Natali_Mis

There are a number of bargains in the office REIT space at the moment, and some better suited for certain investors than others. For those with more risk appetite and seeking a higher yield, REITs such as SL Green Realty (SLG) may be fitting, while those who prefer a stronger balance sheet may want to buy lower-yielding Boston Properties (BXP).

This brings me to Highwoods Properties (NYSE:HIW), which yields in-between the aforementioned REITs while checking off a lot of boxes for investors. As shown below, HIW currently trades far below its 52-week high of $47, and offers investors an appealing 7.3% yield. This article highlights why HIW may be an ideal high yielding pick for income investors.

HIW Stock (Seeking Alpha)

Why HIW?

Highwoods Properties is a self-managed REIT and a member of the S&P MidCap 400 Index. It acquires and develops high quality office properties in what it calls BBDs or better business districts in the growing Southeastern and Mid-Atlantic regions of the U.S., including Atlanta, Charlotte, Dallas, and Nashville, among others.

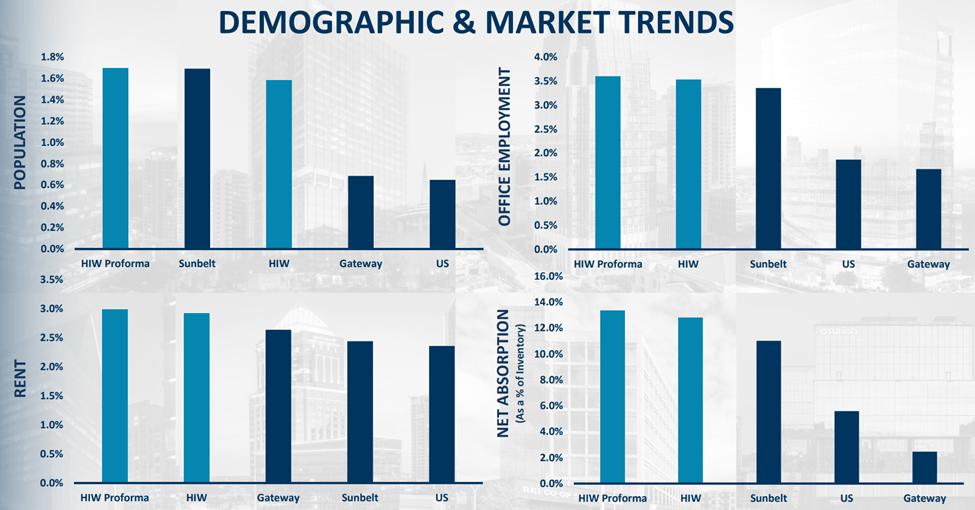

This strategy has worked well for HIW, as its participation in vibrant cities that are otherwise known as second tier markets results in less competition for deals from the big players. Contrary to what some may believe, HIW’s markets actually have more attractive demographic trends than gateway markets.

HIW’s markets are seeing higher population growth (annualized over the past decade) and a higher office employment rate than the overall Sunbelt and Gateway markets. This has translated to faster rent growth and a higher net absorption rate for HIW, as shown below.

HIW Demographic Trends (Investor Presentation)

Meanwhile, HIW is performing rather well, with impressive GAAP rent growth of 13.4% during the third quarter on newly executed leases, covering 1.0 million square feet of renewal and new tenant leases, signaling strong demand for its properties.

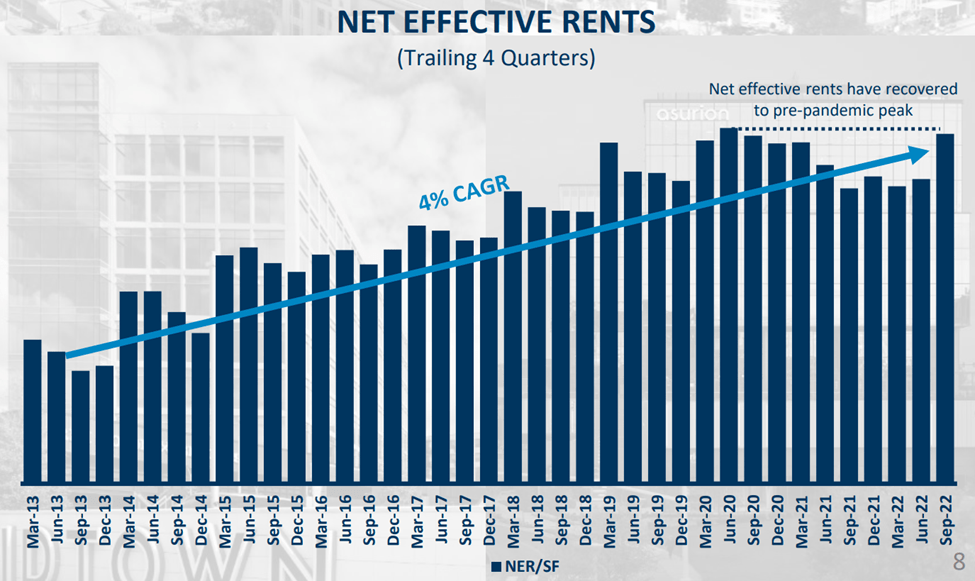

Moreover, HIW carries a long-weighted average remaining lease term of 7.4 years, and substantially backfilled its largest 2023 lease expiration ahead of time. Also encouraging, it appears that period of rent concessions is about over, as the portfolio net effective rents have recovered to their pre-pandemic peak achieved in June of 2020. As shown below, this translates to a respectable 4% CAGR over the past decade.

HIW NER Growth (Investor Presentation)

Looking forward, management anticipates a healthy 91.5% occupancy rate by the end of this year, and HIW is well-positioned financially, with a safe net debt to EBITDAre ratio of 5.6x and a BBB credit rating from S&P. It also maintains ample liquidity, including $640 million in availability on its revolving credit facility, to fund its development pipeline.

Risks to HIW include headline generating concerns around return to office in remote-work friendly environment. However, many CEOs are encouraging workers to return to the office, and I believe the future of work will lie somewhere in the middle with a hybrid arrangement. Moreover, HIW has the advantage of a large land bank, and is developing mixed use real estate that caters to retail, residential, and hotel. Management highlighted its projects related to mixed use during the recent conference call:

We also sold a mixed-use land parcel in Richmond, in our Innsbrook BBD for $23 million, recognizing a $9 million FFO gain. This sale will facilitate the development of retail, residential and hotel uses adjacent to our 1.6 million square feet in Innsbrook. Importantly, the value of our existing and future office will be significantly enhanced by a growing amenity base. As we have mentioned previously, our land bank has never been more attractive with full build-out of nearly $4 billion.

The vast majority of this is master planned for mixed-use development, including office and is adjacent to existing or future Highwoods assets. We announced a 100% leased boutique office building at Morrocroft in Charlotte’s’ South Park BBD. Our team creatively manufactured this opportunity to build a $12 million high quality project on a surface parking lot that had previously not been considered for development.

Importantly, HIW’s dividend is very well covered by a 48% payout ratio, based on Q3 FFO per share of $1.04. HIW also has a long track record of paying an uninterrupted dividend since 2004, and while it didn’t raise the dividend this year, I see potential for a raise next year considering its strong operating fundamentals.

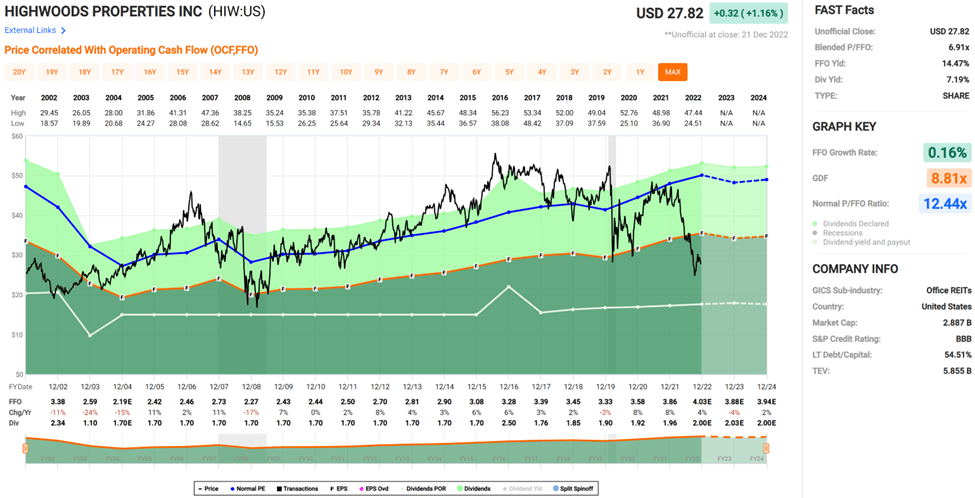

Lastly, I find HIW to be rather cheap at the current price of $27.82 with a forward P/FFO of just 6.9, sitting far below its normal P/FFO of 12.4. Analysts have a consensus Buy rating and HIW could produce strong double digit total returns even with their conservative average price target of $31.50, which calculates to a P/FFO of just 7.9.

HIW Valuation (FAST Graphs)

Investor Takeaway

Highwoods Properties is a strong office REIT with healthy and growing operational metrics. It has a strong balance sheet which supports its development pipeline, including mixed use real estate across its sizeable land bank. Lastly, HIW pays an attractively high dividend that’s well covered by a low payout ratio. As such, I find HIW’s current low valuation and high yield to be an appealing option for income investors.

Be the first to comment