Devrimb

Welcome to 2023, where most people – both economic professionals and ordinary folk – believe we’re going to experience a recession.

Why?

I’m sure I don’t need to tell you, even if you do happen to fall into the “I don’t think we’re in for an official downturn” group. Which, for those of you who consider such creatures absolute myths, here’s one example of a dissenting opinion.

It’s from CNN and was published on Monday, January 2:

“Last year was dominated by scary headlines about crushing inflation, super-sized interest rate hikes and mounting recession fears.

“It was a brutal period for the stock market, with roughly one-fifth of the value of the S&P 500 vanishing and the Nasdaq dropping by more than one-third. All three major U.S. markets suffered their worst years – by far – since 2008.

“And yet now that 2022 is over, there are clear bright spots in this economy that offer hope 2023 will not be the year the next recession begins.”

It then goes on to list:

- Historic jobs recovery.

- Inflation is cooling.

- Gas prices have plunged.

- Real wages are heating up.

- The Fed won’t hike to the moon.

Incidentally, the title is, “Recession or Soft Landing? Five Reasons to Be Cautiously Optimistic About 2023.” So hardly the most bullish stance, I know. But it’s still not bearish.

Moreover, it does make some valid points (and some questionable ones). It’s just that most of us see other points as overriding them all.

Easily.

“The Fed Won’t Hike to the Moon,” Only Out of Earth’s Atmosphere.

Here’s another recent headline, this time from The Hill:

“Two-Thirds of Economists Surveyed Predict Recession This Year.”

Like the CNN piece, it mentions the Federal Reserve – how can it not? – but by acknowledging how the bank is still set on raising “interest rates to try to get inflation under control.” This is one of my issues with the previously mentioned article.

Just because the Fed won’t be taking anything “to the moon” doesn’t mean the cost of borrowing for business deals and housing alike will get worse from here. Plus:

“The [Wall Street] Journal reported that almost 40 percent of U.S. banks were tightening their lending standards in the fourth quarter of 2022.

“That can be a sign that banks are expecting a recession, as banks generally tightened their lending standards ahead of recessions in 2008 and 2020, according to the Federal Reserve Bank of St. Louis.”

And:

“A majority of the economists in the Journal’s survey said they believe the higher interest rates will increase the unemployment level from 3.7 percent recorded in November to more than 5 percent, which would still be historically low but represent millions losing their jobs.”

And:

“Respondents said the effects of the interest rate increases will be more noticeable this year than last year.”

Now, admittedly, the majority also expect a mild recession. So there’s that. But they expect a recession nonetheless.

That’s what their data is pointing to, and I happen to agree with their conclusion.

I’m Still Rooting for a Recession Regardless

I got in trouble this past June for publishing “I’m Rooting for a Recession.” It garnered comments that ranged from mild chastisement to comparing me to Russian President Vladimir Putin.

Suffice it to say, the analogy wasn’t a flattering one.

I think there were actually two mentions of me and Putin in there, one of which got nine likes. With all due respect to the commenters and their supporters though, I’m not sure if they actually read the article.

Not even the summary bullet points, which read:

- I do look forward to weakness in the stock market because I love buying blue-chip equities when they’re trading in the bargain barrel.

- Therefore, I do a lot of work [that] helps to prepare me for an eventual downturn in the market.

- So, you see, I don’t fear this likely “garden style” recession. And in fact, I’m rooting for it.

Does that sound like I’m plotting harm to people for my own personal gain (as accused)?

I’ll also point out, as I often do, that both my business and net worth crashed and burned in the 2008 recession. I lost almost everything to the point where I floundered on how to provide for my family of six.

Yet that experience forced me to reassess my financial behavior. It prompted me to create the smart, sustainable empire I have today.

That’s how I know the benefit of bad times. They open opportunities we otherwise wouldn’t have or wouldn’t act on.

Like buying certain stellar stocks at very attractive prices.

The REITs I’m Gobbling Up

Prologis, Inc. (PLD)

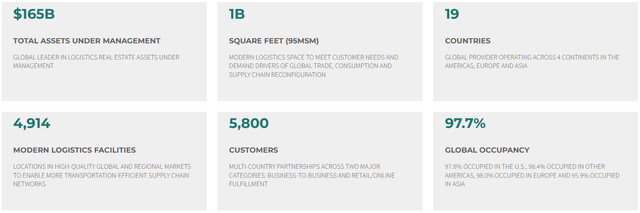

Prologis is an industrial REIT (real estate investment trust) that specializes in logistical properties. In terms of its size, it is a behemoth not only in the industrial space, but it has the largest market cap of all REITs. Prologis has an international footprint with properties located in 19 countries.

In all Prologis has almost 5,000 buildings covering approximately 1.0 billion square feet and serves 5,800 customers, mainly in business-to-business categories and online fulfillment. PLD puts an emphasis on high growth markets and markets that have high barriers to entry. Their properties are in high demand with a global occupancy rate of 97.7%.

Prologis

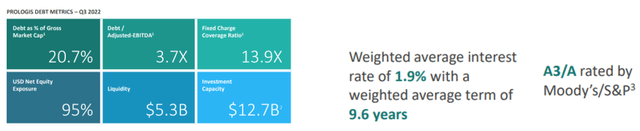

Prologis has one of the strongest balance sheets around with a debt to adjusted EBITDA of 3.7x, a fixed charge coverage ratio of 13.9x, and $5.3 billion in liquidity. Its weighted average interest rate is 1.9% and its weighted average to maturity is 9.6 years. PLD has an A3/A credit rating by Moody’s & S&P respectively.

Prologis Investor Presentation Nov 2022

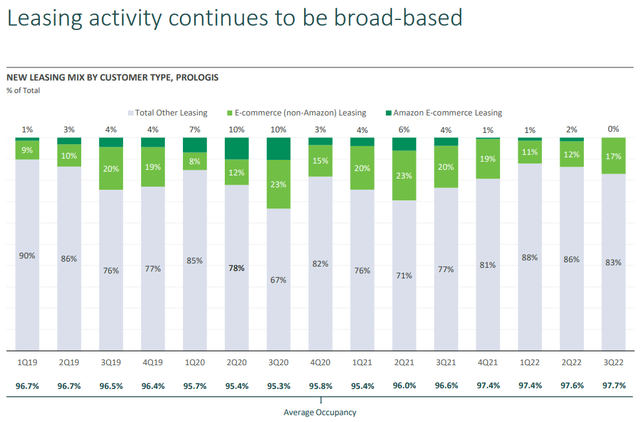

In 2022 Amazon announced that it was reducing its warehouse space, which in turn put a lot of negative price pressure on PLD and other industrial REITs. At first glance this may seem justified since Amazon is the world’s largest e-commerce company, but when reviewing the numbers below, e-commerce only made up 10% of PLD’s new lease signings in 1Q19, with Amazon contributing only 1%.

That climbed to as high as 23% during the pandemic, with Amazon contributing 10%, and is now starting to normalize in 3Q22 to 17%, with Amazon contributing 0% of the new lease signings.

The point is that even with no leases signed by Amazon in 3Q22, PLD’s e-commerce new lease signings in 3Q22 are 7% higher than the 1Q19 levels (as a percentage of new leases signed).

The larger point is that e-commerce is not going away. It will only continue to grow. Amazon over-projected demand and leased more space than it ultimately needed, causing them to hit the breaks in 2022, but this is not an indictment on e-commerce, its more about Amazon misjudging its supply chain needs.

PLD’s e-commerce new lease signings in 3Q22 are only a couple of percentage points lower than its 3Q19 levels and that’s with no new leases signed by Amazon. E-commerce will continue to grow, and when Amazon right-sizes, it will continue to need and sign new leases for logistics space.

Prologis Investor Presentation Nov 2022

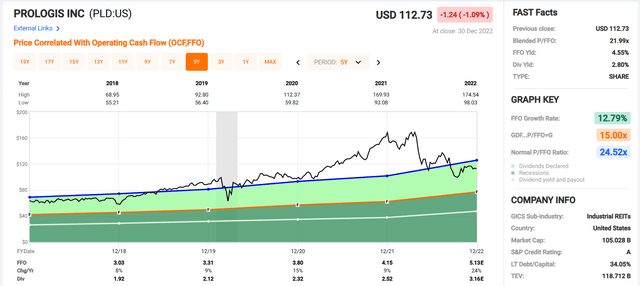

With such a reduction in new leases by the world’s largest e-commerce company one might expect to see a sharp decline in funds from operations, but in 2022 Prologis grew FFO (funds from operations) from $4.15/share to $5.13/share, or a 24% increase.

Sure, some of that FFO growth is from in-place leases, and the reduction in Amazon new lease signings may impact PLD’s earnings to some extent down the road. However, as previously mentioned, PLD’s overall e-commerce new lease signings in 3Q22 are close to their pre-pandemic levels, even without Amazon, and I expect whatever void is created by Amazon’s pullback will be filled by the overall growth in e-commerce demand.

iREIT

Prologis is 1 of the 3 REITs we cover with a quality score of 100. The projected FFO growth in 2023 is expected to be 9% and its 5-year dividend growth stands at 8.80%. Currently PLD has a 2.80% dividend yield which is very well-covered with its 2022 AFFO payout ratio of 72.4%. Additionally, PLD is trading at a blended FFO multiple of 21.99, which is a discount to its historic FFO multiple of 24.52x. At iREIT, we rate Prologis a STRONG BUY.

FAST Graphs

Alexandria Real Estate Equities, Inc. (ARE)

Alexandria is an office REIT that has a distinctive focus on life science and pharmaceutical labs. Some of its largest tenants include giants like Eli Lilly, Sanofi, Bristol-Myers, and Moderna. In addition to life science and pharmaceuticals it also leases space to biotechnology, academic research, and the government.

ARE was founded in 1994 and was the pioneer in the life science / lab space. Joe Marcus founded the company and is still CEO to this day. I had a chance to sit down with Joe earlier this year to discuss ARE’s history and upcoming prospects. iREIT members can find the interview and full transcript at the link below –

The Ground Up Podcast: Alexandria Real Estate Equities, Inc. (ARE) | Seeking Alpha.

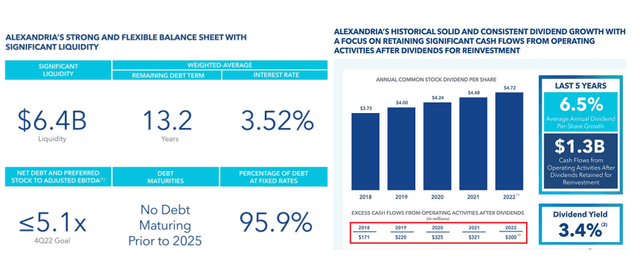

ARE is in excellent financial shape, with a weighted average interest rate of 3.52% and a weighted average debt term of 13.2 years. 95.9% of their debt is fixed rate and no debt maturities occur before 2025. ARE has a BBB+ credit rating and $6.4 billion in liquidity as of 3Q22.

Over the last 5 years, ARE has increased its dividend on average 6.5% annually, and in total was able to retain $1.3 billion for reinvestment. ARE has been able to retain a large portion of its cash flow due to their conservative payout ratios. In 2022, ARE had an AFFO (adjusted funds from operations) payout ratio of 72.17%. This provides the dividend plenty of safety and room to grow and allows them to retain cash to reinvest while being less reliant on external financing. Currently, ARE is paying a dividend yield of 3.32%.

Alexandria – Investor Presentation 3Q22

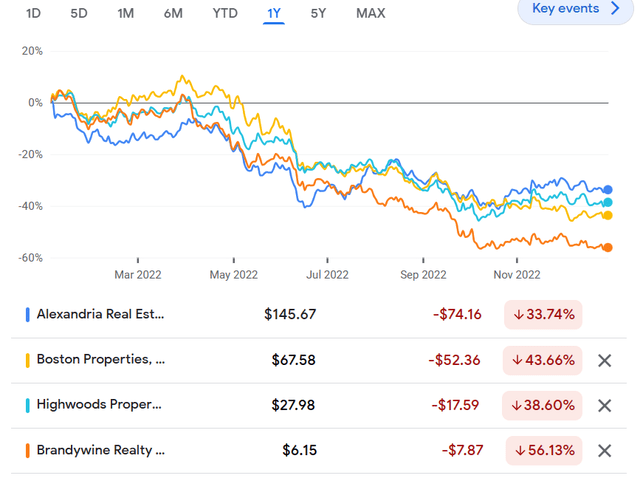

Alexandria sold off in 2022 along with all the other office REITs. On the year, its stock was down 33.74% while the company grew its funds from operations by 8%. Although it finished the year better than most of its office peers, at one point midway through the year ARE was down more than Boston Properties, Highwoods Properties, and Brandywine Realty. Through the first half of 2022, it sold off with the general office sector, which is interesting since the main headwind facing the office sector doesn’t really apply to ARE.

Google Finance

The “work from home” movement has been a major headwind impacting the entire office sector. The concern is that once the current leases expire there won’t be as much demand for office space. While there is a case to be made for this concern, in ARE’s case the issue really doesn’t apply.

The tasks performed in most, if not all, of ARE’s properties cannot be done from home. You can’t perform biotech research from your living room, and you can’t make the newest lifesaving medicine over zoom.

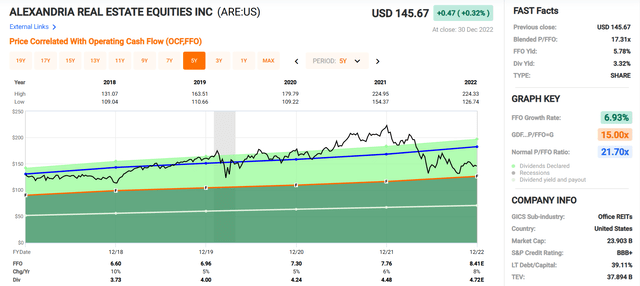

Due to the selloff in 2022, ARE now trades at a blended FFO multiple of 17.31x vs its historic FFO multiple of 21.70. ARE had 8.40% FFO growth in 2022 and is expected to grow FFO at 6.30% in 2023. Like Prologis, ARE is one of only 3 REITs within our coverage to receive a perfect 100 Quality Score. With its growth prospects for both FFO and the dividend, along with its discounted valuation, we at iREIT rate ARE a BUY.

iREIT FAST Graphs

Realty Income Corporation (O)

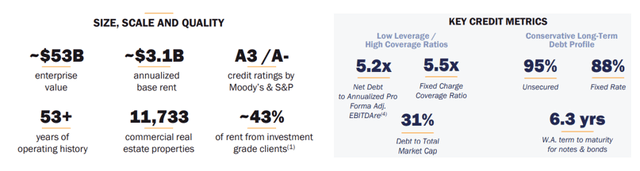

Realty Income is a triple net lease REIT that specializes in single tenant freestanding buildings. Its roots trace back to 1969 with a single Taco Bell before going public in 1994 with 630 properties. As of 3Q22 they have grown to 11,733 properties.

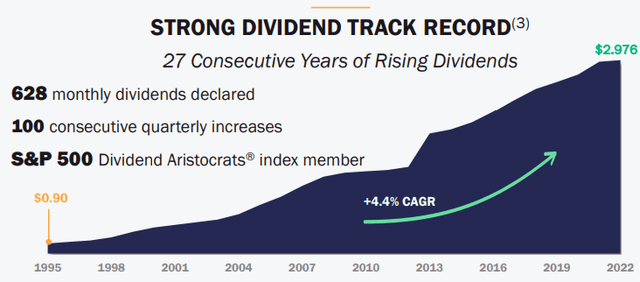

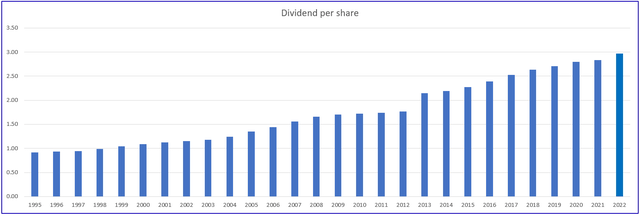

Realty Income pays monthly dividends and has a 27-year streak of rising dividends. In all, Realty Income has declared 628 monthly dividends with 100 consecutive quarterly increases, making them one of the elite companies included as a Dividend Aristocrat member.

The monthly dividend annualized yield is 4.70% and it is well-covered, with a conservative 2022 AFFO payout ratio of 76.15%. In addition to the current yield, Realty Income has a 4.4% compounded annual dividend growth rate since 1995.

Realty Income – Investor Presentation Dec 2022

Realty Income 10-K Reports (information compiled by iREIT)

Realty Income has a strong balance sheet and great debt metrics with a Net Debt to EBITDAre of 5.2x and a Fixed Charge Coverage Ratio of 5.5x. As of 3Q22, 95% of their debt is unsecured and 88% is fixed rate with a weighted average term to maturity of 6.3 years. Additionally, Realty Income has an A- credit rating.

Realty Income – Investor Presentation Dec 2022

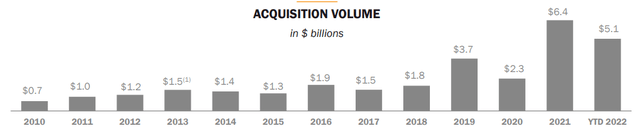

Realty Income has solid on-going growth prospects as well with 5.1 billion in acquisitions as of 3Q22. More recently, on December 30, 2022, Realty Income announced it will buy a property portfolio for $894 million from CIM Real Estate.

Realty Income – Investor Presentation Dec 2022

There has been some discussion recently that the “new normal” in interest rates will increase Realty Income’s cost of capital, compressing their leasing spreads which will make it hard for them to maintain accretive growth.

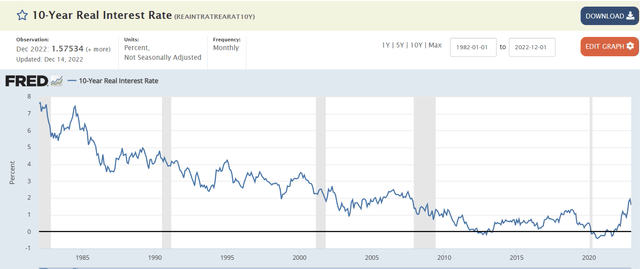

Realty Income has grown both FFO and dividend payments through all types of economic cycles, including periods of high interest rates. To put this in perspective, although we did see a sharp increase in interest rates in 2022, this pales in comparison to high interest rate environments of the past.

The chart below goes back to the early 1980’s. Realty Income was able to grow under much higher interest rate levels. Likewise, they have not only maintained their dividend, but have been able to grow it through both the Great Financial Crisis and the Covid Pandemic.

FRED iREIT

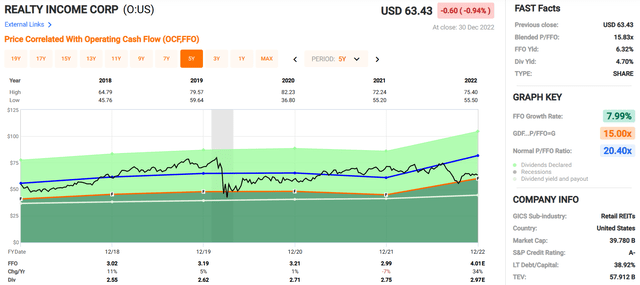

Realty Income is the third one in our coverage to score a perfect 100 Quality Score. While it doesn’t have the FFO / Dividend growth that Prologis and Alexandria have, Realty Income currently offers a higher dividend yield and has historically shown to have a solid business model with responsible and continuous growth over the last several decades. It’s currently trading at a FFO multiple of 15.83x, which compares favorably to its 5-year average FFO multiple of 20.40x. At iREIT we rate Realty Income a BUY.

FAST Graphs

In Closing…

I posted this on Twitter just now:

@rbradthomas

As I pointed out, everyone should Invest in REITs, “you can thank me later.”

We’re living in a very interesting cycle in which our crystal ball can show us…

- Historic jobs recovery.

- Inflation is cooling.

- Gas prices have plunged.

- Real wages are heating up.

- The Fed won’t hike to the moon.

In other words, this is one of the most telegraphed recessions EVER, and that is precisely why I’m deploying more capital into the sector. I’ve been waiting on this type of opportunity and now it’s here…

Be the first to comment