Joe Raedle/Getty Images News

Often, I find myself turned away from companies in the food space. High levels of competition, combined with the possibility of changing consumer sentiment, are not particularly appealing to me as a value investor. Having said that, there are some companies that I have found in this space that offer attractive upside. One firm that has performed exceptionally well as of late is Conagra Brands (NYSE:CAG), an enterprise focused on producing and selling brand names such as Slim Jim, Healthy Choice, Marie Callender’s, Birds Eye, Reddi-Wip, and more. Driven by robust financial performance, combined with the expectation that growth for the company should continue, the stock has seen some nice movement over the past few months. While I would make the case that the easy money has been made by this point, I do still think that shares are cheap enough to warrant some upside from here. So because of that, I have decided to keep the ‘buy’ rating I had on the stock previously.

Tasty results from Conagra

The last article I wrote about Conagra Brands was published in early October of 2022. In that article, I talked about how the company had continued to grow sales, but that profits and cash flows had been somewhat mixed. Despite this, analysts had positive expectations leading into the first quarter of the company’s 2023 fiscal year. Buoyed by that and the fact that shares were trading cheap on both an absolute basis and relative to similar firms, I could not help but to rate the enterprise a ‘buy’, a rating that reflected my view that shares should outperform the broader market for the foreseeable future. Thus far, the company has managed to do just that. At a time when the S&P 500 is up by only 2.2%, shares of Conagra Brands have generated upside of 21.2%.

Author – SEC EDGAR Data

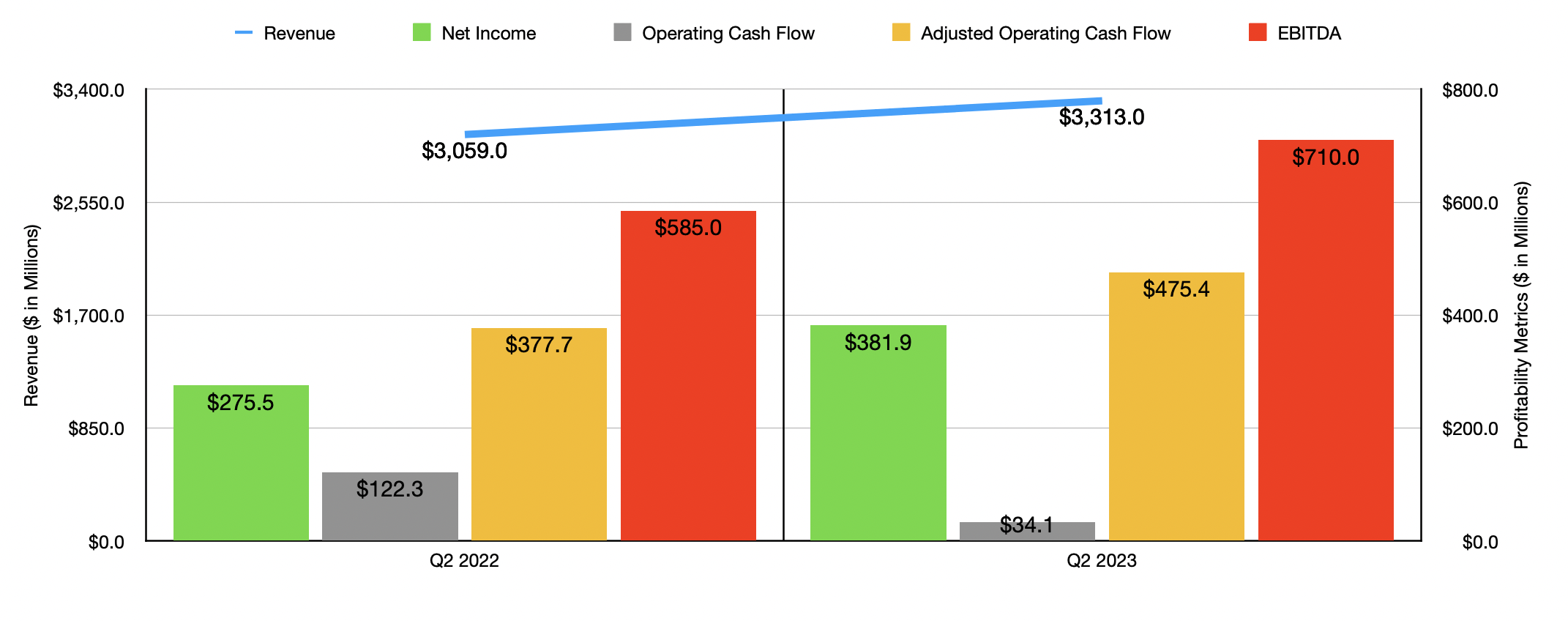

To begin to understand why this outperformance exists, I would like to point first to the second quarter of the 2023 fiscal year. During that time, sales for the company came in at $3.31 billion. That’s 8.3% higher than the $3.06 billion the company generated one year earlier. It’s also worth noting that the amount of revenue the company reported was $30 million higher than what analysts anticipated. On a percentage basis, the greatest growth for the company during that time came from its Foodservice business, with sales climbing 15% from $246.3 million to $282.8 million. This increase, management said, reflected a price and product mix contribution of 18% year over year, with volume declines of 3% offsetting this to some degree. In terms of absolute dollar amounts though, the biggest contribution came from the Refrigerated & Frozen segment, with revenue popping 11% from $1.29 billion to $1.42 billion. Price and product mix added 16% to the company’s sales, with a volume decline of 5% hitting the business.

These increases in revenue translated to improved profits for the company. Net income jumped from $275.5 million in the second quarter of 2022 to $381.9 million the same time this year. Using the non-GAAP earnings per share of $0.81, we also see that the company beat analysts’ expectations by $0.15 per share. Although the increase in sales certainly helped, the company also benefited from a gross profit increase of $78.8 million that management attributed to supply chain productivity improvements and the ability of the company to pass on more than the increase in inflationary pressures to its customers. Naturally, other profitability metrics followed suit. Although operating cash flow dropped from $122.3 million to $34.1 million, this figure, if we adjust for changes in working capital, would have risen from $377.7 million to $475.4 million. And over that same window of time, EBITDA rose from $585 million to $710 million.

Author – SEC EDGAR Data

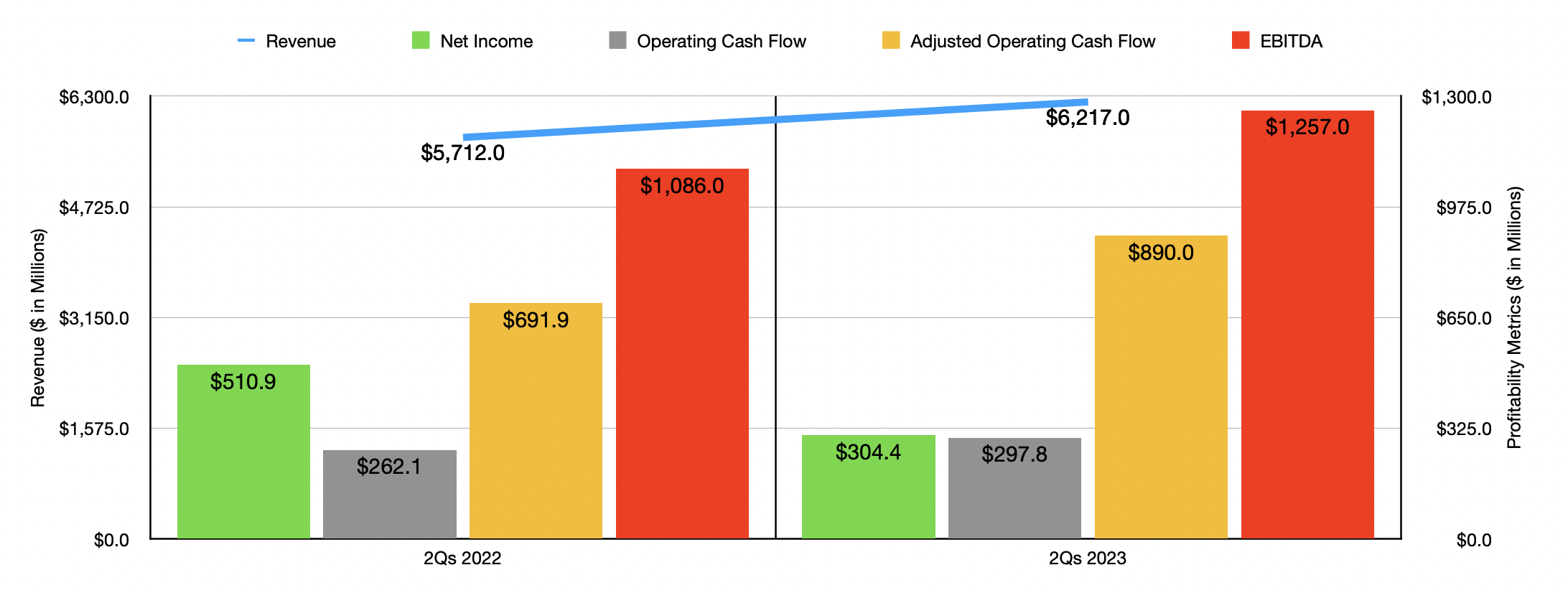

The second quarter for the company was not the only positive quarter. For the first half of 2023 as a whole, revenue came in strong, hitting $6.22 billion compared to the $5.71 billion reported one year earlier. In this case, net income did actually drop, plunging from $510.9 million to $304.4 million. But this disparity was driven largely by a $372.1 million increase in asset impairment charges year over year. Operating cash flow during this time rose from $262.1 million to $297.8 million. On an adjusted basis, it rose from $691.9 million to $890 million, while EBITDA expanded from $1.09 billion to $1.26 billion.

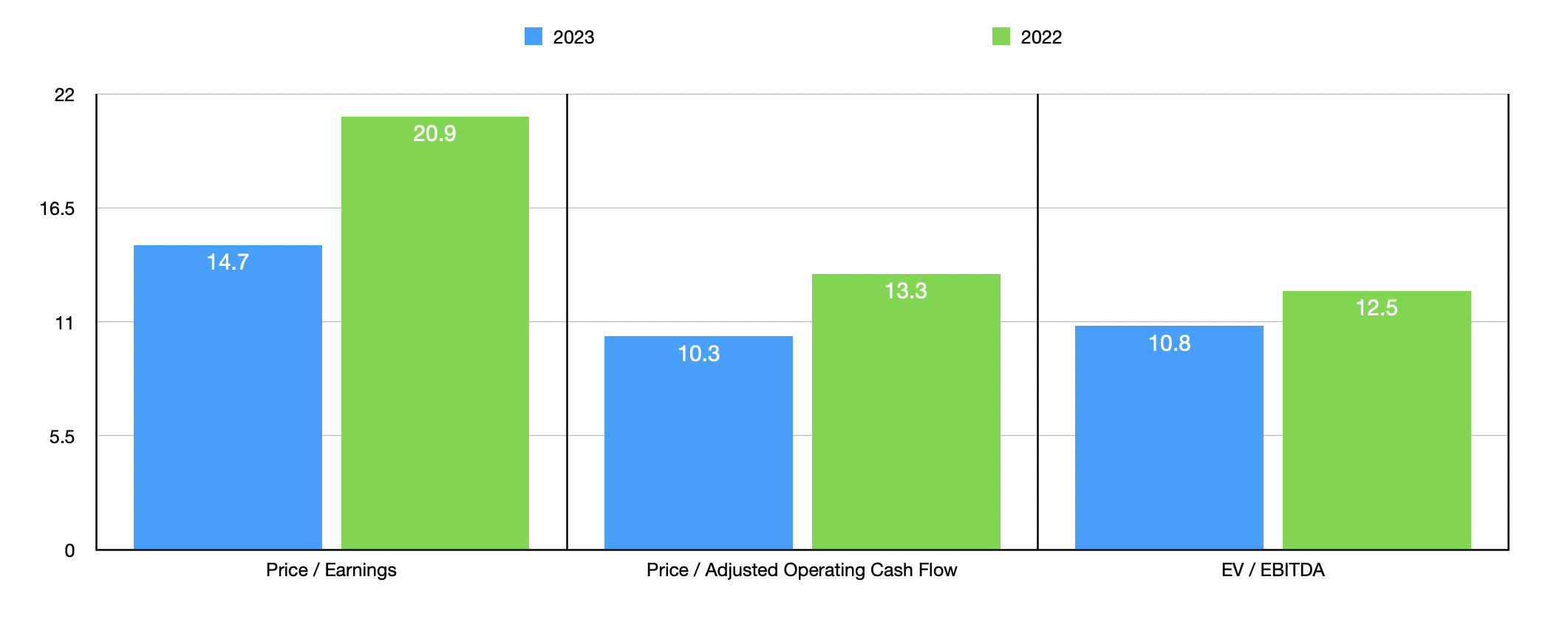

When it comes to the 2023 fiscal year in its entirety, management has some pretty high expectations. Revenue, for instance, is expected to grow by between 7% and 8% on an organic basis. Earnings per share, meanwhile, should be between $2.60 and $2.70, representing a year-over-year improvement of between 10% and 14%. This would translate to net income, given the company’s current share count, of $1.26 billion. It is worth noting that per-share earnings were previously forecasted by analysts for this year to be around $2.47. Unfortunately, no guidance was given when it came to other profitability metrics. But if we annualize results experienced so far, we should anticipate adjusted operating cash flow of $1.80 billion and EBITDA of roughly $2.58 billion.

Author – SEC EDGAR Data

Based on these figures, the company is trading at a forward price-to-earnings multiple of 14.7. This compares favorably to the 20.9 reading that we get using data from 2022. The forward price to adjusted operating cash flow multiple, meanwhile, should be 10.3. That’s down from the 13.3 reading that we get using data from last year. And finally, using the EV to EBITDA approach, the range should be 10.8 compared to the 12.5 reading that we get using data from 2022. As part of my analysis, I also compared the company to five similar firms. Using the 2023 forecast for Conagra Brands, I calculated that, on a price-to-earnings approach, on a price to operating cash flow approach, and on an EV to EBITDA approach, our prospect was the cheapest of the group across the board. Even if we use the data from 2022 instead, using the price-to-earnings approach and the price to operating cash flow approach would result in only one of the five companies being cheaper than it. And when it comes to the EV to EBITDA approach, our prospect is tied as the cheapest of the group.

| Company | Price / Earnings | Price / Operating Cash Flow | EV / EBITDA |

| Conagra Brands | 14.7 | 10.3 | 10.8 |

| J.M. Smucker (SJM) | 25.7 | 15.6 | 13.8 |

| Campbell Soup (CPB) | 19.1 | 12.2 | 12.5 |

| McCormick & Co (MKC) | 28.6 | 25.9 | 21.6 |

| Lamb Weston Holdings (LW) | 27.6 | 18.5 | 15.0 |

| Hormel Foods (HRL) | 25.3 | 19.1 | 17.1 |

Takeaway

What the data in front of me suggests is that, for the most part, Conagra Brands is doing quite well for itself. Yes, investors should continue to watch the volumes of products sold since that could lead to some pain down the road. But outside of that, the data was fantastic. Revenue, profits, and cash flows are all coming in nicely for the year and management feels optimistic about the future. Add on top of this how shares are currently priced, both on an absolute basis and relative to similar firms, and I think it makes for a solid ‘buy’ at this time.

Be the first to comment