tomap49

Thesis

We believe that platinum will be a profitable investment in 2023 due to a combination of favorable macroeconomic and fundamental drivers. On the macro front, the anticipated depreciation of the dollar, along with looser financial conditions in the United States as inflation moderates, will increase demand for risky assets, such as commodities like platinum. On the fundamental front, platinum prices will be supported by supply-side constraints at Norilsk (OTC:NILSY), a shrinking recycled autocatalyst supply, firmer platinum consumption due to substitution for palladium in light-duty gasoline vehicles, and regulations aiming at lowering pollution in the automotive industry. As the supply-demand balance of the platinum market tightens and the macro backdrop for commodities becomes more favorable, we believe that platinum prices will appreciate in 2023.

We believe that the Aberdeen Standard Physical Platinum Shares ETF (NYSEARCA:PPLT) could be an excellent option for investors to profit from our thesis regarding the anticipated price increase of platinum in 2023. By investing in PPLT, investors can obtain exposure to physical platinum bullion and potentially profit from the favorable macroeconomic and fundamental variables that we believe will drive the price of platinum upward.

Yahoo Finance

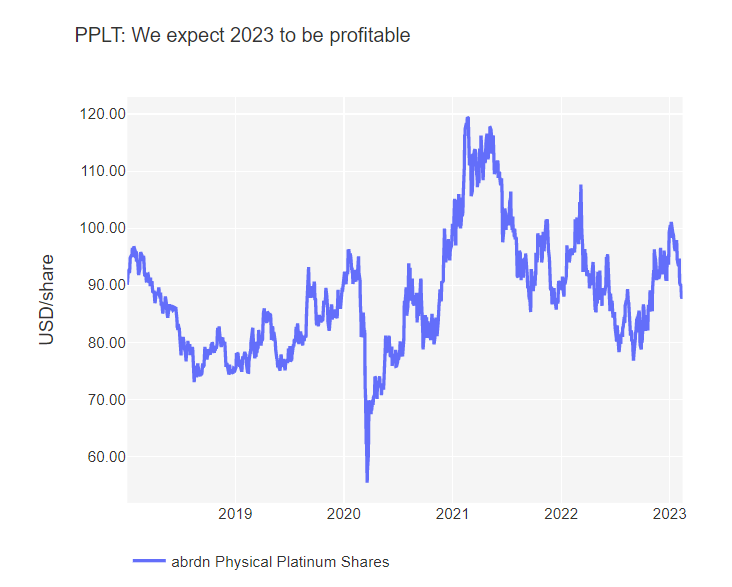

Aberdeen Standard Physical Platinum Shares ETF

The Aberdeen Standard Physical Platinum Shares ETF is a physically-backed exchange-traded fund (ETF). The fund’s base asset is platinum bullion, and it tries to track the performance of the price of platinum. It is designed to provide exposure to the platinum market for investors who are interested in this precious metal as a potential investment opportunity.

Cost

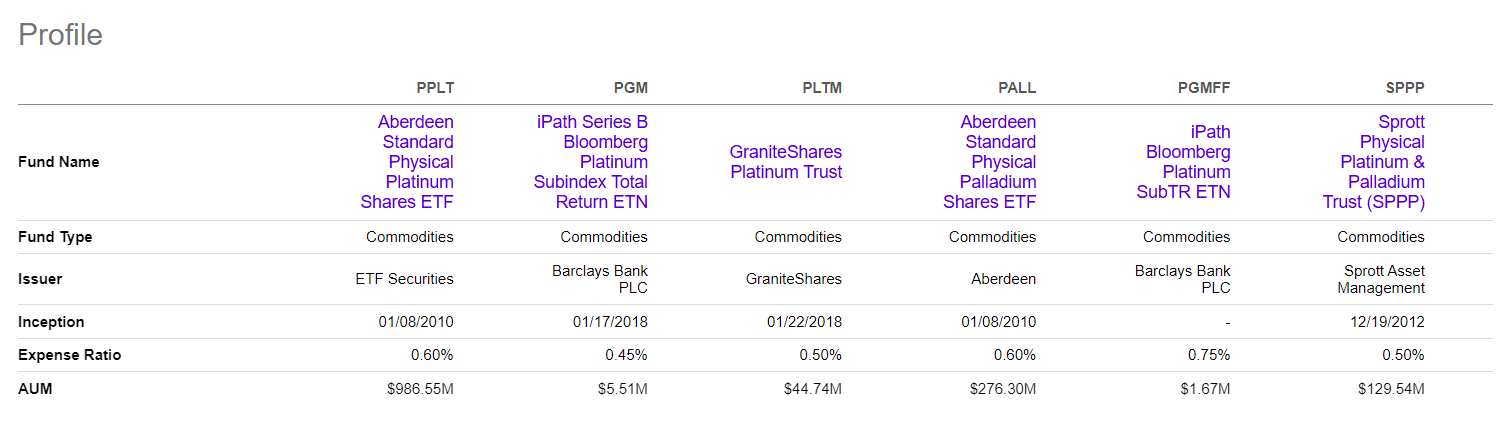

PPLT has an expense ratio of 0.6%. A fund’s expense ratio is the annual price it charges to cover its operational expenses, including management fees, administrative costs, and other costs. The expense ratio is subtracted from the fund’s returns and is expressed as a percentage of the fund’s average net assets.

Seeking Alpha

The expense ratio of PPLT is slightly higher than its competitor, the GraniteShares Platinum Trust (PLTM), which has an expense ratio of 0.5%. However, PPLT has larger assets under management (‘AUM’), providing better liquidity conditions and tighter spreads for investors seeking to enter or exit a position.

PPLT is currently trading at a discount of 1.84% based on its Net Asset Value (‘NAV’).

Aberdeen

The Outlook for Platinum

Like most commodities excluding agriculture and energy, platinum came under pressure in 2022 as a result of a negative macro backdrop, characterized by a stronger dollar index as the Fed tightened massively, poor risk-taking appetite, and a slowdown in the Chinese economy due to the tight Covid policy implemented in the country. As we move toward 2023, these macro headwinds are expected to become macro tailwinds. Indeed, the dollar is likely to come under downward pressure as the Fed becomes less hawkish than it was in 2022 on the back of softer inflation data. Easier financial conditions in the United States will prompt investors to rebuild long positions across risk asset classes, including commodities. Finally, economic activity in China is due to rebound as the country ends its zero covid policy. This positive macro backdrop for commodities should stimulate speculative and financial demand for platinum. This follows significant ETF outflows in 2022 and a contraction in net long speculative positions in the NYMEX.

At the fundamental level, the supply-demand balance of the platinum market could tighten in 2023. On the supply side, platinum production could be negatively impacted by production issues at Norilsk due to its limited availability of spare parts and equipment, power availability limits in South Africa, and scheduled smelter maintenance. Furthermore, platinum consumers in the West could migrate away from Russian PGM material as contracts are renewed, which would elicit market volatility. Finally, the availability of recycled autocatalyst has tightened because cars remain on the road for longer, so recycled platinum supply may emerge with a delay.

On the demand side, we acknowledge that in the automotive industry, the consumer mood is poor, costs are higher, and higher global interest rates may hurt demand. In addition, most of the growth in automotive sales is attributed to electric vehicles powered by non-platinum batteries. Having said that, regulations in developed market economies, like the Euro 7 regulations, whose objective is to tighten pollution standards, will continue to be beneficial for platinum and stimulate demand in the industry.

Another positive force for platinum is the substitution for palladium in light-duty gasoline automobiles, which should boost platinum consumption at the expense of palladium demand.

As the supply-demand balance of the platinum market tightens in 2023 and the macro backdrop becomes more favorable for commodities, we expect platinum prices to move higher.

Conclusion

To sum up, we believe that the confluence of positive macroeconomic and fundamental drivers suggests that platinum could be a profitable investment in 2023. As a result of supply-side constraints and legislation aimed at decreasing pollution in the automobile industry, the supply-demand balance of the platinum market may tighten. Despite having a slightly higher expense ratio than its competitor, investing in the Aberdeen Physical Platinum Shares ETF could provide exposure to a potential increase in platinum’s price. We predict that platinum prices will rise as the macro environment for commodities improves, making PPLT an attractive investment for investors seeking exposure to platinum.

Be the first to comment