SAND555

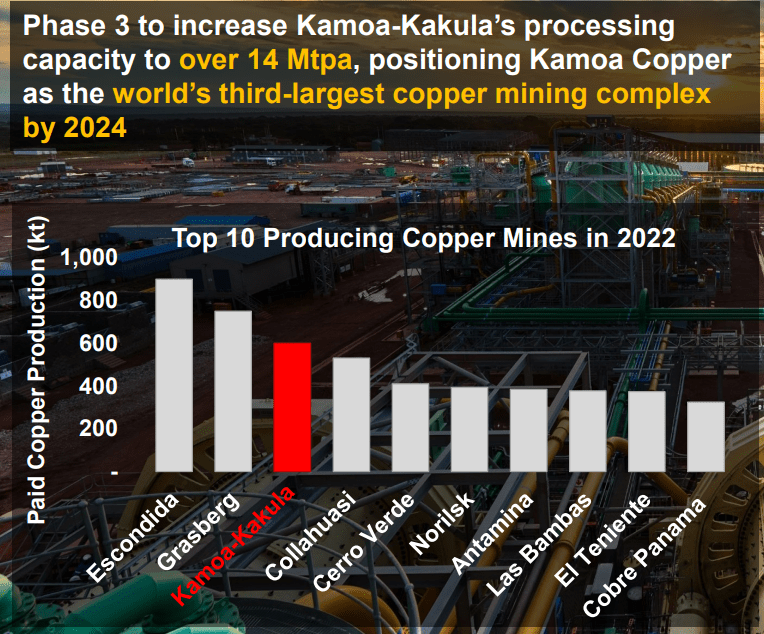

Ivanhoe Mines (OTCQX:IVPAF) is a mining company that is focused on producing copper and zinc in the Democratic Republic of the Congo and platinum group metals (PGMs) in South Africa. The company’s main projects are the Kamoa-Kakula copper mine in the DRC and the Platreef platinum-palladium-nickel-copper-gold mine in South Africa. Ivanhoe Mines owns 39.6% of the Kamoa-Kakula mine and 64% of the Platreef mine. The Kamoa-Kakula mine began production in 2021 and is expanding rapidly. The Kamoa-Kakula project has exceptional resource potential, including some of the highest grade mineable resources. Ivanhoe Mines plans to increase the mining rate at this project to 15 million metric tons per year, which would make the Kamoa-Kakula project one of the largest copper mining complexes in the world.

Ivanhoe Mines website

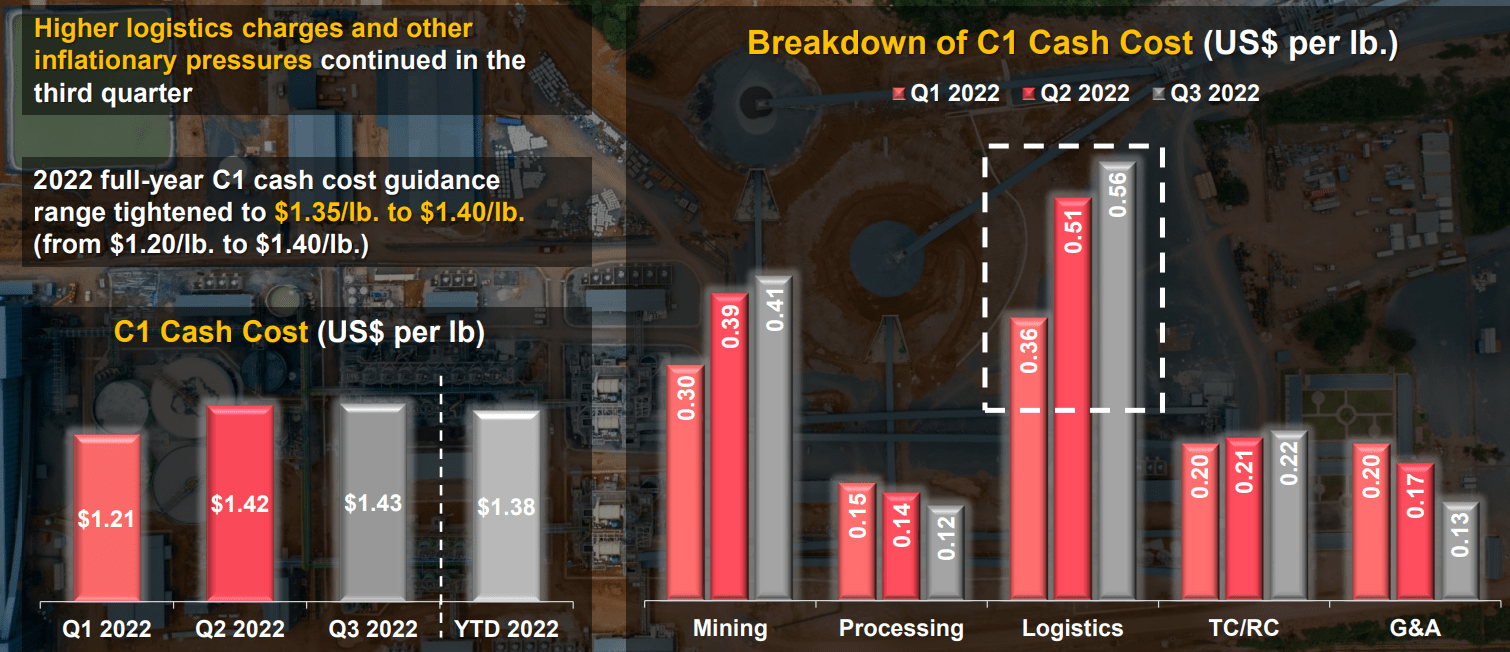

Ivanhoe Mines released lower-than-expected financial results for Q3 of 2022. While the company increased its production guidance for 2022, it also revised the mid-point of cost guidance upward by ~6%. However, the outlook for growth at the Kamoa-Kakula project remains positive. Ivanhoe Mines slightly improved its operating guidance for 2022 to 325-340 thousand metric tons of copper, and updated its C1 cash cost guidance to $1.35-$1.40 per pound. The company also decreased its 2022 capital expenditure guidance to $1.1 billion due to deferrals. A feasibility study for the planned Phase 3 expansion at Kamoa-Kakula is expected to be released in early 2023. As of Q3 2022, Ivanhoe Mines had $663 million in cash and cash equivalents and $667 million in debt, resulting in a net debt balance of $4 million. The increase in costs was due to some provisional pricing adjustments and higher logistics charges. Overall, Ivanhoe Mines revised its full-year 2022 C1 cash cost guidance to a range of $1.35 to $1.40 per pound, from the previous range of $1.20 to $1.40 per pound. Logistics challenges are expected to improve in the near future due to the reopening of the Lualaba smelter, which will reduce the volume of concentrate that needs to be shipped, and the opening of two new border crossings between the DRC and Zambia. In the medium term, Ivanhoe Mines anticipates a significant improvement in cash costs, between 10-20%, once it completes construction of the Phase 3 500,000 metric ton per year copper smelter at the end of 2024. The de-bottlenecking program at Kamoa-Kakula is about 70% complete and is ahead of schedule. This program aims to increase the combined processing capacity of the Phase 1 and 2 concentrator plants from 7.6 million metric tons per year to approximately 9.2 million metric tons per year. The de-bottlenecking program is expected to be completed in Q2 of 2023, which will increase Kamoa-Kakula’s annual production to approximately 450,000 metric tons of copper.

Ivanhoe mines website

Work on Phase 3 is progressing as planned. Basic engineering is complete and procurement is ongoing, as well as detailed engineering. Ivanhoe Mines is also advancing early construction work, including earthworks, which are 70% complete at the smelter site. The company is also making progress on the refurbishment of the Inga II turbine, which will provide an additional 178 MW of hydropower to support the expanded Phase 3 mine and smelter. The runner, the longest-lead item for the turbine refurbishment, is expected to be delivered by the end of 2023 and will improve the efficiency of the operation compared to the previous design. Engineering work is ongoing for the rest of the refurbishment equipment, and a study is being conducted to evaluate upgrades to the transmission infrastructure between Inga II and Kamoa-Kakula. The refurbishment of the smelter is on track for Q4 of 2024, which is the same timeline as the commissioning of the Phase 3 process plant and the smelter. During its quarterly call, management provided an update on the progress of exploration at Western Foreland as the 2022 drilling program nears completion due to the start of the rainy season. The drilling has been focused on regional targeting to define the limits of the roan sandstone, which is the host for Kamoa-Kakula style mineralization, as well as testing more advanced targets such as extensions to the known Makoko discovery and the Makoko West zone. In addition, management mentioned that two other advanced targets, Lupemba in the far southwest of the licenses and Mushiji, located 3km north of the Kamoa-Kakula mine license, were also tested. Ivanhoe was in the news for the wrong reasons recently in relation to the granting of licenses at Western Foreland. A story in the Canadian publication called “The Globe and Mail”, discussed a Royal Canadian Mounted Police (RCMP) search of the Vancouver office of Ivanhoe Mines in November 2021 in connection with $2.7 million in bank transfers from Ivanhoe to a Swiss bank account. The RCMP obtained the search warrant based on reasonable grounds to believe that Ivanhoe violated Canada’s Criminal Code and Corruption of Foreign Public Officials Act between 2014 and 2018. Ivanhoe cooperated with the search and no charges have been filed against the company or its directors or employees. The search warrant authorized the seizure of documents related to Stucky Ltd., Stucky Technologies, and the Democratic Republic of the Congo’s state-owned power company. Ivanhoe’s stock price dropped by about 11% on the Toronto Stock Exchange following news of the search. A significant portion of the report focuses on the issuance and timing of various exploration licenses and the process of converting those licenses into exploitation licenses. The licenses in question relate to the Western Forelands properties owned by Ivanhoe Mines, which are mostly in an early exploration stage and do not have active mining operations. The report specifically mentions the Western Forelands properties, which are valued at $750 million as potential option value for a future discovery. These properties make up approximately 6% of Ivanhoe Mines’ consolidated net asset value.

Ivanhoe released a rather long statement, which pointed at numerous “inaccuracies” in the reporting but it is suffice to say that there is remains ongoing uncertainty around the dealings of the company in the DRC. The DRC itself has proven to be a rather difficult place to work for Western companies as a result of significant corruption within the country. Corruption is a widespread problem in the Democratic Republic of Congo (DRC). The country ranks near the bottom of Transparency International’s Corruption Perceptions Index, with high levels of corruption in the public sector, including in the police, judiciary, and government. The extraction of the country’s natural resources, including minerals such as gold, copper, and diamonds, has also been plagued by corruption, with many officials and businesses profiting illicitly from the country’s wealth. This corruption has contributed to poverty and instability in the DRC, and has made it difficult for the country to develop and prosper. This has been to the detriment of Western companies who are forbidden from engaging in illicit practices and has benefitted the Chinese who have tend to view corruption as a cost of doing business. Lundin Mining (OTCPK:LUNMF) exited the DRC in 2017 by selling their stake in the Tenke mine to the Chinese as did Freeport-McMoRan (FCX) when it also sold its stake in the Tenke mine to the China Moly. Subsequently, Freeport also unloaded its undeveloped project in the DRC to the Chinese in 2020 to the Chinese, effectively exiting the country. A rather significant portion of Ivanhoe is owned by the Chinese in addition to the direct involvement on the project level. CITIC owns 25.9% of Ivanhoe while Zijin owns 13.6% of the company.

From an investor’s perspective, it is important to consider both the positive and negative aspects before making a decision. In my view, Ivanhoe is a good buy, but only at the right price. Currently, the company trades at a discount of around 15% to its net asset value compared to its peers such as First Quantum and Lundin Mining. While neither First Quantum nor Lundin operate in Tier 1 jurisdictions, they are considered to be in more stable locations than the DRC. On the other hand, Ivanhoe’s operations are of a higher grade and more profitable than either FM or Lundin. For my money, Ivanhoe becomes an attractive investment opportunity if its discount compared to its peers widens beyond 25% especially in light of the growth capital that needs to be spent this year. Given its historical volatility, it is likely that there will be opportunities to purchase Ivanhoe at lower prices in the future.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Be the first to comment