designprojects/iStock via Getty Images

Joby Aviation, Inc. (NYSE:JOBY) has made truly fantastic progress in demonstrating the capability of its S4 eVTOL (electric vertical takeoff and landing) aircraft. 2021 was a standout year, as the S4 delivered performance figures that many, including me, thought could not be achieved with existing technology. The S4 demonstrated a speed of over 200 mph, and it flew for more than an hour, covering 155 miles. This was the longest flight of any EVTOL and the fastest speed so far achieved by a commercially orientated eVTOL; it also flew at more than 11,000 feet, well above the stated specification.

These performance records were set at a U.S. Army site in California; Joby has contracted with the Department of Defense under an initiative to understand the potential capabilities of electric flight and work towards authorization.

These achievements are worth putting into context; the US military operates the Bell Helicopter (TXT) Bell 505 Jet Ranger X Helicopter, with a top speed of 125 mph and a range of 300 miles, and The Boeing Company’s (BA) little bird helicopter gunship, with a top speed of 144 mph and a range of 179 nm.

Joby intends to use this aircraft to run an eVTOL taxi service. They have ambitious plans. If successful, they will potentially be a +$100 billion company. In this article, I will try to assess their chances and look at the problems ahead.

The eVTOL Market

Whenever I start to look at a new industry, I look at three things

- The potential size of the market

- The field of competitors

- The key goals that might lead to success

It allows me to focus my thoughts and pick out a likely winner. It is a good strategy and has enabled me to avoid serious harm to my portfolio.

The air taxi services is estimated to be growing at a CAGR of 35% and reach $50 billion by 2026. The market for eVTOL aircraft is forecast to be around $30 billion by the end of the decade.

eVTOL is an enormous new market that will take significant market share from trains, taxi companies, and all sorts of public transport. It may reduce the need for car ownership and is a genuinely disruptive technology.

I identified six companies I might be interested in (I invest in smaller companies with disruptive tech). I compared them to three legacy airline manufacturers working on similar products.

You can see some of the work here: EVTOL_Review.xlsx

The airplane and its certification process

The number of EVTOL aircraft is almost as big as the potential market. The airplanes come in 5 types:

i) Vectored Thrust

Using the same thrusters for lift and cruise, 220 aircraft of this type;

ii) Lift and Cruise

Separate thrusters for lifting and cruising, 106 of these;

iii) Wingless Multicopters

Thrusters for lift only, 172 of these;

iv) Electric RotorCraft

Essentially electric helicopters, 43 of these;

v) Personal flying devices

Essentially hoverbikes and the like, 97 of these.

Source: EVTOL news eVTOL Aircraft Directory a fantastic source for all eVTOL facts and figures.

Joby is developing the S4: a five-seater air taxi of the vectored thrust variety. (One pilot, four passengers). It can reach speeds of 200mph, and its Lithium-nickel-cobalt-manganese batteries give it a range of 150 miles.

It has a distributed electric propulsion drive (Nasa: Leading Edge Asynchronous Propeller Technology: LEAPTech).

When comparing the aircraft and its competitors, you must remember that it is an aircraft. How long it takes and where it flies from are crucial. Passengers do not care about the tech. An Airbus or a Boeing jet? Passengers are agnostic. Same for taxis, Hondas, or Toyotas; unimportant, and who even knows who made the train they are traveling on?

A 36-engine e-jet from Lilium (LILM) or a six-propellor e-copter from (JOBY), it will not matter as long as it gets you where you want to go quickly, cheaply, and safely.

In this regard, the aircraft from all of these companies are comparable; they have four passenger seats, fly at around + 150mph, and have a range of 200 miles. Everything else is just marketing.

Technological Progress

For a long time, Joby was very secretive about what they were planning. Behind closed doors, they were developing their flying taxi. Since 2015, they have made over a thousand test flights of the various versions (subscale and full scale). Some of their competitors have only just begun testing, and some have not yet taken to the air. Joby is ahead of the game now and will likely be first to market.

The technical problems faced by the eVTOL makers are substantial. Takeoff and landing are very energy-intensive, and cruising requires constant, reliable power. Johann Bevirt (Founder of Joby) is the lead on the technical side. He has said that Joby can meet its flight objective using automotive-grade batteries. Other companies have found this problematic (impossible) and have been waiting for 400 wh/kg batteries to make flight possible. Bevirt has said that Joby has painstakingly shaved ounces and improved aerodynamics and battery performance.

Has Joby solved the battery issue? Or will the final performance be less than currently suggested? It is a crucial issue, and it is hard to know for sure. I’m not particularly eager to take a founder’s word, but Joby is so secretive it has been challenging to come up with a definitive answer.

A search for patents revealed some interesting insights. Firstly, Joby Aviation has very few patents, far fewer than the competition. Some have interpreted this as meaning that Joby does not have the intellectual property to make this work. None of their patents seem interesting or game-changing; however, Joby Aviation, Inc. has over 20 patents. They cover critical issues like calculating airspeed (apparently very difficult to do) and running an air shuttle service. Even more interesting are the 60 or so patents registered to JoeBen Bevirt, the Joby founder; these patents seem to cover the more critical tech relating to Battery Management systems, flight control, and eVTOL aircraft.

I am not an engineer, but the patents imply that Joby has developed an external battery cooling system that plugs in when the aircraft is recharging, and also developed innovative ways to cool a battery in flight. This tech would significantly reduce the weight of any potential vehicle and potentially increase the battery’s efficiency.

Finally, we were told in the latest earnings conference call that the recently crashed prototype had flown well beyond the range, speed, and height of the envelope testing. So I think it is safe to assume that Joby has solved the battery issue.

With separate demonstrations of speeds well above 200 mph, ranges beyond 150 miles (240 km) and altitudes up to 11,000 ft (3,350 m), it is clear that the five-seat Joby S4 has capabilities significantly beyond the “limited performance” that had been expected from eVTOL aircraft for so many years.

Source EVTOL News

Patents here for Bevirt: Search Patents – Justia Patents SearchPatents, and here for Joby Aero Inc.: Search Patents – Justia Patents Search.

The Joby Business plan

The eVTOL market competitors have two choices:-

- Manufacture the aircraft and sell them to operators

- Manufacture the aircraft and operate them yourself

Joby is most definitely taking the second option, and they are unique in this regard. They intend to be an air-taxi company and be fully operational across the US before any competitors are in the air.

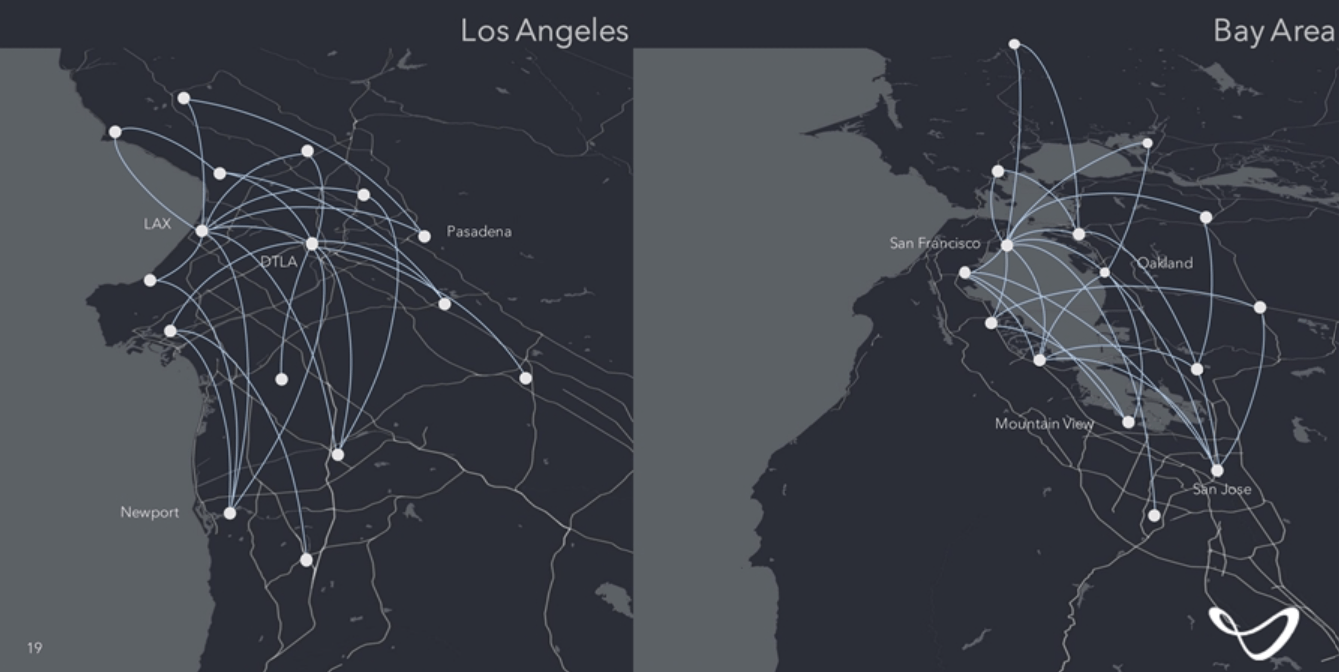

Joby planned routes (SEC.gov Joby slide show)

First-mover advantage always matters, and being the first mover in an entirely new industry will bring significant gains.

Joby intends to be an airline in the U.S., but is partnering with other companies outside of the U.S. Last quarter, they announced agreements with ANA Holdings in Japan and SK Telecom in South Korea.

Joby has announced a presence in the UK and has been working with regulators there for more than a year.

Joby Certification Progress To Date

We received an update on certification at the Q4 2021 earning call (March 2022). Joby needs to have three types of certifications – for the aircraft, the manufacturing process, and the airline – for its business plan to be anything other than a plan.

Joby reported that they had completed 70% of the certification process (signed off and accepted) for the aircraft, and they remain on target to have this complete in the second half of this year. In the last quarter, Joby received the formal sign-off from the FAA regarding their plans for completing the process.

In terms of manufacturing certification, the first stage was passed following a formal inspection. The FAA has also accepted Joby’s quality control manuals, meaning they can move towards building a production prototype for final assessment.

Excellent progress was made with the aircraft carrier certificate. Joby has moved into the fourth of five certification stages and expects to complete the process in 2022.

The takeaway here is that Joby is on target to have everything certified this year. The aircraft, the manufacturing, and the airline. Joby is years ahead of the competition. Certification is the crucial step in being able to fly customers; they have been flying for five years, have chosen their route to certification, and are moving swiftly along the path.

Joby Manufacturing

Toyota (TM) is a leader in automotive battery technology, and they seem committed to the Joby plan. Joby partnered with Toyota early in its life cycle and has used the Toyota engineering team extensively, along with the $400 million of funding Toyota provided. Toyota is the largest non-founder shareholder with more than 12% of Joby shares; interestingly, the second place goes to Intel (INTC), which has more than 8%. A good pair of companies to have on board.

The plan is to mass-produce Joby aircraft the same way as Toyota mass produces cars. This is unheard of in the aviation space. Planes usually are individually manufactured, not mass-produced. FCA certification requires more exacting safety standards than automotive production; it remains to be seen if the Joby-Toyota partnership can do this.

We heard that the first production aircraft would roll off the production line this year during the earnings call. Seeing this first production plane in the skies will be a big step forward and might be a catalyst for a share price surge.

The Joby Taxi Service

UBER Technologies (UBER) opened an air taxi service called UBER Elevate in 2016; it was shuttered during the pandemic. UBER Elevate brought together regulators, real estate companies and operators with a common goal of developing an air taxi service for residents of large urban areas.

In 2020, UBER sold Elevate to Joby. As part of the deal, UBER invested $75 million in Joby (Uber also disclosed it had previously invested $50 million).

The team at Uber Elevate has already developed the necessary software to run an air taxi service and has been through the regulatory hurdles to ensure that the air taxi service will be ready as soon as the aircraft is. It is another example of how far ahead Joby is relative to the competition.

Joby Finances

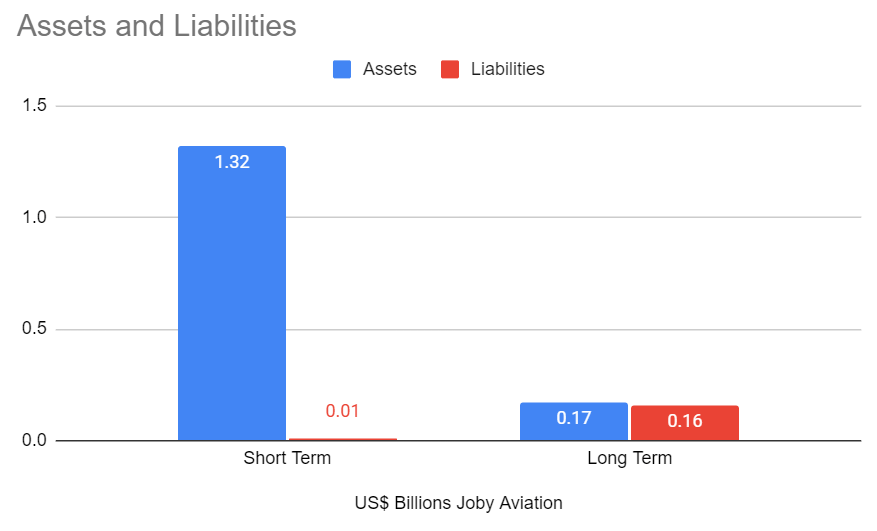

As with most recently launched public companies, they have solid finances with more than three years of cash at hand and no debt.

Joby Balance Sheet (Author generated data from seeking alpha)

With a $1.3 billion cash pile, the company is immune from short-term issues and is unlikely to need to raise capital in the near term.

It would not be easy to calculate reliable DCF for the Joby taxi service. Too many of the costs are unknown. Instead, I have relied on the information contained in the initial SPAC document to come up with a future valuation based on revenue.

Forecast Revenue Joby Airline (Joby Prospectus, Author generated)

The full prospectus is available here. All figures came from the prospectus and the earnings call already linked.

If the taxi service pans out the way JOBY expects, then this company will be worth $100 billion by 2030. Its current valuation is around $3 billion.

The markets are always forward-looking so we can expect Joby to meet that valuation well in advance of 2030. The rise in share price will likely come in jumps as Joby meets particular milestones along its path to complete commercialization. The following is a list of the crucial milestones that will drive the price higher (dates are mine).

- Certification of the Aircraft (probably Q4 2022)

- Accreditation of the Manufacturing process (Q1 2023)

- First commercial flight (Q2 2023)

- Establishment of the first US hub (Q3 2023)

- Entire commercial operation of first Hub (Q1 2024)

- Establishment of the first international hub (Q3 2024)

Risks

The risks are substantial and go roughly like this.

- Certification does not arrive; this is the most significant. It is game over should it happen. In my view, the authorities have gone too far down the track to withhold authorization completely.

- Another company gets certified before Joby. They are currently the frontrunners, but they are not the only horse in the race. If another company gets there first, Joby will be in significant trouble, and it will not reach the values I have forecasted.

- People do not buy the service. I find this hard to imagine if Joby can get the price and the routes right, but it is a possibility.

Conclusion

Joby had an amazing 2021, they have made technical and regulatory progress that puts them a long way ahead of the competition. They have proved that their aircraft can meet the performance criteria they laid out in their offer document and are building out their manufacturing and airline infrastructure.

Joby has partnered with quality companies to run their manufacturing and their international services.

They have done all of this and maintained their enormous cash pile.

If Joby can deliver on the rest of the plan and have an operational eVTOL air taxi service roughly in the timeline laid out in this article, they could be worth more than 30 times their current value. Joby have suggested that they will run an air taxi service in every large City in the US, charging the same price as an UBER X, and that they can make a 58% margin on that service (58% source: Prospectus previously linked).

I have bought shares in Joby and will add to that position as they reach important milestones. I hope to be fully invested early 2023 and hold the shares for 2 years.

Be the first to comment