Jack Taylor/Getty Images News

Thesis

In a challenging macroeconomic environment, in 2022, the consumer discretionary sector recorded large declines, with even large and mega-caps marking significant losses. Hasbro (NASDAQ:HAS) represents a mature, well-known among consumers company in the toy and games industry that has seen a large stock price decline over the past year.

In this analysis, I explore whether the recent large stock price decline presents an attractive investment opportunity or an indication that Hasbro’s future might present serious challenges for the company.

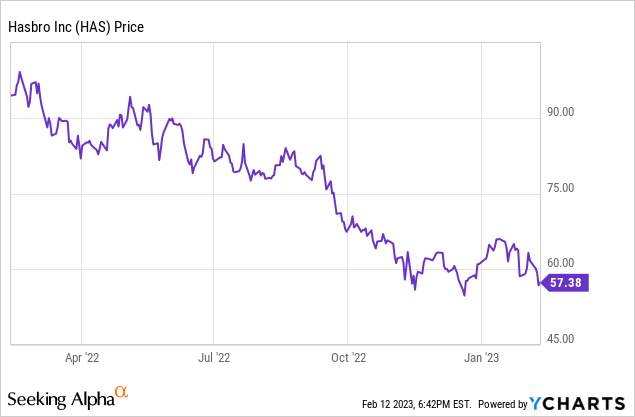

In the midst of inflationary pressures and deteriorating consumer sentiment, Hasbro has seen a steep stock price decline. For the trailing 12 months, the stock has retreated almost -40%. Hasbro is, currently, trading at $57.38 ($7.92B market cap), near its 52-week lows of $54.65 and pays a 4.88% dividend yield.

The Business

Hasbro is a global toy and board game manufacturer, that develops, designs and sells a wide range of toys, including board-games, action figures and collectibles for children and families. The company is well-known to consumers through a diverse range of brands like Monopoly, Play-Doh, Nerf and others.

Hasbro’s business model and revenue streams are primarily business-to-consumer focused, as the company generates the majority of its revenue through retail sales in large chain stores, specialty stores and e-commerce. A smaller portion of its sales can be attributed to licensing agreements for the use of its brands’ intellectual property as well.

The Toy Industry

It is no secret that kids’ entertainment revolves more and more around electronic devices and video games. However, the toy industry still exhibits some decent, yet slowing, growth prospects for the foreseeable future. Toys and board games are unlike to be phased out by video games, as they remain very popular with younger kids and families looking for inclusive entertainment and interaction. Hasbro is among the top four names in the industry, that also include Lego, Bandai Namco and Mattel.

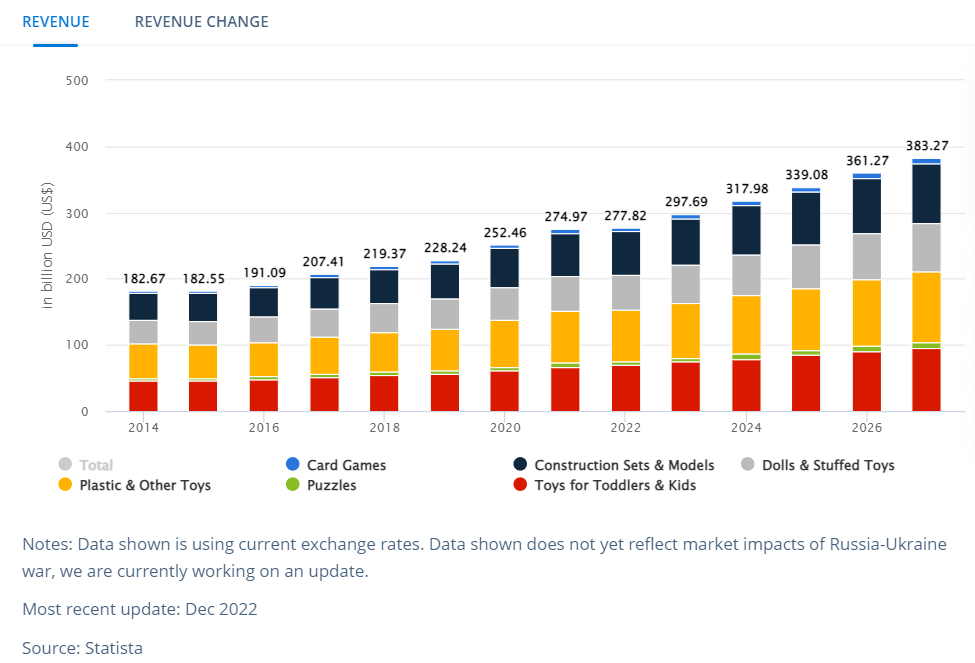

The toys’ and games industry has grown from $183B in 2014 to $275B at the end of 2021. Through 2027, the industry is expected to grow at a 6.5% CAGR to reach $383B. On a per-person basis, revenues of $38.76 were generated in 2023. Around 25% of sales are generated online, compared to 19% in 2017. In 2025, 30% of sales in the industry are expected to originate online.

Statista

Financial Performance

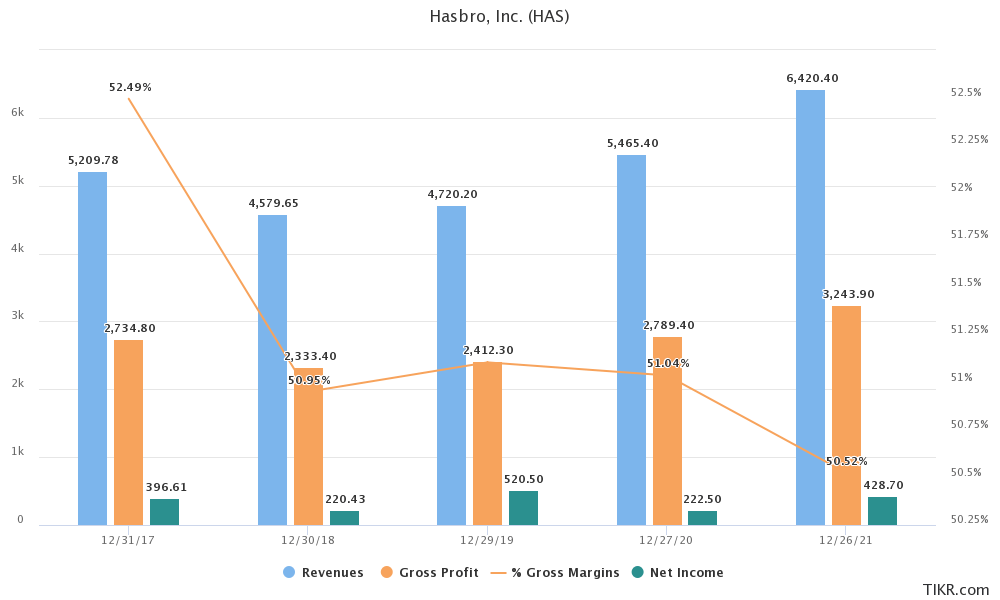

Hasbro’s growth strategy revolves around both organic expansion and acquisitions of smaller, up-and-coming toy brands. Over the past decade, revenue growth has been rather underwhelming, with sales increasing by a CAGR of 4.12% for the trailing 10-year period and 3.38% for the trailing 5-year. While it is clear that the company is struggling to substantially grow its sales, underperforming growth in the toy industry, it is important to note that both Hasbro and the toy industry in general, are mature and exhibit very mild growth characteristics. Gross and Net profits also follow a similar trajectory.

Hasbro exhibits strong cash flow productivity, generating over 800M of Cash from Operations in 2021. Free Cash Flow surpasses net income, offering a sign of efficiency and financial health for the company. Free Cash Flow production has also been consistent over the past decade.

On the other hand, Hasbro displays relatively strong profitability margins. The company’s gross margin, of 48.9%, has decreased somewhat from previous years, yet it still remains significantly higher than sector and market averages. The same is true for an EBITDA margin of 16.4%, while the net margin of 6.5% should, ideally, expand.

Tikr.com

Even though for 2022, analysts expect EPS to contract by around -14%, for 2023 and 2024 moderate growth around 10% is forecasted. When it comes to revenue, Hasbro is expected to generate $5.92B in 2022 with single-digit growth thereafter.

Hasbro maintains a $3.7B long-term debt balance (almost 50% of market cap) that indicates relatively high leverage. Besides raising long-term risk, increased debt levels negatively affect bottom-line profitability as interest payments increase. A current ratio of 1,38 indicates strong liquidity for the company. Hasbro has also built up a $550M cash balance.

Dividend Assessment

Hasbro pays a pretty generous 4.88% dividend yield. The company has also managed to slowly grow its dividend at a 10-year 4.87% CAGR and a 5-year 4.19% CAGR. These growth rates are, however, significantly lower than average rates across the consumer discretionary sector. Many analysts also express some concerns that the current dividend yield might prove unsustainable in the future due to relatively high payout and low coverage ratios (D- dividend safety score from Seeking Alpha). In my view, most indicator values, while somewhat worse than sector averages, are not yet a cause for alarm.

Valuation Attractiveness

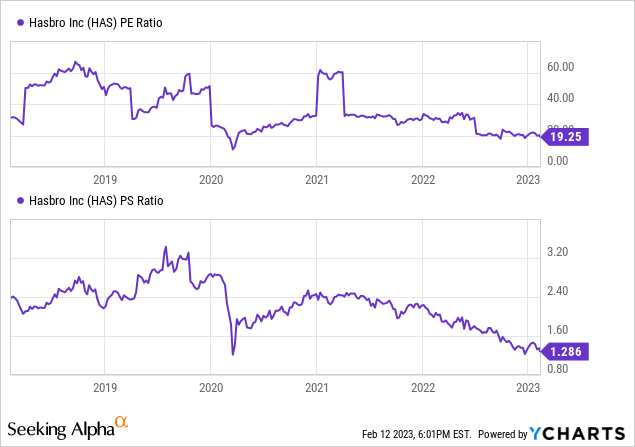

As the stock has seen a large decline in 2022, valuation multiples have contracted across the board. Currently, Hasbro trades at reasonable 19.2x P/E GAAP and 1.2x P/S multiples. Both ratios also stand close to their 5-year lows. On a non-GAAP basis, Hasbro’s FWD P/E stands significantly lower, at 12.8x. If we also consider a 11x EV/EBITDA multiple and a low P/FCF ratio as well, it could be argued that the company offers a somewhat attractive valuation case.

Putting it All Together

After all things are considered, Hasbro offers mixed financial signals as it relates to its attractiveness as an investment. On the negative side, slow growth and relatively high amounts of debt hurt the company’s mid and long-term performance prospects. On the other hand, the company displays good profitability and strong cash flow production, while also trading at a reasonable valuation. Hasbro’s dividend yield is also attractive, though concerns over its sustainability exist. Based on the above, I would currently hold off on buying the stock until a more attractive entry point is established in terms of stock price, in order to attain more secure returns.

Be the first to comment