DNY59/iStock via Getty Images

Author’s note: This article was released to CEF/ETF Income Laboratory members on December 12th.

Interest rate hikes have led to higher bond yields, but lower bond prices. Short-term bond funds tend to see above-average dividend growth when rates rise, as these funds can quickly replace their older, lower-yielding bonds for newer, higher-yielding alternatives. Short-term bond funds tend to see below-average capital losses / reductions in their share price when rates rise, for the same reasons. As such, short-term bond funds are a particularly compelling investment opportunity when interest rates are rising, as they currently are.

I’ve covered many of these funds in the recent past, including those focused on high-yield corporate bonds, investment-grade corporate bonds, and T-bills. In keeping with my coverage on short-term bond funds, thought to write a piece on the SPDR Barclays Capital Short Term High Yield Bond ETF (NYSEARCA:SJNK).

SJNK is a simple short-term high-yield bond index ETF. SJNK offers investors an above-average, growing 5.8% dividend yield, has relatively low interest rate risk, and is a buy. On the other hand, SJNK has relatively high credit risk, and so might not be appropiate for the most conservative investors.

SJNK – Basics

- Investment Manager: State Street

- Underlying Index: Bloomberg US High Yield 350mn Cash Pay 0-5 Yr 2% Capped Index

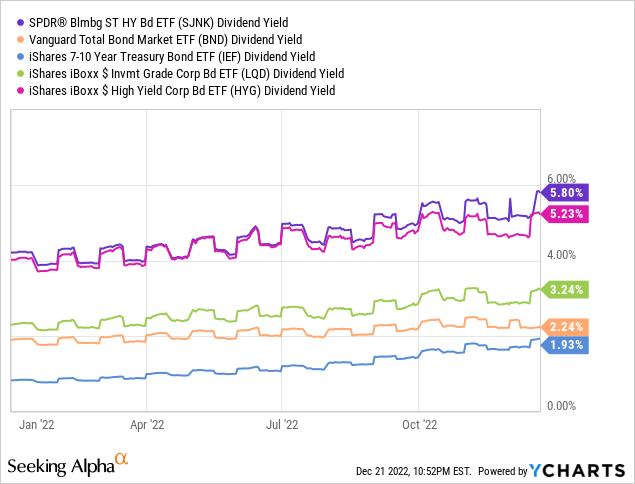

- Dividend Yield: 5.83%

- Expense Ratio: 0.40%

- Total Returns CAGR 10Y: 3.21%

SJNK – Overview

SJNK is a simple short-term high-yield bond index ETF, tracking the Bloomberg US High Yield 350mn Cash Pay 0-5 Yr 2% Capped Index. It is a simple, albeit wordy, index, including all dollar-denominated, short-term, high-yield corporate bonds meeting a basic set of inclusion criteria. It is a market-value weighted fund, with 2% issuer caps meant to ensure diversification. I’ve seen no significant issues with the fund’s underlying index.

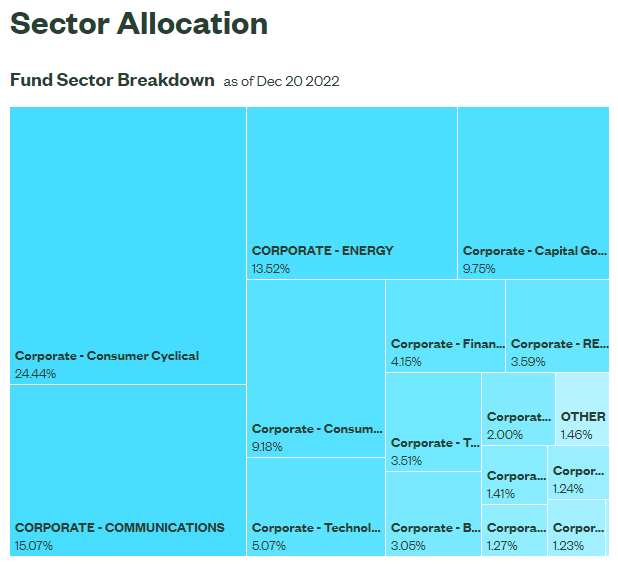

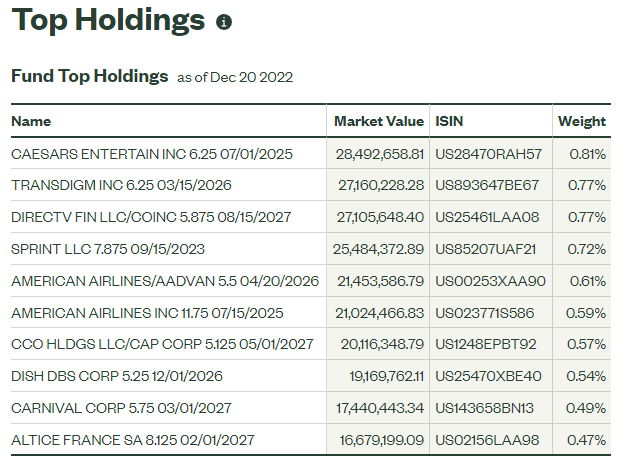

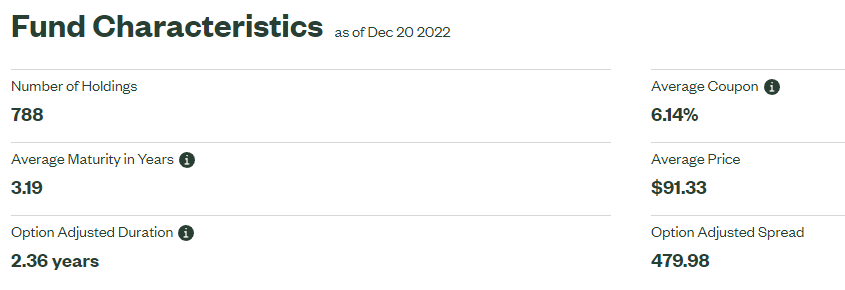

SJNK is a reasonably well-diversified fund, with investments in over 700 different bonds, and with exposure to most relevant industry segments. Concentration is incredibly low, with the fund’s top ten holdings accounting for just 6% of its value. Issuer concentration is marginally higher, as the fund sometimes invests in more than one security per issuer, but remains low, due to the aforementioned issuer cap.

SJNK

SJNK

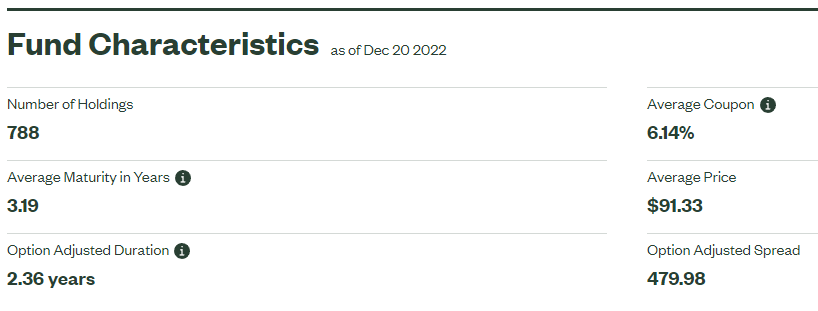

SJNK is a short-term bond fund, with an average maturity of just 3.3 years. For reference, most bond funds have average maturities of +7.0 years, most high-yield corporate bond funds of +5.0 years.

SJNK

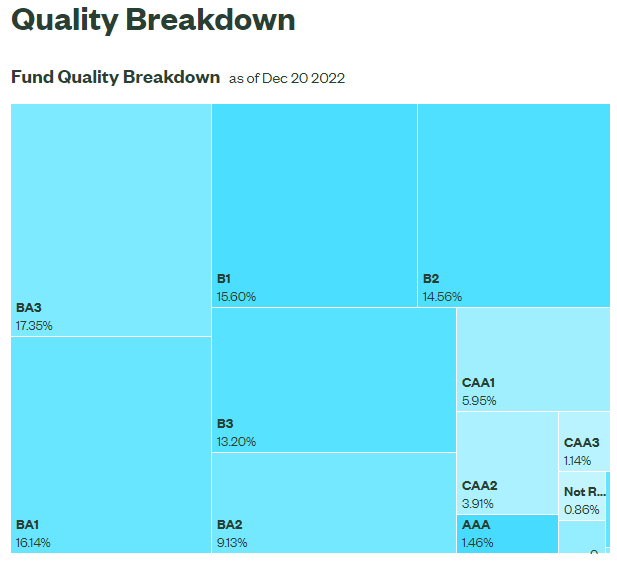

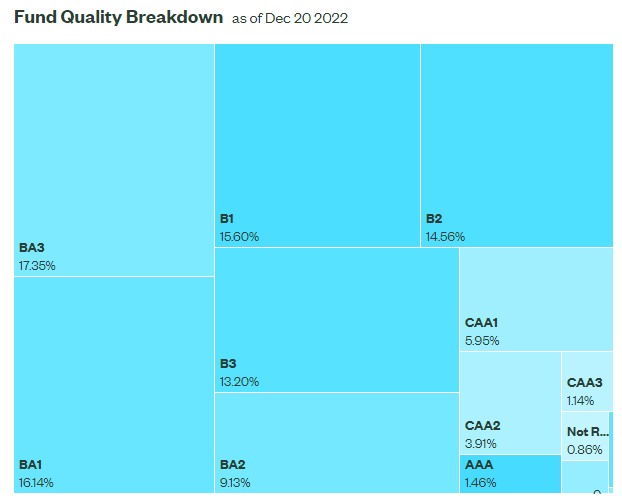

SJNK is a high-yield bond fund, focusing on securities with relatively low credit ratings. The fund sports an average credit rating of BA, according to Moody’s, equivalent to BB in the more well-known S&P credit rubric.

SJNK

In short, SJNK is a simple short-term high-yield corporate bond index ETF, with the portfolio and characteristics one would expect from such a fund. With this in mind, let’s have a look at the fund’s positives and negatives, starting with the positives.

SJNK – Benefits

Strong, Growing 5.8% Dividend Yield

SJNK focuses on high-yield bonds which, almost by definition, sport strong, above-average dividend yields. SJNK itself yields 5.8%, a reasonably good yield, significantly higher than average relative to most bond funds, and slightly higher than average for a high-yield bond fund.

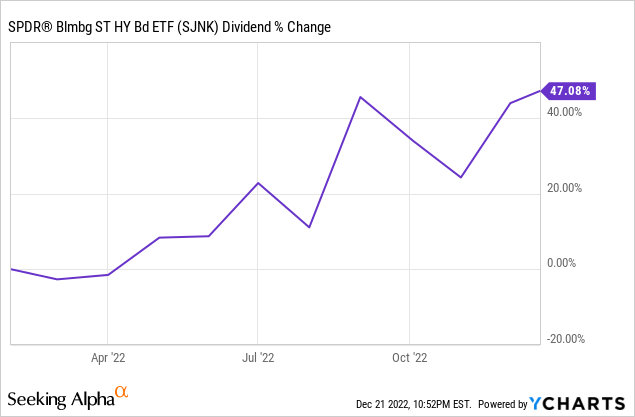

SJNK’s dividends are quite strong, and they have seen very healthy growth YTD, skyrocketing by almost 50% during the same.

Growth is set to continue, as recent interest rate hikes continue to be felt across the economy and investment markets. SJNK’s dividends should grow until the fund’s yield reaches around 8.5%, equivalent to the fund’s SEC yield, a measure of its underlying generation of income. Growth could be even stronger than expected, contingent on future interest rate hikes, which are a distinct possibility.

Importantly SJNK’s dividend growth should be stronger than average, due to the fund focusing on short-term bonds. In simple terms, SJNK’s underlying holdings have an average maturity of 3.2 years, which means it takes the fund an average of 3.2 years to replace an existing, low-yielding holding for a newer, higher-yielding alternative. Most bond funds focus on securities with much higher maturities, and so take much longer in replacing their portfolios to benefit from higher interest rates.

SJNK’s strong, growing 5.8% dividend yield is a benefit for the fund and its shareholders.

Low Interest Rate Risk

SJNK focuses on short-term bonds, which almost always have below-average interest rate risk. The reasons for this are quite technical, but can be summarized thus.

When interest rates increase, newer bonds see increased interest rates, but older bonds maintain their original, lower rate of interest. When interest rates increase, investors tend to sell their older, lower-yielding bonds to buy newer, higher-yielding alternatives. The impact tends to be much more pronounced for long-term bonds, as no one wants to be stuck with a low-yield security for years on end. The impact tends to be much less pronounced for short-term bonds, as these mature relatively quickly, and so investors are only stuck with a low-yield security for a short amount of time.

SJNK focuses on short-term bonds, with relatively low interest rate risk, as evidenced by the fund’s low 2.4 duration (which directly measures interest rate risk). For reference, most bond funds have durations of +5.0 years, most high-yield corporate durations of +4.0 years.

SJNK

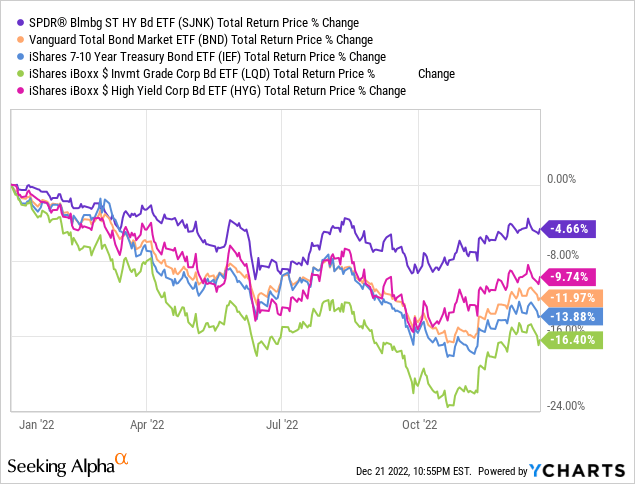

SJNK has relatively low interest rate risk, which means the fund should suffer comparatively low losses when interest rates increase. This has been the case YTD, as expected.

SJNK’s low interest rate risk leads to outperformance when interest rates increase, an important benefit for the fund and its shareholders.

As an aside, SJNK’s low interest rate risk cuts both ways: the fund outperforms when rates rise, but also underperforms when rates decrease. Due to this, investors should expect relatively meager gains and underperformance if inflation normalizes relatively quickly, and if the Federal Reserve pivots from its current policy stand.

SJNK – Downsides

High Credit Risk

SJNK focuses on high-yield bonds, with above-average interest rates. Although these securities provide a lot of income to the fund and dividends to shareholders, credit risk is relatively high too. As previously mentioned, the fund’s underlying holdings sport an average credit rating of BA / BB.

SJNK

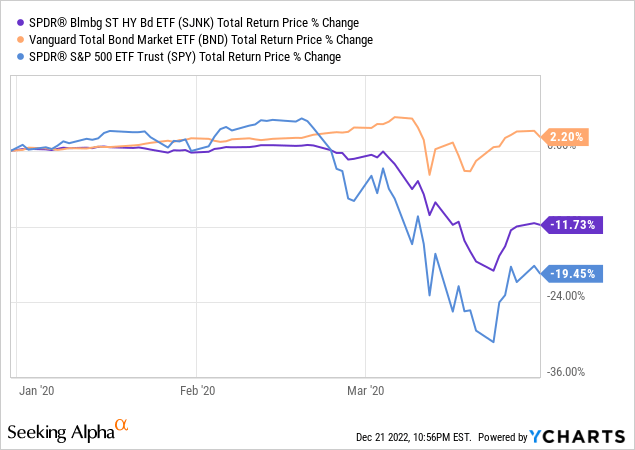

As evidenced above, SJNK’s underlying holdings have an above-average, although not excessive, level of credit risk. In most circumstances, the vast majority of the fund’s bonds are paid on time, and are not at risk of default. When economic conditions worsen, some of their issuers might run into financial trouble, and have difficulties meeting their financial obligations. Some will undoubtedly default, meaning higher default rates and lower bond market prices. Expect moderate losses and underperformance when this occurs, as was the case during 1Q2020, the onset of the coronavirus pandemic. Losses were between those of broader bond indexes and equity indexes.

SJNK has relatively high credit risk, an important negative for the fund and its shareholders. In my opinion, risk is reasonable, definitely not excessive nor a deal-breaker. On the other hand, credit risk is sizable enough that more conservative, risk-averse investors might disagree. Short-term bond funds focusing on less risky securities, including the SPDR Bloomberg Barclays 1-3 Month T-Bill ETF (BIL) and the PIMCO Enhanced Short Maturity Active Exchange-Traded Fund (MINT), might be more interesting choices for some of these investors. I last covered BIL here, MINT here.

Conclusion

SJNK offers investors a strong, growing 5.8% dividend yield, has relatively low interest rate risk, and is a buy.

Be the first to comment