ejs9

Invitation Homes (NYSE:INVH) shares have declined 35% over the past year, underperforming the broader REIT index/ETF (VNQ). While concerns about single family home values and rising interest rates have led investors to sell Invitation shares, I see the company as being well positioned to capture further rent increases, driving increased NOI, FFO and dividends per share.

In addition to having a favorable forward outlook, Invitation Homes has a strong balance sheet with net debt-to-EBITDA of just 5.5x (and a loan-to-value of only ~25%). Further, Invitation shares trade at an attractive valuation, a 20-25% discount to my estimate of the value of its homes, even factoring in an expected decline in home values going forward (discussed below).

With favorable long-term prospects, a solid balance sheet, and discounted valuation, I see Invitation Homes as an attractive investment for long-term, risk averse investors.

Overview

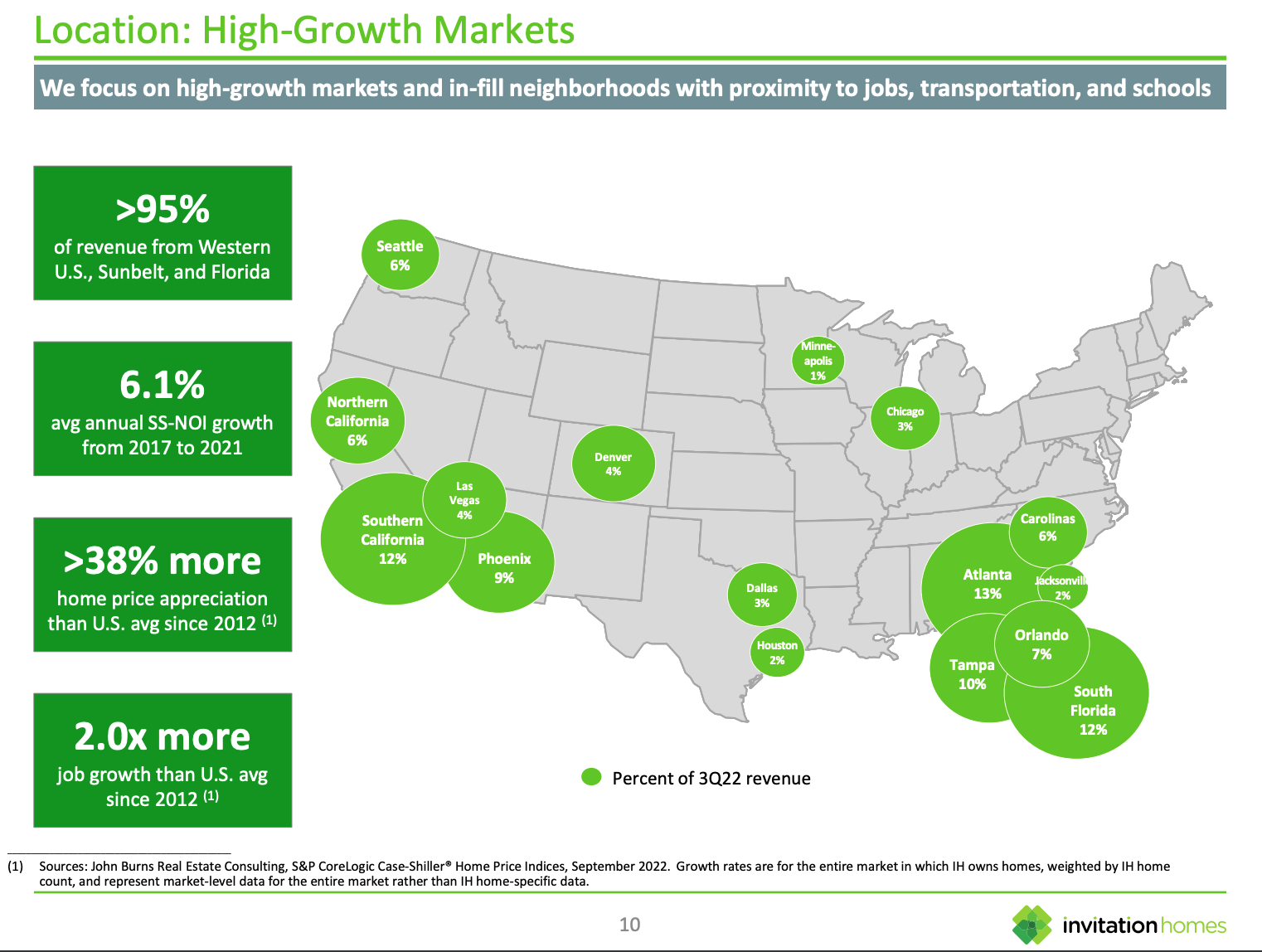

Invitation Homes is the largest owner of single family homes with a portfolio of over 82,000 homes throughout the US. As shown below, the company is focused primarily on markets with above average job and population growth which has translated into very strong same store NOI growth over the past five years.

Invitation Homes – Markets (Invitation Homes Investor Presentation)

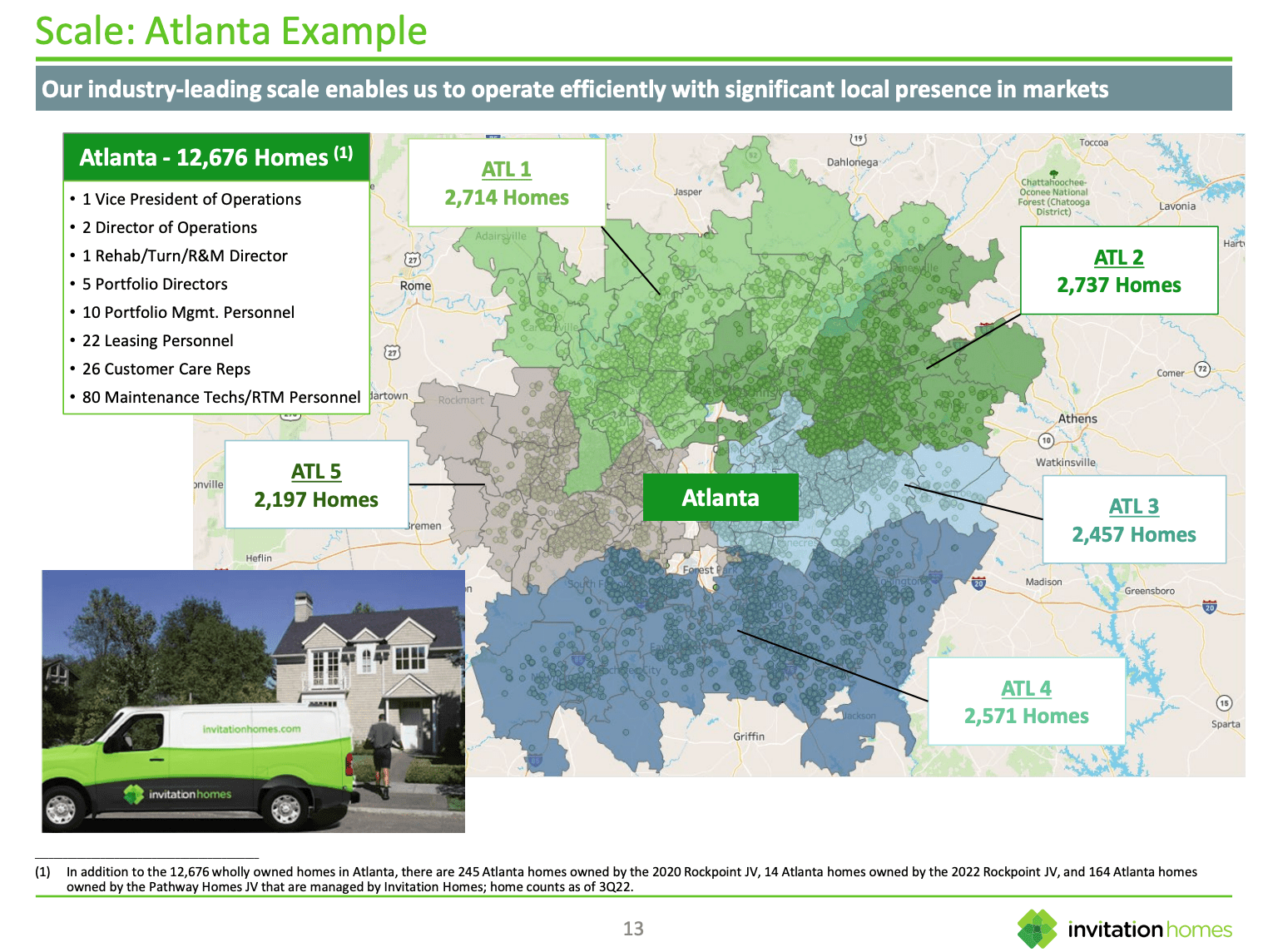

One of the unique aspects of Invitation Homes is its operational platform which allows the company to efficiently service its portfolio of single family homes. While anyone can buy a home and become a landlord, this is a scale/density business. To effectively manage single family homes bigger is much better. Scale allows for in-house provision of services at lower costs. For instance, INVH can hire plumbers, electricians, painters full time and spread the cost out across its vast portfolio of homes. The cost of repairs/maintenance for INVH is significantly lower than for landlords owning only a few houses.

Atlanta – Local Scale (Invitation Homes Investor Presentation)

Local scale and route density are a critical competitive advantage as shown above. On average, INVH owns 5,000 homes per market. This allows INVH to cluster maintenance jobs (aforementioned plumber spends less time driving and can complete more repair jobs per day). These efficiencies have led INVH to achieve NOI margins of ~67%. Put simply, with scale and density INVH retains more of each rental dollar as profit than smaller competitors.

Current Conditions

Invitation Homes had to reduce FY22 NOI growth guidance (from 10.75% to 9% at the midpoint) when it reported 3Q22 results. The main culprit causing slower NOI growth is faster than expected expense growth, namely higher property tax expenses as well as some increased bad debt expenses.

Reduction in Guidance (3Q22 Quarterly Supplemental Report)

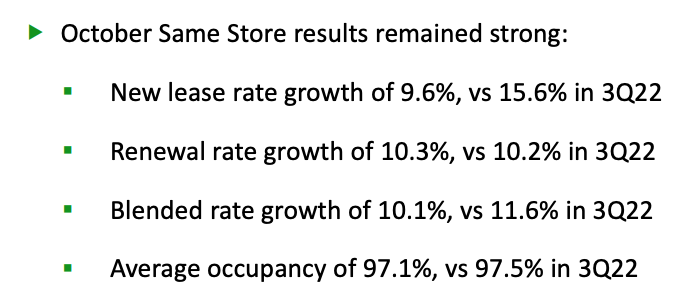

While the share price sold off generally speaking, conditions are quite favorable for Invitation Homes and the outlook remains strong. While rents for multifamily REITs have leveled off (and even started to decline in some markets), Invitation Homes is continuing to see strong rental rate increases (+10.1% blended in October), particularly for renewals as shown below.

October Same Store Rents & Occupancy (Invitation Homes Investor Presentation)

As of the end of September, management estimated that Invitation has a 10% loss-to-lease (rents across the portfolio are 10% below market rents). When coupled with a ~4% earn-in (earn-in is the 2023 benefit from rent hikes which have already been realized throughout 2022) as we head into 2023, the outlook for 2023 NOI growth is excellent. I estimate 8-9%. There may also be an opportunity for Invitation to potentially reduce the rate of growth in property taxes by contesting future increases (given that single family home values are now declining).

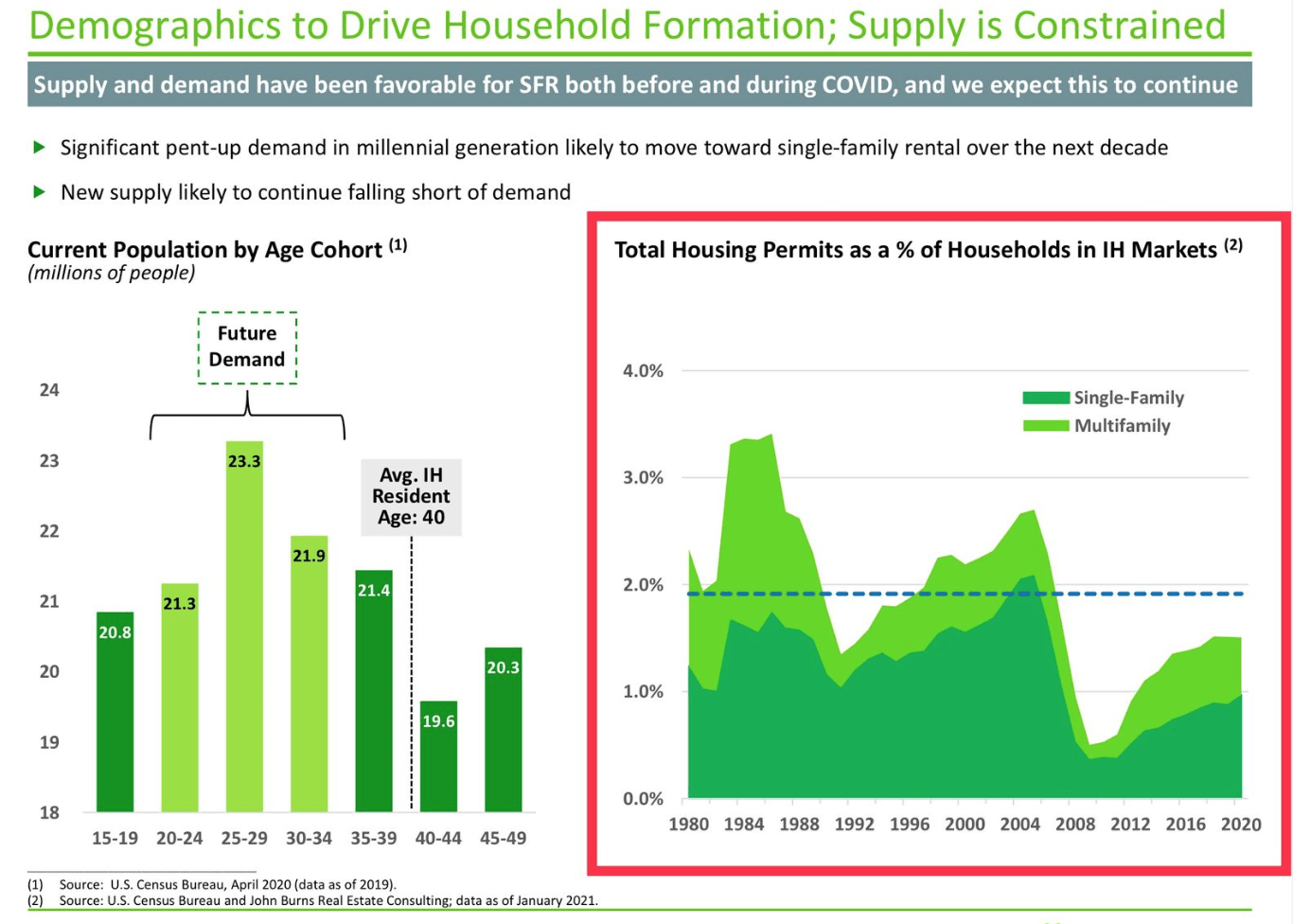

Longer term, Invitation is well positioned for the continued maturation of the millennial generation. As an increasing cohort of millennials continue to wed and procreate, they will increasingly look to rent homes – many have had to put home buying plans on pause given the decline in affordability brought on by rising interest rates. Invitation estimates the costs of single family home ownership to be 25% more expensive (or $600 per month) in its markets. This gap ensures steady demand from renters for years to come.

Demographics Support Invitation Homes (Invitation Homes Investor Presentation)

Valuation

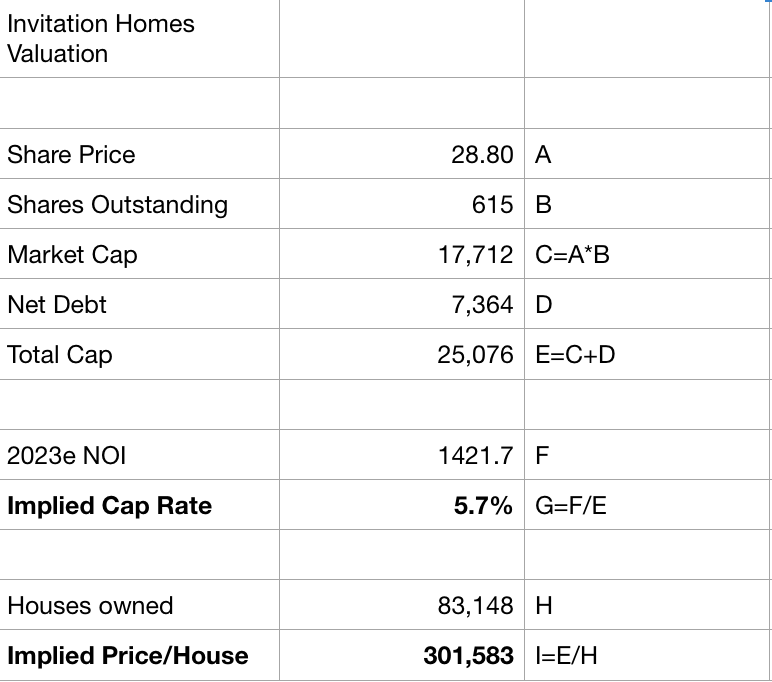

Below I show my implied cap rate and price per home valuation for Invitation Homes:

Invitation Homes Valuation (Company Filings; Author Estimates)

As shown above, at $28.80 per share, Invitation Homes is being valued at just under $302,000 per owned home and an implied cap rate of 5.7% (slightly lower than multifamily REITs which are in the 5.8-6% range).

According to Redfin and Zillow (Z), the most recent available estimate of the median US home price is $390-400,000. However, I believe the median home price in Invitation Homes markets is higher as the company has relatively little exposure to lower priced homes in the Midwest and high exposure to more expensive markets like greater LA, greater SF, and Florida. I believe that the median home value for Invitation is 5-10% above the national average.

While many market observers expect US home prices to decline because affordability has fallen as interest rates have soared, I tend to agree with this view and see a 5-10% decline as likely. Taking into account the expected home price decline but also Invitation’s greater exposure to higher price markets, I think that the fair value per home for its portfolio is in the $380-400,000 range. After deducting net debt, this gets me to an estimated net asset value of $39-42 per share which is 35-45% above the current share price.

Conclusion

With favorable long-term prospects, a solid balance sheet, and discounted valuation, I see Invitation Homes as an attractive investment for risk averse investors.

Be the first to comment