imaginima

On the basis of my filter criteria for small-cap stocks, I’ve been diligently searching for great picks with low revenue volatility, rather than the other way around. Quipt Home Medical Corp. (NASDAQ:QIPT) has a very solid track record, a very positive revenue trend and EBITDA generation trend, and this trend should continue. As the company is expanding positively, primarily due to its acquisitions, there is sufficient room for expansion. Great Elm Group (GEG) has sold its DEM division, Great Elm Healthcare, to the corporation. The acquisition is well-timed and will provide support for higher growth and margin development as a result of synergy effects and cross-selling opportunities.

Brief business overview and company policy

Business overview

Quipt operates in the healthcare sector, which statistically outperforms the market as a whole during the recession. Regardless of whether the recession will last or not, the business model is being substantially impacted by Medicare reimbursement rates, with 35 to 40 percent of revenues being affected. Medicare health insurance policies administered by CMS in the United States may have an effect on the company’s net sales. However, fee revisions should represent a solid CPI rise for DME providers in the range of 6.4% to 9.1% for calendar year 2023.

In the United States, Quipt Home Medical Corp. provides in-home medical equipment and supplies, as well as respiratory and durable medical equipment. It focuses on patients with heart and lung disease, sleep apnea, limited mobility, and other chronic health conditions. The company rents and distributes a lot of these products to people who have selected and comparable diseases. Due to the fact that the fiscal year ends in September, the corporation published their filings for FY 2022 in late December.

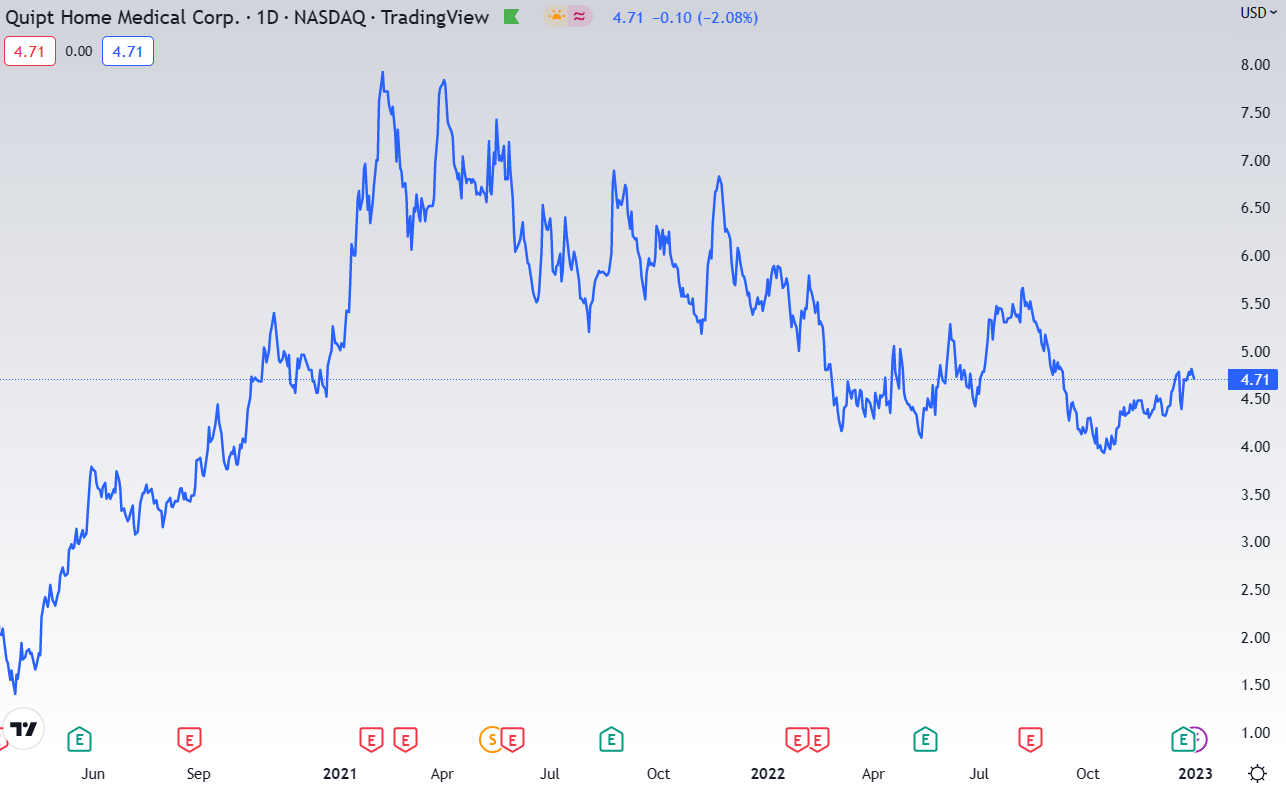

The price has fallen by more than 40% from its ATH, while market value has fallen by “only” -29%. The gap will almost certainly be accounted for by stock dilution in 2021 due to funding requirements.

Quipt Price Chart (Tradingview)

Company policy:

- Increase shareholder value through organic business growth.

- Through its acquisition policy, the corporation is able to acquire not just new patients, but also market share, insurance agreements, and to apply cross-selling of products.

- As the company operates primarily in the healthcare industry, it is not cyclical, but macroeconomic headwinds can have a minor impact on its profitability. Significant weather variations can have an effect on the company’s performance, as its products are in more demand during colder seasons.

- The company’s profitability is essentially determined by reimbursement rates, which are subject to regulatory oversight.

- Quipt Home Medical seeks reimbursement from Medicare and private health insurers, with Medicare serving as the primary payor. This generates a substantial amount of the company’s revenue.

News in FY 2022 and the acquisitions

The firm announced nationwide contracts with the top five U.S. health insurers in April 2022. It is excellent news, as whenever Quipt expands (or makes more acquisitions), the contract will be relevant, making it much simpler to acquire new clients or patients. This significant news provides much possibility for expansion.

By entering into this comprehensive contract with UnitedHealth Group Incorporated (UNH), Quipt has ensured that UNH will pay for its products and services wherever it expands. Due to the fact that UHC is the largest health insurer in the United States, Quipt stands to gain significantly from these national insurance deals. In addition, the transaction enables Quipt to rapidly integrate more equipment and services into the operations of its acquired firms. For instance, if Quipt acquires a company specializing in sleep therapy, it will be easy for Quipt to add its own respiratory or ventilation program, as UHC would already cover these services. There is more specific information in the excellent analysis by Aaron Warwick.

In FY 2022, the company made seven to eight acquisitions that helped to expand its customer base. In the segment the company operates is represented by many little companies (local) in the U.S., but there are similar bigger companies whose strategy is similar – to acquire such tiny enterprises. To be honest, Quipt is currently on the really fantastic track of that. On the other side, there is danger related to the future, about the acquisition policy, because some of the new selects in the future can be the genuinely wrong pick. In spite of a new credit line from banks, shareholders may be concerned about equity dilution for acquisition purposes. However, the corporation will almost certainly be able to generate sufficient cash flow to avoid such step.

A great start into 2023

This week, as of the writing of this analysis, Quipt announced a new acquisition with division of GEG:

We are extremely thrilled to start 2023 with the milestone acquisition of Great Elm Healthcare, which gives us significant coast-to-coast presence across the United States and firmly establishes Quipt as one of the top clinical at-home respiratory providers in the nation. I would like to use this opportunity to extend a warm welcome from the Quipt family to the entire Great Elm team. We are eager to get started. Over 1.5 million people in the jurisdictions serviced by Great Elm suffer from COPD2, and this acquisition positions us to make progress in this primary target market,” said Greg Crawford, Chairman and CEO of Quipt.

The Acquisition adds 8,500 referring physicians bringing Quipt’s referring network base to over 32,500, and increases Quipt’s active patient count by 70,000, bringing Quipt’s total to 270,000 active patients.

According to an unaudited earnings report as of August 2022, Great Elm Healthcare’s revenues for the past 12 TTM was 60 million USD, and EBITDA was 13 million USD. The Quipt acquired the division for $80 million USD, consisting of $73 million USD in cash, $5 million USD in debt, and 430 thousand shares of Quipt at a price of $4.63 per share. The purchase price is equal to 6 times Great Elm’s EBITDA. Quipt utilized senior security credit facility funding ($73 mil. of USD from $110 mil. of USD).

This acquisition is a fantastic deal for Quipt, primarily due to synergy effects totaling $2 million only in the first six months. Cross-selling and synergy effect enable the company to enhance not only its sales but also its profits as a result of the business transformation. Organic growth can be even more robust.

Great improvements in revenues and margin

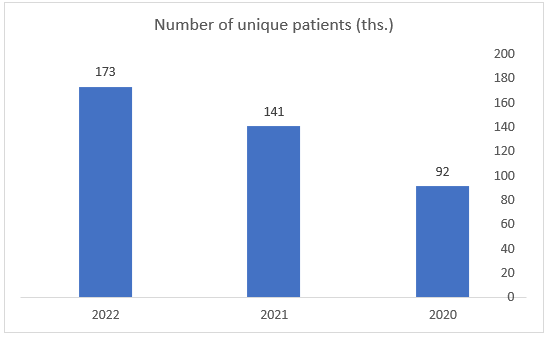

The company’s success in delivering its services and products is mostly attributable to its acquisition policy, but also organic growth. As of fiscal year 2022 (as of September 2022), according to the most recent data, the number of patients is expanding quite rapidly. However, in the most recent earning call, the CEO stated that the company has reached 200,000 active patients.

Number of unique patients (Quipt fillings)

According to the news, the annualized revenue by the end of the first fiscal quarter of 2023 should be between $180 and $190 million.

Based on the income statement, the majority of the company’s revenues were generated from acquisitions rather than organic growth. However, the corporation made a significant number of successful acquisitions and remained quite effective as a result. In the medium to long term, it will result in solid organic growth for the company, as well as an abundance of cross-selling opportunities and synergies.

Despite the fact that sales are mostly determined by reimbursement rates, which tend to increase with inflation, the synergy impact and access to new markets allow for additional margin increases. Based on the bullish industry outlook and already acquired market share, I believe this company is at the point where it may grow by 8-14% YoY even without further acquisitions.

During fiscal year 2022 (12 months to September 2022), the corporation achieved a 37% increase:

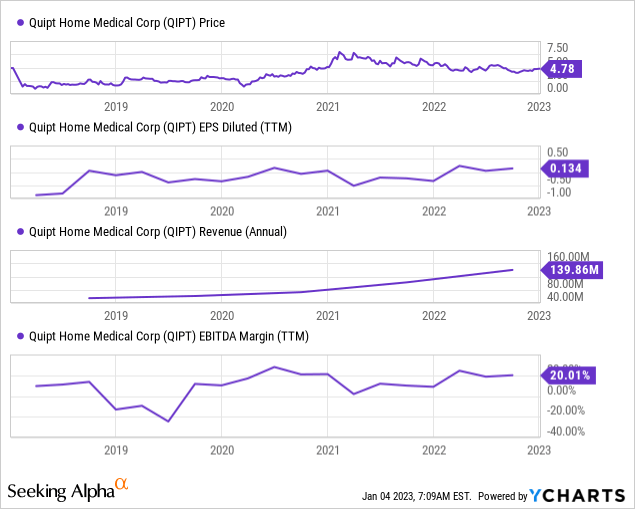

Revenue for fiscal year 2022 was $139.9 million compared to $102.4 million for fiscal year 2021, representing a 36.7% increase in revenue year-over-year. Recurring revenue as of fiscal year 2022 continues to be strong and exceeds 77% of total revenue. Adjusted EBITDA for fiscal year 2022 was $29.2 million at 20.9% margin compared to adjusted EBITDA for fiscal year 2021 of $21.4 million, representing a 36.5% increase year-over-year. Net income for fiscal year 2022 was $4.8 million or positive $0.13 per fully diluted share compared to net income for fiscal year 2021 of a loss of $6.2 million or negative $0.20 per fully diluted share.

In the following charts, we can examine some of the most important components of the Income Statement. The revenue trend is really optimistic and encouraging. The EBITDA margin is relatively solid at 20%, although has fluctuated significantly between quarters.

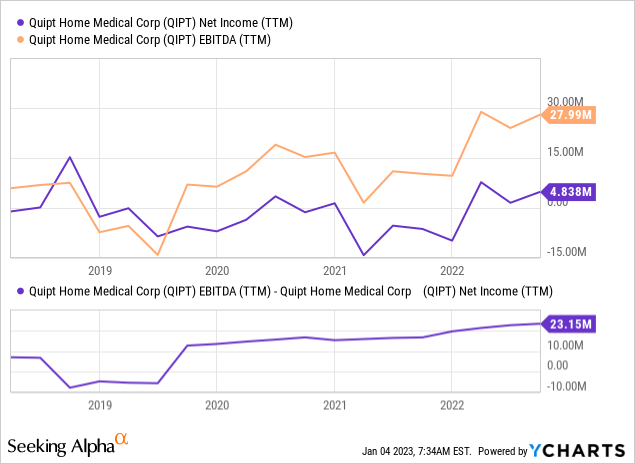

The relationship between EPS or Net Income trend and EBITDA margin indicates that EBITDA generation is essential to the company. Based on the most recent three-year evolution, the gap between EBITDA and Net Income has been marginally growing but remains stable. It is essential for EPS forecasting. Interest can be found under EBITDA, and with the current senior debt loaded to finance a new acquisition, the spread will continue to expand modestly.

However, based on Quipt and Great Elm’s annualized EBITDA figures, the annualized EBITDA would be as follows:

Annualized Adjusted EBITDA as used in this press release is calculated as Quipt’s Adjusted EBITDA for the three months ended September 30, 2022 of $8.4 million multiplied by four, or $33.2 million, plus Great Elm’s Adjusted EBITDA of $13.4 million, for a total of $47 million.

Quipt’s shares climbed by 7% in pre-market trading, but according to new criteria, the company’s EV/EBITDA ratio would decrease considerably, making it an extremely inexpensive stock relative to its sector and past performance.

Pre-transaction valuation:

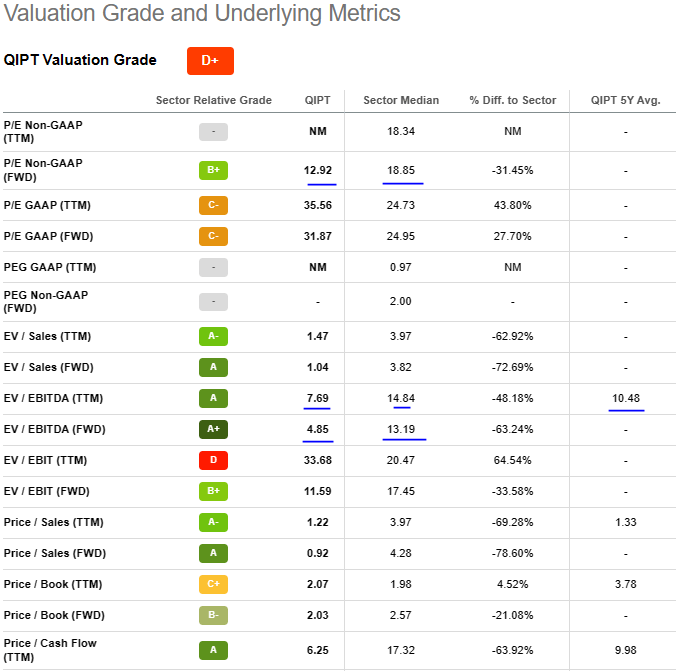

Valuation Grade (Seeking Alpha)

When the stock’s price reached $4.78, its EV/EBITDA ratio reached 7.69, considerably below the industry median of 14.84 and the 5-year average of 10.5. The forward EV/EBITDA ratio was 4.85 vs 13.19 for the industry. The forward P/E Non-GAAP attained a relatively conservative 12.92, compared to the sector average of 18.85. Keep in mind that these numbers are pre-acquisition.

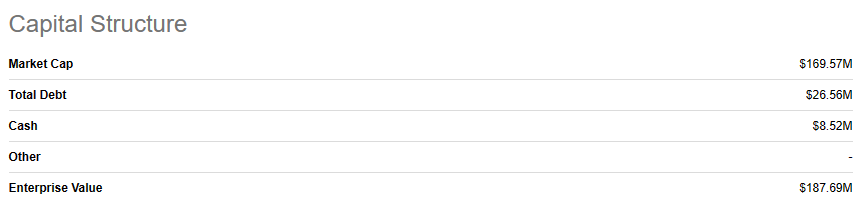

Enterprise Value (pre-acquisition) (Seeking Alpha)

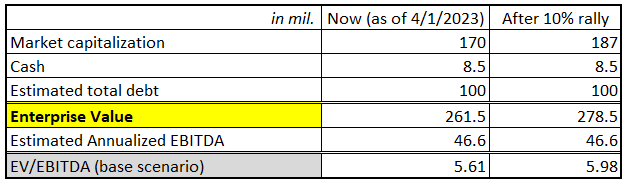

Assuming that the stock would increase by 10% in response to the news, the market capitalization would be close to $187 million USD (170 million USD as of 4/1/2023). As of 4Q2022, the cash position was USD $8.5 million and the debt was USD $27 million. However, the debt estimate is inaccurate because the corporation utilized a USD $73 million senior security facility (from $110 mil. of USD). These funds were used to complete the acquisition. Therefore, we should include it into EV calculation.

Regarding total debt, we must add the $73 million USD. It totals $100 million. The pre-acquisition EV/EBITDA ratio was 7.69, and the annualized EBITDA resulted in a considerable improvement to 5.61. Overall, it appears to be a wonderful deal.

EV/EBITDA on Annualized EBITDA (Author´s calculation, Data from Quipt (press release))

Okay, but historical data and mainly annualized performance may not necessarily be the best indicator of the company’s future. Now, let’s examine future assumptions.

Once Great Elm’s sleep patients are included to Quipt’s resupply program, there is a big opportunity to increase sales and profitability, according to the firm. This is one of the most significant benefits of this transaction. The Quipt EBITDA margin is reached 20% by fiscal year 2022. According to the most recent earnings call, the EBITDA margin should be stable and improve. But in my view, I see the lower boundary at 19% and the top limit at 22% (conservatively speaking). My viewpoint is supported by the CEO’s view earnings call:

We are operating in an extremely bullish regulatory environment, which was most recently evidenced by the Medicare fee schedule adjustments resulting in a significant CPI increase for DME providers for calendar 2023 of 6.4% to 9.1%. This CPI adjustment is extremely meaningful for us in 2023 as we have seen margins stabilize and believe peak inflation has already run through our business to date. As a result, we believe that the CPI increase will have a materially favorable effect on our net income in calendar 2023.

Finally, the underlying positive regulatory environment is anchored by the decision CMS has made to cancel the 2021 competitive bidding program for 13 product categories. The cancellation of this program has provided us with a clear margin outlook across our product mix and ensured our patient stability for the foreseeable future. We are glad to see these ongoing favorable regulatory improvements because the need for the home medical industry has never been greater.

Based on this assumption, I expect the margin to increase rather than decrease. On the other hand, I would rather value the business using a more conservative dataset with lower growth and would use only 8-10% organic growth in revenues, as is mentioned in the latest earnings call in Q4:

We saw steady and timely inventory allocations of sleep devices through fiscal Q4 and in real-time in fiscal Q1 and continue to drive patient setups. This real-time development is anticipated to be a powerful tailwind and to significantly contribute to our organic growth in the upcoming year.

Medicare has been a decent percentage, almost 40% of our revenue, 35% to 40% of our revenue. And the weighted average, if you look at the CPI increases from 6.4% to down 9%, so somewhere in between is where we would put a weighted average. So we can all factor in what that organic growth would look like just from a CPI increase plus the additional growth from this availability of devices and the recurring nature of those, we do suddenly expect us to, at a minimum, hit our historical growth rate, which was kind of somewhere between 7% to 10% in the past to hit in 2023.

Sensitivity analysis on EBITDA and valuation

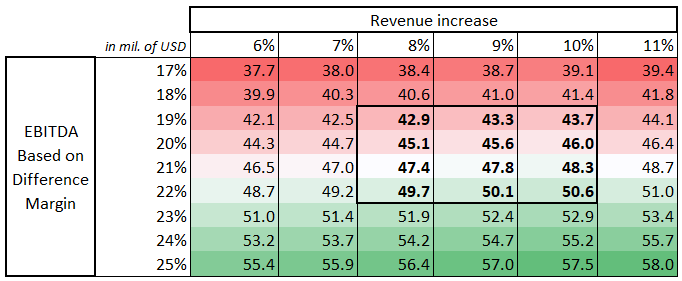

Okay, now let’s incorporate it into our assumption via sensitivity analysis. Keep in mind that organic growth of 6.4% to 9% should only be achieved through CPI; further growth potential exists, but we will be somewhat conservative. My revenue projections for the first year are based on the combination of Quipt and Great Elm (division) to total $209 million USD ($139 mil. for Quipt as for FY 2022 and $70 mil. of USD for Great Elm TTM).

Sensitivity analysis, based on Revenue and EBITDA margin (Author´s calculation)

I ran some scenarios based on the increase in pricing and the continued strength of demand. If nothing breaks in the sector dramatically or there isn´t some major impact from the U.S. government, this is my probability outcome:

- There is a high likelihood that overall revenue will climb by 8 to 10 percent, as a result of an increase in reimbursement rates and extra organic growth. We used conservative revenue calculations = $209 mil. USD as a starter, despite management sees $220 mil. of USD.

- My conservative, base case estimate for EBITDA is bolded in the table, or between $42.9 and $50.6 million. The range of EBITDA margin is 19-22% of USD.

- I must emphasize that this is a conservative perspective, as the new acquisition will have a substantial influence on cost reduction and may result in improved cross-selling prospects. Based on the text below, I believe there is a far greater likelihood of achieving a larger EBITDA margin and revenue growth than my projection.

- Due to its anticyclical nature, healthcare is an excellent area in which to invest during a potential recession.

- As previously noted, the company’s chief executive officer claimed that this is the best time period in terms of regulatory conditions, and that the reimbursement rate will fuel the company’s profitability.

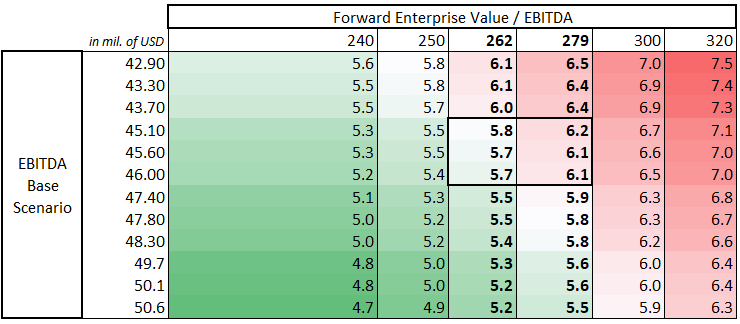

Based on this result and the present Enterprise Value, which is close to $262 million US or $279 million US after a 10% increase (in price), we may calculate Forward EV/EBITDA with sensitivity analysis as before:

Sensitivity analysis – Fwd EV/EBITDA (Author´s calculation)

This sensitivity analysis is based on the range of EBITDA margins from 19 to 22%. ($42.9 – 50.6 mil. USD). But the bolded range of 45.1 to 46 million USD (on the left) shows the EBITDA in absolute terms with a 20% margin, based on sales growth by 8 to 10%.

So, the most conservative result of this analysis is that the right range for Forward (2023) EV/EBITDA is between 6.1 and 6.2, assuming a 20% EBITDA margin and an increase in sales of 8–10%. I assumed the market cap would go up by 10% after the acquisition announcement (also assumed new debt). So, going forward (2023):

- Is not 4.85 as in the previous shot from the SA valuation because it does not reflect new additional debt or potential additional EBITDA because the information is very new.

- Differs from 5.89 (upper stated in the table) because the previous EV/EBITDA was calculated by using annualized data from management.

- The outcome of 6.1–6.2 is still very conservative and could be lower at 5.5 if EBITDA margins are higher.

Summary and risks

Quipt is a small-cap company with numerous risks. First and foremost is the future acquisition policy, which is uncertain because a large trade can result in a disastrous deal, halting a large number of sources from the balance sheet (cash or extra finance), thus could worsen financial health. If such a circumstance happens, it could jeopardize future financial stability. The company may potentially issue new shares if additional financing rounds are required for further acquisitions. The liquidity position may also be a factor in a further stock dilution, particularly if the business performs poorly. On the other hand, the corporation still possesses a substantial amount of capital (credit facility).

However, these risks are mitigated by the solid revenue and EBITDA trend and the impressive track record of management. The issuing of stock should not be considered currently, since Quipt Home Medical Corp. can earn sufficient cash for future investments. In the coming years, reimbursement rates and regulatory perspectives may pose a problem.

The company’s revenue and earnings before interest and taxes (EBITDA) are growing steadily and predictably due to its successful acquisition strategy. The reimbursement rate should improve by 6 to 9 percent in the future, what is highly positive. As indicated by management, the company’s regulatory position is the greatest it has ever been, which should help to boost revenues and margins.

Quipt Home Medical Corp.’s revenues have increased continuously for 8 to 9 quarters and, according to yearly reports, for more than 4 years. This trend will continue in 2023 as a result of the new acquisition. This small-cap stock has tremendous growth potential for the next one to three years and is also attractively valued, with a forward EV/EBITDA ratio of approximately 6.1-6.2 based on conservative calculations.

The average EV/EBITDA ratio for companies over the past five years is 10.5, while the average for industries is 14-15. The company should become solidly profitable in 2023 and 2024 due to its robust, low-volatility business strategy. In addition, the business began to create substantial cash from its operations, but the majority of the new cash was spent on acquisitions as the company’s main strategy. Price to cash flow is between 6-7, which is extremely low in comparison to the sector (P/CF = 17) and its past performance (P/CF = 10)

This small-cap stock is, in my opinion, an exceptional opportunity. As a result of the new acquisitions, as well as solid gains in organic growth and new contracts with insurance firms, the Quipt Home Medical Corp. stock price could increase dramatically. In one to three years, the stock might provide a double or triple-digit return.

Editor’s Note: This article covers one or more microcap stocks. Please be aware of the risks associated with these stocks.

Be the first to comment