FilippoBacci

Situation Overview

iHeartMedia (NASDAQ:IHRT) is ~70% on a one-year basis. The primary reason is that IHRT is a cyclical media company with heavy advertising exposure and the recession risk is top of the mind for investors. IHRT is also highly levered at >6.0x, so IHRT’s combination of operating leverage and financial leverage makes this a name that’s difficult to hold onto in front of a recession.

On the other hand, I believe IHRT is more resilient than during previous recessions. First, the Digital Audio Group is roughly 30% of the sum of the segment EBITDA (i.e. excluding corporate SG&A) and still with significant growth runway. Second, IHRT has a favorable maturity profile with a runway until 2026. Taken together, I believe IHRT should be able to survive a downturn.

However, past recessions show that traditional radio advertising goes down by 15-20%. Given the high fixed cost structure of IHRT (and all radio operators), IHRT’s EBITDA could drop by 10-15% even accounting for the high growth rate at the Digital Audio Group segment. While I expect IHRT to generate positive FCF even in a downturn, IHRT’s current highly levered capital structure simply doesn’t work for the equity.

Financial Model

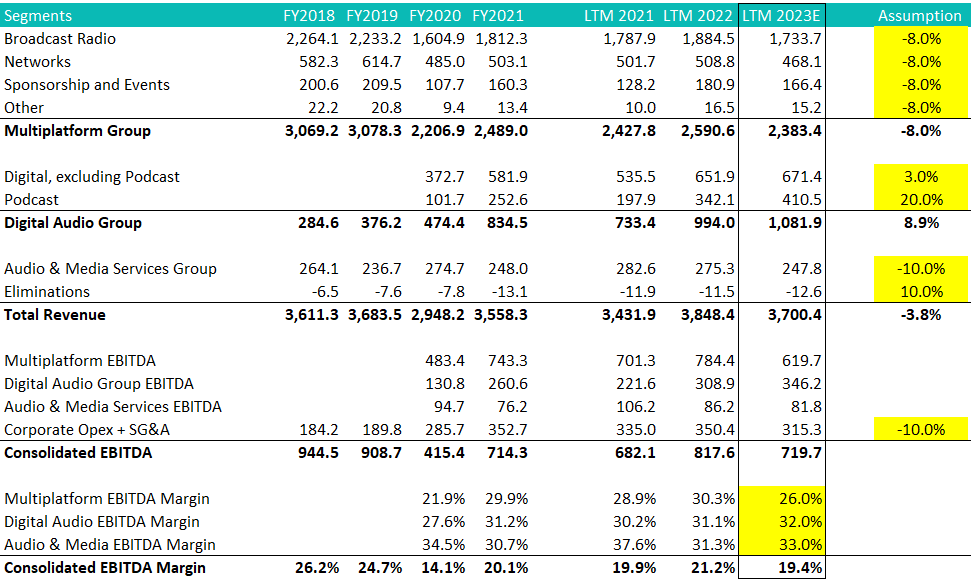

Since the FY2022 numbers are not released, my simple model is done on an LTM basis. While the timing of the recession is impossible to pin down, the conventional wisdom is that it’s more likely to happen in 2H2023, so I dialed back my expectation for the revenue drop to be 8.0% as opposed to the 15-20% historical range (i.e. more pain to come in 1H2024 before revenue could rebound). I believe Podcast could maintain its impressive growth trend as the penetration rate increases, but general digital advertising to taper a bit (it’s still advertising after all).

Margin-wise, I’m mostly using LTM 2021 as a guide given the similar segment revenue levels. I assume the LTM 2023 Multiplatform (which includes the traditional radio ad revenue) does a little bit worse than LTM 2021. The Digital Audio segment EBITDA margin should expand with operating leverage. The Audio & Media segment Margin is a little higher because it captures the Q4-2022 political ad tailwind. Overall, LTM 2023 consolidated margin is a little worse compare to LTM 2021, but far below the pre-COVID level.

Taken together, my expectation for LTM 2023 EBITDA is roughly $720 million. Multiplatform topline drop and margin degradation is partially offset by the Digital Audio Group growth. I also assumed a 10% cost reduction at the corporate level to account for cost rationalization in a downturn.

Company Report and Author’s Estimate

Capital Structure

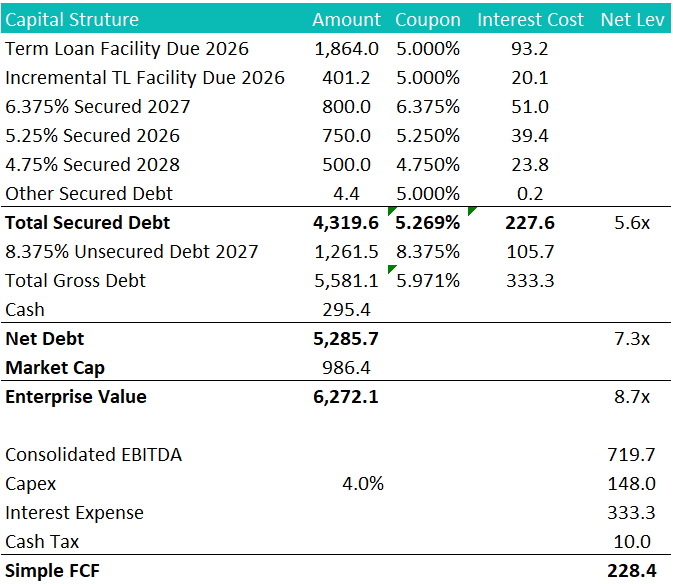

IHRT has ~$4.3 billion secured debt, ~$1.26 billion unsecured bond, and ~$300 million cash on hand. At my estimate of $720 million EBITDA, this puts IHRT’s secured net leverage at 5.6x and unsecured net leverage at 7.3x. At 8.7x EV/EBITDA, IHRT isn’t particularly cheap on a recessionary-level EBITDA. One silver lining is that because of the low capex intensity nature of the business, IHRT is expected to generate positive free cash flow on a more depressed EBITDA level.

Company Report and Author’s Estimate

The management’s focus is on deleveraging. IHRT has repurchased the 8.375% unsecured bonds in the market. However, given the economic outlook, it’s difficult to see IHRT delevering meaningfully. While the ~$230 million FCF makes sure IHRT won’t run into any liquidity issues in the near term, it’s merely ~4% of the total debt (one way to interpret this number is that it takes 25 years to be debt free).

Game Plan

Just because something is down ~70% doesn’t make it cheap. I wouldn’t own the stock right now given the downside earnings risk. IHRT trades at 8.7x my estimate of LTM 2023 EBITDA, while radio broadcasters trade around 8-9x. In my opinion, IHRT equity is overvalued considering the macro and balance sheet risk. The equity value also becomes very sensitive with an overly leveraged balance sheet – assuming a multiple 8.0x, IHRT stock is worth $3.20/share.

TRACE

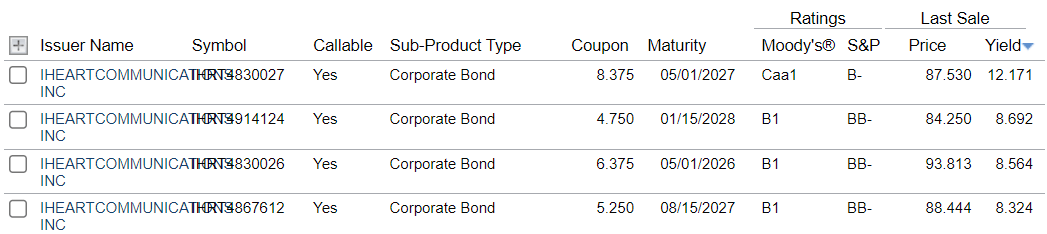

IHRT is levered at 7.3x through the unsecured, which is not particularly attractive from a valuation coverage standpoint (i.e. very little margin of safety). Also, the 8.375% unsecured bond’s $87.5 bond price is most likely elevated by the fact that the market knows the management wants to chip away at this high-cost debt, which is another way to say that the price should probably be lower if not for this technical buying pressure. However, if you are in the soft landing camp and want to have long exposure to cyclical media, I think this unsecured bond is a better bet than the stock at this point.

IHRT’s three secured bonds are all trading in the ~8.5% YTM range. I could somewhat warm up to owning these secured notes. Besides the secured status, the 4.75%/2028 particularly is trading at $84 which means you can create IHRT at less than 5.0x recession-type EBITDA (5.6x levered at face value, multiple by 84% of par). While the current yield is not particularly attractive, I think this is the best risk-adjusted part of the capital structure. I’d recommend shorting some IHRT stocks as a hedge for the downside.

Risk

The upside risk is a soft landing defined by inflation coming down to the central bank’s 2% target while the unemployment rate doesn’t jump up to levels that are historically associated with a recession – this is less likely but still a realistic scenario according to some market strategists. If the soft landing scenario becomes the consensus view, the market might start to incorporating a view that IHRT could achieve a pre-COVID EBITDA level of $900-920 million. At $920 million EBITDA, the equity is valued at 6.8x EV/EBITDA, leaving some room for a multiple expansion. The >$400 million FCF also goes a long way to delever the balance sheet.

Conclusion

In the face of a potential recession, IHRT’s stock is not cheap even after a 70% drawdown. The advertising revenue will inevitably shrink and the high fixed cost structure is going to cause the EBITDA to drop significantly. While IHRT could survive a downturn due to its ability to generate free cash flow, given the high starting point of leverage, it’s difficult to see how IHRT could delever meaningfully to make the equity work. In my opinion, the 8.37% unsecured bond is a better alternative for the positive carry and IHRT has been a buyer of this particular bond. I favor the secured bonds within the capital structure, particularly the 4.75%/2028s, but I’d recommend shorting some stock as a hedge going into 2H2023. Alternatively, I’d wait for the secured bond price to drop further. I consider $73 (or 12% YTM) an attractive risk/reward.

Be the first to comment