da-kuk

The Indian economy could hit $7 trillion in the next seven years. – Anantha Nageswaran.

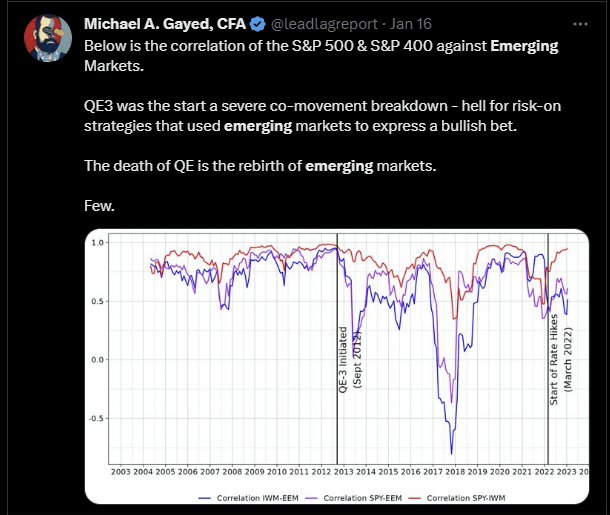

If you’ve been paying attention to some of the infographics I put out on the timeline of The Lead-Lag Report, you’d note that emerging markets are something I’ve been highlighting for a while now.

Twitter

My thesis is premised on the fact that risk-on strategies that previously used emerging markets (“EMs”) as their proxies struggled when QE had come into play in Sep 2012; with monetary stimulus dissipating by the day, this cohort may look to make up for lost time.

Towards the end of January, the IMF came out with its latest economic outlook for different regions across the world. If there’s one terrain that looks in particularly good shape, it’s the emerging markets Asian region, which will likely witness a 100bps improvement in the GDP growth rate this year to 5.3%, well ahead of the global average, which will see a 50bps contraction (2.9%), and the wider emerging market basket itself, which will only see a 10bps improvement (3.9% to 4%).

With EM Asia, there’s one name that is well ahead of the pack, and that’s India, which is poised to emerge as the fastest-growing major economy for yet another year, with expected GDP growth of 6.1%.

Twitter

The strong growth narrative is not a flash in the pan. In fact, in my Lead-Lag Live conversation with a portfolio manager, we touched upon the exponential pace at which India’s economy has been exploding. Note that it took 60 years to reach its first trillion dollars of GDP, but then the second trillion was achieved in just 7 years! Currently, India is close to being a $3.5 trillion economy, and the Chief Economic Advisor of India believes they could double this over the next 7 years!

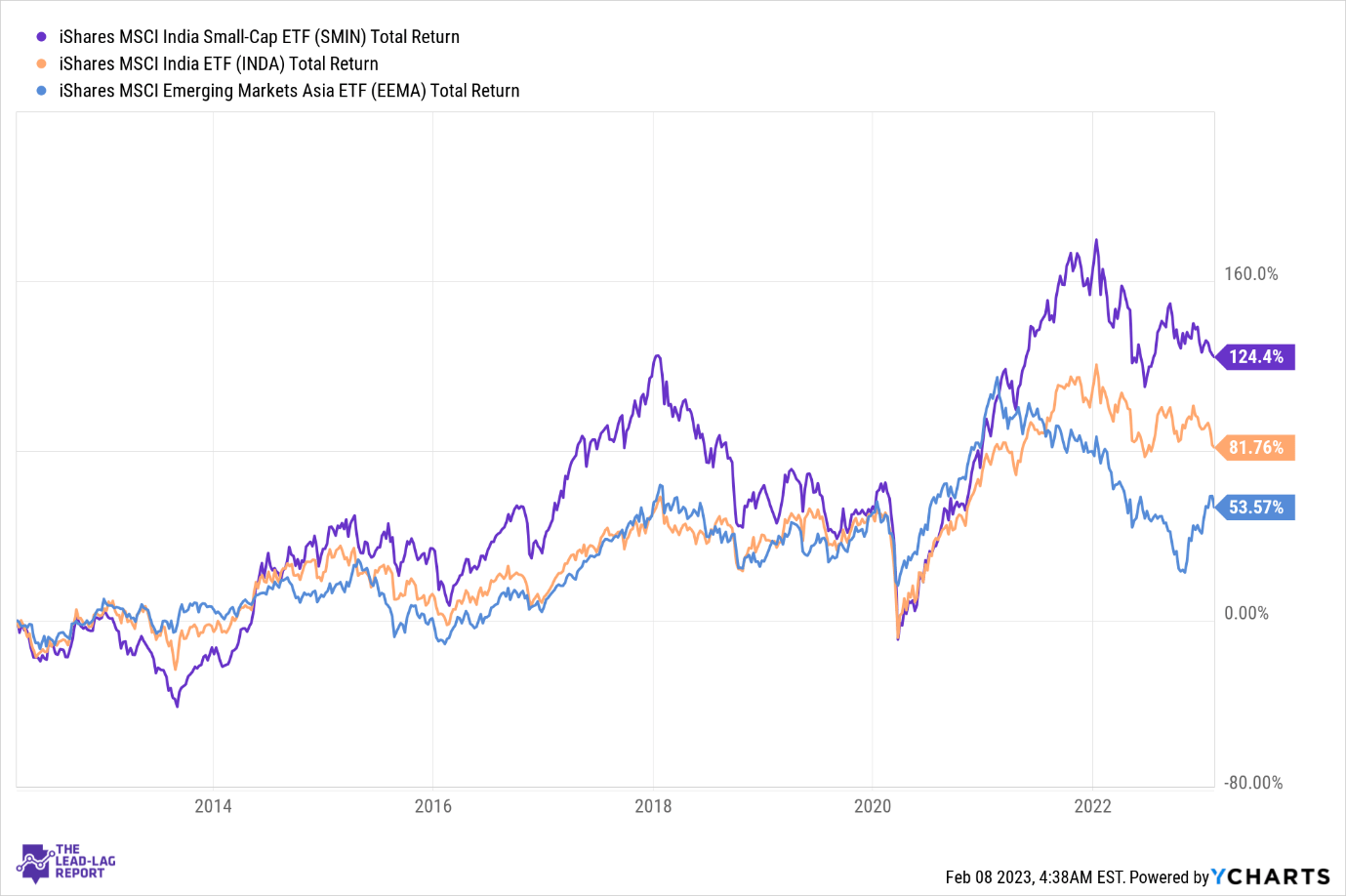

If you want to play India, you may consider looking at the iShares MSCI Small-cap ETF (SMIN) that gives you coverage towards small public companies based in India. Longstanding holders of this product will tell you what a world of good it has done for them. Since its inception in 2012, it has comfortably outperformed not just its larger Indian counterparts by 1.5x, but also the broader EM Asia Cohort by 2.3x!

YCharts

Subscribers of The Lead-Lag Report would know that my inter-market signals currently support a risk-on play, and SMIN with its heavy exposure to high-beta plays such as industrials and materials (these two sectors are the largest, jointly accounting for ~40% of the holdings) may see additional interest.

Besides that aspect, I thought the Indian Union Budget which came out last week was extremely favorable to these stocks which look set to benefit from the heightened outlay towards the manufacturing sector. The Indian finance minister put forward a budget that will see capital spending towards roads, ports, and airports grow by 33% YoY to $122bn or INR 10 Lakh crore. Meanwhile, there also appears to be a focused thrust towards raising India’s electric vehicle (“EV”) manufacturing credentials. Do consider that India is one of the fastest-growing EV markets in the world. In 2021, less than 350,000 EVs were sold, and last year, EV sales ended up crossing the 1m mark, representing annual growth of over 200%!

ING`

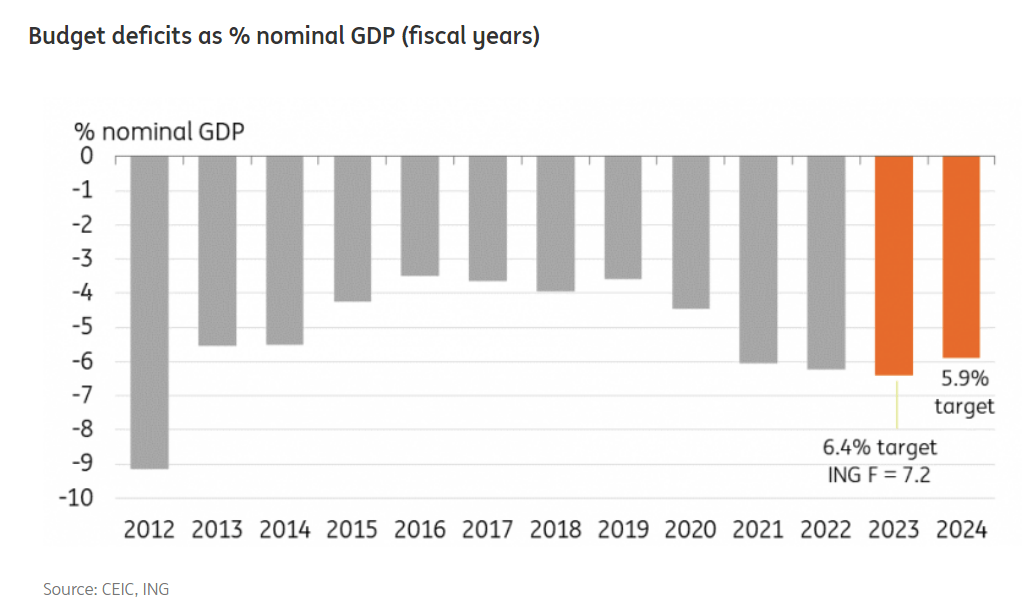

The encouraging aspect of the budget is that it was not overly populist, and that’s quite an achievement when you consider that national elections in India will take place next year. In fact it looks like the fiscal deficit will actually decline by 50bps and drop to 5.9% of nominal GDP in 2024!

A reduced fiscal deficit should be music to the ears of INR bulls who may have to contend with some near-term volatility given some of the recent Fed commentary that may support the dollar. India looks like it is at the end of its rate hiking cycle while noted Fed member- Neel Kashkari is on record stating that he believes the Fed Funds Rate still needs to transition to around 5.4%. Even if the dollar does appreciate, note that the Indian central bank still has ample forex reserves (nearly $600bn) to manage things as that translates to solid import cover of 9.4 months!

Conclusion

Given the strong alpha track record, and the enticing growth potential on offer, investors shouldn’t be under any illusions of expecting a cheaply priced product. Indeed, SMIN trades at 15.4x forward P/E, pricier than its emerging markets Asian counterparts who trade at 13x P/E.

Stockcharts.com

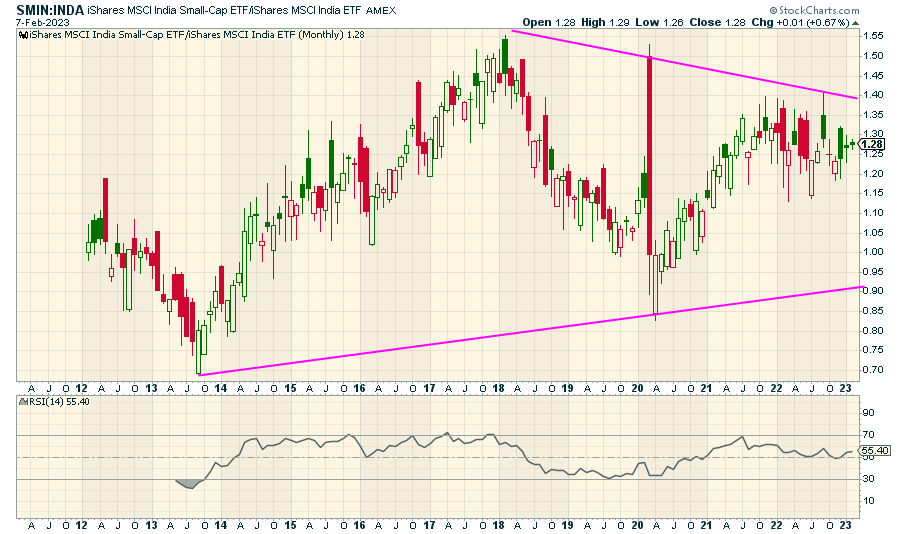

Besides, if you measure Indian small-caps against the large-cap focused Indian portfolio INDA, it doesn’t appear that there’s a great deal of value to be found as the ratio favoring SMIN is not too far from the resistance point.

Twitter

As noted in the “Opening Thoughts” section of this week’s Lead-Lag Report, while conditions for a risk-on environment in the short-term still look good, investors may want to go a little slow on a high-beta play like EM small-caps. I say this because I’ve been left a little concerned by the ferocity of my risk-on proxy-Lumber’s uptrend over the past three weeks, even as the risk-off proxy-Utilities has struggled over the past few weeks. One shouldn’t dismiss the boomerang effect of these sorts of violent moves and what this could do for a reversal of risk sentiment in a few weeks, particularly given the looming shadow of a potential credit event.

Anticipate Crashes, Corrections, and Bear Markets

Anticipate Crashes, Corrections, and Bear Markets

Sometimes, you might not realize your biggest portfolio risks until it’s too late.

That’s why it’s important to pay attention to the right market data, analysis, and insights on a daily basis. Being a passive investor puts you at unnecessary risk. When you stay informed on key signals and indicators, you’ll take control of your financial future.

My award-winning market research gives you everything you need to know each day, so you can be ready to act when it matters most.

Click here to gain access and try the Lead-Lag Report FREE for 14 days.

Be the first to comment