sshepard

Over the last few months, we have written several articles outlining our views of banks in general. We explained the relationship that you, as a depositor, have with your bank is in line with a debtor/creditor relationship. This places you in a precarious position should the bank encounter financial or liquidity issues. Moreover, we also outlined why reliance on the FDIC may not be wholly advisable. And, finally, we explained that the next time there is a financial meltdown, your deposits may be turned into equity to assist the bank in reorganizing.

So, at the end of the day, it behooves you, as a depositor, to seek out the strongest banks you can find, and to avoid banks which have questionable stability.

While we outlined in our last articles the potential pitfalls we foresee with regard to various banks in the foreseeable future, we have not provided you with a deeper understanding as to why we see the larger banks as having questionable stability. Over the coming months, we intend to publish articles outlining our views on this matter.

First, we want to explain the process with which we review the stability of a bank.

We focus on 4 main categories which are crucial to any bank’s operating performance. These are: 1) Balance Sheet Strength; 2) Margins & Cost Efficiency; 3) Asset Quality; 4) Capital & Profitability. Each of these 4 categories is divided into 5 subcategories, and then a score ranging from 1-5 is assigned for each of these 20 sub-categories:

- If a bank looks much better than the peer group in the sub-category, it receives a score of 5.

- If a bank looks better than the peer group in the sub-category, it receives a score of 4.

- If a bank looks in-line with the peer group in the sub-category, it receives a score of 3.

- If a bank looks worse than the peer group in the sub-category, it receives a score of 2.

- If a bank looks much worse than the peer group in the sub-category, it receives a score of 1.

Afterwards, we add up all the scores to get our total rating score. To make our analysis objective and straightforward, all the scores are equally weighted. As a result, an ideal bank gets 100 points, an average one 60 points, and a bad one 20 points.

If you would like to read more detail on our process for evaluating a bank, feel free to read it here:

Our Methodology & Ranking System: Banks – SaferBankingResearch

But, there are also certain “gate-keeping” issues which a bank must overcome before we even score that particular bank. And, many banks present “red flags,” which cause us to shy away from even considering them in our ranking system.

As mentioned before, it is difficult to overestimate the importance of a deeper analysis when it comes to choosing a really strong and safe bank. There are quite a lot of red flags to which many retail depositors may not pay attention, especially in a stable market environment. However, those red flags are likely to lead to major issues in a volatile environment. Below we highlight some of the key issues that we are currently seeing when we take a closer look at Bank of America (BAC).

Bank of America was ranked #1 in U.S. retail deposit market share as of the end of 1H21, according to the FDIC. In our view, this is due to the fact that the bank has historically had a strong franchise thanks to its brand and marketing efforts. As a result, many customers still think that BAC is the strongest credit institution from a retail depositor perspective as well. However, a closer look at the bank’s financial statements reveals several factors that are very likely to become significant issues in a systemic crisis. In this article, we would like to highlight some of these issues we believe BAC’s clients should be aware of in order to be well prepared for a potential bear market and a recession.

Still a high share of unsecured consumer lending

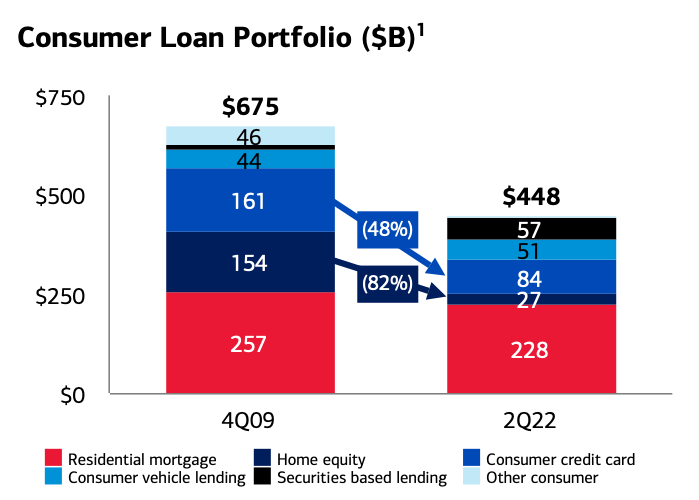

In its 2Q22 earnings release, BAC mentioned that its loan portfolio has less inherent risk now compared to YE2009 due to less exposure to unsecured consumer lending. Indeed, the bank’s portfolio of credit consumer cards has fallen by 48% since 4Q09.

Company data

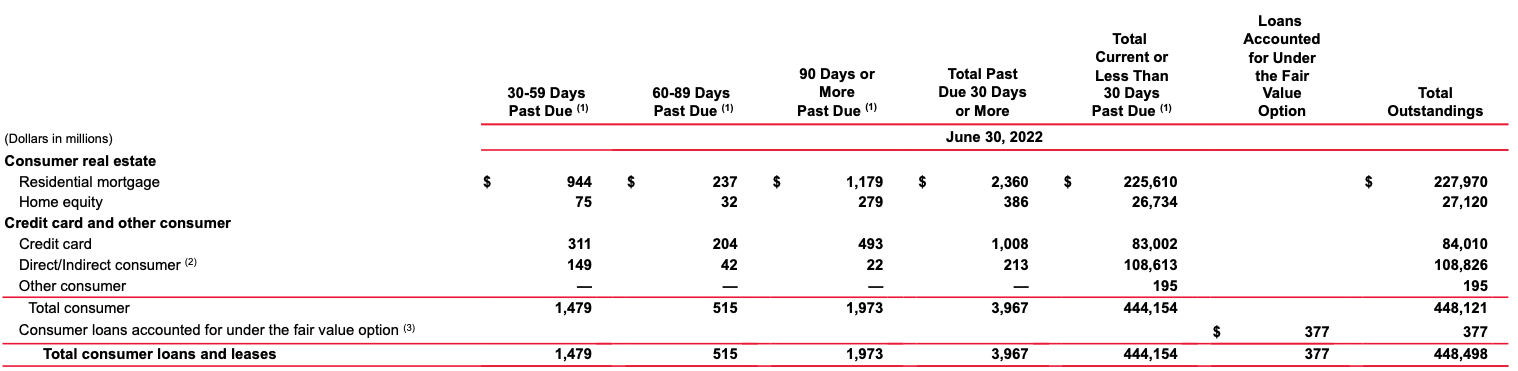

However, if we take a look at the bank’s latest 10-Q form, we will see that non-mortgage retail lending (excluding home equity lines of credit) correspond to 19% of BAC’s total loan book.

Company Data

As we said in our previous articles on Citigroup and JPMorgan, unsecured consumer loans are one of the riskiest business segments for a bank in a volatile environment, as provisioning charges on these loans could increase dramatically, and, as a result, a bank could face significant losses. The fact that BAC has still quite a risky and large unsecured consumer book has been once again shown in the recent Fed’s stress tests, which we will discuss later.

Another important thing is that BAC decreased its residential mortgages portfolio from $257B as of YE2009 to $228B as of 1H22. While we do acknowledge that mortgages were one of the key reasons of the 2007-2008 financial crisis, we note that credit quality of U.S. residential mortgages has significantly improved since then due to stricter lending standards as the U.S. banks have increased requirements to many metrics (for example, to an LTV (loan-to-value ratio). Also, if we look at longer-term historical data, we will see that despite the 2007-2008 crisis, provisioning losses on mortgages were among the lowest compared to other lending segments. As such, we do not think that a decrease in U.S. residential mortgages should be viewed as a de-risking of BAC’s book.

Massive growth in non-U.S. commercial lending

BAC also mentioned that one of the factors that supported the de-risking of its credit portfolio is an increase in commercial loans. As the chart below shows, there was indeed quite a large pick-up in commercial lending. Notably, non-U.S. commercial lending grew 4x times, from $29B as of YE2009 to $128B as of 1H22.

Company Data

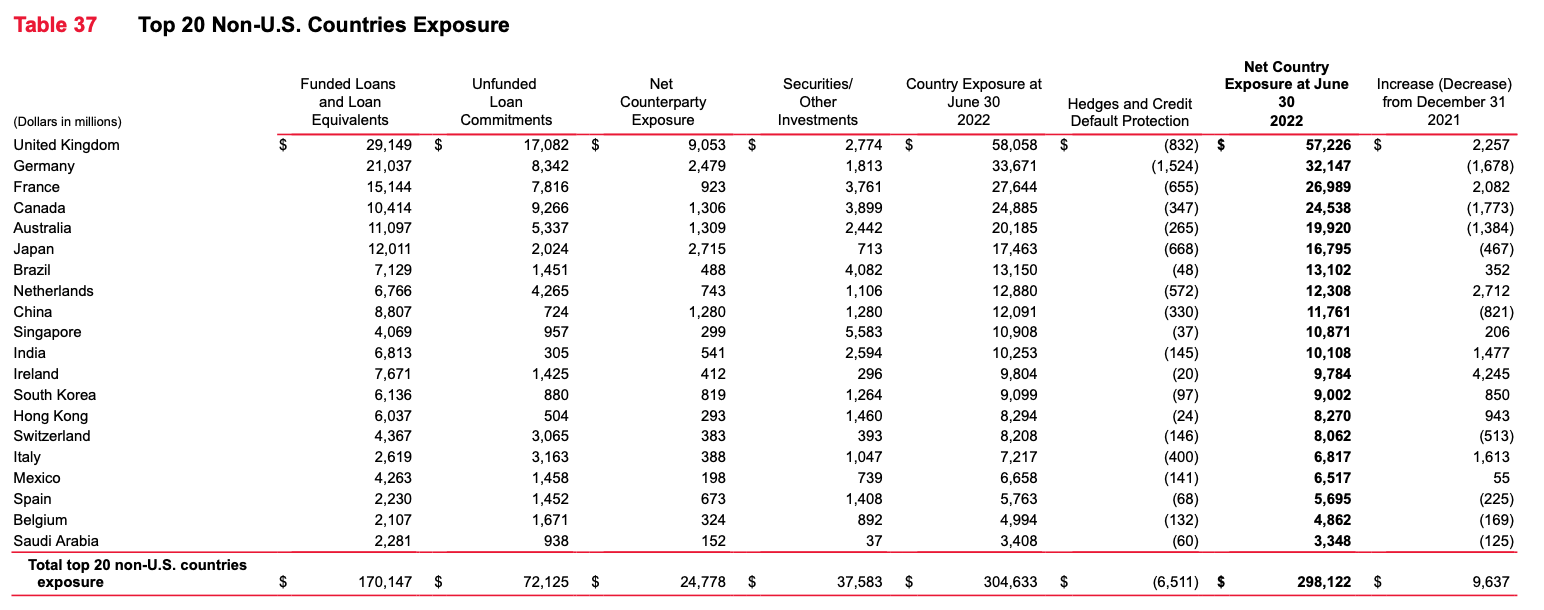

While BAC views non-U.S. commercial lending as a less risky segment compared to U.S retail loans, we think it is far from certain that quality of non-U.S. commercial credits would be better than quality of U.S. mortgages in a recessionary scenario. The table below shows BAC’s Top-20 countries exposure.

Company Data

As we can see, non-U.S. loan exposure is $170B, while total net exposure, which includes unfunded commitments and securities, is $298B. This corresponds to 28% of BAC’s total retail deposits. The table above shows that top-3 countries are the U.K., Germany, and France. We currently see that while the global economy is still technically rising, both the British pound and the euro have been very weak against the dollar due to differences in the policy rates, inflation, and GDP growth between the U.S. and Europe. Those differences would very likely become larger in a global crisis scenario, and, as a result, the dollar would appreciate more against other global currencies. That would result in revenue pressure and asset quality issues for BAC’s non-U.S. commercial credit book.

Commercial loan book is skewed towards asset managers, finance companies, and real estate

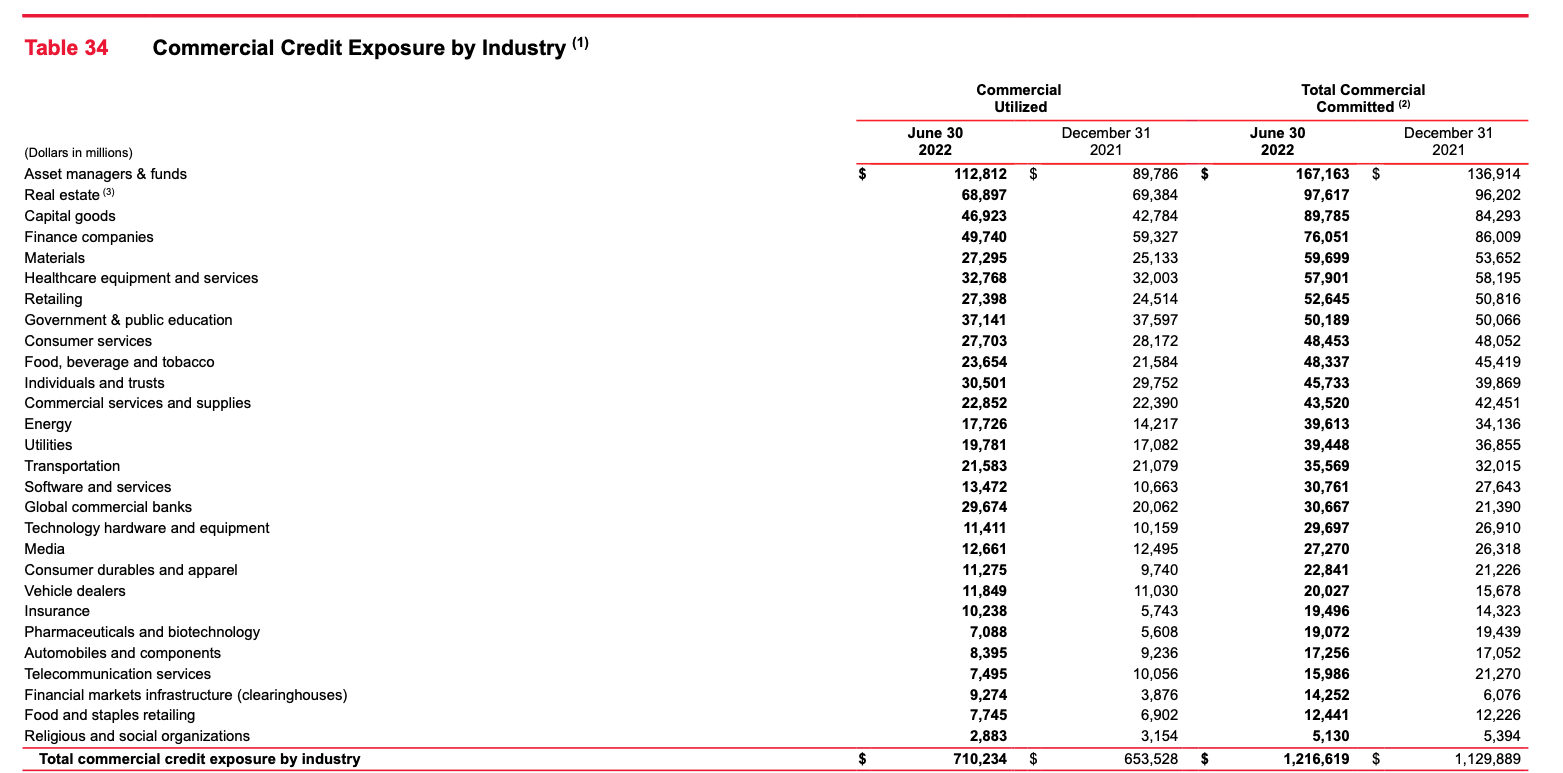

The table below demonstrates BAC’s commercial credit exposure by industry. It might come as a surprise for many readers, but based on utilized loans, the top-3 industries are asset managers, real estate and finance companies.

Company Data

As history tells us, those industries would be among the most vulnerable ones from an asset quality perspective in a volatile environment. As a result, that would likely lead to losses for BAC in a crisis scenario.

Share of securities is significantly above than that of the peers; more than $500B of MBS on the balance sheet

The table below shows BAC’s consolidated balance sheet.

Company Data

If we sum up federal funds sold and REPO securities, trading assets, derivatives, and debt securities, then the total amount of securities on BAC’s balance sheet is $1,561B, which is more than half of the bank’s total assets. By comparison, BAC’s total loan book is $1,031B, and total retail deposits are $1,072B. Notably, BAC’s share of securities is significantly above that of its peer group (U.S banks with total assets of more than $100B), which is 28%.

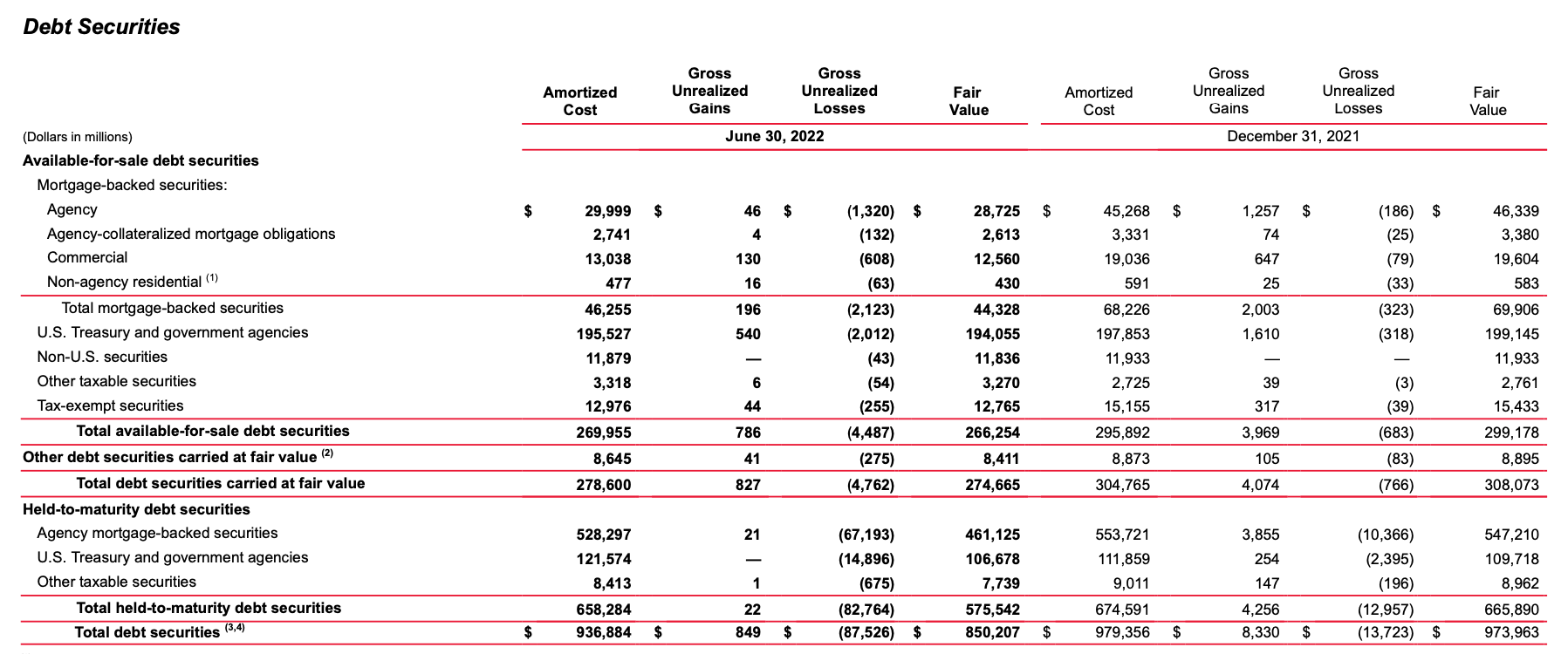

Below is a breakdown of BAC’s debt securities, which were more than $900B as of the end of the first half of the year. As the table shows, there is significant exposure to mortgage-backed securities ($528B). This is by $300B higher than BAC’s total mortgage loans of $228B.

Company Data

BAC’s GWIM: low operating efficiency and weak capital position

Bank of America Global Wealth & Investment Management (GWIM) consists of two primary businesses: Merrill Wealth Management (MWM) and Bank of America Private Bank (BAPB). According to the company, MWM’s advisory business provides various investment services to retail clients with over $250K in total investable assets. Bank of America Private Bank provides wealth management solutions targeted to high net worth and ultra-high net worth clients.

This is one of the largest BAC’s business segments as its revenue for 1H22 correspond to 24% of the group’s total revenues, while its net income corresponds to 17% of the group’s profit. We published a detailed report on BAC GWIM on our service, and if you are a client of BAC GWIM, you might want to read it to be aware of all the weaknesses of this business. In this article, we would like to mention the most important issues. First, BAC GWIM has a weak capital position, with an allocated capital-to-assets ratio of just a tad above of 4%. Second, the business has subpar operational efficiency with a cost-to-income ratio of as high as 72% for the first half of the year.

The 2022 Fed stress tests suggest a potential capital loss of $45B

In June, the Fed published stress-test results for 33 U.S banks. As shown below, under the severely adverse scenario BAC posted a net loss of $45B (a net loss plus AOCI included in capital) or more than 25% of BAC’s CET1 capital as of the end of 1H22. As we noted before in our articles, the Fed’s assumptions for its severely adverse scenario are quite mild, in our view. In particular, Fed assumed a relatively short-lived market correction and a V-type recovery of both the markets and the global economy. However, even under these assumptions BAC loses a quarter of its CET1 capital.

The Fed

The bottom line

In contrast to BAC, our Top U.S 15-banks identified at Saferbankingresearch.com have a low-risk loan mix with minimal exposure to unsecured lending and non-U.S. lending, have very conservative securities books, which consist predominantly of U.S Treasuries and U.S municipal bonds, and do not have any derivatives on both their balance and their off-balance sheets. Moreover, BAC has more red flags, which we did not discuss in detail due to the limitations of the article, such as reliance on investment-banking revenues, the bank’s off-balance sheet items and a potential increase in RWA (risk-weighted assets) in a volatile environment. However, all our Top-15 banks have been tested for these red flags to ensure their long-term stability.

Housekeeping matters

This article, as well as Saferbankingresearch.com, was a combination of efforts between Avi Gilburt and Renaissance Research, who has been covering U.S., European, LatAm and CEEMEA banking stocks for more than 15 years.

If you would like notifications as to when my new articles are published, please hit the button at the bottom of the page to “Follow” me.

Be the first to comment