Midnight Studio

Since last November’s market top, the true unraveling has taken hold throughout 2022. The euphoria-driven craze has finally come to a halt, despite the illusion that stocks could continue their seemingly perpetual trajectory of “up and to the right.”

In reflecting on what has been a turbulent year, it is worth recognizing this great reset for what it is: a stripping of the fat and an eradication of the frothiness that came to embody what was yet another coming – and surely not the last – of Tulip mania. Just as building muscle requires generating muscle tears in one’s muscle fibers, so too will this pain ultimately benefit those who embrace the short-term pain and learn from – to borrow from Lux Capital’s Josh Wolfe – yesterday’s “excess of excesses.”

We’re no exception here at CC, as we’ve had to digest our ration of humble pie. We mistook our fair share of momentum-driven companies as fundamentally sound, robust business models. While some picks have outperformed even our most optimistic expectations (i.e., IT), others that showed plenty of potential (i.e., ROKU) have been significantly beaten down over the past couple of months and continue their freefall.

It is a fascinating aspect of human nature that, though we may know many things to be objectively true (i.e., advice, words of wisdom, etc.), we willingly choose to disregard them. Is such a defiance a marker of our volition? If so, such plain noncompliance does not seem very profound – or free for that matter – to begin with.

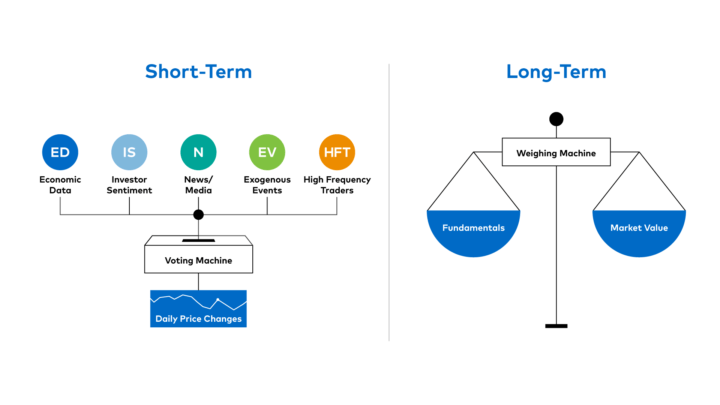

In that vein, we find ourselves returning to Ben Graham’s appraisal of the stock market:

In the short run, the market is a voting machine, but in the long run it is a weighing machine.

Though simple, this is a potent metaphor that is often misunderstood or not fully grasped. Polen Capital’s excellent article visually elucidates Graham’s point.

Pollen Capital

It is also worth highlighting that the voting machine works in both directions. At peak market activity, stock prices are a phantasmagoria underpinned by the naivete that someday, far far away, the company’s fundamentals will finally show just cause for exorbitant valuations. This is a cycle that has repeated itself countless times and, again, we can count on its reoccurrence.

Conversely, market crashes lead to widespread panic and forced selling, which can precipitate a spiraling that is equally baseless in the short term. The irrationality pendulum swings both ways, and in either extreme, a vicious cycle gives way to nonsensical behavior. But that’s the nature of the beast.

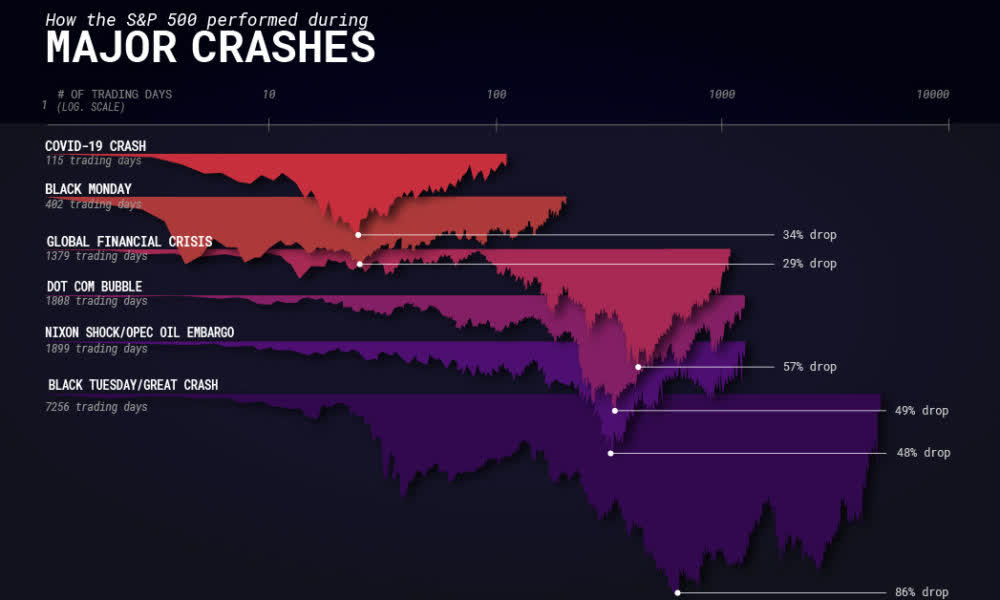

Like most challenging experiences, every market crash seems apocalyptic in the moment, only to be met by a nonchalant shrug when looking back. Taking a bird’s eye view, we can appreciate how the more significant crashes have impacted the market’s long-term growth trend.

Visual Capitalist

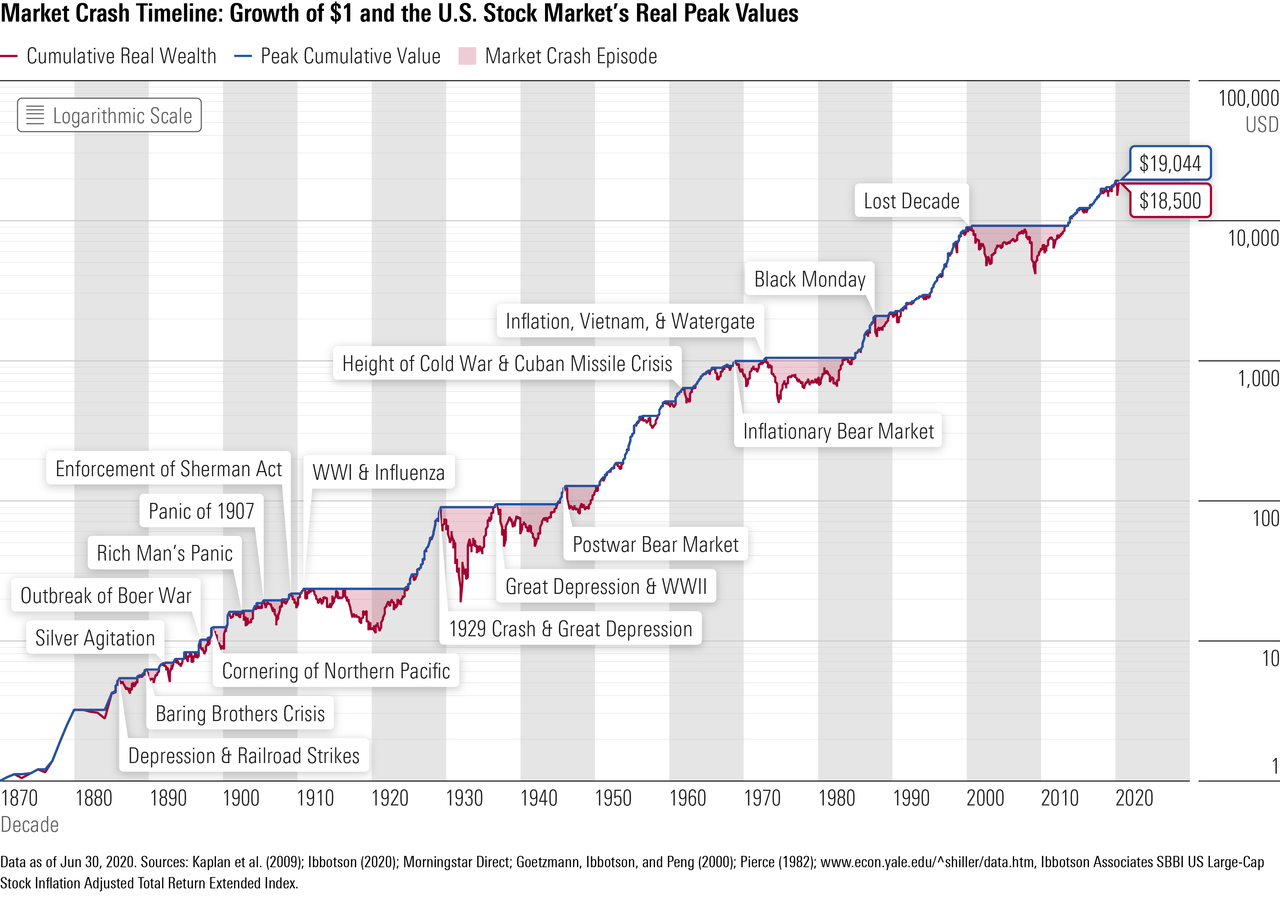

If we take a closer look, however, it is more reminiscent of Dan Carlin’s book, The End is Always Near. Something is always going on, and if we’re not careful, we’ll get sucked into the vacuum. The news cycle has a perverse incentive to fill the air. After all, if you were forced to report on something every day, wouldn’t you run out of things to say? Beware of perverse incentives and resist the urge to be absorbed by short-term volatility.

Morningstar

It’s anyone’s guess as to how long this tempest will draw out, and there have already been (false) cries that we’ve bottomed throughout the year. We’re all sitting around the poker table and waiting for those with terrible hands to fold. Yet, many are clutching to increasingly elusive hope that we’re bound for a rebound. It’s not a loss until you sell, right?

Forbes

The point is that though there may very well be a significant amount of pain left to be endured, it is important to remember that this too shall pass.

Gone are the days (for now) when monkey JPEGs traded for millions of dollars, crossover hedge funds disrupted venture capital, and a Ponzi scheme masquerading as a crypto exchange lacking basic accounting controls was valued at $30B.

Going forward, it would be wise to question the narrative more often, for a lie told often enough becomes indistinguishable from the truth. Adopting a full-blown pessimistic approach has its perils, however. Pessimists may sound both intelligent and eloquent, but it is the optimists who end up reaping the rewards. Again, a fine balance must be struck to generate alpha in the long run. To doubt everything is to believe in nothing, and is a surefire way to miss out on the next big thing.

Who could have predicted that a digital book retailer named Amazon would transform into a profitable, trillion-dollar behemoth underpinned by its cloud infrastructure arm? What about Google’s $1B splurge on a quirky video upstart dubbed YouTube that would go on to transform media consumption for an entire generation? Didn’t FB critics balk at a then 28-year-old’s decision to acquire a pre-revenue 13-person startup called Instagram – now one of the world’s most profitable ad-driven social graphs? The list goes on…

Examples such as these abound, and the reason they stand out is due to their immense accretive value that is only readily apparent in hindsight. No mean feat while in the thick of it, of course, but it is worth peeling an eye for companies uniquely positioned to succeed in times of uncertainty. The strategic moves that they might pursue today might seem counterintuitive-or borderline irrational-but they may very well represent the foundation of the compounding growth that is often associated with the aforementioned generational companies. Only time will tell.

There are headwinds ahead, no doubt. Rates continue to rise, inflation remains rampant, supply chains are under pressure, and an actual war with global ramifications drags on with no end in sight. The goal, then, is to think long-term and back companies that possess “antifragile”-like qualities regardless of existing and hitherto unforeseen macroeconomic events.

In the spirit of this prescient Mike Milken quote, it comes with the territory:

When your business depends on technology – whether it’s aerospace, computer and electronics firms in the 1960s or Internet, telecom and networking companies in the 1990s – volatility is a fact of life. Unlike slower-changing industries like supermarkets, which can appropriately assemble a balance sheet with more debt, technology is an inherently risky business and needs a strong balance sheet to survive. In fact, risk in capital structure should vary inversely with business risk.”

Now, staying invested in dismal names doesn’t mean you’ll just end up hitting breakeven at some point (just ask CSCO), and that’s why, for most investors, indices are the way to go. If, notwithstanding, stock-picking is still one’s poison, then it is crucial to identify and invest in quality names that will stand the test of short-term volatility.

As a follow-up to this article, we’ll delve deeper into names that satisfy these criteria and are poised to endure near-term fluctuations and emerge stronger on the other side. To many, these will seem like troubling times, but these are also analogous with great opportunities in disguise. Stay tuned as we attempt to uncover them.

Be the first to comment