LL28/E+ via Getty Images

Intuitive Surgical (NASDAQ:ISRG) makes what it calls robotic surgical equipment, though a more accurate description would be equipment that allows a surgeon better control and vision than in the old hand-me-a-scalpel type of procedure of yore. These robots, the da Vinci series, tend to cost over a million dollars each, so each one is a major investment for a hospital or clinic. After a rapid growth period lasting over a decade, the company saw earnings decline in Q3 2019, and they have mainly stayed at about that low level for the past few years. My current thesis is that the growth rate will remain relatively low, so Intuitive stock should be priced as if it has an established company with at best a moderate earnings growth rate. On that basis, the stock is a Hold until earnings have had time to grow enough to justify the current stock price. I will, however, look at some potential upsides to this scenario.

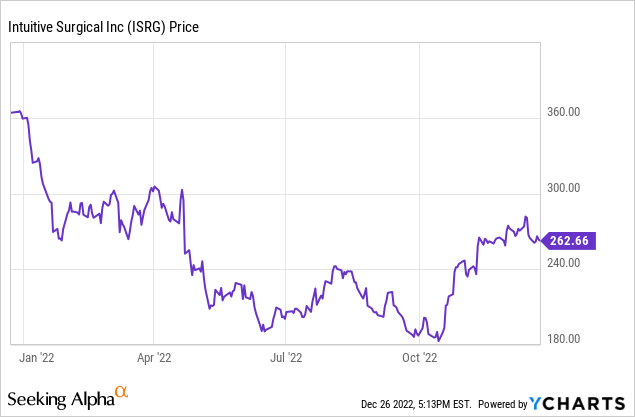

Q3 2022 Intuitive Surgical Results

Intuitive breaks down income into three components: sales of surgical systems, sales of instruments and accessories, and sales of services, which is largely maintenance of systems. For Intuitive Surgical’s Q3 2022, the company reported selling 305 da Vinci systems, down 9% from 336 in Q3 2021. Revenue from sale of systems was $426 million, up 3% from $415 million a year earlier, indicating the average system price increased. Instrument and accessories revenue climbed 15% y/y to $872 million. Services revenue of $260 million was up 12% y/y.

It is important to understand that the number of systems sold y/y can decline, yet the total revenue (and hopefully profits) can increase. Each newly installed system, when used for surgeries, generates new instruments and accessories revenue. When maintenance is needed, it generates services revenue. Despite the lower number of system sales, total revenue in Q3 was $1.56 billion, up 11% from $1.40 billion a year earlier. Because of increased costs, however, GAAP net income dropped 15% y/y to $324 million. That works out to $0.90 per share, down from $1.04 per share in Q3 2021. On a non-GAAP basis, net income was down 1% y/y to $429 million.

At the end of Q3, Intuitive reported a cash and equivalents balance of $7.39 billion, with no debt. In the quarter, it helped keep its stock price high by spending about $1 billion on share buybacks. The company does not pay a dividend.

2023 Prospects

Intuitive Surgical’s prospects for 2023 depend on four major variables. One is the ability of hospitals and clinics to make capital purchases. Second is the clearance of new procedures and indications by regulators. Third would be overall demand for procedures. Finally, there is the potential impact of competition. Costs and supply chain issues had an impact in 2022, but I believe that is largely in the past.

Between roughly 2005 and 2015 it was very easy for a hospital to rationalize buying a da Vinci system. Generally, da Vinci made surgeries safer and faster. In particular, by minimizing incision sizes, patients healed faster. If one hospital in an area could offer a robotic surgery and another could not, patients and even surgeons would migrate to the better-equipped hospital. This created competition that helped drive the rapid growth of Intuitive’s sales.

That dynamic may still exist in some nations or even in areas of the United States, but it has largely tapered off in the developed parts of the world. We see that in Intuitive system sales dropping in Q3 2022 compared to Q3 2021. Meanwhile, the pandemic and other changes during the past few years have negatively impacted hospital profitability [See WA Hospitals’ Huge Financial Losses Continue]. The ability of hospitals to pay for new robotic systems is currently constrained. Given the available picture, I expect unit system sales to be flat in 2023, plus or minus 10%. Revenue should grow because at whatever level of system sales there is within this range, procedure sales revenue will grow, as will service revenue. Profits should grow with revenue unless costs are inflating faster than Intuitive is able to raise its own prices.

Potential Upside

In addition to selling new machines, Intuitive could have new procedures and instruments approved by regulators. It could gain traction in nations that are not yet saturated with machines. If procedures have been delayed by the pandemic, the pace of procedure expansion may pick up in 2023. It is difficult to put numbers on these unknowns, so I see these areas as similar to 2022, until data proves otherwise.

Potential Downside

Other companies make surgical robots, or at least are developing them. That is how classical capitalism works: if there is a particularly profitable sector of the economy, it will attract competitors. I would review the competition before investing in Intuitive, but I am not likely to invest at current prices. My take from following the field for many years is that the competition is having trouble keeping up with Intuitive’s pace of innovation. I do not see much downside from this variable in 2023, but I could be underestimating rivals’ capabilities.

Conclusion

Although it does not operate with the regularity and predictability of Newton’s law of gravity, there is a law of gravity in financial markets. The point of buying stock is to capture profits in the present and then into the future. A high-growth company should have its stock priced differently than a low-growth company, with a spectrum of moderate growth companies between the high band and low band. For over a decade, Intuitive Surgical was priced as a high growth, high profit margin company. I see it as a great company, one that has done patients and the medical world a lot of good. But it is now somewhere in the moderate growth range, with no obvious path to significantly faster growth. It could even be simplified to the reality that growing fast on a high base is much harder than growing fast on a small base.

Based on moderate growth expectations, I do not see Intuitive Surgical meriting a PE (price to earnings) ratio above 30. Its current forward estimated PE is 55. I would not be surprised to see the stock price drop back to the 52-week low of $180.07. But given how much money Intuitive has made for its investors since its inception, I also would not be surprised to see it keep its glow for a while longer, perhaps even years. In mid-October, it surged 10% after reporting Q3 earnings because it beat analyst estimates. Yet it is still well below its 52-week high of $369.21. That high seemed very out of touch with reality, since it was far above its pre-pandemic prices, when Intuitive’s growth rate was significantly higher.

Be the first to comment