Mario Tama/Getty Images News

Investment thesis

Since the 2021 all-time high, FedEx (NYSE:FDX) has lost approximately 43% of its market capitalisation as the recent stock market bubble has been unwinding. I believe the company has strong competitive advantages despite not being able to earn superior ROIC over the last several years. In addition, I think the company is likely to face a weaker demand and volumes as we probably enter into recession in this upcoming year.

Business Overview

FedEx is a global transportation and logistics company that operates a large network of planes, trucks, and sorting and distribution centers around the world. I believe the company’s extensive network is a key aspect of its business model, and it has played a significant role in helping FedEx to become one of the leading players in the industry.

Economic moat

One of the main advantages of FedEx’s large network is that it enables the company to offer a wide range of services to customers in more than 220 countries. In addition to its well-known package delivery services, the company also provides freight transportation, supply chain management, and other logistics services. I believe this diversified range of services allows FedEx to cater to a wide range of customers and generate revenue from multiple sources.

I think another advantage of FedEx’s large network is that it enables the company to offer fast and reliable delivery to customers around the world. The company has a reputation for delivering packages on time, and its extensive network of planes (more than 660 aircrafts), trucks (more than 170,000 motorized vehicles), and sorting and distribution centers helps to ensure that packages are delivered to their destinations quickly and efficiently. This is especially important for time-sensitive shipments, such as medical supplies or e-commerce orders.

Finally, I think FedEx’s large network also gives the company a competitive advantage in terms of its ability to handle large volumes of shipments, with 80% of Americans being “within 9 minutes of a FedEx hold location“. The company’s sorting and distribution centers are able to process a large number of packages efficiently, which enables the company to handle high levels of demand from customers.

Overall, I believe FedEx’s large network is a key aspect of its business model, and it has helped the company to become a leading player in the transportation and logistics industry. By continuously investing in its network and adapting to changes in the industry, FedEx is able to maintain its competitive advantage and generate consistent profits over time.

I believe the company’s Onsite initiative provides significant benefits to its customers. Through FedEx’s multiple partnerships with some of the biggest retailers in the world such as Walmart (WMT), Kroger (KR) and Walgreens (WBA), the company is able to offer customers convenient locations where they can drop off or pick up packages, often in the same location where they are already shopping.

I think it is also worth considering that according to the company, FedEx Freight is the first and only nationwide of less-than-truckload service (LTL) shipping from a major national carrier, while providing for domestic shipments proprietary features such as tracking technology for pallets and digital bills of lading (BOLs).

Despite these strong competitive advantages, the company’s management team has not been able to translate them in high returns on invested capital. More specifically, FedEx earned an average ROIC of 7.8% over the last 5-years.

| Year | Return on Invested Capital (ROIC) |

|---|---|

| 2022 | 8.1% |

| 2021 | 7.8% |

| 2020 | 3.6% |

| 2019 | 9.2% |

| 2018 | 9.2% |

Financials

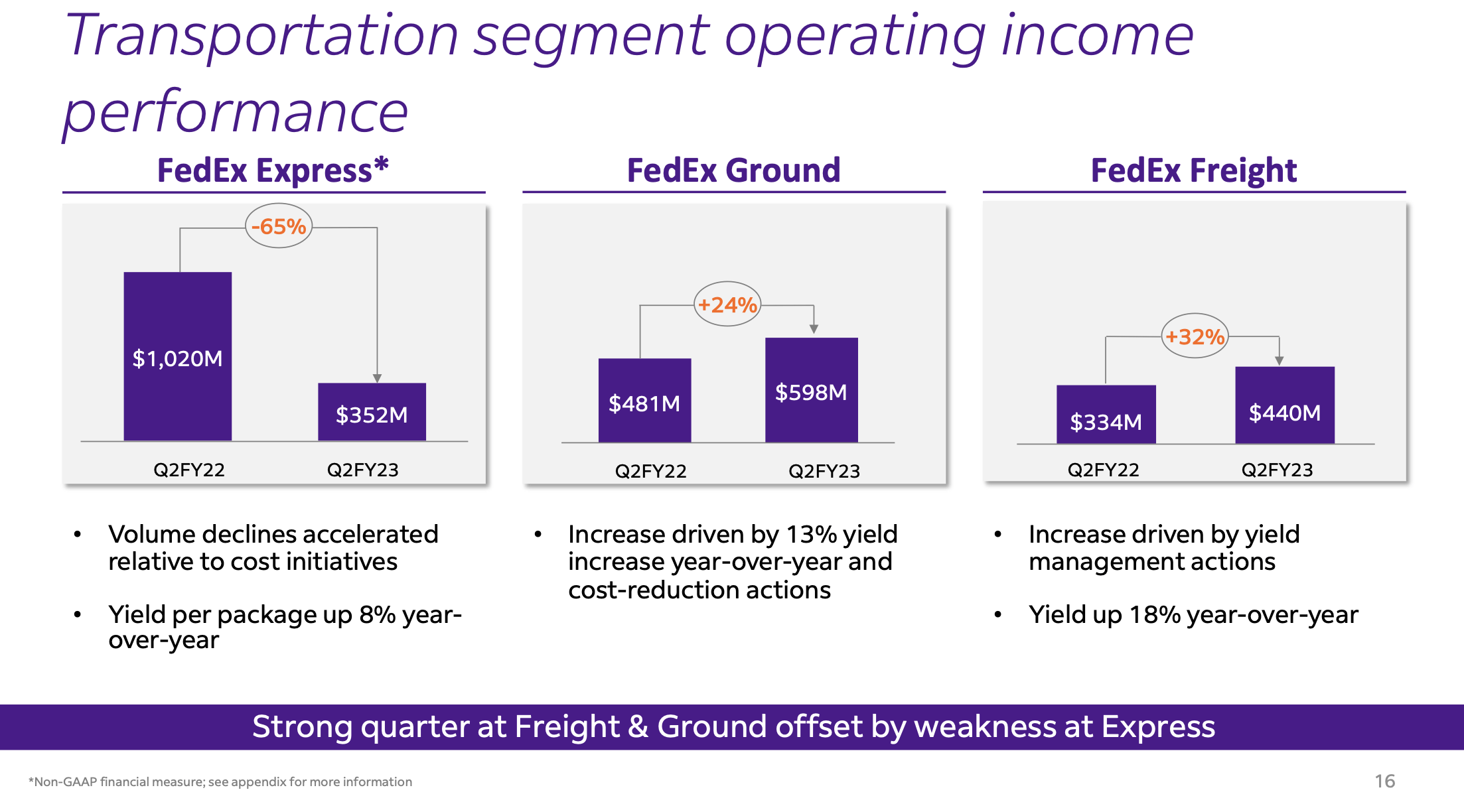

FedEx reported its fiscal 2023 second quarter earnings on December 20, 2022, and while the company’s net income topped analysts’ expectations, its revenue missed the target, causing shares to decline. Despite this, the company’s financial performance showed strong growth in several areas, including a 9% increase in revenue to $22.2 billion. However, the company’s overall operating income declined significantly, falling by 30% year over year to $1.18 billion with operating margin trending down to 5.2% from 6.8% in the previous year. Unlike FedEx Express operating income falling 65% YoY, FedEx managed to improve its Ground and Freight segments operating income by 24% and 32% respectively primarily because of the company’s cost cutting initiative to reduce the impact of a much lower global demand.

FedEx

One factor contributing to this decline in operating income was the drop in global volumes, which negatively impacted the company’s performance. This decline in global volumes was only partially offset by an 8% increase in package yield, which helped to boost the company’s revenue.

FedEx

In anticipation of weaker demand in 2023, FedEx’s management team is taking action to significantly reduce costs and implement structural changes to the company’s air network. These measures include temporary parking of aircraft and other cost-cutting initiatives, which are expected to result in total cost savings of $3.7 billion by 2023.

FedEx

Despite the challenges and declining operating income in the most recent quarter, FedEx remains a strong player in the transportation and logistics industry and has a long track record of success. The company’s focus on cost management and capital discipline has helped it to reduce the negative impact of a much softer than expected global demand.

Multiple valuation

Based on the company’s last quarter results, it seems that FedEx’s management team is expecting weaker earnings per share in 2023 due to ongoing challenges related to lower global volumes. The company’s earnings per share for 2023 have been revised down by almost 4% as a result of these headwinds. Despite the company’s forward earnings multiple is 25.3% lower than the sector median, I expect that the company’s multiple will materially change as earnings will further be revised down and demand to continue slowing as we enter into a severe recession the following year.

Conclusion

Overall, I believe that the company has robust competitive advantages over potential new entrants even the management team has not been able to earn significant returns on invested capital. From an investment standpoint, today’s price doesn’t provide any margin of safety, which means that it should be preferable to wait a much better price entry.

Be the first to comment