Inflation isn’t going away any time soon. It’s time to think about using cash you have in the bank to fight back!

Khanchit Khirisutchalual

Brian Dress, CFA — Director of Research, Investment Advisor

If you’ve read this newsletter over the past year, there is no doubt you are tiring of hearing the constant drumbeat of the inflation and interest rate narrative. Believe me, inflation is exhausting me too.

However, the reality is that we remain deeply entrenched in the inflation story, with little end in sight. Though these figures can be backward-looking in nature, this week we saw fresh prints in the Producer Price Index (PPI) of +8.5% year-over-year and in the Consumer Price Index (CPI) of +8.2%. Despite whether we quibble with the way these numbers are calculated, the Federal Reserve continues to use these metrics in their decision making process.

The upshot: we expect rate hikes to continue with fervor in the near term, which continues to weigh on markets. As we’ve said over the past few months, we continue to approach markets, particularly stocks, defensively. We have just seen a more-than-a-decade long bull market come to an end and, even after all that carnage, we see household name stocks still carrying premium valuations. These include Microsoft (MSFT; price/sales ratio of 8.9x), Nvidia (NVDA; price/sales of 10.2x), and Tesla (TSLA; price/sales of 11.4x). These are high-quality companies with strong business models and robust growth. With that said, markets became accustomed to high valuations on growth companies over the last decade of near-zero interest rates.

In investing, almost as important as the securities you own is the price you pay for them. Is it reasonable to expect that companies like Microsoft, Nvidia, and Tesla will be higher in five years than they are today? Probably. But given the current valuation on these businesses, our view is that there will be turbulence for shareholders, so long as interest rates remain elevated. At this stage, given inflation data, we don’t expect this dynamic to change soon.

As active investors, we pride ourselves on reading the trends in the market. Not only do we want to be invested in companies with strong business fundamentals, but also we want those stock prices to be moving in the right direction. The mere fact that the stock associated with a quality business is down 30, 40, 50% (or more) does not define an appropriate investment thesis. In our view, we have yet to see investors fully throw in the towel on growth stocks and, until that day, it is hard to imagine large cap growth stocks to rebound meaningfully.

The flip side of lower securities prices is opportunity. Just like stocks, bond prices have dropped dramatically in 2022. We are starting to see investment grade bonds from well-known companies carrying yields of 6-9%, even in sectors that are actually performing well in today’s economy. We think investors sitting with cash in the bank, losing ground every day to inflation, need to act with some urgency. Now is the chance to lock in the types of yields we have not seen in the bond market in nearly a generation. Once the rate cycle does reverse, we think these securities will be some of the first to rise. In today’s letter, we will describe two such securities for you.

With that all being said, let’s get into it!

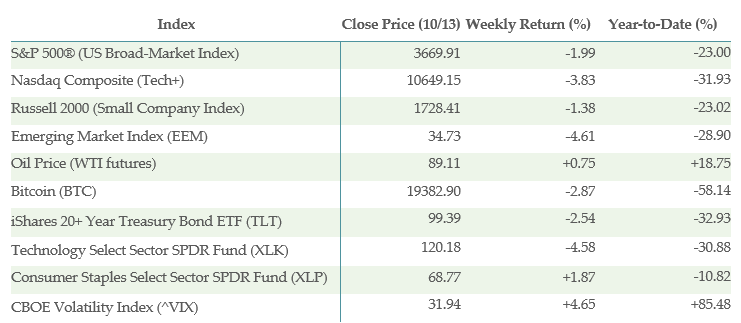

Below is the performance data of key indices, ETFs for the five trading days between 10/6/22 and 10/13/22:

Yahoo! Finance, Left Brain

What is/is not Working?

Despite an impressive counter-trend rally in Thursday’s session, the broad market S&P 500 still lost 2% in value over the past week of trading. Given the volatility that marked the last week, it certainly felt worse to us. Just two sectors gained on the week, consumer staples (up 1.74%) and energy (up 1.19%). Energy continues to be our highest conviction and most-overweighted sector.

We are warming to the story in consumer staples. This week we received the earnings report from PepsiCo (PEP). We learned that the company grew revenues by 10% in the last quarter, but prices were up 17% on a yearly basis. That report makes us look at consumer staples stocks with fresh eyes: they have struggled throughout the year, but it is clearly that these companies have pricing power. Further, food and other commodity prices have started to slide significantly. As that trend continues, we think margins could expand for these companies. We will study this theme more in depth in our future articles and videos, as additional earnings reports come in over the next few weeks.

In a week where both stocks and bonds sold off significantly, you would not be surprised that the best performing ETFs were those that bet against those markets, including Direxion Daily 20+ Year Treasury Bear 3x Shares (TMV), ProShares Short QQQ (PSQ), AdvisorShares Ranger Equity Bear ETF (HDGE), and ProShares Short High Yield (SJB).

Among the long-oriented funds that did well, there were a couple surprises. The first was the strength in the cannabis sector, which has been one of the most-downtrodden groups of stocks in the markets. The AdvisorShares Pure US Cannabis ETF (MSOS) was the strongest of all the ETFs we follow, rising nearly 11% over the past week. Also, despite rising rates, we saw strong performance from the PIMCO Municipal Income Fund (PMF). We like municipal bonds for investors in high tax brackets, currently holding cash at the bank. Many municipals are tax-free and may be appropriate for those with funds in taxable brokerage accounts, looking for a place to hide.

Beyond those surprises, we saw four of our top 20 ETFs coming from the energy space, including the Energy Select Sector SPDR Fund (XLE) and the ClearBridge MLP and Midstream Fund Inc (CEM), which covers stocks in the pipeline side of the energy business. We will cover our thoughts on pipelines further later in the letter.

On the negative side of the ledger, we continued to see the biggest slides in the “risk on” segments of the market, concentrated in tech and tech-adjacent sectors. Crypto was hit especially hard this week (even though Bitcoin itself held up fairly well), with Invesco Alerian Galaxy Crypto Economy ETF (SATO), Grayscale Ethereum Trust (OTCQX:ETHE), and Bitwise Crypto Industry Innovators ETF (BITQ) all down double-digits for the week.

Chinese internet stocks were the worst performing group this week, with the KraneShares CSI China Internet ETF (KWEB) down a whopping 14.28% in just a week. We continue to preach caution to investors in terms of investing in emerging markets, particularly in China. Our preference for international exposure continues to be for US multinationals, who have plenty of economic sensitivity to those regions. Our favorite play on China continues to be Starbucks (SBUX).

Tech and other risk on sectors here in the US also are having a hard time finding footing. We saw major declines in VanEck Semiconductor ETF (SMH), First Trust Cloud Computing ETF (SKYY), Invesco Solar ETF (TAN), Renaissance IPO ETF (IPO), and the ARK Innovation ETF (ARKK). In practice, we have observed these particular segments of the market to be extremely interest-rate sensitive, with high multiple stocks moving with almost complete negative correlation to interest rates. We think caution continues to be warranted in these areas until interest rates stop rising so consistently.

Inflation Fighting Idea #1: Starwood Bonds

We have been as explicit as possible in this space, over the past months, that we think the best opportunities in financial markets lie in the fixed return space. This means we have oriented much of our research capacity to identifying new and novel opportunities in bonds. For years we were forced to reach down into the lower depths of the junk bond markets to find income for our investors in or near retirement. Though we had some reservations with the risk profiles of these instruments as an asset class, persistently low rates forced investors to bear more risk than was comfortable to generate the income that was essential to cover their expenses in retirement.

Clearly, higher interest rates have been a challenge for both stock and bond investors throughout 2022. On the other hand, for investors with cash in the bank still earning close to zero, we continue to unearth attractive opportunities to lock in generous income for many years going forward. Not only that, higher rates empower investors to find those generous annual yields in high quality income securities with relatively low default risk. For those straining to generate income with your portfolios over the last 15 years, you will know that this opportunity has not existed at all in that time.

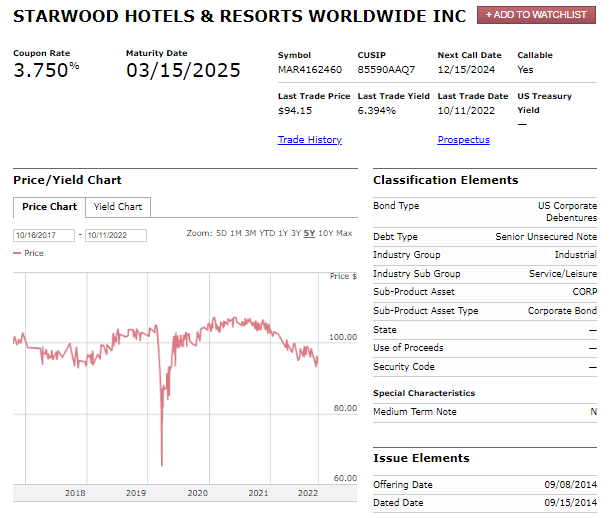

Right now, we are carrying cash balances much higher than normal in investor accounts. The reason for this is that we have sold many stocks that we previously favored, understanding that we are in a bear market. One such company stock that we have sold over the past year is Starwood Property Trust (STWD). For those unfamiliar with Starwood, this is a diversified mortgage Real Estate Investment Trust (REIT) that provides financing for a variety of real estate projects, including residential, commercial, infrastructure, and beyond. The company is managed by one of our favorite CEOs in Barry Sternlicht, who has overseen the growth of the company since its 2009 IPO to become one of the largest commercial real estate financing companies in the world.

REITs (and real estate in general) has been one of the hardest hit corners of the economy, owing to the obvious interest rate sensitivity of the business model. As such, we have moved away from any stock positions in companies like Starwood. But we still like the underlying business and the superior management in place. Despite the challenges in 2022 from the interest rate perspective, Starwood has maintained its interest coverage ratio (one of the most important metrics for creditworthiness) at a constant value relative to historical levels. This gives us great confidence that the company remains strong and well-positioned to service its obligations, even in a higher rate environment. A number of the bonds in the capital structure of Starwood continue to maintain an investment grade credit rating of BBB, another data point that adds to our comfort level with the story.

We like a number of securities in the bond “stack” of Starwood, but one stands out. The 3.75% 2025 Starwood bonds do carry an investment grade credit rating. As rates have risen, the price of the bond has fallen and now trades at a discounted price of roughly 94 cents on the dollar. Considering both the capital appreciation potential and the coupon income involved here, investors have the opportunity to lock in roughly 6.4% of annual return on these bonds. We also like the short-term nature of the bonds here. Once the bond matures, we are hopeful that the stock market will be on stronger footing. At that time, an investor can decide whether to move on and redeploy the money into stocks or, if rates remain elevated, roll into another fixed income investment.

For investors looking to lock in yield for a longer time frame, we also like the 4.5% 2034 bond, which implies an annual total return yield of just over 6.7%. We think either bond is a good candidate for investors looking to lock in a bond ladder in the current period when interest rates are high.

FINRA Trace

Inflation Fighting Idea #2: Pipeline Bonds (and Stocks)

For most of 2022 (and some of 2021), our CEO Noland Langford has talked my ear off about the pipeline companies. Yes, we have long been in agreement that the energy sector is a great area of the market for investors to consider for overweighting their portfolio. But Noland has constantly banged the drum that the pipeline operators are especially attractive. He’s finally gotten through to me.

Over the last year, the Energy Select Sector SPDR Fund (XLE), a basket of energy-related companies in all corners of the industry, has delivered more than 41% of return to investors. We also follow a basket of master-limited partnership companies, which is a more technical term for oil/gas pipeline operators. This basket is the Alerian MLP ETF (AMLP), and this group of stocks is up just 4% over the same period! We’ve included the yearly chart of the two funds below to show the stark difference in performance!

We think this represents a significant disconnect and we think it is potentially investible. Pipeline operators generally have fixed-rate contracts with the oil/gas companies that use them to move their product around the country. As a result, business results for pipeline operators are less sensitive to changes in oil prices than are stocks in the broader-energy index of XLE. However, when prices are high as those contracts come up for renewal, negotiated rates tend to be higher. As we are now in a period of persistently high energy prices, we think pipeline operators are in a strong position come contract renewal time.

As a result, we think pipeline securities are very attractive. The AMLP ETF itself pays a dividend yield to investors of more than 7% annually, so income investors should definitely take note. We think that the disconnect between the stock prices of energy broadly and of the pipelines could narrow over the coming months and years, suggesting an opportunity for capital appreciation, as well. Some individual components of the index, like Magellan Midstream Partners, L.P. (MMP; dividend yield 8.45%) and Energy Transfer LP (ET; dividend yield 7.98%), carry even higher dividends than the overall index, so there are many ways to play the theme here.

Speaking of other ways to play the theme, we also like bonds in the space, should you want a more fixed return structure to your investment in pipelines. One such bond comes from Enbridge Energy Partners, LP (ENB), another pipeline operator. The Enbridge 6.3% 2034 bond trades at a slight premium to par, but carries a BBB investment grade credit rating and implies an average annual yield of 6.15%. We think there are ample ways to play the theme of investing in pipeline companies, which consistently deliver steady cash flows.

Takeaways from this Week

The inflation and interest rate theme continues to grip the narrative across investment markets of all types. There are certainly areas that investors should avoid, particularly growth stocks that still carry high valuations. However, lower prices do mean opportunity in some circles, especially for investors holding cash in the bank and still earning very little interest in those accounts.

We think investors should still be digging deep to find individual bonds and other income securities which now carry impressive income yields at current prices. Two such examples are Starwood Property bonds, as well as both the stocks and the bonds associated with the oil/gas pipeline industry.

Be the first to comment