tolgart/iStock via Getty Images

By Rob Isbitts

Strategy

iShares Core Growth Allocation ETF (NYSEARCA:AOR) is really a code name. This is a 60% stock and 40% bond allocation portfolio, comprised of iShares ETFs. 60/40 investors likely associate this allocation with a “balanced” approach. But this is one of a foursome of objective-driven iShares ETFs, with the others being Conservative Risk (AOK), Moderate Risk (AOM) and Aggressive Risk (AOA).

The strategy is to allocate among a group of iShares that offers a mix of different types of stock and bond exposure, so as to track the S&P Target Risk Growth Index. This is what is known as a “fund or funds,” or more properly in this context, an ETF of ETFs. The fund’s 2% turnover rate implies that the allocation is essentially fixed, with only occasional adjustments based on a set time period.

Proprietary ETF Grades

-

Offense/Defense: Offense

-

Segment: Multi-Asset

-

Sub-Segment: Moderate

-

Correlation (vs. S&P 500): High

-

Expected Volatility (vs. S&P 500): Low

Holding Analysis

AOR holds 8 iShares ETFs. The bond side is dominated by a core US bond ETF (34% of the total fund), with a 6% allocation to an International bond ETF. A slight majority of the equity side of the portfolio is held in an S&P 500 ETF, and another 19% is currently allocated to International/Developed Markets (Europe and Japan, primarily). Emerging Markets make up about 7%, and a trace amount of exposure is devoted to a US Mid Cap ETF (2%) and a US Small Cap ETF (less than 1%).

Strengths

For investors who are true believers in the traditional 60/40 balanced portfolio model, AOR replicates that, and has the size and strength of the iShares behemoth ETF brand behind it. During periods when global stocks and bonds enjoy sustained success, AOR can be viewed as a one-stop portfolio allocation. After all, it is 8 ETFs in one.

Weaknesses

OK, so we said about all the nice things we can say about this ETF. It does what it aims to do. But we warn investors, even ardent 60/40 fans, about expecting the past to be prologue here. The stock market, and especially the bond market, are coming off of an era driven by Central Bank excess, which promoted massive investor speculation. That drove stock prices up, interest rates down (which pushed bond returns up), and created what we firmly believe is a false sense of security for balanced investors. In other words, the era of easy money produced an era of investor overconfidence. We do not think that will reverse itself immediately. That is a long-term, sustained threat to certain investment strategies that used to work.

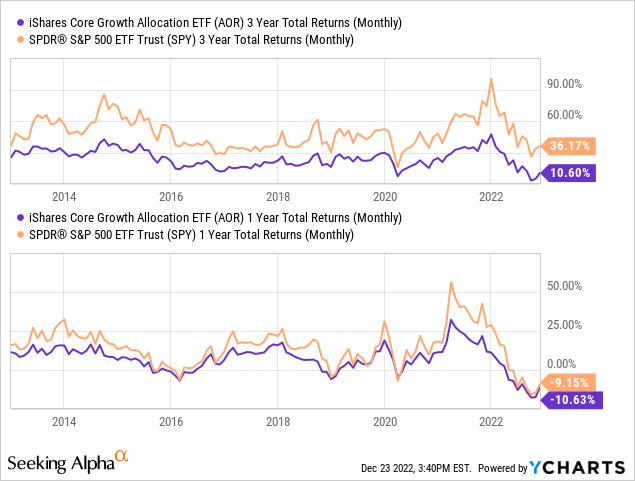

This 2-level chart below relates to both the strengths and weaknesses cited above. The top part of the chart shows 3-Year rolling returns of AOR, as compared to the S&P 500 ETF (SPY). As you can see, over every 3-Year time frame since AOR’s debut in late 2008, it has trailed the S&P 500. In a nearly uninterrupted period of strong US stock market returns, that is to be expected. But it may also lull some investors into complacency, thinking that by investing in AOR, they can get similar returns to what that balanced approach produced in the past (a total return of 224% from late 2008 through the end of 2021). Most likely, returns for stocks and bonds will be lower over the next 5-10 years.

While that may help AOR versus the S&P 500 (see lower part of the chart, where AOR’s path on a 1-Year return time frame is picking up versus the S&P 500), the old Wall Street saying is very helpful here: you can’t eat relative returns. In other words, beating the S&P 500 is not going to be a very helpful objective as it was in the past. For instance, in 2022, beating the S&P 500 meant “only” losing mid-teens on a percentage basis.

Opportunities

As sanguine as our intermediate to long-term outlook is for what we’d call “traditional balanced asset allocation,” nothing in investing is for certain. So, even as we do not expect broad market stocks and core bonds to work together in beautiful harmony as they did for most of the period 2009-2021, that does not mean we can’t be wrong. For that to be the case, we think the one card left in the deck for traditional 60/40 advocates is for the Fed and other Central banks to “blink” in response to investor losses, and again do what we think they should have avoided doing in 2016, 2018 and 2020. Namely, loosening credit conditions in a way that stokes excess speculation in investment markets.

Threats

Can that happen? Sure. But if it does, we might as well just get used to periods like 2021-2022 reoccurring over and over again. Boom-bust in rapid succession. For the sake of long-term investors everywhere, we hope that is not what happens. But hope is not a strategy, so we simply conclude that AOR is a longshot to replicate its past success, or even approach it, as a steady producer of balanced total returns. In an era of potentially lower returns across markets, the old methods are a much bigger risk than some investors recognize.

An Old Saturday Night Live TV show routine, for those old enough to remember, had a newscaster talking about how a deceased rogue world leader was “still dead.” That’s our view of traditional 60/40 investing, even after 2022’s debacle for that revered approach.

Proprietary Technical Ratings

-

Short-Term Rating (next 3 months): Sell

-

Long-Term Rating (next 12 months): Sell

Conclusions

ETF Quality Opinion

AOR was a simple, effective way to participate in bullish markets like what we had in 2018 and 2019, where AOR posted back-to-back years of 19% and 11% returns. It still appears to be structurally sound. But that’s not the same as being a sound investment.

ETF Investment Opinion

We know our take on AOR will cause some, or even many investors, to attack our view. That’s what the comments section of Seeking Alpha is for, and we welcome the discussion as always.

But recognize this about 60/40: it was a very good long-term investment technique, developed decades ago by academics, who had very good intentions. They never expected it to morph into a Wall Street marketing cry that rose to a fever pitch last decade, taking on cult-like status.

Why is this so attractive to traditional Wall Street? Because the story keeps the fees coming in. In the case of AOR, iShares is charging 0.15% on top of the fees on the 8 ETF sub-components in the fund. That’s their right. But we encourage investors to think about whether such a one-stop shop technique that is AOR and its 3 relatives mentioned above is going to work in the future like it did in the past. Or, to even resemble it. 2022 is just one year, and stocks and bonds fell together.

We would not assume that’s the last of that behavior in the coming years. And that strikes at the core of the traditional 60/40 portfolio model. We rate it a Sell.

Be the first to comment