Ibrahim Akcengiz

Inflation is now down significantly from its peak and it is becoming increasingly clear that recent inflation has been a transitory phenomenon induced by a unique confluence of events. Inflationary pressures could remain elevated with the war in Ukraine ongoing, reshoring, China’s economy reopening and increased appetite for fiscal stimulus. Absent another large disruption to supply (war, pandemic) it is likely inflation will return to a more normal level, even if it is still somewhat higher than pre-COVID levels.

A Return to Normal

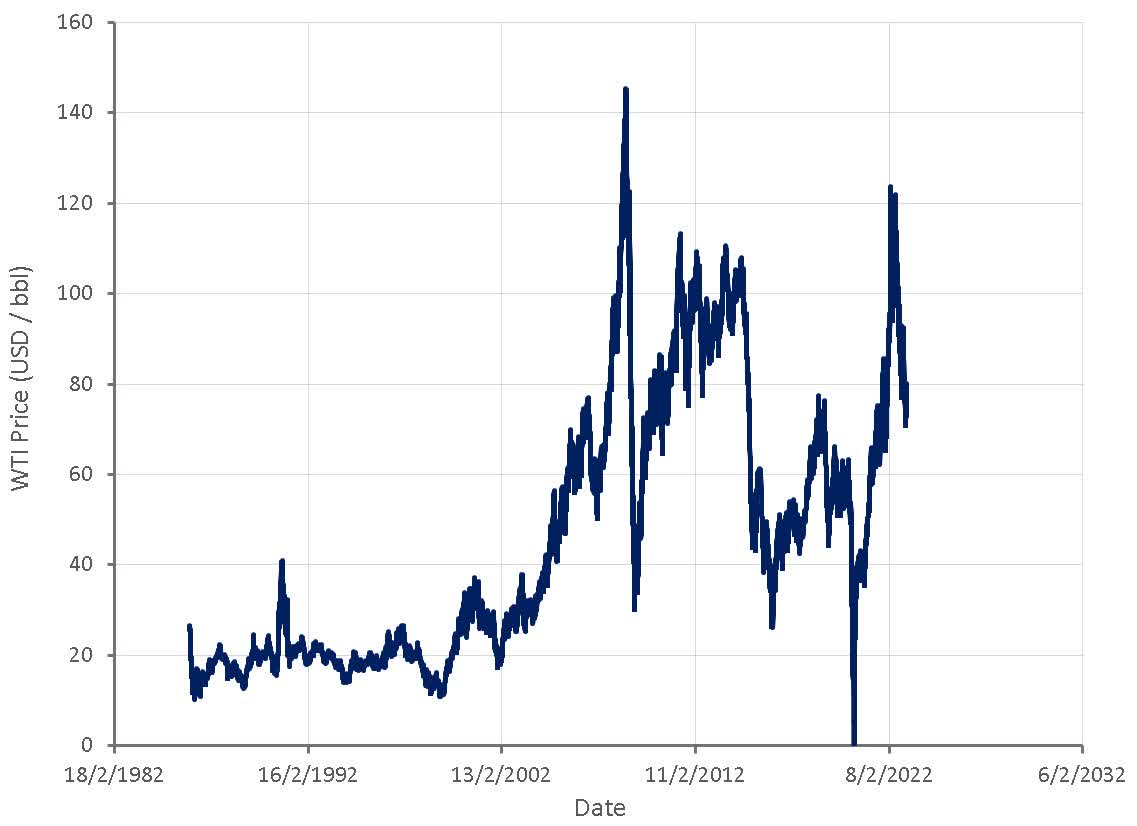

Oil prices have eased significantly since their peak in 2022 and would be much lower if not for the war in Ukraine and support from OPEC. The impact of China’s reopening must be weighed against the potential for moderating economic activity in much of the world. Regardless, energy prices are unlikely to provide the inflationary impulse in 2023 that they did in 2022.

Figure 1: WTI Oil Price (source: Created by author using data from The Federal Reserve)

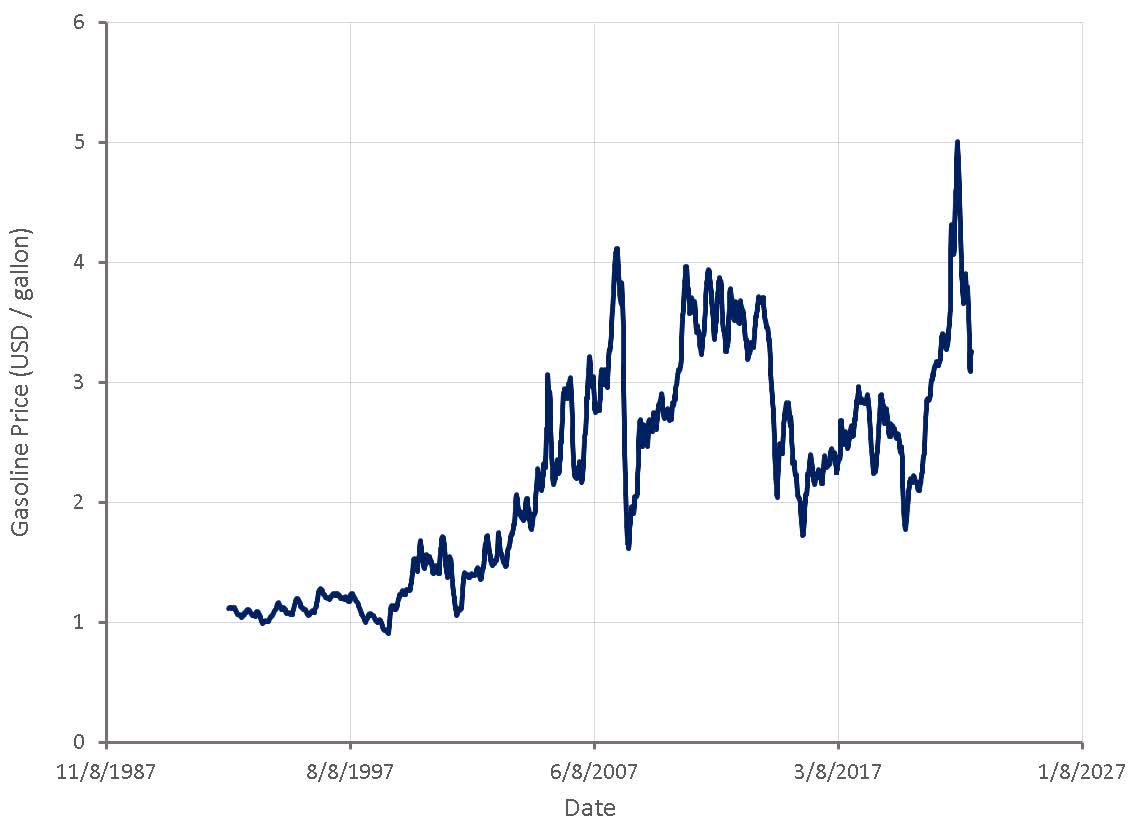

Gasoline prices have also been elevated due to the combination of high oil prices and strained refining capacity. Gasoline prices are down significantly from their peak, and absent further supply issues it is not clear why they would move significantly higher.

Figure 2: Gasoline Price (source: Created by author using data from The Federal Reserve)

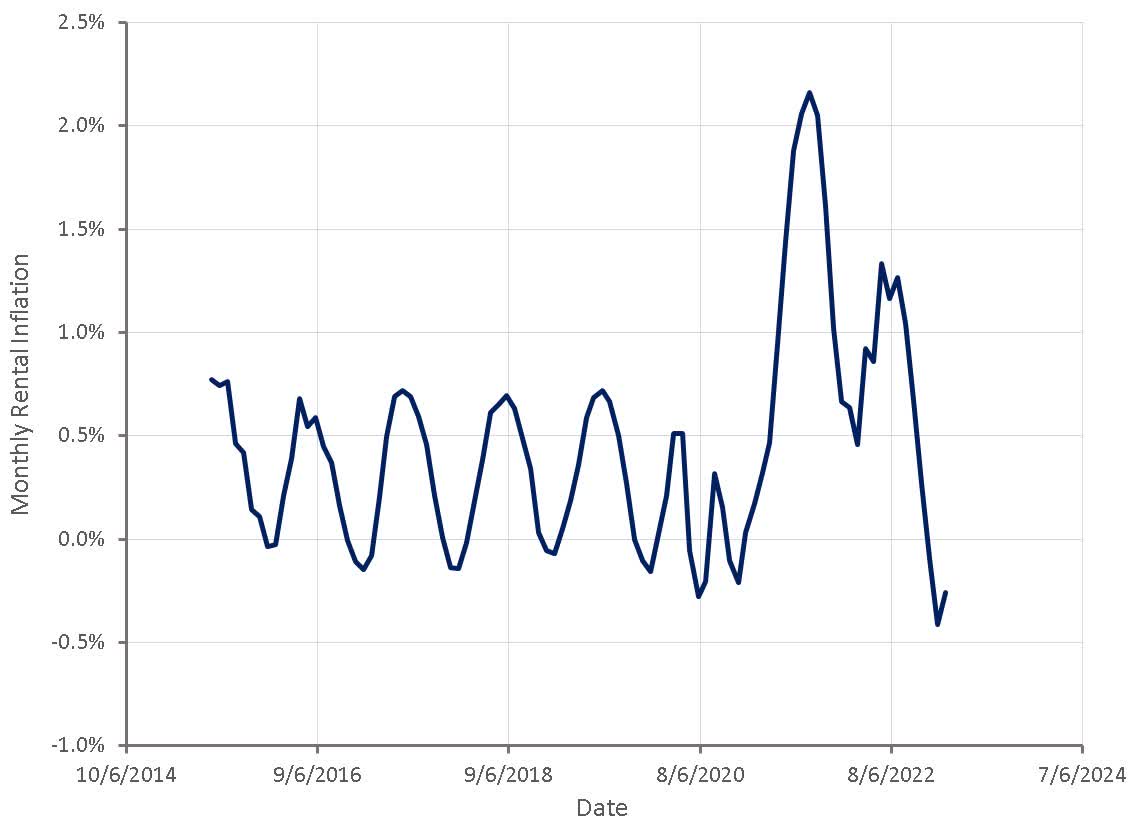

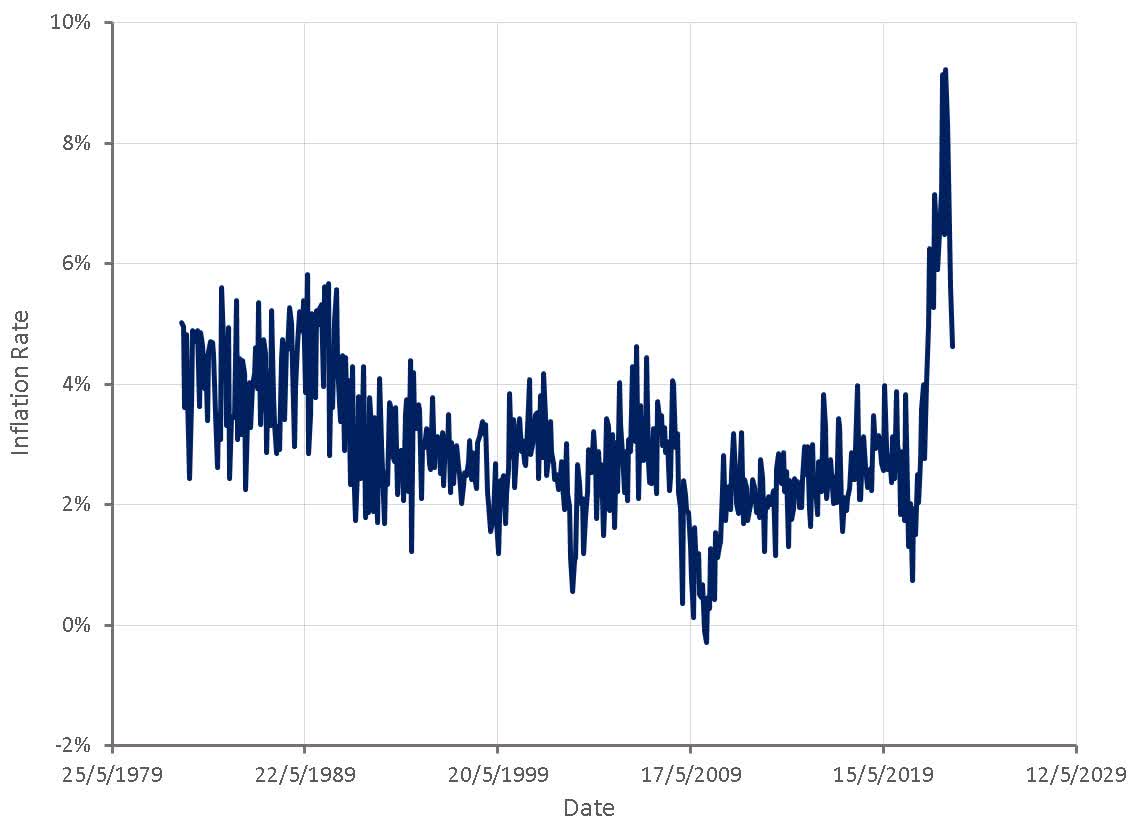

Rents and home prices now appear to be decreasing, rather than moving higher as indicated by CPI data. Absent a complete shift in policy by the Fed it is difficult to see the housing market regaining momentum in the near term. Arguments have been made for a structural shortage of housing, but the housing stock is clearly high relative to the population.

Figure 3: Monthly Rental Inflation (source: Created by author using data from Zillow)

Other items that were key contributors to inflation over the past 2 years also appear to have peaked:

- Fertilizer prices are still over 50% above pre-COVID levels, but are down approximately 30% YoY.

- Used car prices are also still well above pre-COVID levels but down significantly YoY.

- Lumber prices are back to pre-COVID levels.

- Freight rates have also nearly round tripped back to pre-COVID levels.

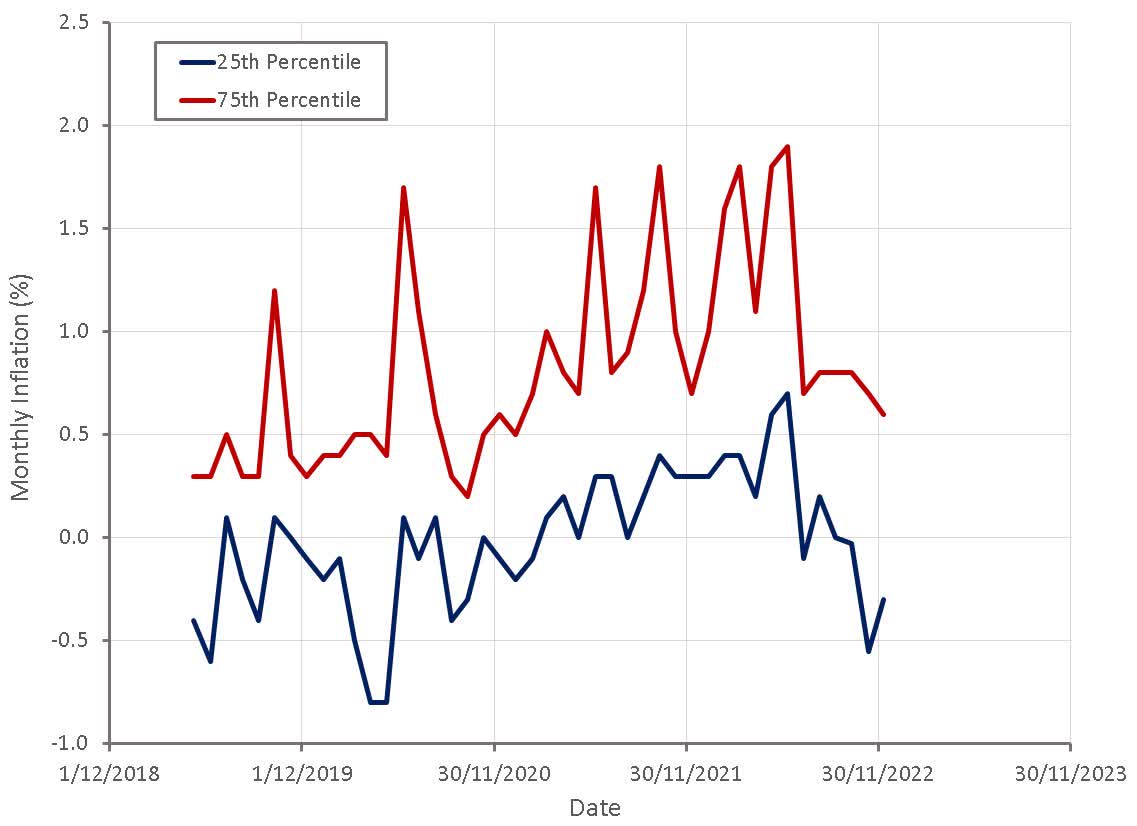

It should be noted that a lot of this post-pandemic normalization is creating price deflation that is temporary. Just as it made little sense to project mid to long term inflation based on COVID induced supply chain issues, it makes little sense to estimate future inflation based on current price declines. The drop in inflation is not being driven by deflation in a handful of items though, it is broad based, indicating a rapid return to a more normal inflation environment. Whether inflation settles at the low levels seen prior to the pandemic remains to be seen though.

Figure 4: CPI Inflation by Percentile (source: Created by author using data from BLS) Figure 5: Median CPI Inflation (source: Created by author using data from The Federal Reserve)

Labor Markets

Much of the reason for believing that this won’t be the case is due to labor market tightness. The reason for doubting a wage-price spiral is twofold, the link between labor markets and inflation is weak and labor markets are not as tight as many think.

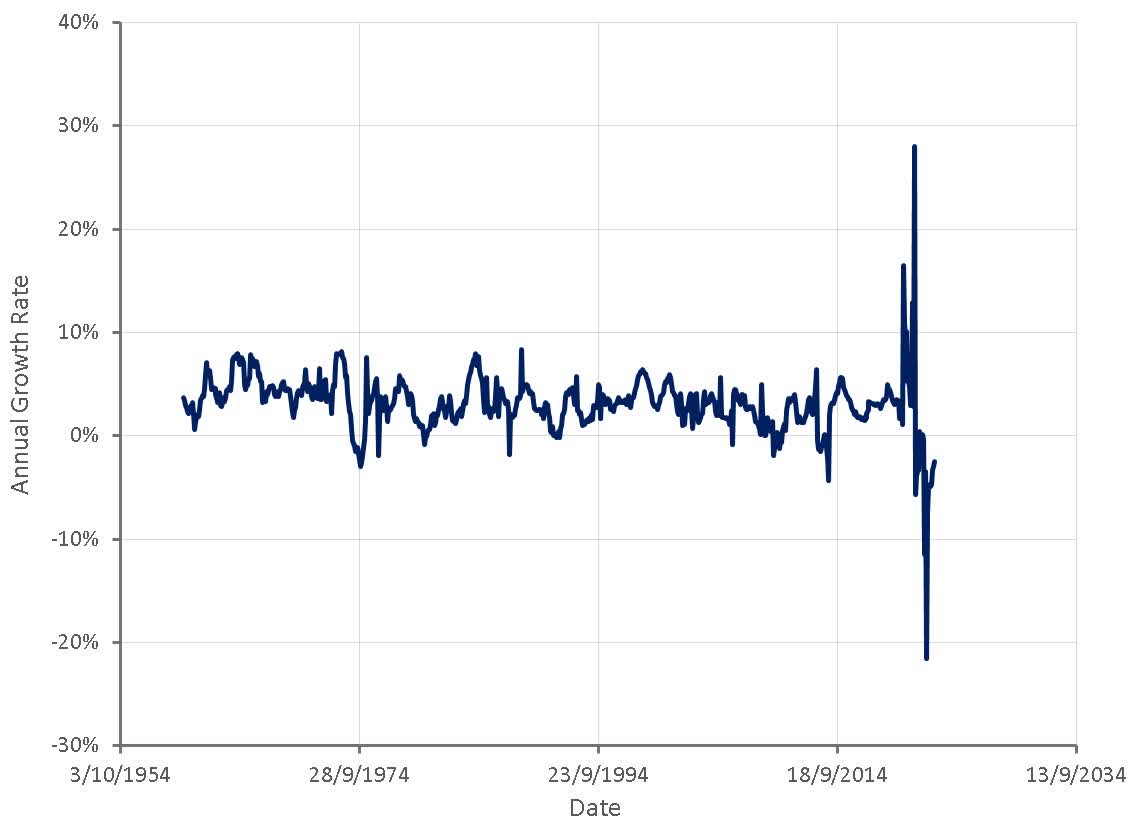

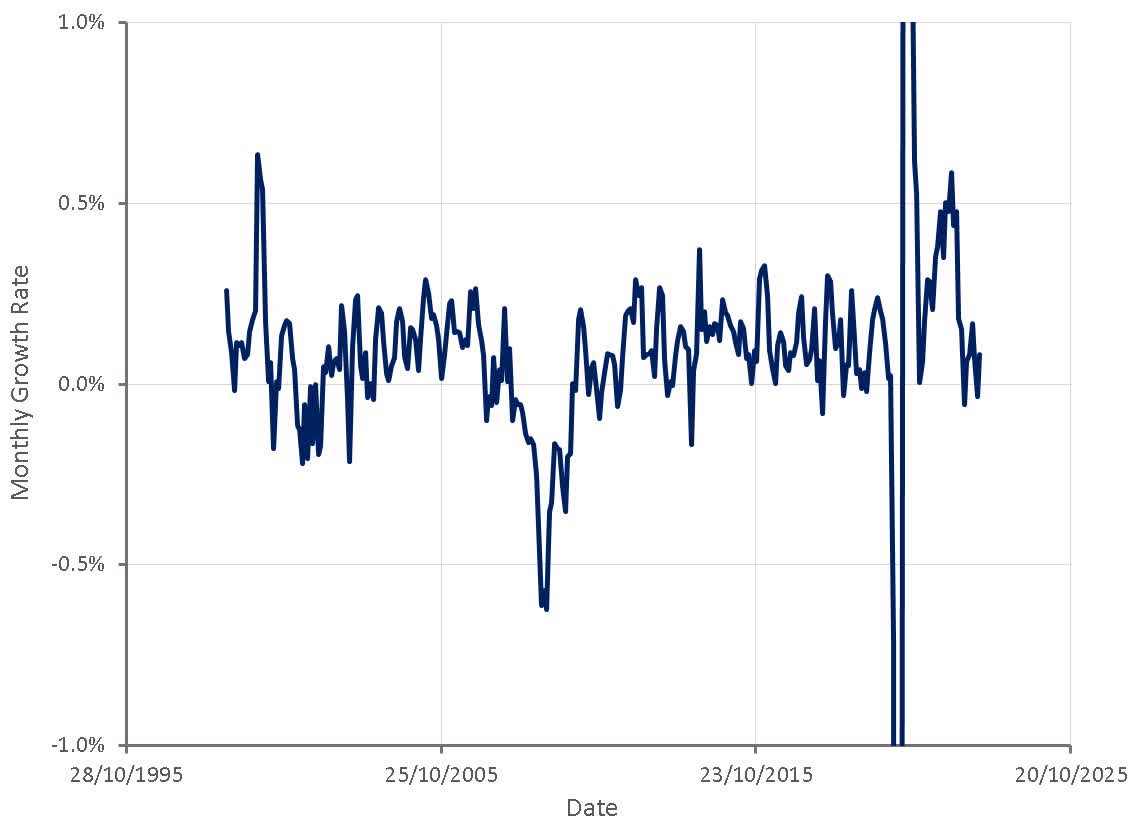

Demand side inflation must be driven by spending power increasing relative to the productive capacity of the economy, and this is clearly not the case at the moment. Real disposable income has been decreasing for the past year and half due to high inflation and modest income growth. Based on this, a decline in spending in real terms creating deflationary pressure is more likely than a wage-price spiral.

Figure 6: Real Disposable Income Growth Rate (source: Created by author using data from The Federal Reserve)

While labor markets have clearly been tight, they are trending back towards pre-pandemic conditions. Quit rates have been elevated and are often associated with strong wage growth due to employee demand for higher wages when switching jobs. Quit rates are still high, but are well down from their peak at the end of 2021.

Figure 7: Quit Rate (source: Created by author using data from The Federal Reserve)

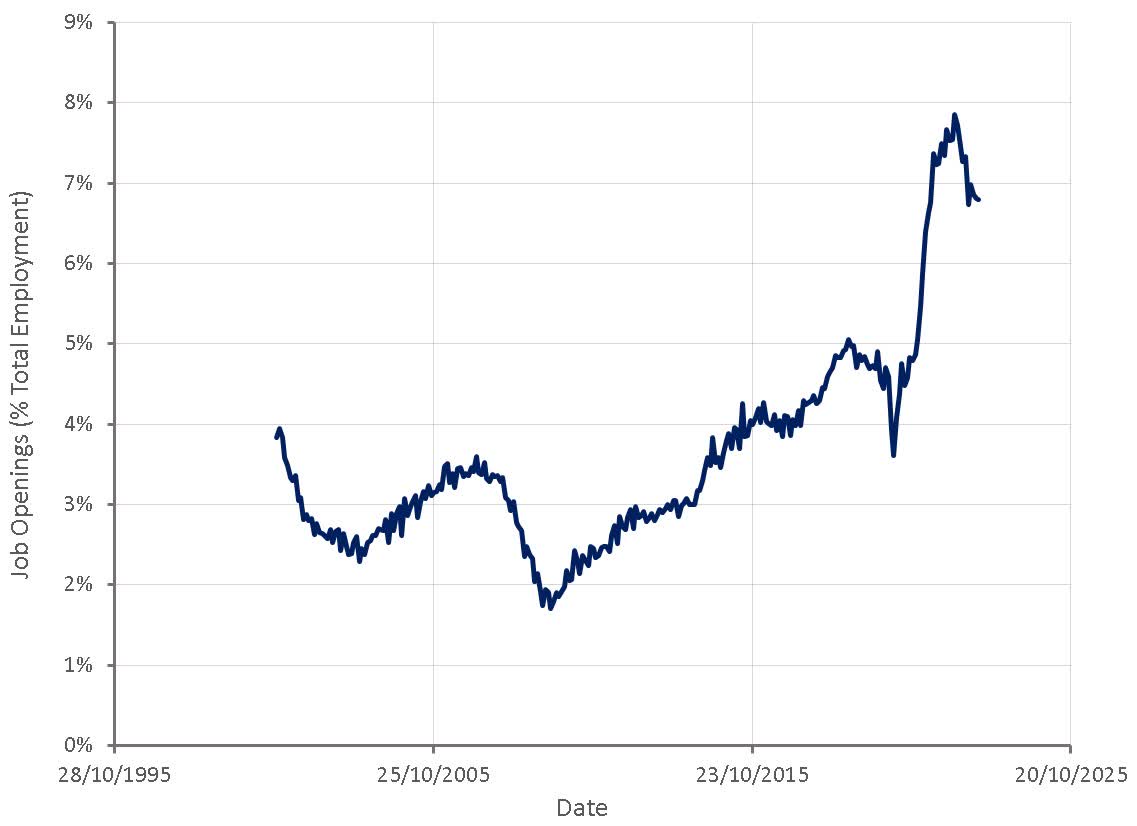

Job openings are also high, although well down from their peak in early 2022. Job openings have clearly been inflated by the low cost of posting and likely do not reflect the number of real employment opportunities. The number of job openings is still likely directionally indicative of labor market conditions.

Figure 8: Job Openings (source: Created by author using data from The Federal Reserve)

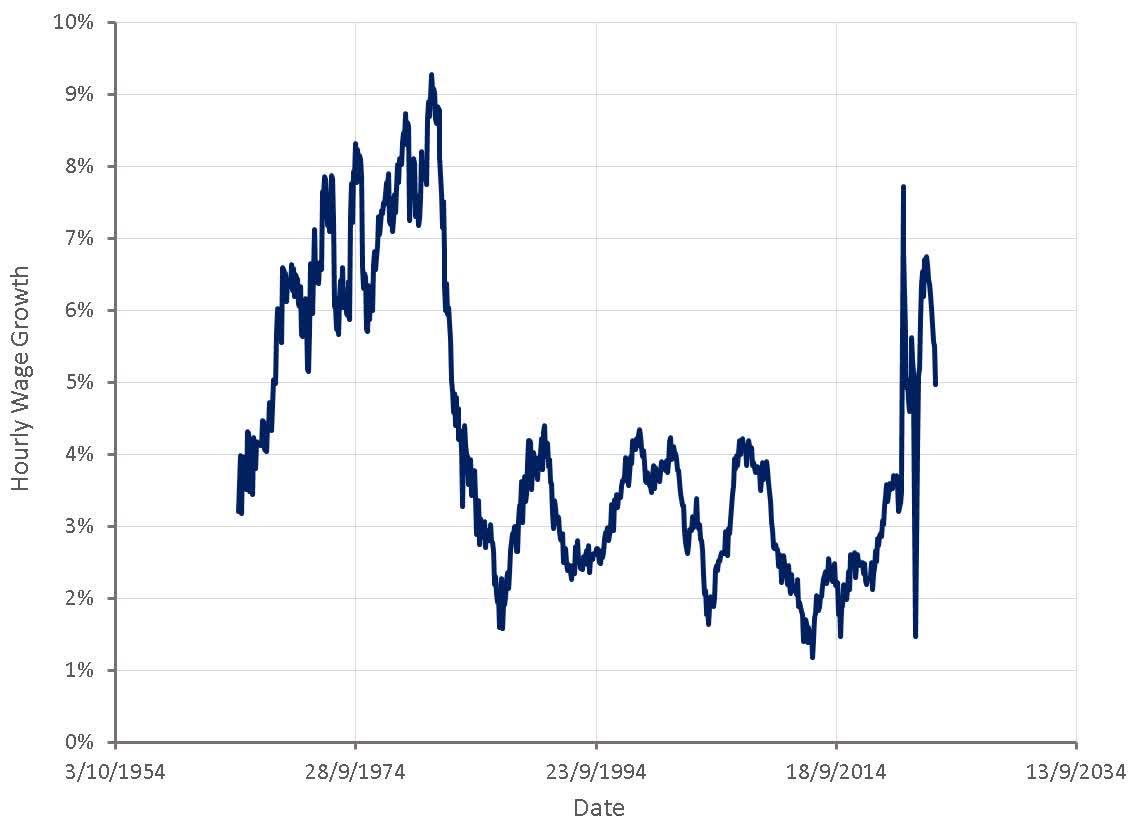

There has been a lot of focus on robust average hourly wage growth leading to demand side inflationary pressure, but this cannot be considered in isolation. Employment levels and hours worked must also be considered to gain a better picture of the labor market and spending power.

Figure 9: Hourly Wage Growth (source: Created by author using data from The Federal Reserve)

While there is some uncertainty in total employment levels due to discrepancies between the household survey and non-farm payrolls, employment growth has clearly normalized after a boom in 2021 and the early part of 2022.

Figure 10: Employment Growth Based on Household Survey (source: Created by author using data from The Federal Reserve)

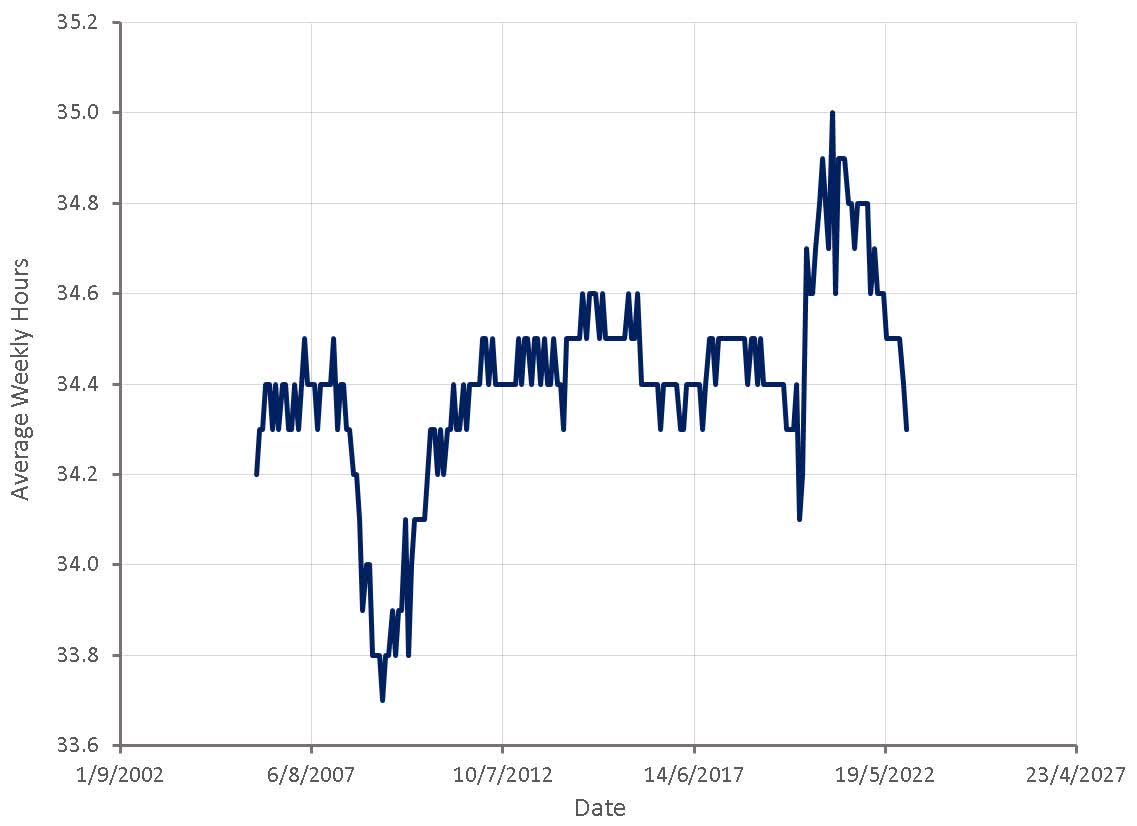

Average weekly hours worked peaked in 2021 and have been trending down since, with increased employment balancing declining average hours. Average hours are now approaching a level typically associated with economic problems though, and this could start to translate to decreased employment levels.

Figure 11: Average Weekly Hours (source: Created by author using data from The Federal Reserve)

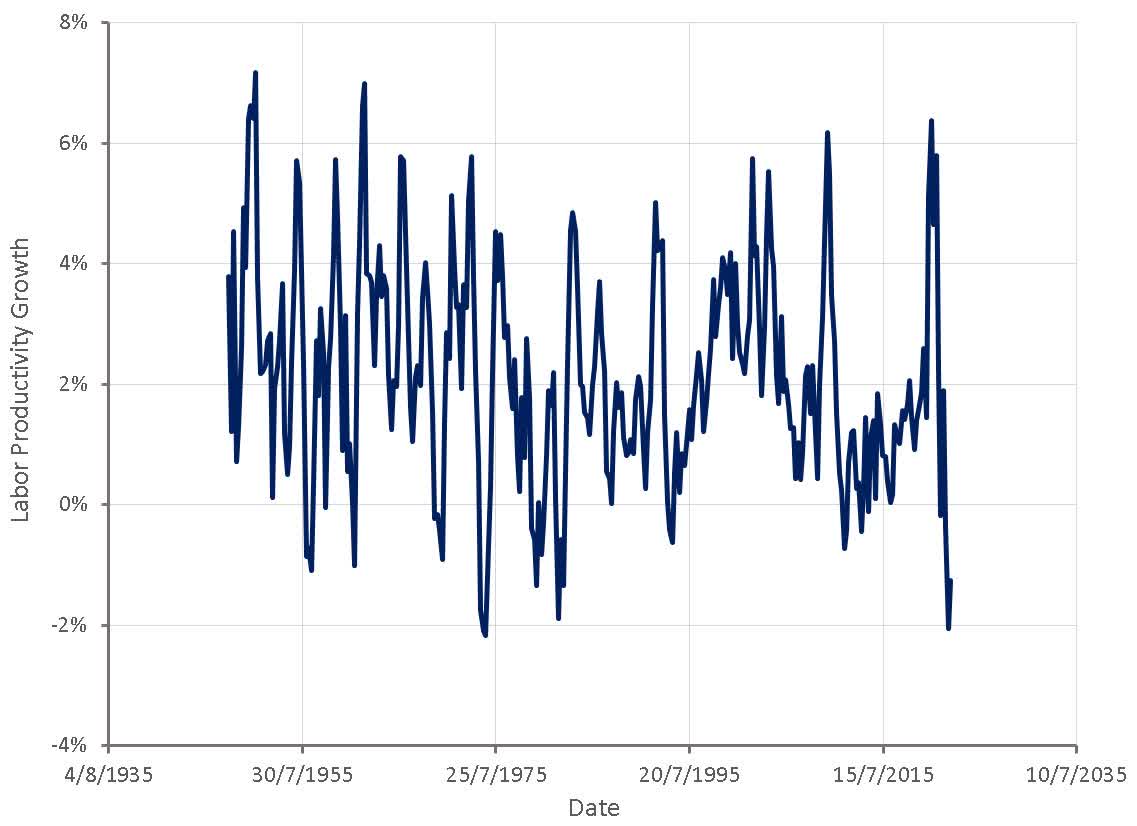

Labor productivity continues to decline, which could indicate that employment remains too high for the current level of economic output. If this is the case, demand for labor is likely to continue declining, but this will increasingly come from a reduction in employees rather than a reduction in hours.

Figure 12: Labor Productivity Growth (source: Created by author using data from The Federal Reserve)

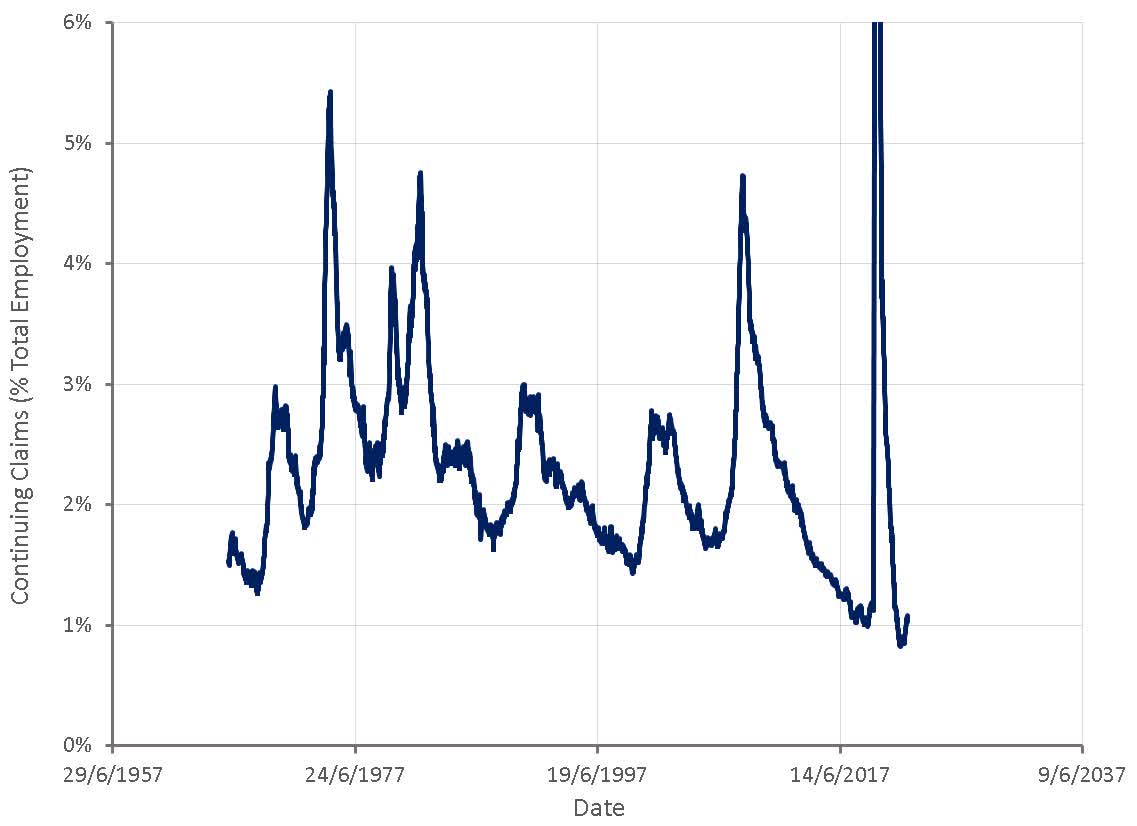

Unemployment levels remain near historically low levels, but this is likely to be the last domino to fall, and I believe shouldn’t be used as evidence of a potential wage-price spiral.

Figure 13: Continued Claims – Insured Unemployment (source: Created by author using data from The Federal Reserve)

Conclusion

The majority of the evidence points towards a rapid fall in inflation in the first half of 2023 and this has little to do with monetary policy. The pandemic and the war in Ukraine created unique conditions, the impact of which was never likely to be ongoing.

Despite the ongoing fall in inflation, the Fed is likely to wait until cracks begin to show in the labor markets before changing monetary policy. There continues to be fear of a return of inflation due to a wage-price spiral, even though there is no evidence of this.

An elevated level of fiscal stimulus could contribute to higher levels of inflation in the future, but this is unlikely in the next few years given the current balance of power. Reshoring is another proposed driver of inflation going forward, although the commitment of organizations to this strategy won’t really be known until profit margins are being pressured and cost control becomes the primary concern rather than supply chain resiliency.

Be the first to comment