Henrik Sorensen/DigitalVision via Getty Images

Thesis

Social Capital Hedosophia Holdings Corp. VI (NYSE:IPOF) is a special purpose acquisition company led by venture capitalist Chamath Palihapitiya. On Tuesday, it was announced the vehicle would wind down due to the lack of acquisition targets. The announcement is important due to the size of the fund (approximately $1.5 billion) and the fact that Chamath is known in the venture capital circles as the “SPAC King“. The vehicle was incorporated mid-2020 and targeted technology companies:

We are a blank check company incorporated on July 10, 2020, as a Cayman Islands exempted company, for the purpose of effecting a merger, share exchange, asset acquisition, share purchase, reorganization or similar business combination with one or more businesses. While we may pursue an initial Business Combination target in any industry or geographic location, we intend to focus our search for a target business operating in the technology industries.

Source: Annual Report

The reasoning behind the closure (at least the stated one), was the inability to find suitable deals to undertake. On the positive side, investors are not losing money, the initial $10/share being planned to be returned after clipping US government yields since inception:

Upon the closing of the Initial Public Offering and the Private Placement, $1,150.0 million ($10.00 per Unit) of the net proceeds of the Initial Public Offering and certain of the proceeds of the Private Placement were placed in a trust account (the “Trust Account”) located in the United States and invested in U.S. government securities

Source: Annual Report

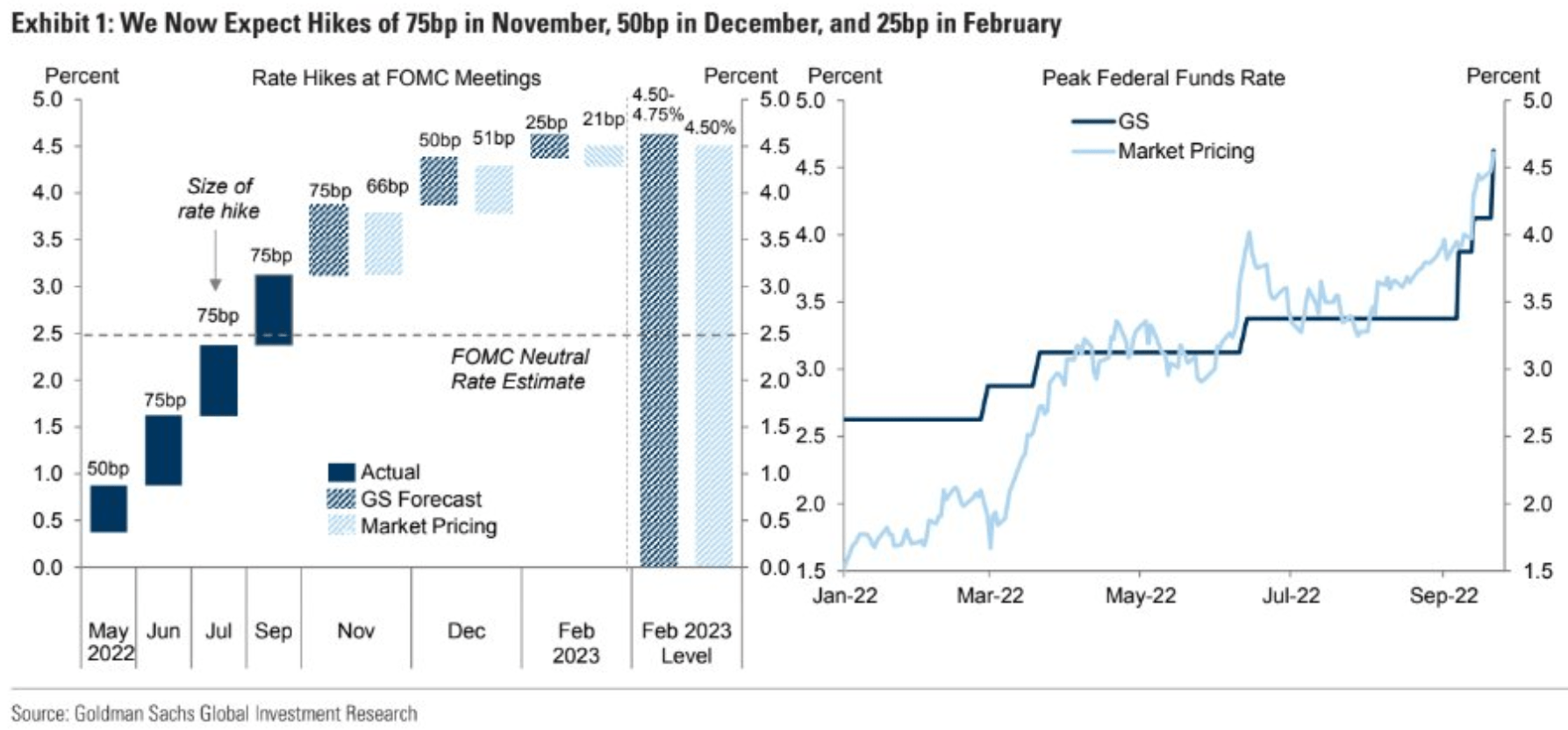

Rates are continuously moving higher and all revisions are moving up:

Goldman analysts […] were revising their forecast for rate hikes to 75 basis points (bps) in November, 50 bps in December, and 25 bps in February, for a peak funds rate of 4.5-4.75%, versus 4-4.25% previously

GS Rate Schedule (Goldman Sachs)

Higher rates are taking the wind out of all classes of speculative assets that thrived on investors’ beliefs rather than actual free cash flows. This is an important macro aspect because until liquidity is drained from “belief assets” we will not have reached a bottom yet in the wider market. The excesses of the past need a complete re-set, and investors who bought securities they did not understand just because a neighbor told them they are the next best thing need to lose a substantial amount of capital to capitulate on the asset class.

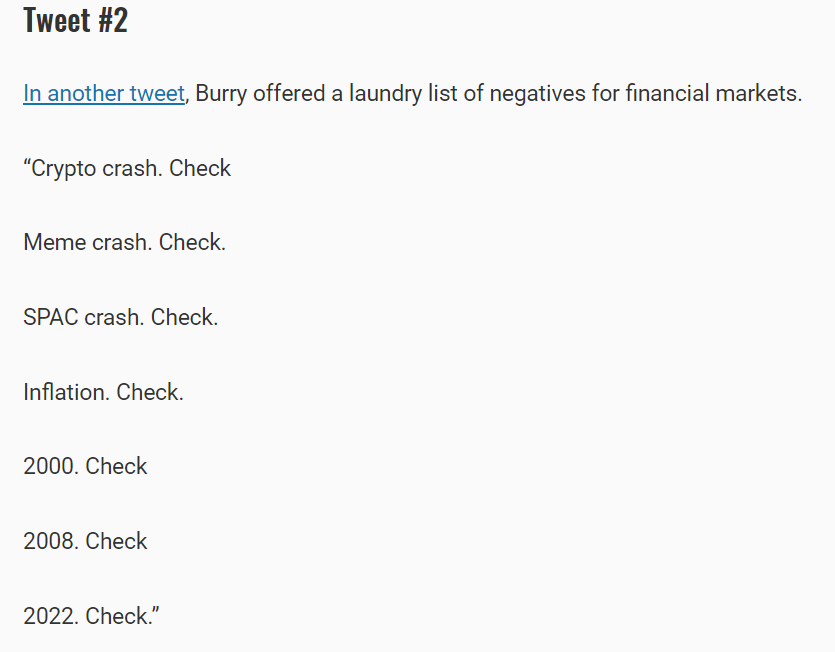

IPOF was coming up on an October 14 deadline to make a deal or be forced to return capital to investors. This closure comes on the back of two SPAC-focused ETFs also closing. Tried and tested investors like Mike Burry are also closely monitoring the demise of prior high-flying speculative assets as a means to assess a wider market bottom:

Tweet (The Street)

IPOF is a good story for investors who bought around the IPO prices because they did not lose any money. Retail holders who bought the mania in late 2020 and early 2021 likely have been taken to the cleaners with the fund’s closure, returning just the IPO pricing. This is a great example of a term fund that if not bought at attractive prices crystalizes substantial losses.

Performance

The vehicle did not achieve any meaningful results during its short life span:

3-Year Total Return (Seeking Alpha)

It is interesting to note, however, the bubble that saw the SPAC’s price balloon to an almost 50% return in early 2021 on the back of nothing more than promises.

This return profile is symptomatic of the 2021 excesses when Tech was the name of the game and simply coming up with a SPAC produced a craze based on belief rather than results.

Conclusion

The announced closure of two SPAC structures run by Chamath Palihapitiya is yet another domino to fall in the current bear market. Liquidity is being drained out of the excesses of 2020/2021 and specifically Tech. Assets which thrived in zero rates and investors’ beliefs are now being taken to the cleaners or wound down. Expect more to occur before we can reach a bottom. Just like RMBS and CDO securities in 2008/2009 we need to see a total capitulation in the speculative assets space before we can call a bottom. Retail investors holding speculative tech names hoping for a “V-shaped” recovery should know better, in our opinion. There is probably more weakness and pain to come, and the market needs to see these investments as pariahs before we can personally call a bottom in the wider market.

Be the first to comment