Panama7

So often we hear about tech startups that deserve eye-watering valuations due to their potential. On the flip side, stalwarts of the tech industry like Apple (AAPL) and Microsoft (MSFT) rightfully earned their price to earnings through a history of consistent performance.

But what about the firms that have fallen out of favor with investors simply because they don’t grab the headlines?

Enter HP Inc. (NYSE:HPQ), a tech giant with a strong foundation and an impressive track record, facing headwinds in its operations but priced at an unbelievable discount.

HP Inc. is a tech behemoth that services several business areas: personal computing, imaging and printing, and related technologies. Personal Systems provides PCs, workstations, and other devices, while Printing offers printers, supplies, and solutions. Corporate Investments is involved in research and business incubation.

This article will look to give a short assessment of the firm’s financial health, address some headwinds and concerns on the balance sheet, and provide a pricing mechanism for HP based on its historical financials vs the US market as a whole.

We will be comparing HP Inc. to the “All US Stocks” screener on Seeking Alpha, which includes 2,462 of the largest US stocks on the market.

(Data & prices correct as of pre-market 5th November, 2022)

(The “All US Stocks” list referred to in this article can be found on this Seeking Alpha screener)

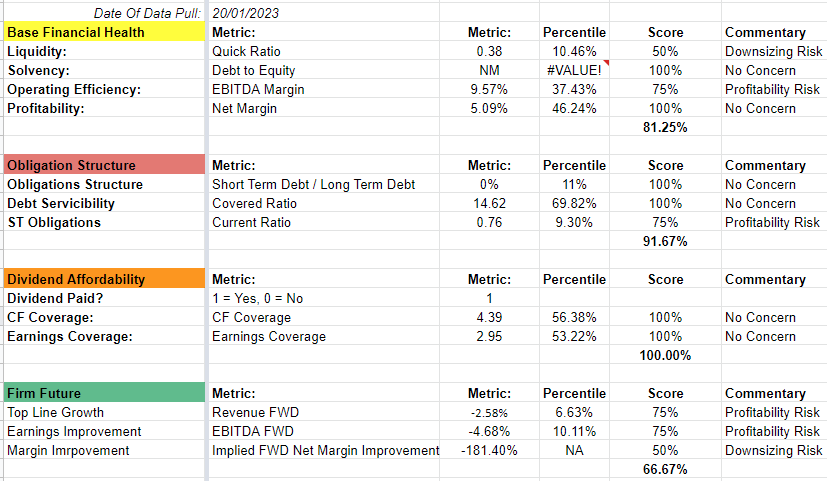

HP Inc.’s Base Financial Health

When assessing the financial health of HP Inc., the Quick Ratio of 0.38 indicates a level of risk associated with a worst-case scenario for the firm. The EBITDA Margin of 9.57% is relatively low, as is the Net Margin of 5.09%. However, the Covered Ratio of 14.62 and Current Ratio of 0.76 suggest a relatively good ability to meet short-term debt obligations. The FWD Revenue growth outlook of 5.48% is reasonable. Additionally, the FWD EBITDA of 12.27% and Implied FWD Net Margin Improvement of 223% suggest an improvement in efficiency.

Overall, HP Inc. has a fair financial health, with a good coverage ratio and improving efficiency, indicating that the company may have the ability to meet its short-term obligations.

Author

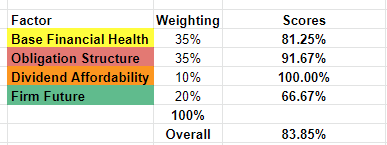

Overall, the company’s financial health score of 83.85% suggests that it is a relatively stable but highly leveraged company, though areas of concern are understandably the short-term future outlook and its liquidity.

Author

Assessing HP Inc.’s Pricing Attractiveness

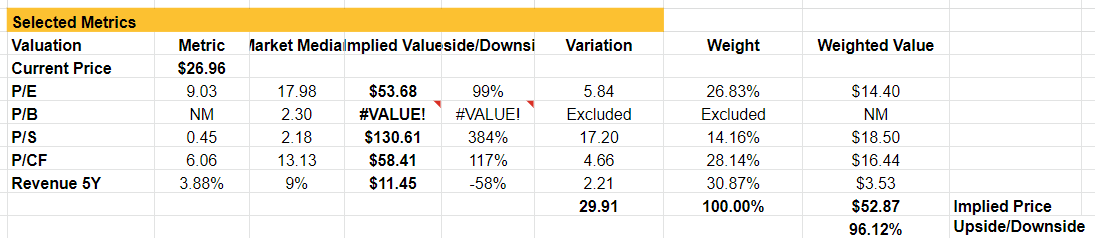

When assessing the pricing attractiveness of HP Inc., the Price/Sales ratio of 0.45 and EV/Sales ratio of 0.58 suggests that the firm is trading at a discount compared to its peers. The P/E TTM of 9.03 is relatively low, while the Price/Cash Flow ratio of 6.06 is also relatively low. The company’s pricing attractiveness score of 81.99% suggests that it may be undervalued based on comparing these valuation metrics to the peer group.

(Note however that the firm has a negative Book Value, and therefore the P/B metric is not useful to us. More on negative equity later.)

Author

Noteworthy

It’s important to note that the firm is producing $60.68 in revenue per share, while trading at $26.96 per share (at the time of writing), offering investors a 2.25 multiple in revenue generation for every dollar in share value.

Looking Forward

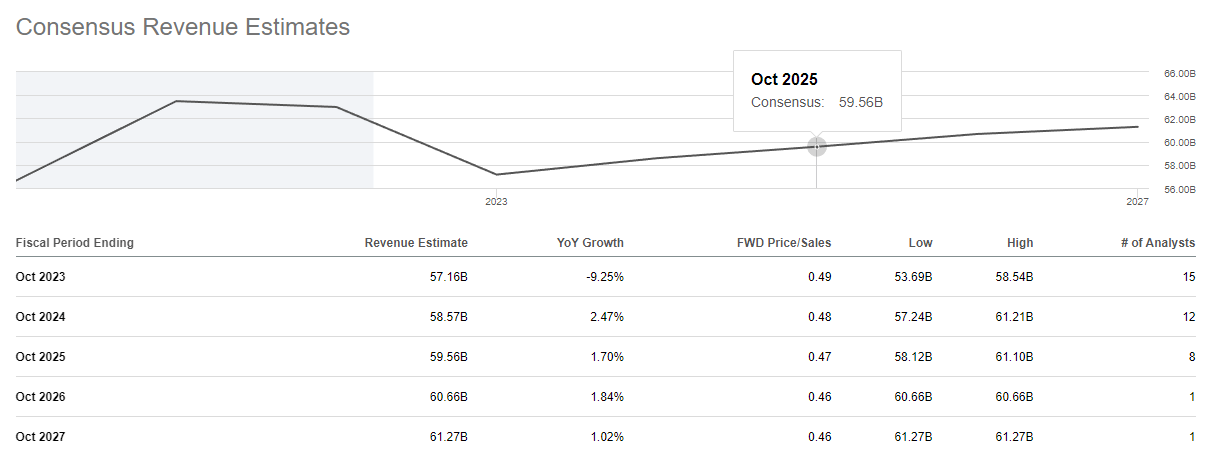

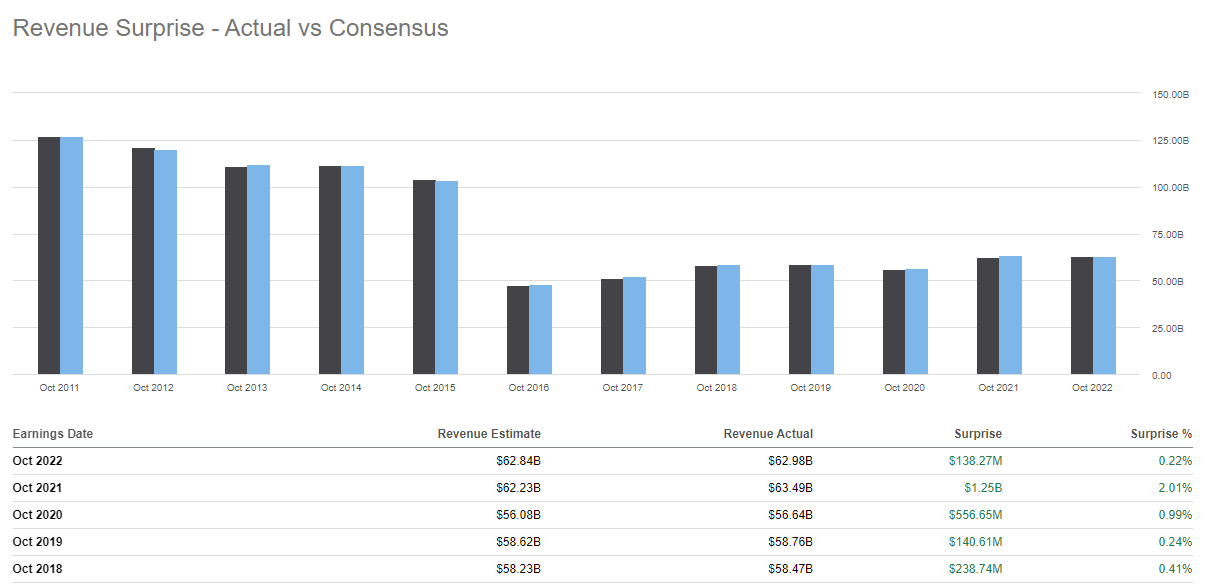

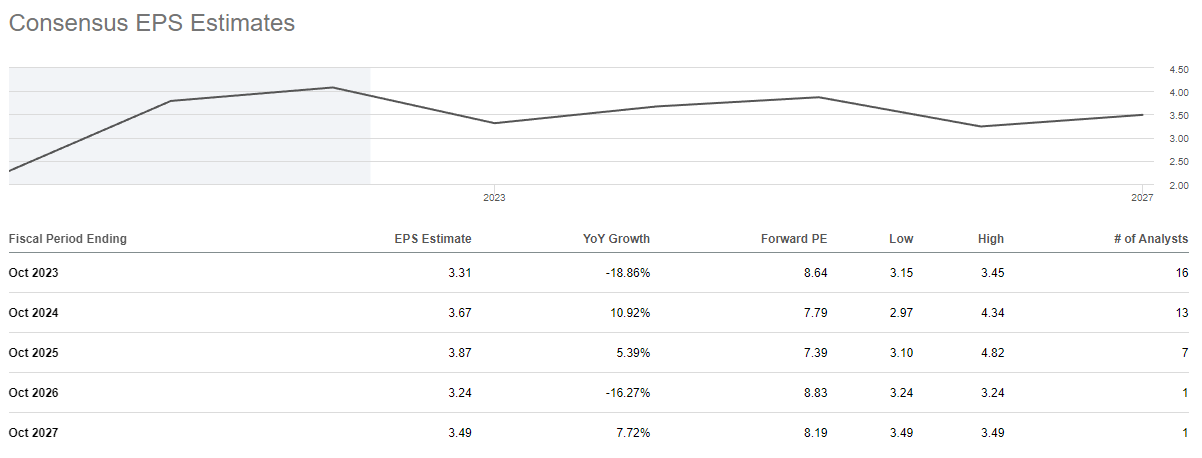

Taking a forward-looking view of HP, we’ll rely on analyst forecasts to guide us in setting our expectations of future revenues. There are a good number of analysts covering the firm with estimates looking forward at least 2 years (12 analysts), and at least 8 giving us a 3-year picture.

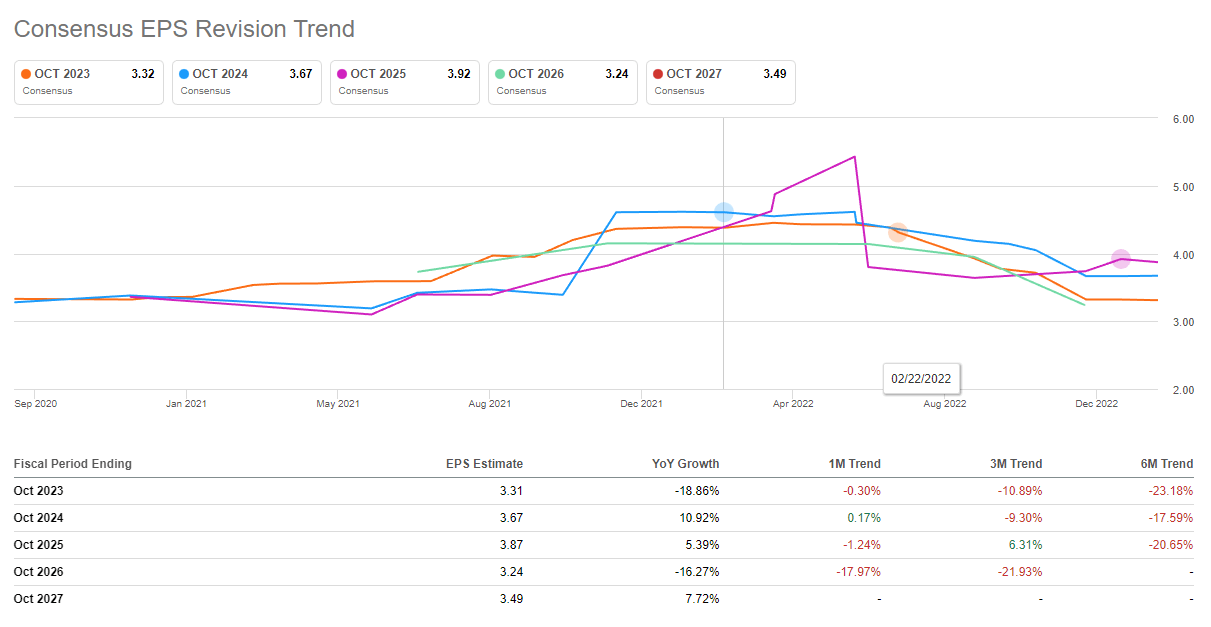

Revenues are forecast to fall in the short term seeing a ~9% fall in 2023, which will hamper EPS by roughly double that (~18%).

Seeking Alpha

Unfortunately, these estimates have downward trending revision histories, however the positive is that historically the analyst’s estimates appear to be very accurate, giving us a sense of confidence in their forecasts.

Seeking Alpha Seeking Alpha Seeking Alpha

While these forward-looking estimates don’t envision the most attractive near-term future for the firm, further forward-looking estimates (3+ years) do give hope for growth for HP.

Investors could view this as an opportunity to acquire a stake in the firm during its tougher years, with expectations set for a positive future.

The Worm In The Apple – Negative Equity

One aspect that does make HP unattractive is the negative equity aspect of its balance sheet. Total Liabilities of (41,505M) outweigh Total Assets (38,587M) by 2,918M (7.5%), while retained earnings is -4,413M.

Is that bad? Well, not entirely.

In context, the firm’s debt of $12.372B puts it within the top 92nd percentile in the US market for size, and its debt-to-capital ratio of 124% is in the 97th percentile. But this debt has a coverage ratio of 14.62, a 69th percentile ratio suggesting this debt is well covered by income and better covered than most listed company debts. Further, a current ratio of 0.76 means the firm has a level of cushioning in the event of softening revenues.

While this indicates that HP is leveraged in the extreme, it is a well-serviced debt that doesn’t appear to be a significant near-term threat.

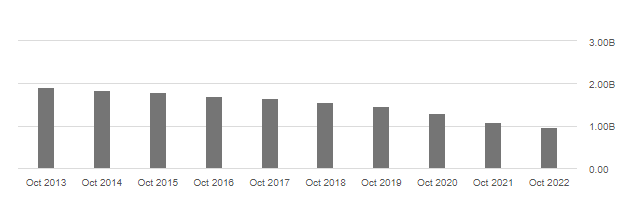

Further, a cause of negative equity for the firm also appears to be an overall fall in shares outstanding, and therefore, shareholder equity funding the company, skewing the total equity figures as the firm’s balance sheet profile changes.

HPQ Total Common Shares Outstanding (Seeking Alpha)

Finding An Appropriate Valuation Method For HP Inc.

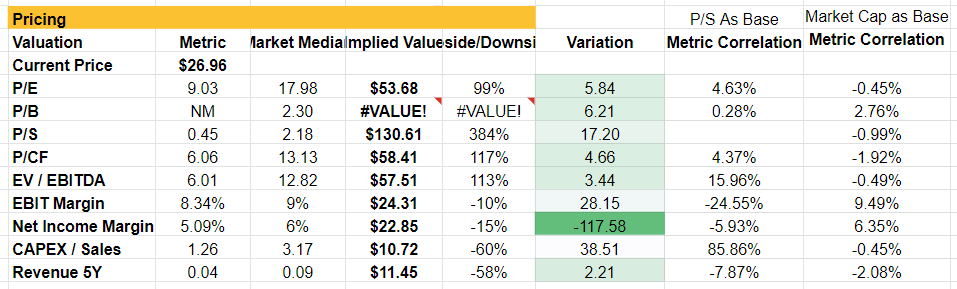

In determining the appropriate valuation method for HP Inc., we will compare various metrics to the company’s peer group and evaluate the reliability and correlation of each metric with regard to Price-to-Sales and Market Capitalization before determining the most crucial metrics to focus on.

It’s worth remembering that this is a pricing analysis based on historical metrics, and so we are pricing HP against the peer group based on the past 12 month’s performance, and not factoring in forward estimates in this valuation.

Author

Based on our analysis of HP Inc.’s financial health and pricing attractiveness, it appears that the company is performing well and is slightly undervalued compared to its peers.

Our analysis suggests that there is potential for growth if the company’s narrative improves, as it is severely undervalued against the peer group based on historical financials, creating a catalyst for large upside swings.

Author

Potential Upside Risks

-

The company’s focus on personal computing and printing products, which are staples in the technology industry, could provide a steady stream of revenue even in a recession.

-

HP Inc.’s diversified revenue streams through its three segments, Personal Systems, Printing, and Corporate Investments, could provide cushioning against any potential downturns in specific segments.

-

The company’s strong financial health, as demonstrated by its high liquidity ratios, low debt-to-equity ratio and strong margins, suggests that it has the ability to weather a recession.

-

HP Inc.’s recent investments in business incubation and research and development through its Corporate Investments segment could lead to the development of new, potentially profitable products or services.

-

The company’s strong brand recognition and reputation could allow it to maintain or even gain market share during a recession, as consumers may be more likely to stick with established brands during uncertain economic times.

Potential Downside Risks

-

The personal computing and printing industry is highly competitive and subject to rapid technological change, which could negatively impact the company’s revenue and profitability.

-

HP Inc. relies heavily on its Personal Systems and Printing segments for revenue, and a decline in demand for these products could negatively impact the company’s overall financial performance.

-

The company operates in a global market and is exposed to currency fluctuations, geopolitical risks, and economic conditions that could negatively impact its financial performance.

-

HP Inc. has a significant amount of debt on its balance sheet, which could increase the company’s financial risk in the event of an economic downturn.

-

The company’s revenue and profitability is dependent on its ability to continue to innovate and develop new products and services. If it is not able to do so, it may struggle to compete in the market.

Closing Remarks

In conclusion, HP Inc. appears to be a financially stable company with a fair overall financial health score of 83.85%. The company’s pricing attractiveness score of ~82% suggests that it is undervalued compared to its peers based on its valuation metrics past performance.

But HP is not without its risks, and the extreme leverage is one aspect investors should be cautious of when they factor in forward-looking estimates with negative growth, as this leverage will leave the firm vulnerable in its ability to service debt.

Given these factors HP is not for the faint of heart, so for investors with risk appetites, we recommend buying HP Inc. with a price target of $52.87 over a longer-term horizon.

With that said, it would be irresponsible of me not to point out that this analysis is limited in its scope to just a quantitative peer analysis. While we do look at the firms financials, it does not go searching for detail and context that one might find reading earnings transcripts. Further, the analysis is of the market as a whole but does not consider the specific industry the firm operates in, and does not break down a near-peer comparison. Investors should use this analysis as a base-line for their analysis, but spend time looking at the firm’s qualitative aspects to further inform their thinking.

Be the first to comment