Matteo Colombo/DigitalVision via Getty Images

Investment Thesis

In searching for investment opportunities in Japan, we noticed ITOCHU (OTCPK:ITOCF) because despite its attractive 7-8x P/E, it was trading at a higher multiple than its Japanese trading company peers. Upon further investigation we found some nuances in its performance and valuations that we feel an investor looking for exposure to the Japanese economy or trading companies should consider.

The Company

ITOCHU is currently the second largest of the “Big 5” Japanese trading companies by market value, behind Mitsubishi Corporation (OTCPK:MSBHF). ITOCHU’s operations are divided into 8 segments, which are spread across industrial, manufacturing, and services sectors.

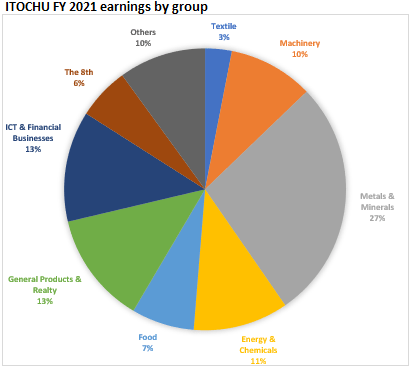

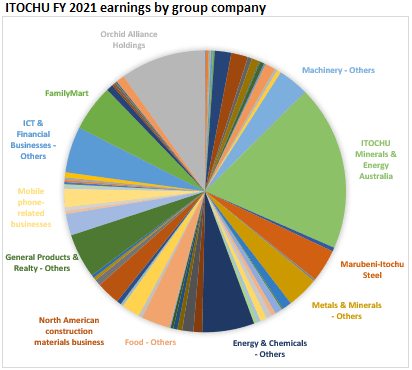

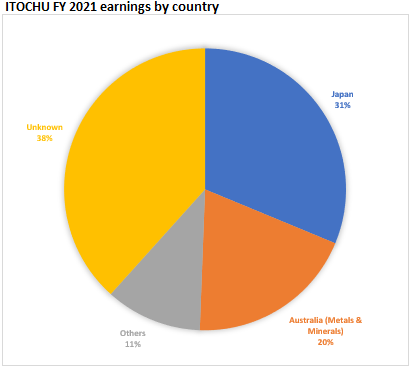

Well-distributed contributions by all business segments driving earnings (compiled from financial results presentation) Breakdown by top performing companies again shows contributions across the board (compiled from financial results presentation) Breakdown by country shows that ITOCHU is primarily focused on Japan (compiled from financial results presentation)

ITOCHU announced record earnings in Financial Year 2021 of JPY820bn. A breakdown shows a balanced contribution from all groups, although the Australian metals and minerals business (boosted by record high iron ore and coal prices) alone contributed a sizable portion. It is notable that the management communicates a “% of non-resources” metric (73%) in its results presentation – this reflects a clear intention not to be over-reliant on windfall gains/losses from commodity price volatility.

In attempting to break down top performing companies from each segment and better visualise overall strengths, we found it very difficult to pinpoint the key drivers of earnings. Instead, it appears that ITOCHU has assembled a sizable number of businesses across all areas that are contributing equally to overall earnings. The company itself states that 90.9% of its group companies reported profits for the year.

Similarly, attempting to breakdown profits by country also yielded inconclusive results, however we saw Japanese domestic businesses likely accounted for a majority of company profits. This led us to form an opinion that although not able to specifically identify where its strengths lie, ITOCHU is a well-balanced reflection of the Japanese business landscape.

Recently announced 2022 Q1 earnings of JPY231bn shows that 33% progress has been made against full-year management forecasts (JPY700bn). Upon analysing segment breakdown, on balance we see steady performance across segments, and predict the company is on track to realise full year forecasts.

ITOCHU is broadly on track to meet its FY forecast of JPY700bn after Q1 earnings of JPY231bn (compiled from financial results presentation)

Valuation

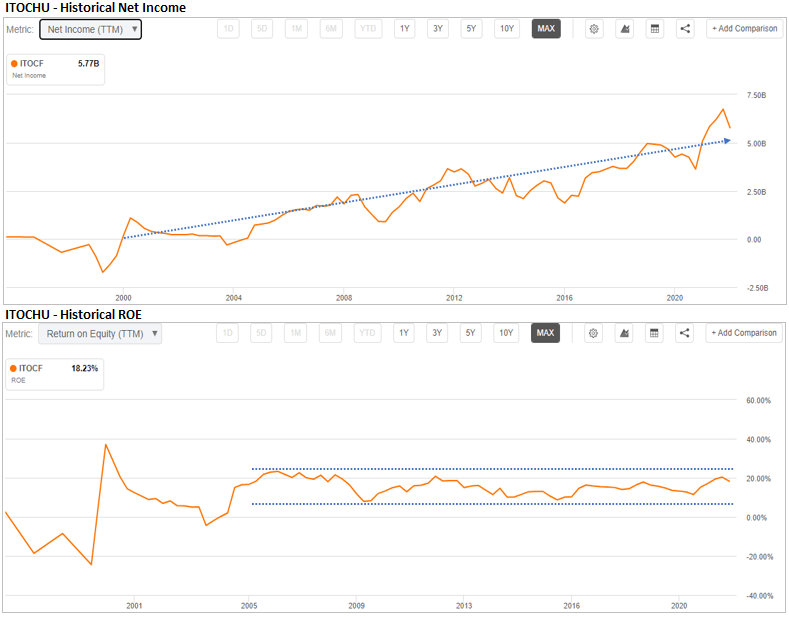

Analysis of historic performance reflects a company that has since 2005 shown a clear trend of progressively increasing earnings, as well as demonstrated resilience during prior economic downturns (2008 Global Financial Crisis and 2020 pandemic-recession). Stability in its earnings can be attributed to its well-balanced business portfolio, and its focus on minimising exposure to commodities and its price volatilities. ROE during this period has stayed within a range of 8-20%, which is a sign of not only durability of earnings, but also a track record of successful capital deployment and re-investment.

The company demonstrates a track record of steadily increasing earnings (above) and an impressively consistent ROE (below) (Seeking Alpha)

Historical price-earnings ratios during this period has largely been rangebound between 6-10x; current trailing and forward P/E sit at the midpoint of this range. From a value-investment standpoint, a stock with recent history of returns consistently over 10% at P/E of 8x is attractive. With current year earnings likely to be close to forecast, and trading at a reasonable P/E ratio, we calculated fair value to be around $28.

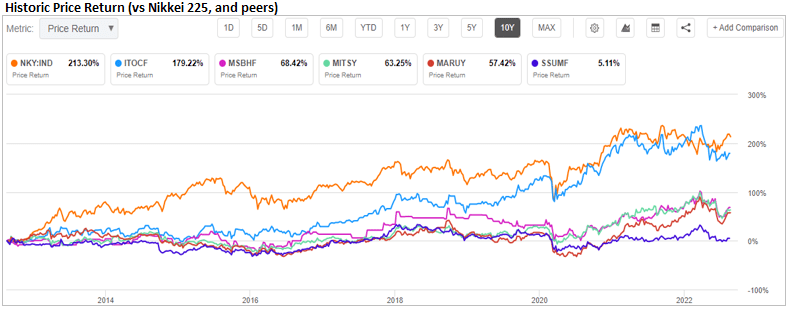

In looking to qualify our earlier “well-balanced reflection of the Japanese business landscape” assertion we looked to benchmark the stock against the Nikkei 225 index (NKY:IND), and noted that ITOCHU’s price movement (179%) over the last 10 years has been comparable to the index’s (213%). With the Nikkei 225’s P/E ratio also mostly rangebound (between 16-22x) during this period, we calculated that the Nikkei 225’s earnings growth has broadly kept pace with ITOCHU. Admittedly it isn’t particularly remarkable for an index to perform in line with one of its constituents, however the same cannot be said for industry peers (Mitsubishi Corporation, Mitsui & Co. (OTCPK:MITSY), Marubeni Corporation (OTCPK:MARUY), and Sumitomo Corporation (OTCPK:SSUMF))

Over the last 10 years, ITOCF price (light blue) has diverged from its peers and now closer tracks the Nikkei 225. (Seeking Alpha)

Peer Comparison

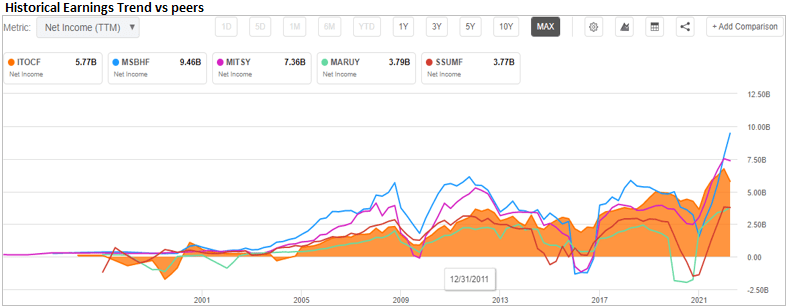

The stock’s price outperformance relative to peers perhaps can be explained when comparing historical earnings for these 5 companies. Although all five show increasing earnings trends over time, ITOCHU has been more uniform in its upward trajectory, whereas the competition have instead followed the boom-and-bust cyclical trends of its underlying key commodities businesses. The c.5x P/E ratio these 4 peers trade at likely has priced in a risk premium for earnings volatility, in comparison to ITOCF, which has been “rewarded” for its predictability with a higher P/E multiple.

ITOCHU has shown a much steadier earnings trajectory to its peers, however all companies have grown over time (Seeking Alpha)

We have noted that Japanese trading companies operate in a unique business environment where although they often operate in similar industries to each other, each identify pockets of competence and geographical strongholds which help them maintain a competitive advantage over each other. ITOCHU’s strength lies in it being focused more towards domestic operations, and having less exposure to resource sectors. We think this positioning will not be threatened by other trading companies soon and therefore ITOCHU can be expected to protect its competitive standing.

However, in theory its portfolio of many siloed operations leaves each business vulnerable to lower barriers of entry for (non-trading company) competitors, and higher risk from disruptive technology. This though is as true in the past as it will be in the future, and ITOCHU’s track record suggests it has unmeasurable value in its culture, know-how, and networks on its side.

Risks

We look for the following themes to weigh on ITOCHU’s future performance:

Strength of the Japanese economy: In the current environment where US, European, and Chinese economic growth is expected to slow down, we have instead been looking to Japan for opportunities. We feel that Japan can buffer itself from economic headwinds in other major economies, and be on stronger footing globally in the next 2-3 years. We think Japanese trading companies in general will benefit if the Japanese economy can show resilience.

Diversified product mix: Its numerable operations across all segments are performing strongly, which gives multiple streams of potential future growth, and protection against isolated underperformance of certain businesses. We will be monitoring to see if this continues in the coming reporting periods.

Earnings growth and resilience in recessionary environments: There is hope that ITOCHU’s track record of consistent earnings growth even during economic downturns can be sustained in future. However, difficulty in pinpointing the company’s strengths and growth drivers makes it equally difficult for us to map out its future trajectory. We could probably surmise that in time it will downsize less profitable businesses, and find new opportunities that maximise returns, but we would like to see a more concrete vision.

Passive sustainability focus: Although we acknowledge that ITOCHU is on track with its own sustainability objectives through the exiting of emissions-intensive businesses and streamlining of existing workflows, we don’t see the company proactively positioning itself to support and monetise the energy transition build-out and capex spend of clients and in the broader economy.

We feel that sustainability will be the most integral growth-driving theme for the next few decades, and imagine ITOCHU has the set-up to benefit from this. We sense there is risk that ITOCHU could lose out on this growth tailwind to its peers if it doesn’t focus resources to this pursuit.

Geopolitical risks: ITOCHU has a sizable international presence which leaves it exposed should geopolitical hostilities escalate. However, its strong focus on domestic operations should position it to be less impacted relative to peers. Furthermore, it could potentially benefit if mooted intentions for companies from Japan and like-minded economies to onshore/friend-shore provides new business opportunities.

Conclusion

ITOCHU distinguishes itself from rival Japanese trading companies by focusing on the domestic economy and away from overreliance on Resources, and that may be compelling rationale for an investor seeking exposure to the industry but not keen on oversized commodity market exposure.

Instead, we wish to pose ITOCHU’s relative attractiveness to the Nikkei 225, and ask what differentiates it. For one, sector compositions are different: areas such as Technology, Consumer Goods, and Health Care are underrepresented in ITOCHU’s business model. Also, by value-standards ITOCHU’s P/E of 8x offers more safety than 16x for the Nikkei 225. We think both ITOCHU and the Nikkei 225 would be reasonable broad-based bets on overall Japanese business performance. We would ask investors to form a clear opinion on where the alpha over the Nikkei 225 lies if they are considering investing in ITOCF.

In the meantime, with a target of $28 we will keep watch if market prices drop meaningfully below this level.

Be the first to comment