deeltijdgod

Hess Corporation (NYSE:HES) is a large and global independent energy company with market capitalization of more than $40 billion. The company has a 30% stake in the massive Guyana oil field and substantial oil assets elsewhere. As we’ll see throughout this article, Hess Corporation has a unique ability to drive substantial shareholder returns.

Hess Corporation’s Unique Portfolio

Hess Corporation has a unique and well-distributed portfolio of assets that’ll enable continued shareholder returns.

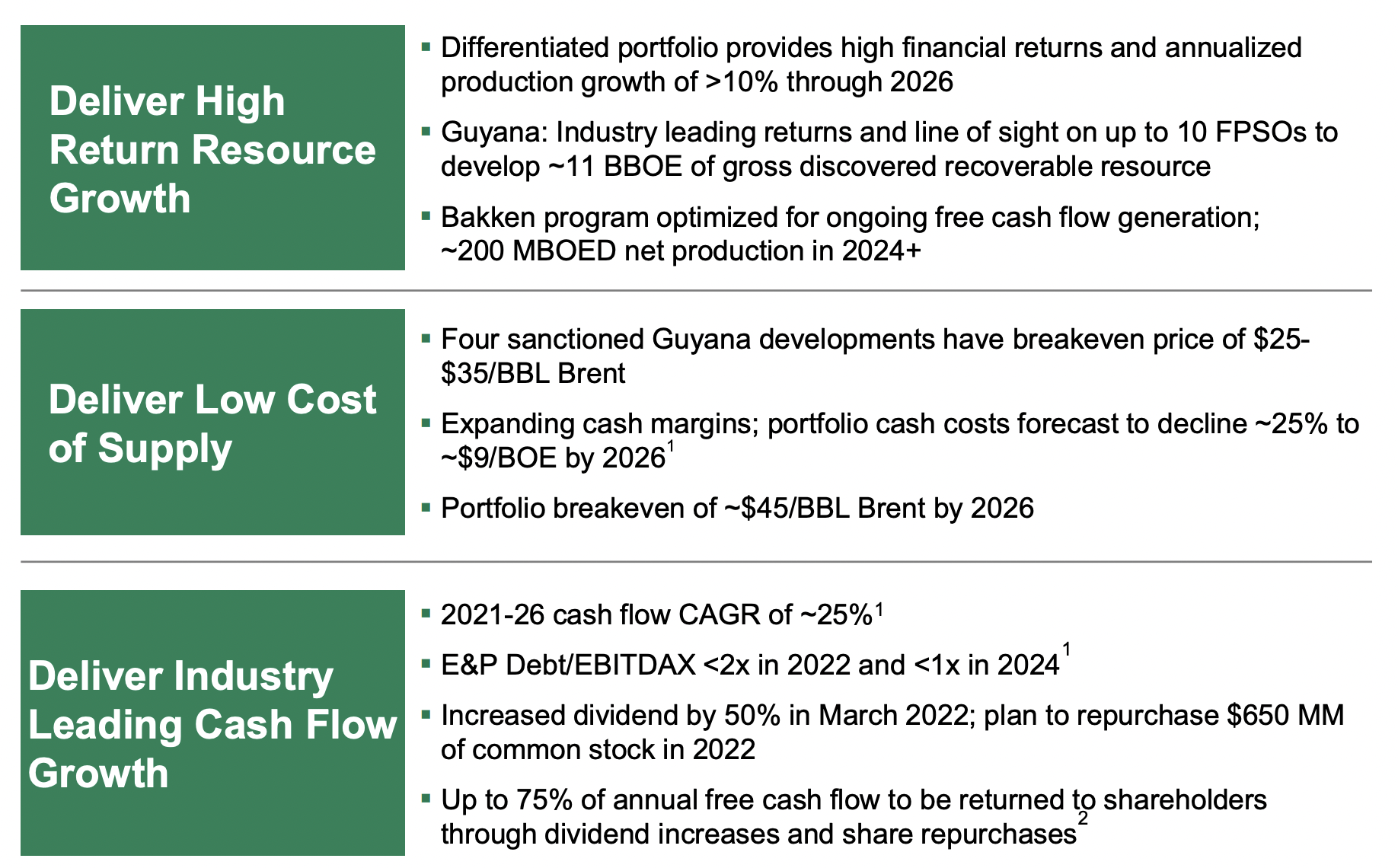

Hess Corporation Investor Presentation

The company has a unique and differentiated portfolio. It expects annual production growth in the double-digits through 2026, although given the strength and continued discoveries in Guyana, we expect production to continue past that point. The company expects production to hit >2 million barrels/day with 10 FPSOs for ~11 billion barrels of resources.

The company’s Bakken program is continuing to generate strong FCF, with 2024+ production at 200 thousand barrels/day. The company’s Guyana developments so far have a breakeven price of $30/barrel Brent, meaning cash costs are expected to continue declining. Portfolio breakeven is expected to hit ~$45/barrel in 2026 meaning a very profitable company.

From 2021-2026, the company expects 25% FCF growth with lowering E&P Debt. The company is continuing to increase its dividend and focus on share repurchases; however, even with these two things, annual shareholder returns are <3%. The company does expect to grow the annual FCF to be returned to shareholders.

Hess Corporation’s Financial Strength

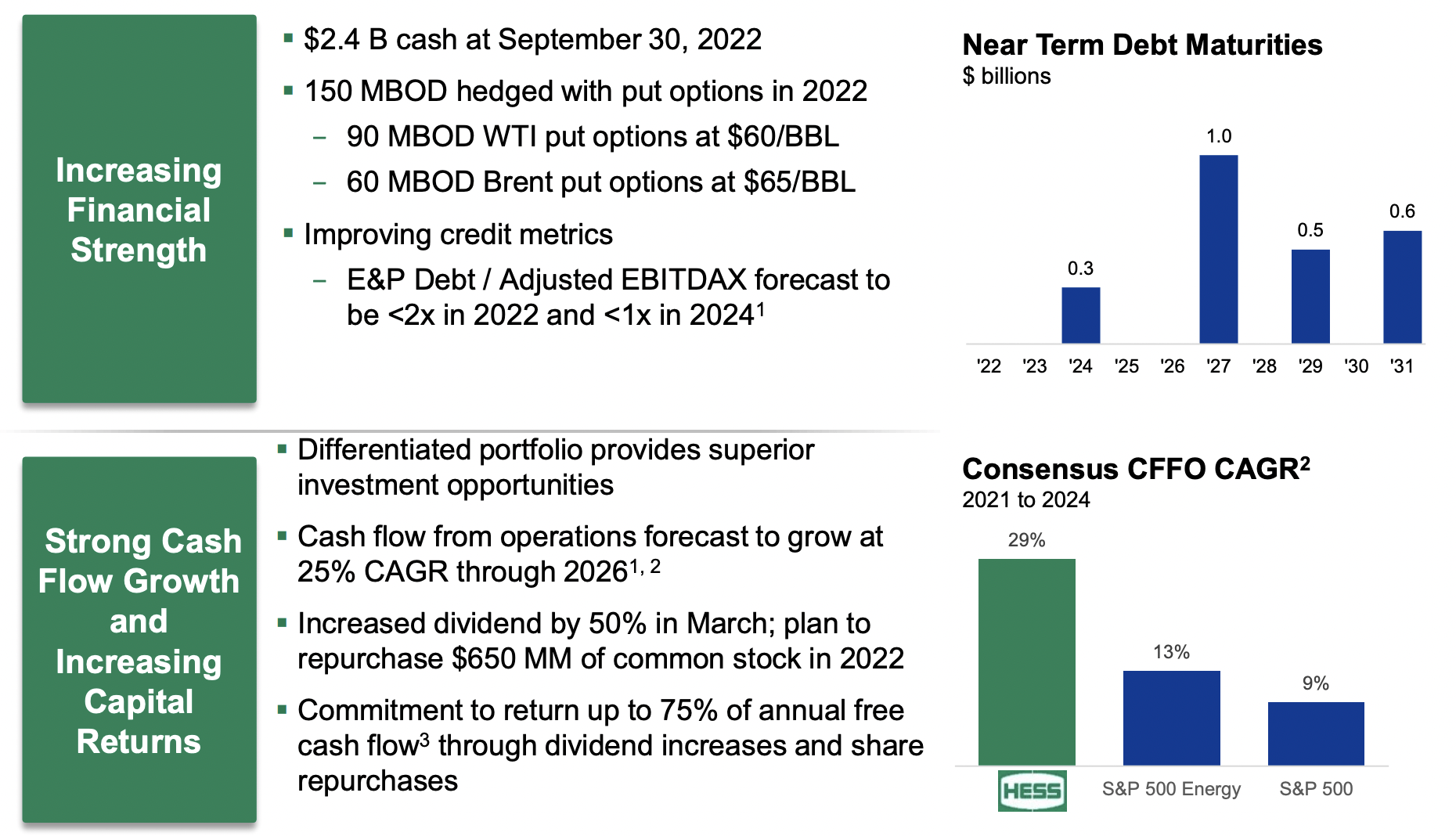

Hess Corporation has the financial strength to manage any maturities and focus on shareholder returns.

Hess Corporation Investor Presentation

The company has a relatively strong financial position, meaning it’s not entering its cash flow period with substantial debt. The company has $2.4 billion in debt due until the early-2030s and $2.4 billion in cash, enough to exactly match it. Paying down debt can help save on interest expenses, although the company’s current expenses are modest.

We expect the company’s debt to remain incredibly manageable.

Hess Corporation’s Financials

Hess Corporation is working on aggressively improving its financial position, and the 2020s will be a time of strong transformation for the company.

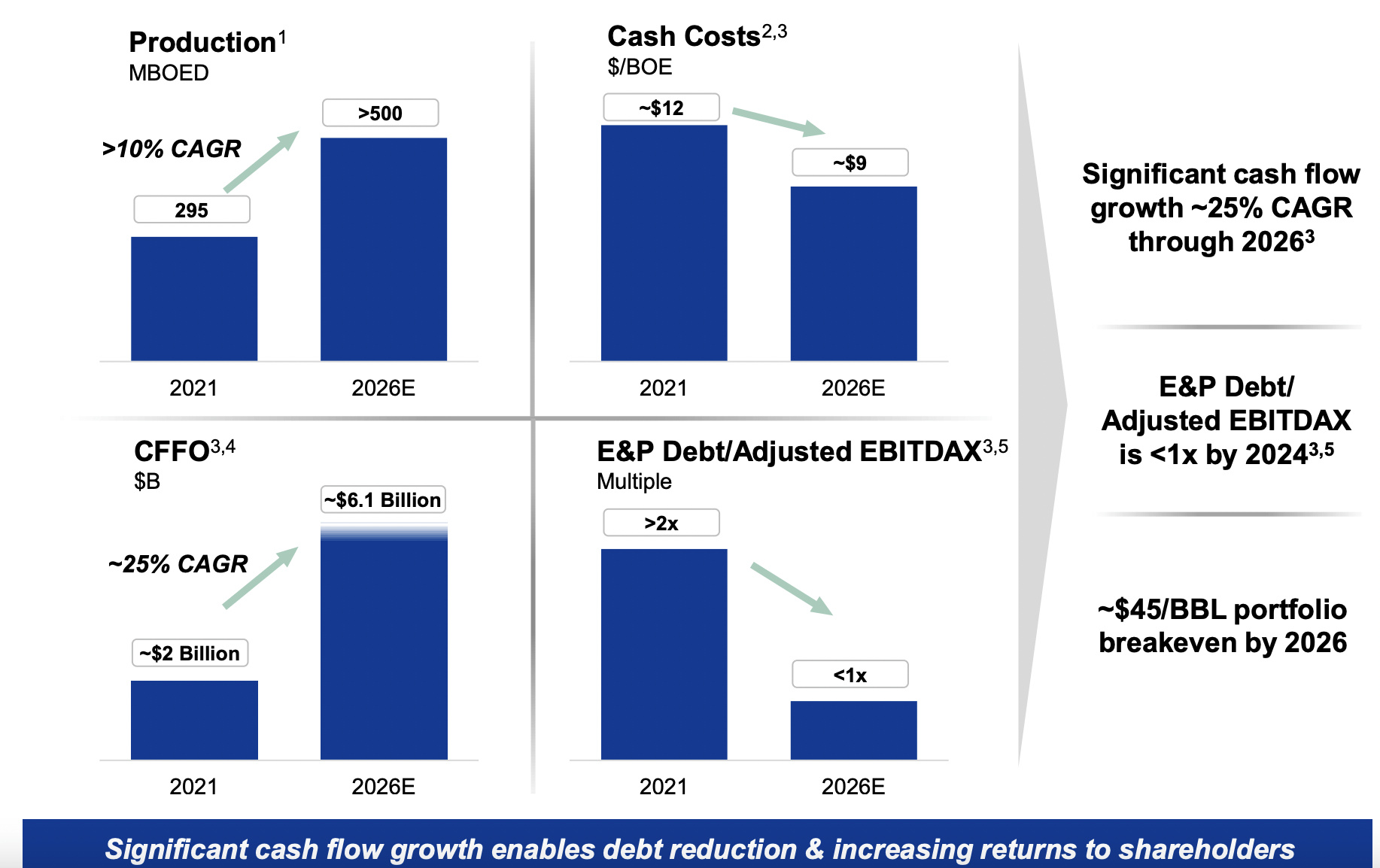

Hess Corporation Investor Presentation

The company’s guidance is above. Production is expected to grow to more than 500 thousand barrels/day by 2026 of which roughly half will be from Guyana. CFFO is expected to grow to more than $6 billion as cash costs and the company’s debt multiples drop, mainly driven by its continued cash flow increases.

We expect capital spending to sit at roughly $2 billion annualized, implying $4 billion in 2026E FCF or a 10% FCF yield. That’s solid, but nothing special to hit several years from now, and as a result, relies on continued growth past 2026E in the company’s portfolio. Fortunately, the company has a strong ability to execute in Guyana.

Hess Corporation’s Shareholder Returns

Putting all of this together, we expect Hess Corporation to be able to generate substantial shareholder returns.

Hess Corporation Investor Presentation

The company’s current dividend is just a hair over 1%. The company is looking to grow that over the dividends past 2% by 2026 and then also spend ~4-5% of cash on share repurchases. Continued share repurchases can enable the company to grow long-term shareholder returns faster. Earlier share repurchases will accelerate this.

The takeaway here is that the company has strong potential with 2026E FCF of 10%.

Thesis Risk

The largest risk to our thesis is that Hess Corporation is trading at a fairly lofty valuation with a 7% FCF yield in 2026. That’s at $65/barrel Brent, so it will outperform when prices are higher. However, if prices are below that level or lower, we expect the company to underperform, which will hurt its ability to continue shareholder returns.

Conclusion

Hess Corporation is an expensive company. The company is currently trading at a 10% estimated 2026 FCF yield, which continued cash flow growth expected between now and that time. The company is planning to invest that cash into both dividends and share repurchases, with earlier investments potentially helping increased returns.

However, despite the company’s valuation, we still see some potential from continued high-margin production growth. Specifically in Guyana, where production attributable to the company can comfortably hit hundreds of thousands of barrels a day. Putting this all together, we see the company as a valuable asset that can drive substantial returns.

Be the first to comment