions came under pressure.

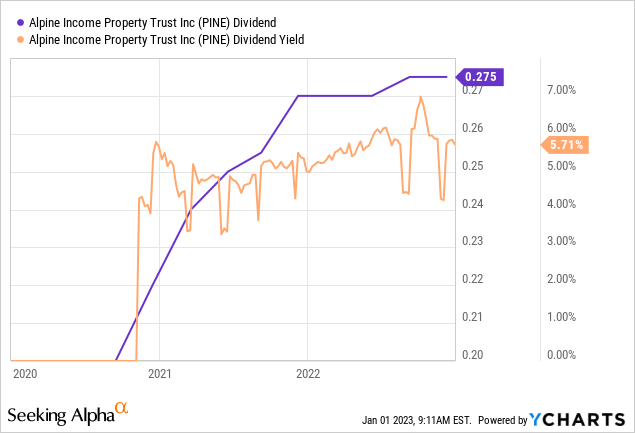

Whilst the REIT is relatively young as it only went public in November 2019, it has still managed to build an attractive dividend history as its payout was not only maintained during the pandemic but increased. The REIT’s last declared quarterly per share cash dividend payout of $0.275 was a growth from $0.20 when it went public. This means a 5.76% dividend yield on the current price of the commons.

The yield, of course, is a function of price and Alpine Income’s common shares have broadly traded in a range where its yield has held steady at just below 6%. The primary objective of an income investor is stable growing course income, so assessing the health of this payout against the volatility expected this year is important.

The Dividend Is Covered And FFO Is Growing

The Winter Park, Florida-based REIT last reported earnings for its fiscal 2022 third quarter. This saw revenue come in at $11.53 million, an increase of 41% from $8.17 million in the year-ago quarter. This also exceeded the consensus of $10.52 million and came on the back of the REIT’s extremely active property acquisition and disposal strategy. Management is targeting not less than $170 million in total acquisitions for fiscal 2022 with disposals of between $150 million to $170 million being targeted.

Alpine Income’s per share FFO during the quarter also came in ahead of expectations at $0.40 versus consensus estimates of $0.38. This was also higher than its FFO of $0.37 in the year-ago quarter. This more than covers the last declared FFO per share and also comes as guidance for FFO was revised up for the full fiscal 2022 by $0.13 per share at the low end to be between $1.73 to $1.75 per share.

However, the REIT is not without risks. Firstly, I’m not a fan of overly active asset recycling strategies as it embeds execution risks into what’s otherwise a safe and predictable asset class. Secondly, with a debt-to-capital ratio of 51.83%, the REIT employs a level of leverage that’s 6.1% higher than its peer group median. Whilst the difference to the median is somewhat marginal, not all its debt is fixed and the company just implemented interest rate swaps to hedge its overall exposure to Fed rate hikes. Bulls would be right to state that Alpine Income has no debt maturing until 2026 and that following the swaps, the only unhedged debt is a new $250 million revolving credit facility. Further, the company ended the quarter with net debt to pro forma EBITDA at 8.3x, which is entirely manageable.

The biggest risk comes from its external management structure. This is the key reason why it trades at 0.97x its book value, 32.5% lower than its peer group median. The mix of a quality tenant base, a 100% occupied property portfolio, and a near 6% dividend yield makes Alpine Income a good consideration for 2023 for shareholders who don’t mind an externally managed REIT but I’m not a buyer.

Be the first to comment