hudiemm/iStock via Getty Images

Thesis: This Small Fish Has Potential

I have to admit something right off the bat.

The following company is not in my sphere of competence. I am a neophyte to information technology services and digital transformation. But I am nevertheless intrigued by it, and considering the paucity of available information or analysis on this company on Seeking Alpha, hopefully you’ll forgive my feeble attempt to tackle a stock outside of my lane.

Broadly speaking, though, I consider my lane to be dividend growth stocks, and in Information Services Group (NASDAQ:III), I think I may have found a brand new one – only one year old in dividend growth years.

Can ISG grow and mature beyond the DGI baby stage into an “adult” dividend growth stock? In other words, can the company extend that record indefinitely? If so, buying this tiny, ~$240 million market cap stock today could be an excellent long-term decision.

That’s the purpose of this article. Let’s find out.

Intro To ISG

As the name implies, ISG is an information services company. What does that mean?

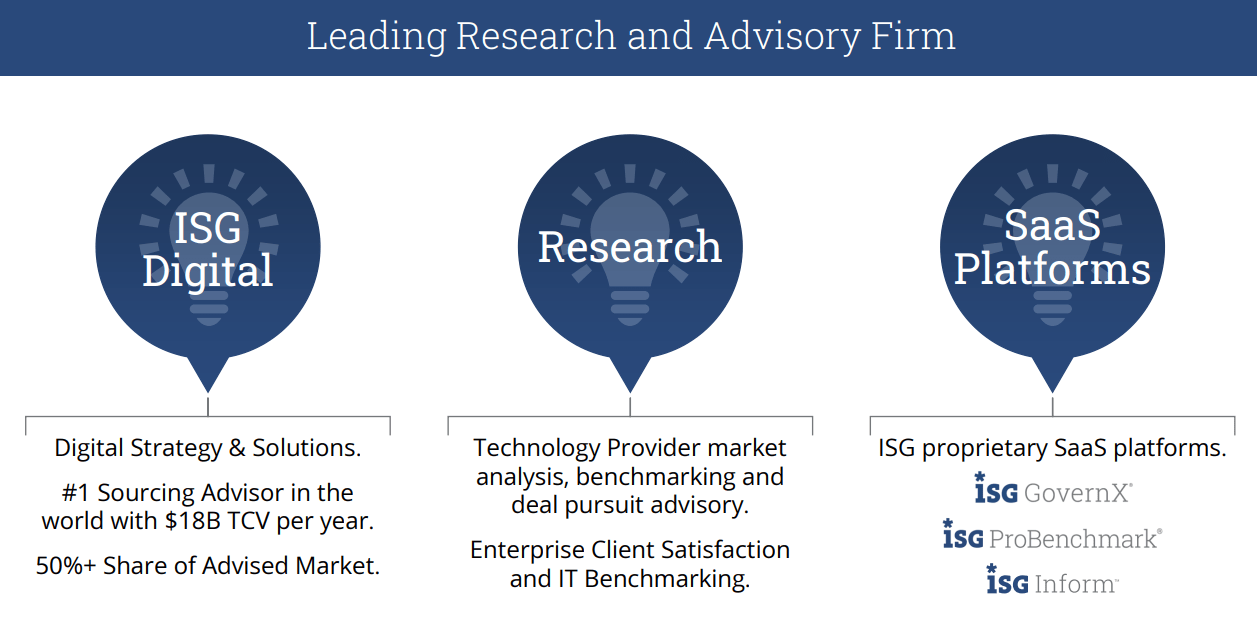

Well, ISG provides consulting and technology services to various businesses, organizations, and government entities across half the planet, primarily for the purpose of digital transformation and modernization of product offerings and/or customer experience. But ISG also provides advisory services in the areas of change management (any substantial change an organization is undergoing), automation, outsourcing, and cost savings.

III Q3 2022 Presentation

ISG proports that its business model is to provide “must-have” information-based services to organizations in the fields of consumer products, retailing, financial services, manufacturing, media, marketing, healthcare, legal, government, telecommunications, and technology.

The goal of ISG in working with a client, and the reason a client would pursue ISG’s services in the first place, is to increase the client’s operational efficiency and the efficacy of its mission.

Digital transformation services is a fast-growing line of business that could give ISG the opportunity to profit from the growth in cloud computing, app modernizations, cyber security, adapting to the workplace of the future, and hybrid work-from-home situations.

III Q3 2022 Presentation

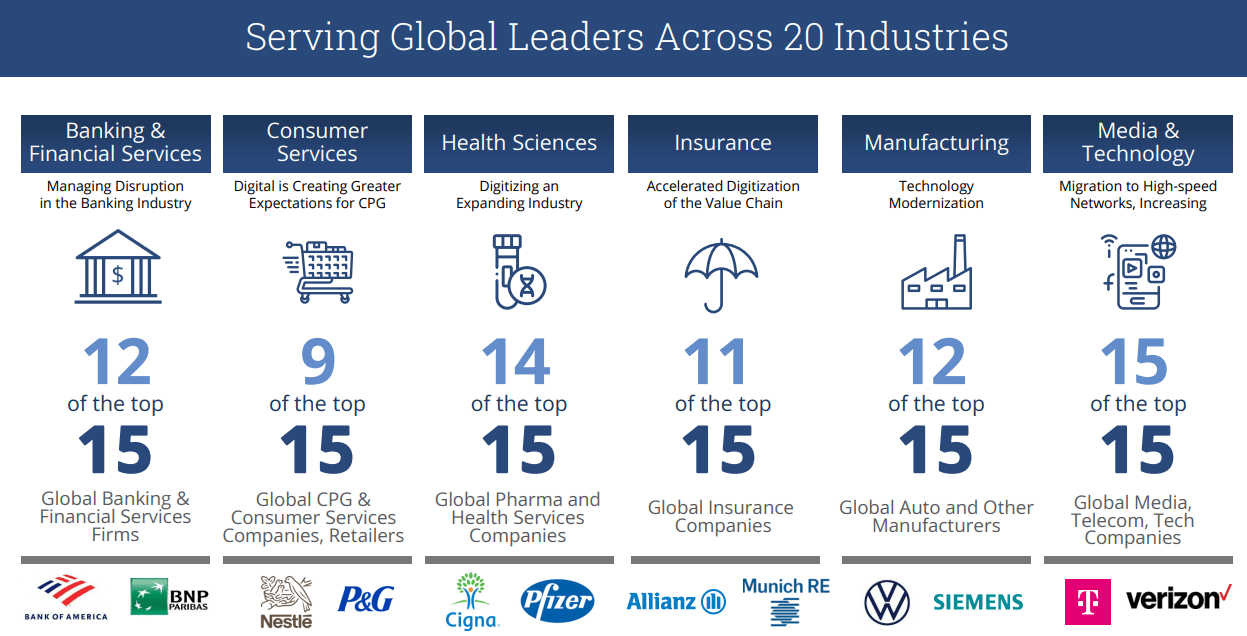

Despite being a relatively tiny company by market cap, ISG has worked for some of the largest corporations in the world across multiple sectors.

III Q3 2022 Presentation

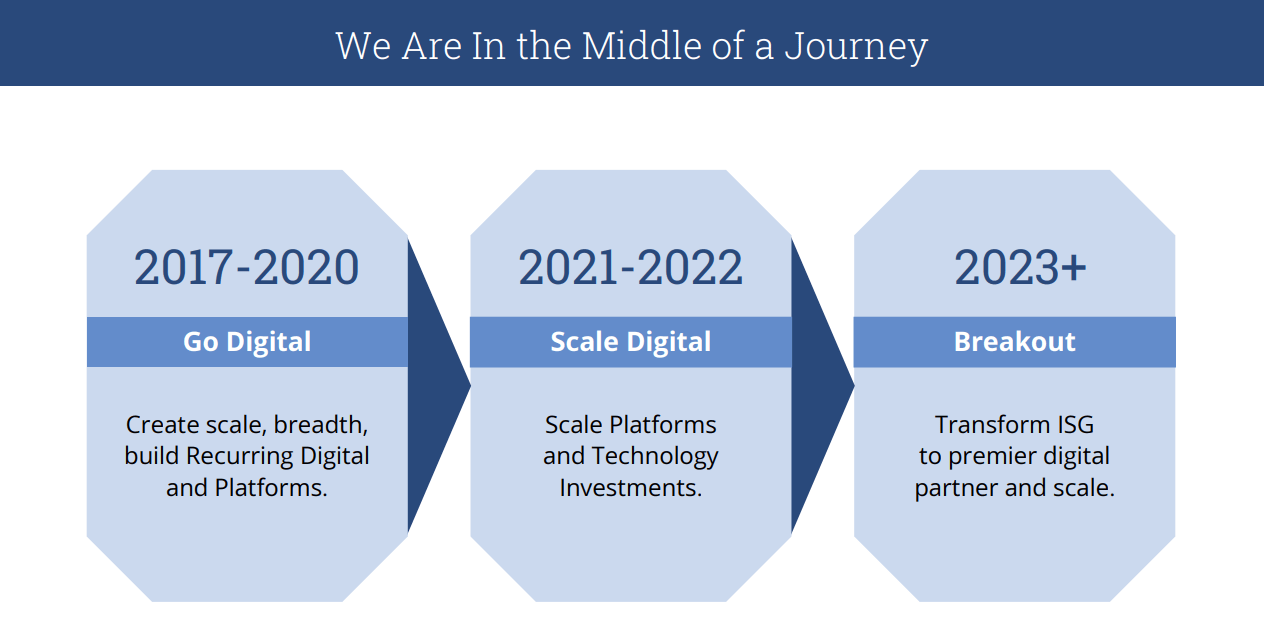

Given the contract-by-contract nature of III’s revenue as well as dependence on businesses to engage in such contracts, ISG’s revenue tends to be a bit lumpy and cyclical. But management has taken some steps to shore up recurring revenue streams, including through a few proprietary software-as-a-service platforms.

III Q3 2022 Presentation

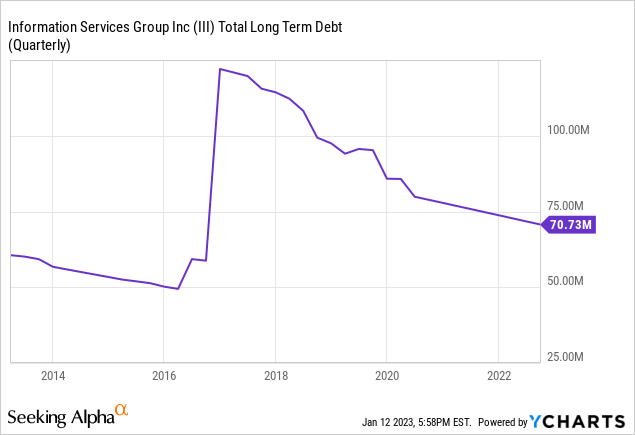

One of the primary mechanisms of growth for ISG since about 2016 has been M&A. And yet, after several bolt-on acquisitions over the last five or so years, ISG’s balance sheet remains in fairly good shape.

ISG more than doubled its total debt load in 2016 in order to make a few key acquisitions, and ever since then it has been successfully and uninterruptedly whittling down its leverage.

Total debt to EBITDA now sits at 1.7x, while net debt to EBITDA is even lower at 1.1x due to ISG’s $0.40 per share in cash & equivalents (7.7% of market cap).

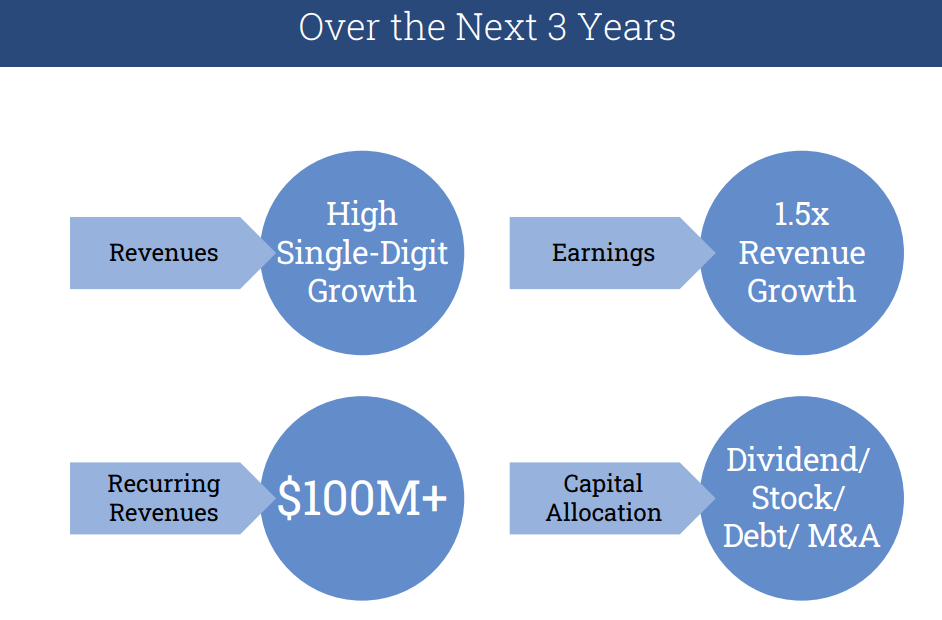

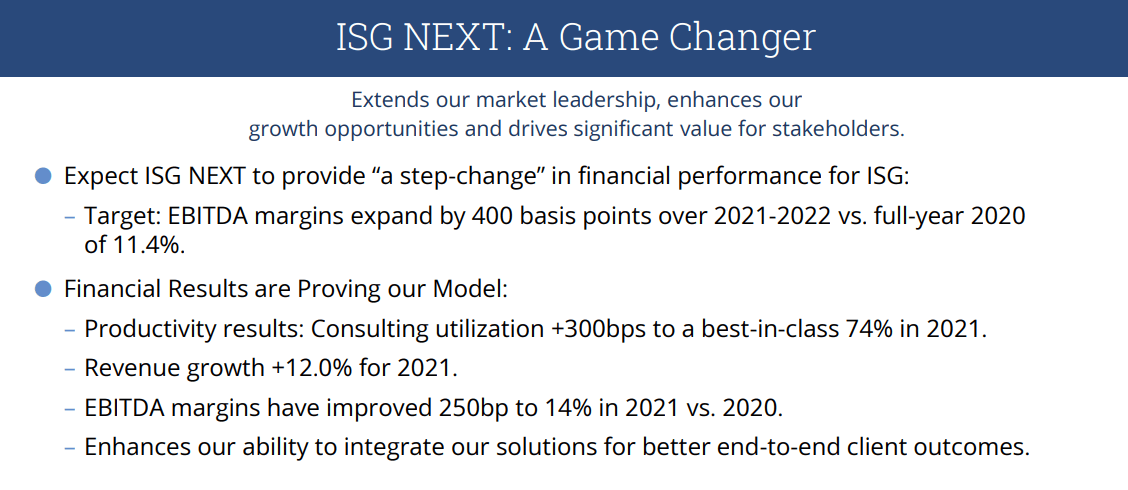

ISG also recently initiated a program it calls “ISG Next,” intended to increase its profitability by not only growing revenues but also expanding EBITDA margins.

III Q3 2022 Presentation

So far, this program seems to be working pretty well.

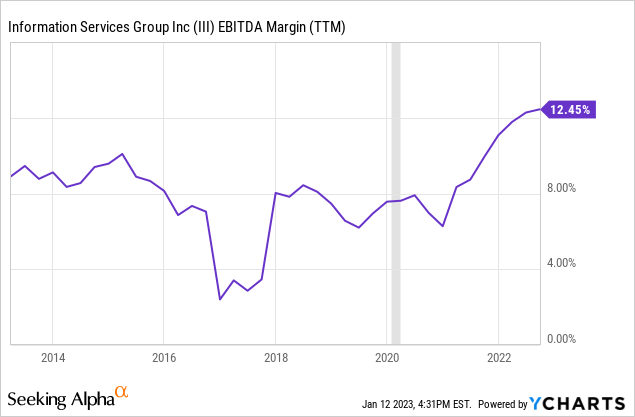

This chart shows GAAP EBITDA, which undershoots non-GAAP EBITDA, but it is at least directionally accurate:

In the most recently reported quarter of Q3 2022, ISG’s adjusted EBITDA margin reached 16%, the highest in company history. Compare that to the 14.5% to 15% margin expected for the fourth quarter. Clearly, ISG has been successful in raising its EBITDA margin.

Given management’s target of high-single-digit revenue growth, expanding margins should translate into solid EBITDA and earnings growth.

III Q3 2022 Presentation

In the first nine months of 2022, adjusted EBITDA of $32 million rose 12% year-over-year, while adjusted EPS of $0.40 surged 18% YoY.

Finally, adjusted EPS in Q3 2022 reached $0.14, which compared to the $0.04 quarterly dividend amounts to a payout ratio of only 29%.

For the full year of 2022, the dividend payout ratio is expected to have been around 30-32%.

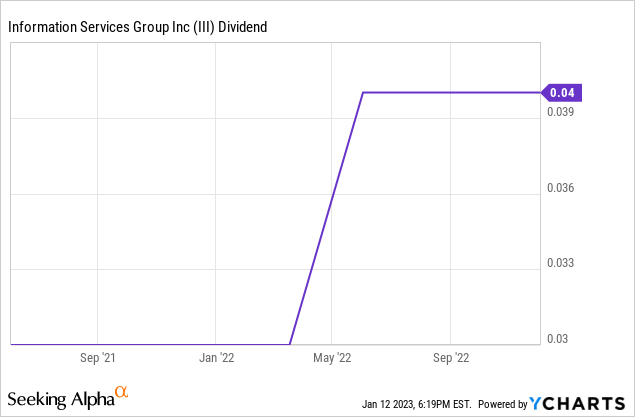

Last year, ISG gave its first dividend raise after initiating a dividend in 2021. The quarterly dividend jumped one penny, which doesn’t sound very impressive except when you consider that going from 3 cents to 4 cents is a 33% increase.

If ISG gave another one-penny dividend increase in 2023, it would mark 25% dividend growth.

That isn’t bad for a company with a 3.1% dividend yield and a sub-33% payout ratio!

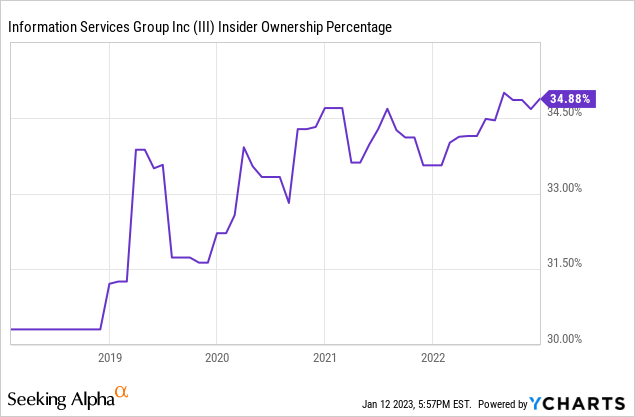

One last thing to point out in ISG’s favor: high insider ownership. This is perhaps to be expected from a microcap company with very little following.

To be fair, it is not clear to me if this chart above is exactly correct, but I know simply by researching Chairman & CEO Michael Connors’ share ownership that the CEO alone owns about 11.5% of ISG. I really like seeing this kind of insider ownership and management alignment with shareholders.

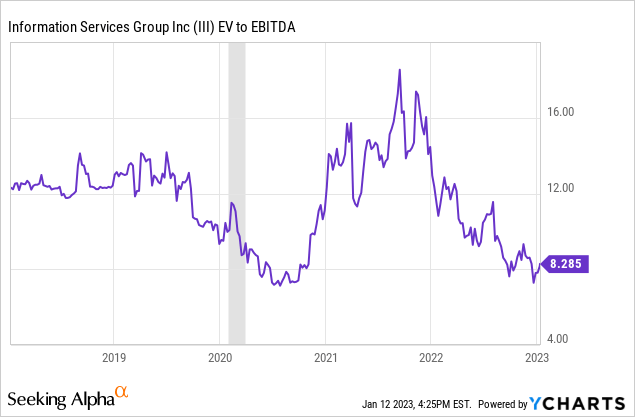

When it comes to valuation, ISG also looks very cheap.

Take a look at enterprise value to EBITDA (again, noting that this is GAAP EBITDA and that adjusted EBITDA is higher, which would make EV to adjusted EBITDA lower):

Likewise, though operating cash flow dried up in the first nine months of 2022 due to the timing of the receipt of income from certain contracts, ISG’s price to 2021 operating cash flow is a low 5.7x.

Bottom Line

I still have much work to do in learning about ISG’s business model and growth prospects, but I like what I see so far. It is still a question mark to me how this company would fare through a recession this year, but at first pass I would guess that ISG has certain cyclical business lines, others somewhat counter-cyclical, and still others somewhat more “steady-eddy.”

For dividend growth investors, ISG appears to be worthy of further research and investigation. In the coming months, especially with the release of ISG’s Q4 2022 earnings report, I intend to do just that.

Be the first to comment