Andy Feng

Article Thesis

NIO Inc. (NYSE:NIO) has, like many other EV stocks, seen its shares decline quite a bit so far this year. This has made the stock a lot cheaper, relative to where NIO traded when its shares hit their highs last year. At the same time, NIO has made some operational progress and started its expansion into Europe. NIO isn’t profitable yet, and thus may not be suitable for risk-averse investors. But its current valuation is not very demanding, and the company’s growth potential is strong.

Why Has NIO’s Price Dipped?

NIO has seen its share price decline by 72% over the last year. More recently, its share price performance has been far from great, too. Over the last month, NIO’s stock price declined by a little over 40%, which destroyed more than $10 billion in market capitalization. There are several factors at play when it comes to explaining NIO’s share price decline.

First, the company had been trading at a rather high valuation last year, when the market was overly optimistic about EV stocks. NIO, along with stocks such as Tesla (TSLA), Lucid (LCID), Rivian (RIVN), and so on, was trading at a very high valuation back then. Since then, enthusiasm has waned, which is why all of these and many additional EV stocks have performed badly in that time frame, some even worse than NIO.

Second, rising interest rates are a headwind for companies such as NIO. The company is not profitable yet but has a strong growth outlook, which should allow it to become profitable eventually. All of NIO’s profits thus will be generated years or decades from now. In a zero-interest-rate environment, where discount rates in DCF models are low, these not-yet-profitable long-duration assets may be trading at high valuations. But since interest rates have risen sharply this year, including over the last couple of weeks, discount rates have risen, which has an especially large impact on growth stocks/long-duration assets, whereas less expensive value stocks aren’t impacted as much.

On top of that, the market has also become more worried about Chinese equities in general, due to escalating tensions between China and the US. Recent moves such as the US’s decision to block the sale of some semiconductors to China have made some investors worry about whether it’s a good idea to invest in Chinese equities. So far, the Chinese government has not taken any action against US-based investors in NIO and other Chinese companies, but escalating conflict between China and the US is nevertheless a macro risk for companies such as NIO. It should be noted that many US-based companies could be highly impacted by growing tensions as well, such as Tesla with its large China footprint, or Apple (AAPL) that generates billions of dollars in revenue in China.

NIO has also been impacted by some company-specific items, such as its weaker-than-expected growth in recent months. During September, the most recent month we have data for, NIO’s deliveries totaled 10,900 vehicles. That’s just up by 2% year over year. Q3 numbers overall were better, but with a 29% year-over-year growth rate NIO grew less than the overall EV market in China, and it underperformed competitors such as BYD (OTCPK:BYDDY), which delivered growth of close to 200% in the same time frame. NIO’s smaller peers, such as XPeng (XPEV) and Li Auto (LI) also did not grow their sales as much as the market, thus NIO was not the only EV player that saw its sales growth rate dip. Nevertheless, market share losses aren’t positive, and BYD has shown that it was possible for Chinese EV players to grow considerably in recent months.

NIO’s management has stated that the not overly high delivery growth rate was caused by supply chain issues and that there is not a demand problem. That’s good news, as supply chain issues can and will be solved, especially once COVID measures in China ease. As long as NIO’s brand remains strong and there is demand for its vehicles, the underwhelming deliveries growth rate thus looks like a temporary issue. It’s nevertheless clear that other EV players, mainly BYD, have apparently managed to handle supply chain issues better, which could be due to BYD’s larger size that allows for more experience in sourcing material from different suppliers, etc.

What Is NIO’s Outlook?

As an EV pureplay, NIO’s market potential depends on the ongoing growth of the global EV market. Especially in NIO’s home country, China, where growth has been excellent in the recent past. In China, around 20% of new vehicles are NEVs, or new energy vehicles. This primarily includes EVs (plug-in hybrids and BEVs) while other technologies such as hydrogen play a negligible role for now. With millions of EVs being sold in China alone (in September NEV sales totaled more than 600,000), and with that number growing at a rate of almost 100% year over year, there is a huge and rapidly expanding market opportunity in NIO’s home country – the most important EV market in the world.

NIO’s vehicles are above-average in price and quality, which is why the company can’t address all parts of the market. But even the premium market it addresses is very large and growing rapidly, showcased, for example, by Tesla’s sales pace. NIO’s production constraints should ease going forward, based on easing supply chain worries that I expect over the next couple of quarters as lockdown measures in China will hopefully wane eventually and since companies adapt to these issues over time.

NIO is also expanding outside of its home market, China. Recently, the company opened its first battery-swapping station in Germany, which is Europe’s largest automobile market, where other EV companies also see a lot of potential – such as Tesla, which built a Gigafactory there. NIO had already been active in Norway before that, which is usually the first European market EV companies from outside of Europe expand to. Now, NIO is active in several European markets, including the Netherlands, Sweden, and Denmark, on top of the aforementioned Norway and Germany. The first model that was introduced in Europe is the ET7, NIO’s high-end sedan, but NIO will introduce additional models over time. The company plans to build 20 swapping stations in Europe by the end of the year, which will introduce the vast European market to NIO’s unique tech that differentiates it from other EV players where consumers have to accept long charging times, whereas NIO’s battery swaps only require a couple of minutes, thereby providing a clear unique selling point that should be beneficial for NIO’s potential to sell vehicles.

Between these factors, NIO should be able to grow its business very meaningfully over the next couple of years. Of course, revenues alone do not make a company a great investment, thus NIO will have to prove that it can also generate compelling profits over time. Thanks to the high prices for its vehicles, as it sells to the less price-sensitive premium market, that should be possible, although the exact timing when it will first become profitable is not yet known.

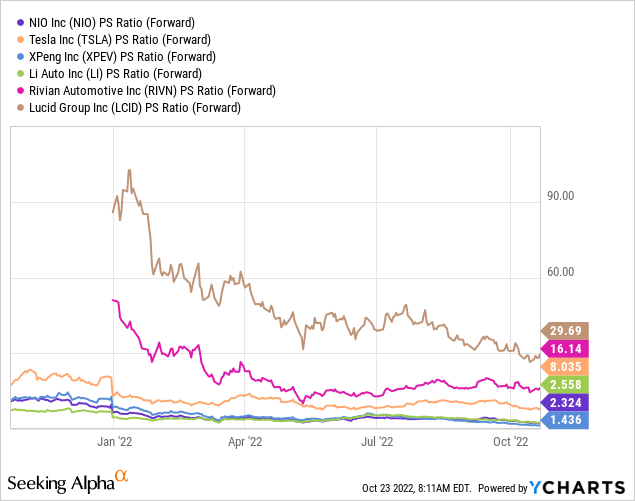

From a valuation basis, NIO does not look very expensive versus other EV players:

XPeng is less expensive than NIO, but other relevant peers such as Li, Tesla, Lucid, and Rivian are more expensive on a price-to-sales basis. Especially the three US-based peers, which are trading at way higher valuations than NIO, which makes NIO look attractive by comparison.

Is NIO Stock A Buy, Hold, Or Sell?

NIO is battling with some supply chain problems, which is why its growth in recent quarters wasn’t overly strong. Still, NIO hit a new record in Q3, and delivered growth in the 30% range, which is far from bad. With the ongoing expansion in Europe, growth could accelerate going forward, especially when/if China eases its COVID policy.

From a valuation perspective, NIO looks like one of the better EV players, as it trades at a hefty discount relative to many of its peers. That being said, there are some China-specific risks that investors should consider. If tensions between China and the US escalate further, an investment in Chinese companies such as NIO could be risky, although that would also impact American companies that are reliant on the Chinese market, such as Tesla.

Overall, NIO has some opportunities, but in the current environment of rising interest rates and macro uncertainties, it is far from a sure bet that NIO will rise in the near term. I thus am neutral when it comes to NIO right now.

Be the first to comment