bymuratdeniz

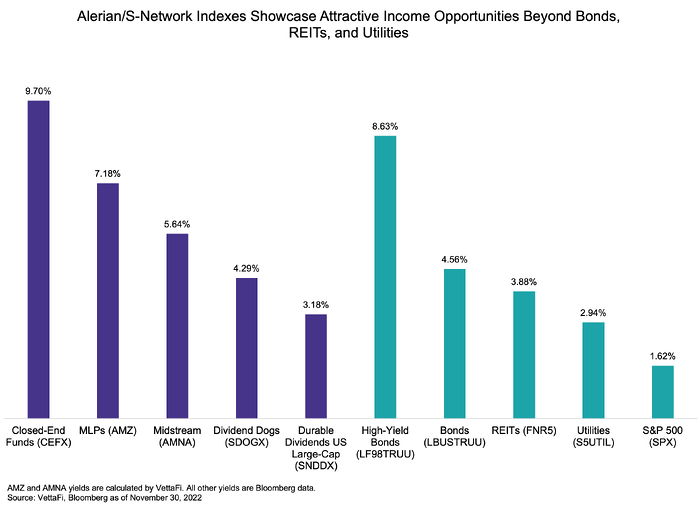

Even with the nice rebound in equities in November, it has largely been a frustrating year for investors, with a weak start to December providing little respite. Dogged by high inflation and rising interest rates, stocks have been pressured, with the S&P 500 down over 14.5% on a price-return basis through the end of November. As a result of the faltering market conditions and rising interest rates, yields for income investments have generally increased. Corporate bond benchmarks are now yielding more than REITs and Utilities.

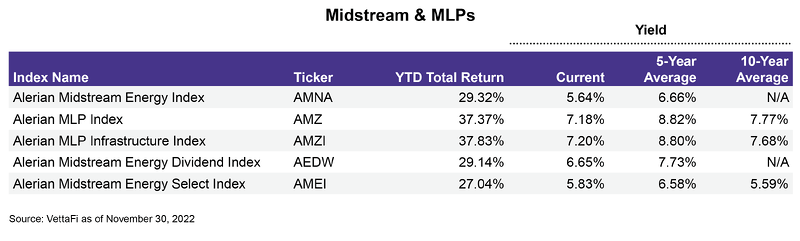

Unlike many other income investments, Midstream/MLPs have lower yields today than at the start of the year due to strong performance. Even with price gains of 27.6% for the Alerian MLP Index (AMZ) and 22.5% for the broader Alerian Midstream Energy Index (AMNA) through November, midstream and MLP indexes are still offering yields comfortably above corporate bonds, REITs, and Utilities as shown below. Not only do midstream and MLP yields remain generous, but payouts have seen a strong bias to growth, with several names raising their payouts by more than 10% over the last year.

Dividend growth gives confidence to the generous yields from midstream/MLPs.

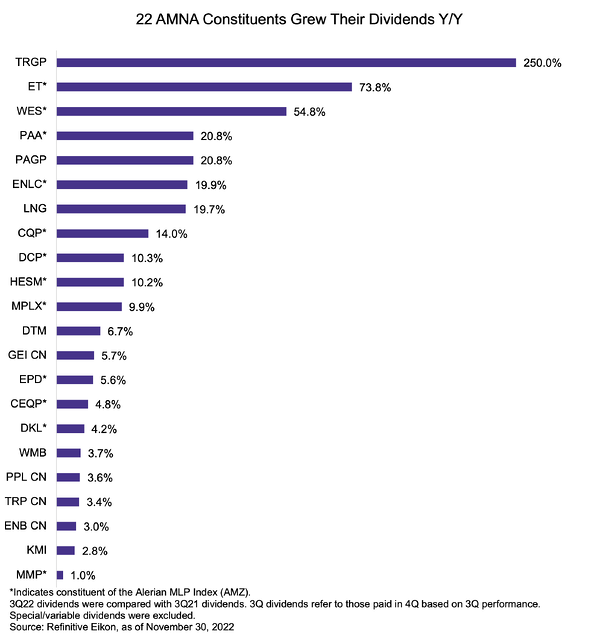

With a weak start to December, the AMZ Index and AMNA Index were yielding 7.5% and 5.9%, respectively, as of December 6. Investors wanting greater confidence in these income streams may benefit from a more granular look at the companies paying these dividends and how payouts have increased over the last year. Midstream corporations and MLPs are largely generating free cash flow and returning excess cash flow to investors through dividend increases and equity repurchases. Over the past year, 22 of the 30 dividend-paying constituents in the broad AMNA Index have increased their dividends. This cohort represents over 88% of the index by weighting as of November 30. Notably, there have been no dividend cuts among Alerian energy infrastructure index constituents since July 2021.

The chart below shows year-over-year growth for AMNA constituents’ dividends, comparing the 3Q22 dividend (recently announced and paid in 4Q22) with the 3Q21 dividend. Ten constituents increased their dividend by 10% or more, and the median increase for the 22 companies was 8.3%. Admittedly, some of this hefty growth follows painful dividend cuts in the past (i.e., growth is off a lowered base). Seven of the top ten dividend growers below slashed their payouts during the onset of the pandemic in 2020, with none of the seven having increased their dividend to pre-pandemic levels. That said, Energy Transfer (ET) is closing in on its target of restoring its distribution to the pre-cut level of $0.305 per unit per quarter, with the latest payout just 15% below that target. Of the top ten growers below, Cheniere (LNG), Cheniere Energy Partners (CQP), and Hess Midstream (HESM) have never cut their dividends, nor has MPLX (MPLX), the next largest grower. Others that have never cut, such as Enterprise Products Partners (EPD) and Magellan Midstream Partners (MMP), are providing more moderate growth.

Bottom Line:

Midstream/MLPs offer generous yields backed by positive dividend trends, as many companies have used free cash flow to increase payouts to investors.

AMZ is the underlying index for the JPMorgan Alerian MLP Index ETN (AMJ) and the ETRACS Quarterly Pay 1.5x Leveraged Alerian MLP Index ETN (MLPR). AMNA is the underlying index for the ETRACS Alerian Midstream Energy Index ETN (AMNA).

Current Yields vs. History

With strong performance year-to-date, midstream and MLP yields are generally below their historical averages.

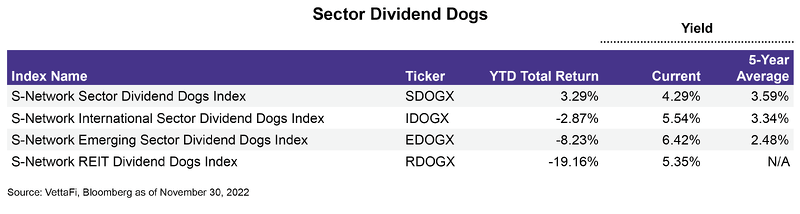

Yields for the Dividend Dogs index suite are above their five-year averages. SDOGX has seen the best performance this year with its equal-weighted strategy benefitting from an energy overweight relative to the S&P 500, which is the starting universe for the index.

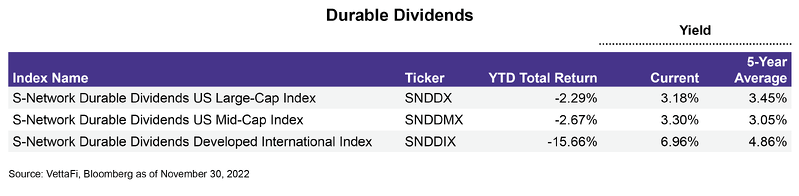

Multiple screens for dividend durability, including evaluating cash flows, EBITDA, and debt-to-equity ratios, help ensure reliable income from the durable dividend indexes.

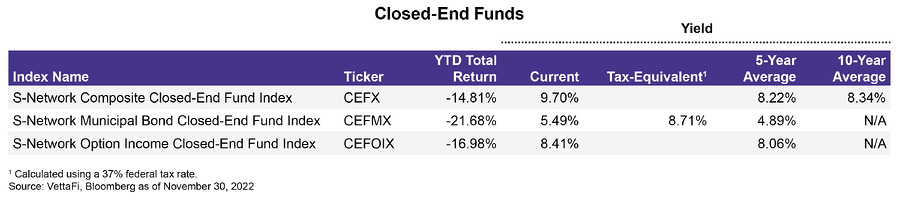

Closed-end funds have been pressured by the rising interest rate environment, and current yields for the three CEF indexes are above their historical averages.

Disclosure: © Alerian 2022. All rights reserved. This material is reproduced with the prior consent of Alerian. It is provided as general information only and should not be taken as investment advice. Employees of Alerian are prohibited from owning individual MLPs. For more information on Alerian and to see our full disclaimer, visit Disclaimers | Alerian.

Editor’s Note: The summary bullets for this article were chosen by Seeking Alpha editors.

Be the first to comment