Jonathan Kitchen

The iShares Russell Top 200 Growth ETF (NYSEARCA:IWY) features a pretty heavy skew towards tech stocks which are typically the banner for growth stocks. As such, compared to a more broad bet on the S&P with the iShares Core S&P 500 (IVV), the IWY is going to be more levered to risk sentiment, reflected by its YTD performance of -30%. We think that it’s a better risk reward given economic data which is increasingly pointing to the likelihood of a Fed pivot. Inflation is down, as are inflation expectations, and further factors support macro data for the US in particular. We think that the time is coming soon for a return to vigor of growth stocks.

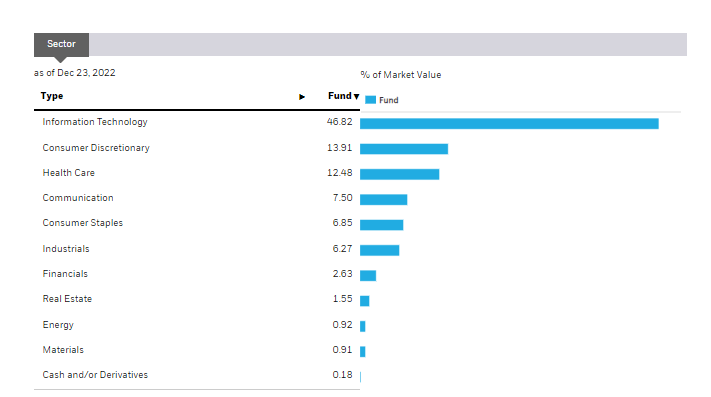

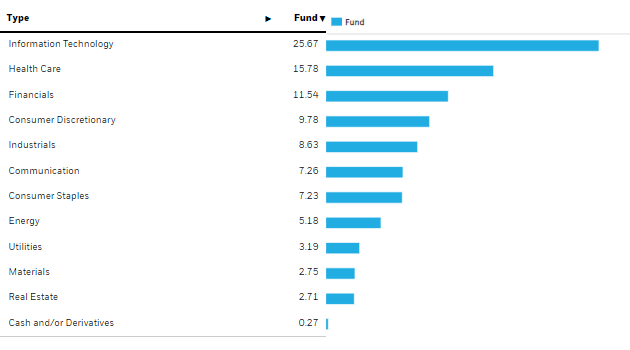

IWY Breakdown

The IWY has generally similar exposure to IVV, but from categories like consumer staples, industrials and financials, the allocations have been shifted meaningfully to tech.

IWY Sectoral Exposures (iShares.com)

IVV Sectoral Exposures (iShares.com)

A 46% exposure of course is consistent with the growth mandate, which would overrepresent US tech which was and still remains an overwhelming source of valuation in the US markets.

While IWY is still a directionally value-weighted ETF, with exposures like Apple (AAPL), Microsoft (MSFT) and Amazon (AMZN), i.e., the megacaps, featuring heavily with 14%, 13% and 5% weights respectively, it appears that almost all tech exposures have been doubled in exchange for carving out allocation from other less growth oriented categories.

Bottom Line

The upshot of this is that the IWY ends up being quite a bit more levered to market movements than the typical IVV which naturally benchmarks at a 1x Beta. While megacap exposures are the market, and therefore don’t really add to Beta for the IWY, they are driven by general equity sentiment more than value categories which have been rotated into from growth in these past months, with more marginal tech exposures being even more sensitively driven by risk-on sentiment. The YTD performance of -30% YTD for IWY relative to IVV, which is down 18%, accentuates this differential. The shorter term Beta is 1.22 for IWY, consistent with this.

What can we say about the likely risk sentiment over the next few months? While it’s impossible to say exactly, we feel that the need for further rate hikes is already limited. Inflation expectations are back to June 2021 levels, and inflation in general is easing further. This is before we’ve even lapped the really high inflation quarters in early 2022, especially those after the invasion. Traders are receiving this information well, but not enough according to us. Moreover the relative misfortune of the EU and China actually cushion the USA landing by taking their own feet off the economic pedals before the US has to fold. Everything comes in cycles, and as time passes it’s more likely that growth could become vogue again.

On the other hand, geopolitics is still a factor. If nuclear weapons are deployed in Ukraine the markets will tank, and Europe will sacrifice more of its economy for defense considerations, and the inflation from further spiraling of the East-West relationship will put renewed pressure on markets. We are still not out of the woods there, and this would be the main reason to be careful.

Thanks to our global coverage we’ve ramped up our global macro commentary on our marketplace service here on Seeking Alpha, The Value Lab. We focus on long-only value ideas, where we try to find international mispriced equities and target a portfolio yield of about 4%. We’ve done really well for ourselves over the last 5 years, but it took getting our hands dirty in international markets. If you are a value-investor, serious about protecting your wealth, us at the Value Lab might be of inspiration. Give our no-strings-attached free trial a try to see if it’s for you.

Be the first to comment