GoodLifeStudio

Investment Thesis: I take the view that Hyatt Hotels Corporation (NYSE:H) could see further upside on the basis of RevPAR growth across luxury brands and the lifting of COVID restrictions in China.

In a previous article back in November, I made the argument that Hyatt Hotels could see further upside going forward. My reason for making this argument was that encouraging growth in RevPAR and earnings, as well as a reduction in long-term debt, demonstrated that Hyatt was performing strongly in spite of inflationary pressures.

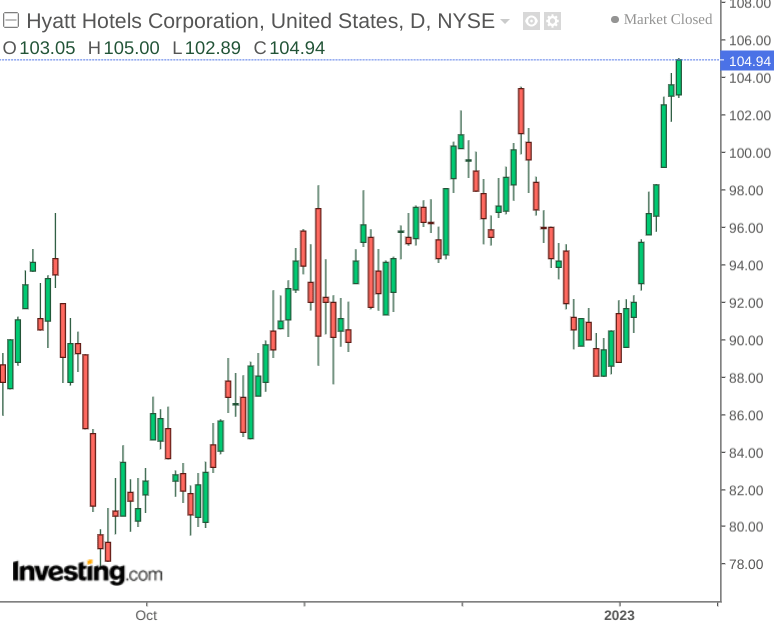

Since my last article, Hyatt Hotels Corporation stock is up by over 15%:

investing.com

The purpose of this article is to investigate whether upside in Hyatt stock can continue from here and what investors may look for in full-year earnings next month.

Performance

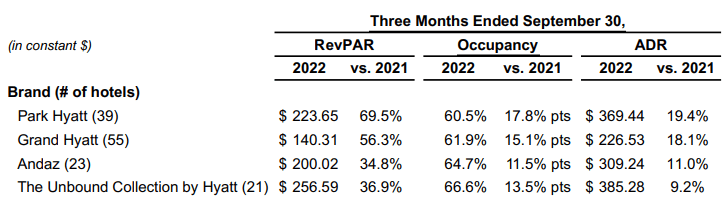

In my previous article, I argued that Hyatt Hotels has been performing well given that while ADR (or the average daily rate) was increasing across its high-priced brands, RevPAR (revenue per available room) was also increasing. This is an indication that, even with inflationary pressures, revenue growth has continued to rise. This is particularly the case across luxury brands, where customers are not as price sensitive.

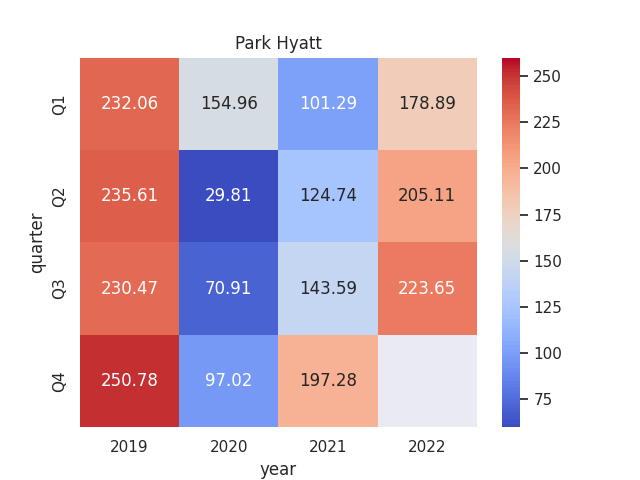

For instance, when looking at RevPAR trends for the Park Hyatt – which had the second-highest ADR across brands for Q3 2022 after that of The Unbound Collection by Hyatt, we can see that RevPAR levels for Q3 2022 have virtually recovered to that of the same level as seen in Q3 2019.

Figures sourced from Hyatt Hotels Quarterly Earnings Reports (Q1 2019 to Q3 2022). Heatmap generated by author using Python’s seaborn library.

What is also notable is that the Park Hyatt also had the second-largest number of hotels by brand – after the Grand Hyatt:

Hyatt Hotels Corporation: Q3 2022 Earnings Release

From this standpoint – Hyatt Hotels as a whole has significant exposure to the luxury end of the market – with three out of four hotel brands showing an ADR above $300. In this regard, the company is in a good position to withstand inflationary pressures.

Looking Forward

Going forward, I expect that a significant focus for investors will be whether Hyatt Hotels can ultimately continue to bolster RevPAR going forward.

We have seen that for the Park Hyatt – Q3 2022 RevPAR virtually rebounded back to the level seen in Q3 2019. From this standpoint, investors may also expect significant RevPAR growth for Q4 back towards the level of $250 seen for Q4 2019.

Should RevPAR remain significantly below this – then this might be a risk of downside for Hyatt Hotels Corporation stock, as it may signify that the recovery in RevPAR has run its course and recessionary concerns are finally starting to negatively affect demand across Hyatt’s luxury hotel brands.

With that being said, the reopening of China from an extended “zero-COVID” policy could still present significant growth opportunity for Hyatt Hotels. For instance, Hyatt is currently undertaking 352 projects across the four and five star segments globally – consisting of 77,709 rooms in total.

It is notable that 57% of these developments are set to appear in Asia – with China comprising the largest Asian market with 146 premium developments.

In this regard, while there is the possibility that revenue growth across the United States and Europe is reaching a peak – the company’s investment in Asia along with the full reopening of the Chinese economy could lead to further growth opportunities for 2023.

Conclusion

To conclude, Hyatt Hotels has seen strong RevPAR growth across its higher-end luxury brands. I take the view that concerns of a peak in post-COVID revenue growth notwithstanding – Hyatt Hotels Corporation has continued to show strong resilience in an inflationary environment and I expect that this is set to continue.

Moreover, with the reopening of China and the continued investment by Hyatt Hotels in the Asian region – we could see further revenue growth potential across this market in 2023.

For these reasons, I continue to take a bullish view on Hyatt Hotels Corporation.

Be the first to comment