Abstract Digital Currency and Exchange Stock Chart Background for Cryptocurrency Technology Coin Market in Finance and Economy Display cemagraphics

The iShares S&P Small-Cap 600 Value ETF (NYSEARCA:IJS) supposedly gives you exposure to small stocks, value, and a very reasonable expense ratio of 0.18%. It wins a popularity vote with $6.7 billion in assets under management. What’s not to love? Surprisingly, a number of things.

Before I discuss this funds methodology, I want clear the air. If you understand how this fund is designed and you are okay with it, then you may not want to read any further. But many investors do not fully understand how a fund works and they might believe something based simply on the label. In my opinion, IJS does not effectively deliver small-cap value exposure.

With that said, let’s begin our dissection of the small-cap value fund.

The Lack of Size Premium

Most investors who buy a small-cap product likely want to take advantage of the size premium.

Pulled right off the FINRA website (Financial Industry Regulatory Authority) is one definition of market cap ranges. Keep in mind that definitions vary.

- mega-cap: market value of $200 billion or more;

- large-cap: market value between $10 billion and $200 billion;

- mid-cap: market value between $2 billion and $10 billion;

- small-cap: market value between $250 million and $2 billion; and

- micro-cap: market value of less than $250 million.

With that in mind, let’s look at the top few holdings of this small-cap fund.

In fact, the largest 45 stocks that make up 25% of this funds weighting have a cap range of $2 billion up to $6.2 billion. Is this what you were expecting with a small-cap fund? Maybe…maybe not.

I can’t completely fault the fund for including larger cap stocks because they clearly say that they are drawing from the S&P 600 index. But what I don’t like is that they are weighting according to market-cap. Bigger stocks get more weight in this fund. They are working directly against the size premium that investors are hoping to take advantage of.

If this was a large-cap fund, then the market-cap weighting scheme would just be tilting further toward size. But in this case, it is tilting away from it.

But it gets worse.

Defining Value

There are many ways to measure value and this fund selects three well-known and commonly accepted ratios.

- Book Value to Price Ratio

- Earnings to Price Ratio

- Sales to Price Ratio

I have no issue at all with how they define value. Now bear with me a moment as I switch gears and tell you how they define growth.

- Three-Year Net Change in EPS over Current Price

- Three-Year Sales per Share Growth Rate

- 12-Month Price Change

Now I raise my eyebrows a little at what they call a growth stock. They are throwing in price momentum and an odd way of calculating earnings growth that actually favors low PE value stocks. But whatever…moving on. That’s not my point.

What if you asked someone to define a value stock and they told you that it was a stock with: negative earnings growth, declining sales growth and horrible relative price strength? Would you agree or disagree? Chances are you would tell them that those three items have nothing to do with value. And I would agree with you. A value stock may have growth or it may not. It may have high price momentum or it might not. That isn’t what defines a value stock.

The IJS ETF defines a value stock as one which has a high value score. But what is a high value score? It is a combination of deep value and low growth. Wait. Back up. Deep value is good. But low growth is not the same as deep value. What does this mean?

This fund isn’t a pure value play. You are getting a mish-mash of value, low growth and low momentum. You know how GARP (growth at a reasonable price) is a thing? You won’t find that here. You know value momentum stocks? Again, that will be excluded here. I strongly disagree that low growth and low momentum is similar to deep value. They are just very different concepts.

But theory is theory and fact is fact. I wanted to see if the stocks in this fund actually had high value scores or not. Therefore, I designed a simple 3-factor value ranking system identical to theirs. What I found is that there are some very low value ranking stocks in this fund. Look at some examples below. The

- (ENSG) – Value score of 15 out of 100 in S&P 600

- (HP) – Value score of 20 out of 100 in S&P 600

- (ADC) – Value score of 21 out of 100 in S&P 600

I could go on and one but I think you get the point. And if you look up the Seeking Alpha valuation rank of these stocks, which are heavily weighted in the fund due to their larger market capitalizations, you’ll see that these are not value stocks at all. There is a value rank of D to F.

Why The Weighting Scheme?

The guys at iShares are smart. No doubt about it. They know what a value stock is and isn’t. So why is this fund designed this way?

To be honest, they kind of have to. With billions of dollars to invest, there is literally no other way to do it other than to focus on larger stocks and cap-weight. Can you imagine the slippage if they tried to pump $24 million dollars into a stock that trades only $2 million a day?

There are a couple things you can do to lower turnover. One is to cap-weight. The other is to design a system that lowers turnover. Which is what they did by calling deep value and low growth the same. The mechanics of it are a bit complicated and you can read about it here, but the nuts and bolts are that they wanted to take the entire S&P 600 and assign each stock into the value or growth fund. Well…actually there are some stocks that are in both if they rank as a moderate value/growth stock but the market-cap of the stocks are divided up between the two funds. Again, I don’t want to get hung up on small matters. The main point is that they wanted to reduce turnover so they created a system that is inferior in my opinion.

That being said, they do have a pure style version of these ETFs. I would encourage you to closely examine them instead if you are looking for actual value or growth.

How Much Return is Lost?

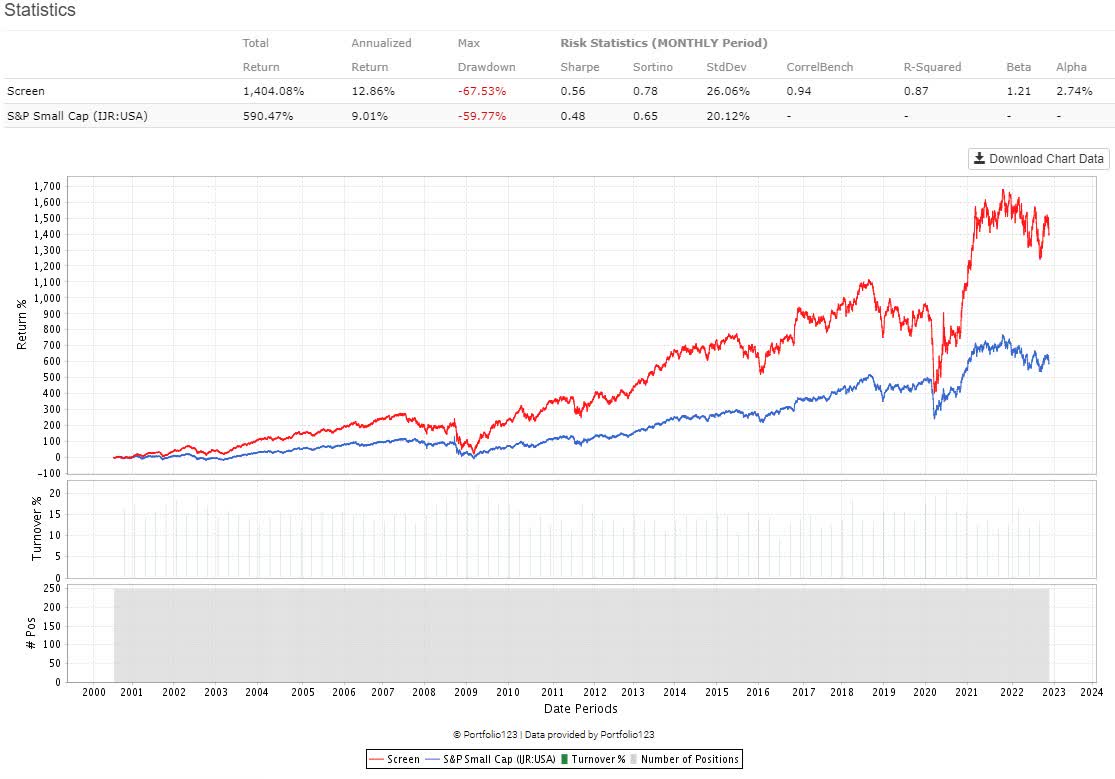

Perhaps you feel that a low expense ratio of 0.18% makes this all worthwhile. But how much is being lost by cap-weighting and not having a pure value approach? This is a simulation where I keep the 250 stocks in the S&P 600 index which have the highest value score (according to their 3 value ratios). Furthermore, I hold these stocks equal-weight. This is a better way to take advantage of the value-size premium. I rebalance quarterly. This translates into about 50% annual turnover.

portfolio123.com

IJR is leaving 4.86% of annual return on the table since inception.

Final Word

If you are looking to invest in low growth, low momentum stocks that may have some value component while favoring mid-cap stocks over small-caps…this might be a fund to invest in. The upfront expense ratio is cheap enough. But I would strongly encourage you to seek out a non cap-weighted fund if you are wanting the size premium. And focus on pure value factors instead. Any fund with this much AUM will struggle to properly deliver the small-cap premium.

Be the first to comment