Anna Moneymaker/Getty Images News

When a company announces big financial targets and the stock doesn’t hold a rally, investors need to question the big announcement. In the case of Tritium DCFC Limited (NASDAQ:DCFC), the company didn’t provide any path to financial improvements from a big new order. My investment thesis remains Neutral on the EV charging station company due to issues in the deal terms of a record backlog while the stock trades at only $1.50.

Source: FinViz

Big Order

While Tritium announced a record order from repeat customer BP (BP), the company announced a target for meager gross margins in 2023. The EV charging station manufacturer remains mixed up in the business structure requiring the buildout of a large charging network while being the company eating those costs to help build the EV market.

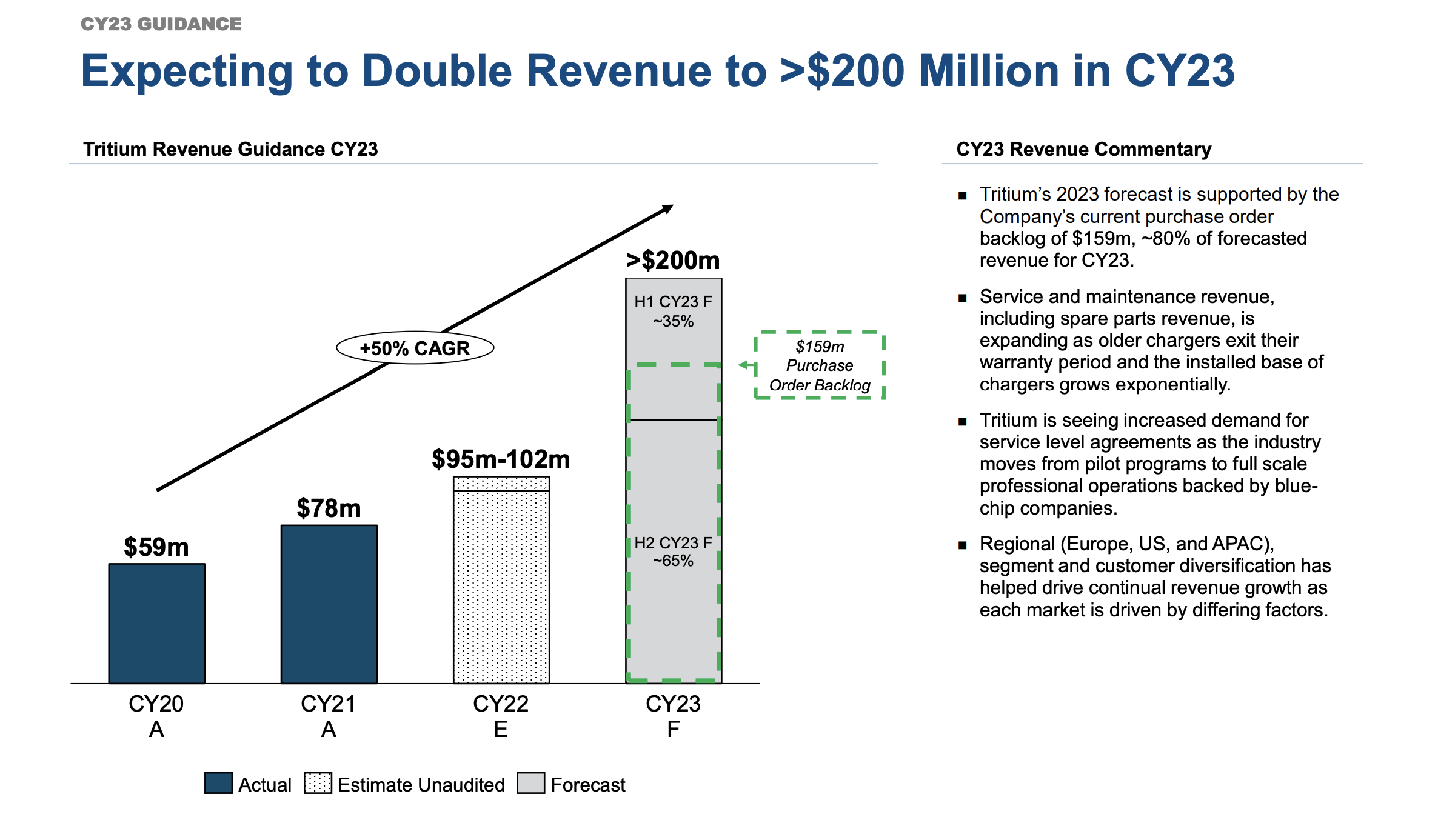

Tritium didn’t actually provide financial details of the BP order other than to suggest the 2022 bookings were a record of $195 million, up 38% from $141 million last year. The company ended 2022 with a backlog of $159 million, up just fractionally from the $149 million backlog total at the end of FY22 in June.

The problem facing the sector is that the fast charging specialist only forecasts 2023 gross margins with an average of 10% to 12%. Tritium is hardly charging BP above costs for a record order which does virtually nothing for the business and shareholders.

BP is ordering a mix of Tritium’s 50kW RTM and 150kW PKM chargers for use in fleets and general public settings in the U.S., Europe and Australia. The message of Tritium CEO Jane Hunter highlights the problem:

As a result of bp’s order, Tritium’s industry-leading fast EV chargers will make it easier than ever before for commercial and everyday drivers to join the e-mobility transition.

Tritium appears too eager to help the market adopt EVs than build a profitable business model. The issue is troubling considering the company ended December with $70 million after apparently raising additional cash recently.

Margin Problem

The problem with the gross margin story is that Tritium forecasts generating ~65% of CY23 revenue of $200 million in the 2H of the year. Even with an improved pricing and planned product suite, the company isn’t going to produce much more than 15% gross margins in the 2H of year to equate to an average yearly gross margins of 10%.

Source: Tritium January ’23 presentation

The revenue story focus is a big part of the problem for investors. Any company in the EV charging space can sell charging stations at cost and show huge revenue growth.

The question remains whether Tritium can sell these charging stations far above costs in order to cover expenses when the company is running out of cash. Tritium makes the numbers difficult to compare with a FY ending in June and all of the financial information provided on January 17 based on calendar years.

The guidance for operating expense growth of 16% at the midpoint has expenses reaching up to $95 million for CY23. At a 10% gross margin, Tritium is only generating $20 million worth of gross profits this year leaving a massive operating loss of $75 million.

Remember, this is just the operating loss. The company still needs to cover interest expenses and capital expenditures with the finance costs alone listed at $18 million back in FY22.

Investors are left with a massive hole without the cash to cover despite huge growth prospects. In addition, the company isn’t providing quarterly financial data making it difficult for investors to track the financial progress.

No doubt, Tritium can make a lot of progress towards covering the operating loss hole via stronger revenue and a boost in the gross margin rate. The major hiccup that hits competitive sectors is that competitors are also trying to build market share and sometimes willing to undercut prices.

A case where Tritium doubles CY24 revenues to $400 million and only boosts gross margins to 20% (doubling 10% margin in CY23), the company is still producing a gross profit below the operating expense levels. Most companies have a very difficult time doubling revenues in a competitive market without increasing costs, though a good business can usually drive more efficiency on the production costs.

Tritium raised $20 million from a working capital facility during December and has access to another $10 million from the senior debt facility. The senior debt facility was expanded from $150 million to $160 million.

The company will need to further expand access to debt in order to keep the cash position up at $70 million. With the stock at $1.50 access to equity sales under the B. Riley committed equity facility isn’t appealing, but Tritium may end up with no other path as debt becomes increasing impossible with large ongoing operating losses.

Takeaway

The key investor takeaway is that Tritium isn’t appealing until the charging station companies quit bearing the financial brunt of building out large EV charging networks. The stock is likely stuck around the current price due to the promises of EV growth and the ongoing cash burn harming shareholders via either equity dilution or additional debt.

Be the first to comment