Junko Kimura/Getty Images News

Investment thesis

Capcom (OTCPK:CCOEF) is aiming for its tenth consecutive year of operating profit growth in FY3/3023, demonstrating its ability to sustain growth with high-quality IPs. Although a high-risk strategy, the release of two new major titles in FY3/2024 is likely to have some success, allowing the company to build further growth opportunities. We reiterate our buy rating.

Quick primer

Capcom is a Japanese videogame developer and publisher with core franchises such as ‘Resident Evil’, ‘Monster Hunter’ and ‘Street Fighter’. It also develops arcade game machines, pachinko/pachislot (Japanese gambling machines), and operates ‘Plaza Capcom’ arcade centers. Its peers include BANDAI NAMCO (OTCPK:NCBDF), Sony (SONY), Kadokawa (OTCPK:KDKWF), and Sega Sammy (OTCPK:SGAMY).

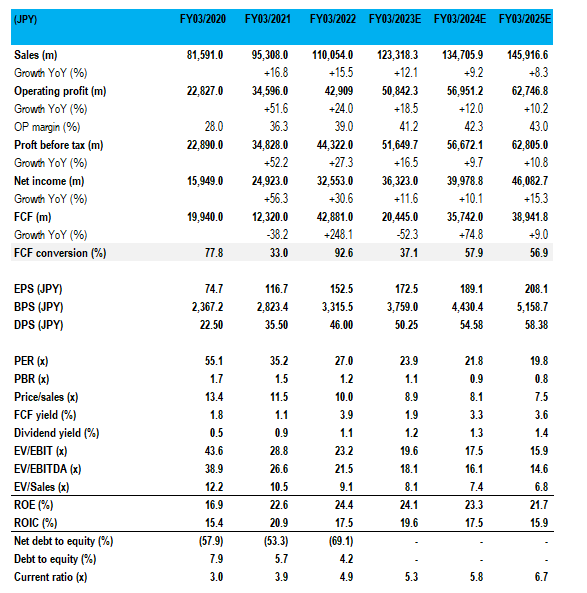

Key financials with consensus forecasts

Key financials with consensus forecasts (Company, Refinitiv)

Our objectives

We want to update our view from our buy rating in May 2021, as visibility was strong in Capcom’s two key franchise titles – ‘Monster Hunter’ and ‘Resident Evil’. Since then, the company has highlighted its objective to sustainably grow annual sales by 10% YoY, and has continued the development of two new franchises that are planned to become major titles – ‘Pragmata‘ and ‘Exoprimal‘.

Strong recent trading, driven by ‘Sunbreak’ and back catalog

Q1-2 FY3/2023 results were stronger than expected, with operating profit 20% above consensus estimates. Despite both sales and operating profit declining nearly 30% YoY due to high hurdles YoY, the performance of ‘Monster Hunter Rise: Sunbreak’ and back catalog sales were stronger than expected. Unit volume sales in the consumer software business (primarily console games) increased to 21.3 million from 19.8 million (+7.5% YoY) (page 9), bucking the trend of the post-pandemic decline in gaming activity worldwide. A weak Japanese yen helped sales grow stronger YoY, but operating margins remained elevated at 44.6% for the period, versus 41.3% a year previously.

Capcom has also benefitted from customers returning back to the arcades, with same-store sales growing 26% YoY (page 11), as well as amusement equipment sales ramping up for the pachislot business. The company opened a new arcade center in October 2022, and a major title ‘Monster Hunter World: Iceborne’ for Pachislot is due to launch in January 2023.

The positive performance to date as well as tailwinds in the arcade business led to the company raising its FY guidance mildly for FY3/2023, with sales and operating profit raised by 4% from the original. Expectations remain for a very year-end loaded performance with the release of the key remake title ‘Resident Evil 4’ for March 24th, 2023. It nevertheless is highly commendable that Capcom is set to achieve 10 consecutive years of operating profit growth – a rarity in any business, moreover in a hit-driven game industry.

Outlook for the medium term

Capcom has established a strong track record of sustained growth over the last 10 years and has a roster of strong IPs to shuffle and release in order to maintain momentum. However, there is always the risk that top franchises begin to underperform, so the company has been working on new IPs in order to increase its portfolio.

The company has traditionally been quite conservative with regard to new IPs. There have been iterations of a similar theme (for example, ‘Resident Evil’ and ‘Dead Rising’), and niche but highly acclaimed titles such as ‘Viewtiful Joe’, ‘Phoenix Wright’ and ‘Okami’ usually for Nintendo (OTCPK:NTDOY) platforms. After much fanfare, a key release for the PlayStation 4 called ‘Deep Down‘ was canned and never released. There is limited news on the new IPs, but both ‘Exoprimal’ and ‘Pragmata’ are due in 2023 on PlayStation 5, Xbox, and PC.

Although it may be too optimistic to expect both new major titles to become million-seller hits, we expect at least one will make the grade. With ‘Resident Evil 4’ expected to continue selling into Q1-2 FY3/2024, there is still potential for the company to grow earnings YoY through the combination of back catalog repeat sales and new IP adoption. FY3/2024 will also see the release of old favorites ‘Street Fighter VI’, and ‘Mega Man’.

What gives us an indication of Capcom’s lasting power is its high ROIC which has averaged a high 16.6% over the last 5 years. This signifies that the company has been successful at investing in projects yielding high returns, which bodes positively for future releases.

Valuation

On consensus forecasts (see Key financials table above), the shares are trading on PER FY3/2024 21.8x on 12% operating profit growth YoY, and a free cash flow yield of 3.3%. Whilst these multiples are not low, the company is a high-quality franchise with a sound track record, high ROE consistently above 20%, a net cash balance sheet, and high double-digit profitability which would place a premium on the shares.

Risks

Upside risk comes from a strong finish to FY3/2023 with the release of ‘Resident Evil 4’, providing high earnings visibility with repeat sales into FY3/2024.

More news and positive feedback on ‘Exoprimal’ and ‘Pragmata’ releases at the E3 conference in May 2023 will heighten expectations into the second half of FY3/2024.

Downside risk comes from lower-than-expected sales for ‘Resident Evil 4’, which is a remake title of arguably Capcom’s most acclaimed original title.

Delays and postponements for ‘Exoprimal’ and ‘Pragmata’ will be negatively viewed by the market.

Conclusion

Capcom has defied the usual business model of a game developer by maintaining a sustained growth profile, even with a pandemic as well as console cycles. Whilst hurdles are being set higher YoY, we believe the company’s high-quality IP can continue to generate growth, and the probability of a brand-new IP performing well during FY3/2024 is high. We reiterate our buy rating.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Be the first to comment