Jaskaran Kooner

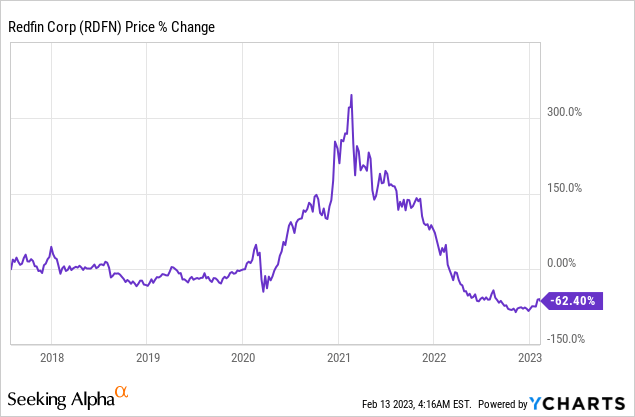

Redfin’s (NASDAQ:RDFN) 73% decline over the last 12 months has been dramatic, usurping the pandemic-era rally and leaving the future of the residential real estate brokerage firm under marked uncertainty. The Seattle, Washington-based company is now trading at a third of its 2017 IPO price level with a 19% short interest attached to its commons and with continued macroeconomic uncertainty providing little reason to think there’ll be some respite in the near term. Is this an opportunity to go bottom fishing for a company whose market cap now sits at $890 million against trailing 12-month revenue of $2.45 billion?

To understand the possible direction of the commons this year you will have to look at the underlying reasons the market has decided to cut down the valuation multiple attached to Redfin. The company’s price-to-sales ratio now sits at 0.36x from over 10x just over two years ago and is around 93% lower than its peer group median.

Freddie Mac

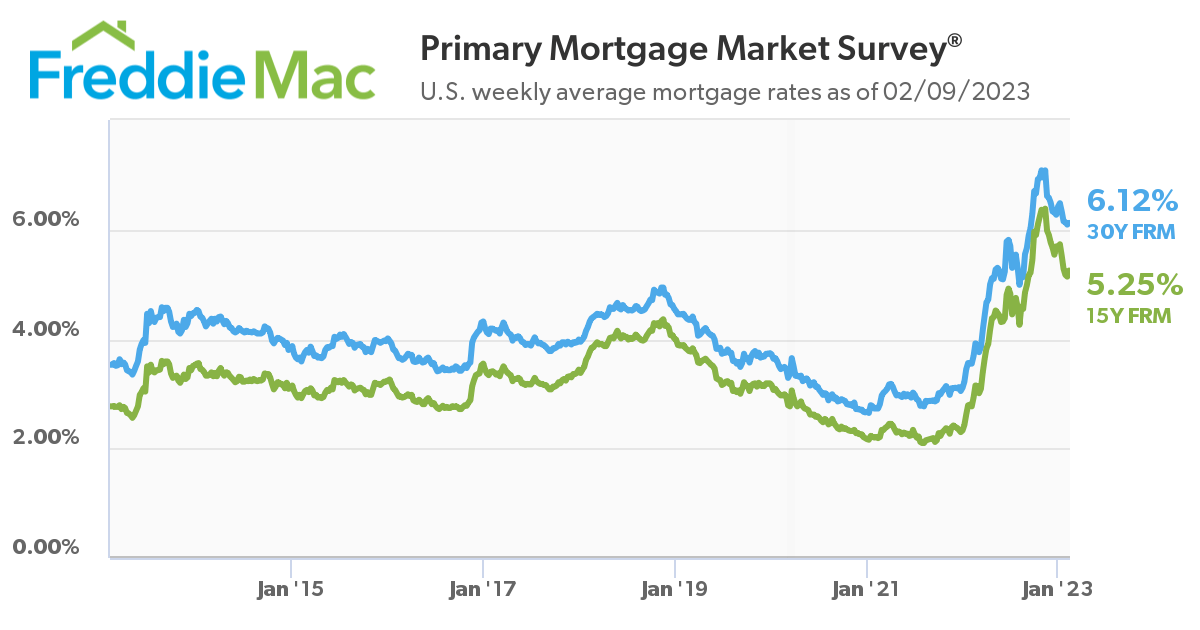

Existing US home sales have declined for 11 consecutive quarters as of December 2022 with demand rapidly cooling on the back of rising Fed funds rates. This has pushed up the 30-year mortgage rate to 6.12%, its highest level since 2008 but down from highs north of 7% in November last year to provide some slack. The situation is critical with total home sales in 2022 at just over 5 million, down 17.8% from 2021.

Revenue Flatlines As Housing Slows

Bankrate

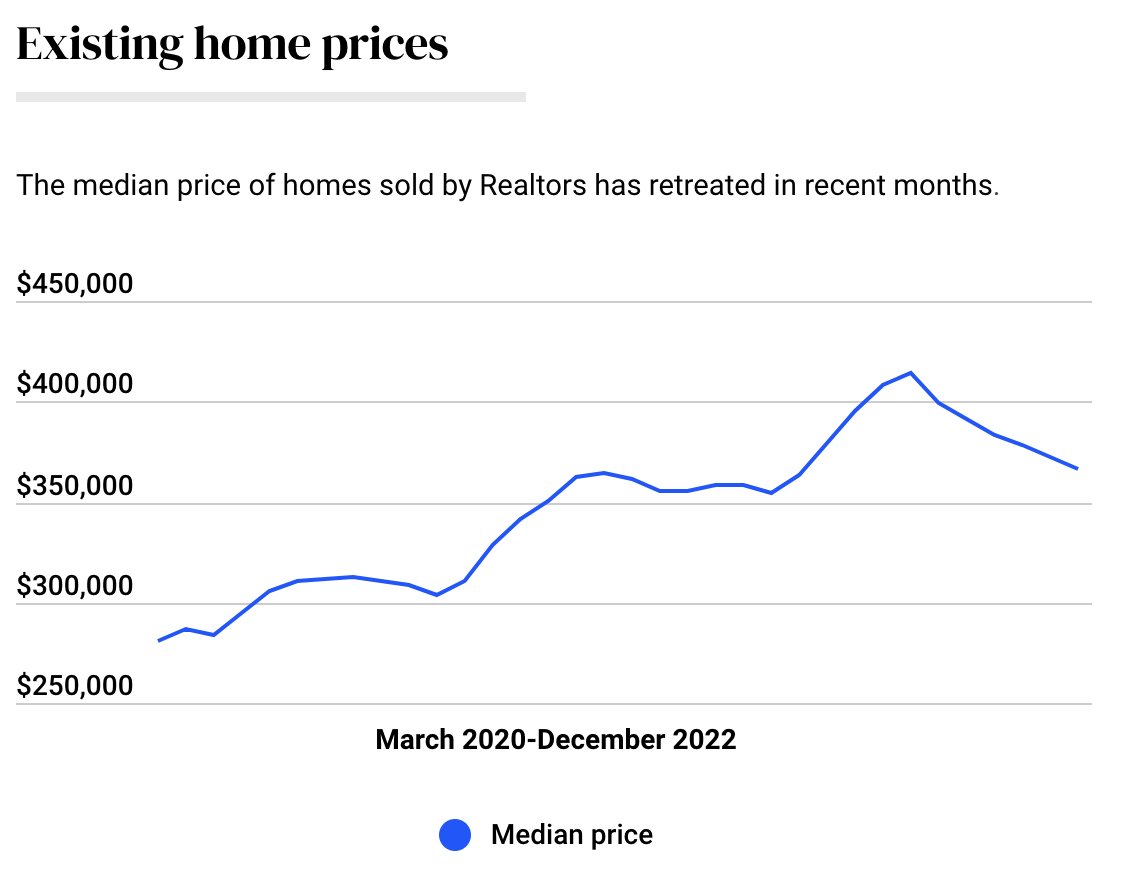

Housing affordability has increasingly become beyond the reach of millions over the last 12 months on the back of a historic cost of living squeeze catalyzed by elevated inflation and rising mortgage rates. The specter of a recession has also worked to rapidly collapse buyer sentiment with existing home prices down 11.3% from their recent peak. Hence, with the Fed funds rate set for at least two further 25 basis point hikes, 2023 could at minimum see a lacklustre operating performance by Redfin as the higher rates work their way through the economy.

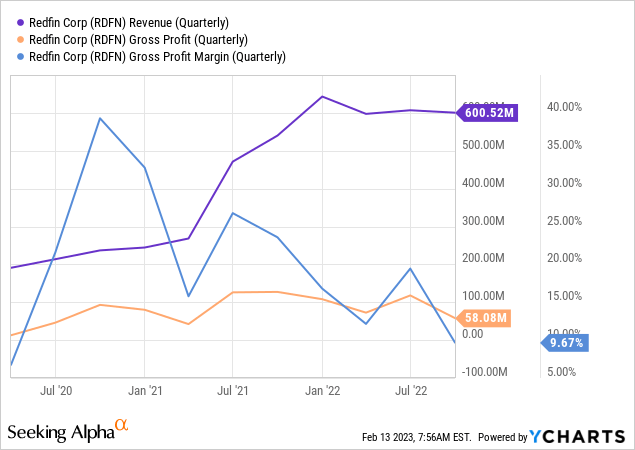

Redfin last reported revenue of $600.5 million for its fiscal 2022 third quarter. This was up 11.2% from the year-ago comp but a miss by $2.15 million on consensus estimates. The company deploys technology to optimize the home buying and selling experience and generates revenue by charging a listing fee for every home sold on its platform.

The company also had an iBuying business, RedfinNow, which it shuttered in November last year. This essentially saw Redfin use its balance sheet to fund the purchase of homes with the aim of selling at a higher price at a future date.

Gross profit during the quarter was $58.08 million on the back of margins that fell sequentially from 19.44% to 9.67%. This was mainly driven by the disposal of RedfinNow’s homes at what management described as lower than expected prices during their earnings call. The company anticipates gross profit from their property segment for the fourth quarter to be negative to push the full-year figure to a loss of between $22 million to $26 million.

Redfin Faces Uncertainty And The Pullback Could Have More Legs

The company is set to announce fiscal 2022 fourth quarter earnings on the 16th of February and has provided forward guidance. Revenue is expected to be between $430 million and $459 million, a huge miss on the consensus of $557.32 million even at the top end. Net loss is expected to not be less than $118 million and would come on the back of a net loss of $90.2 million during the prior third quarter. This was up from a net loss of $18.9 million in the year-ago comp.

The results were poor and could get worse with housing affordability now hovering around its lowest level in 15 years as higher mortgage rates and house prices still at historical records aggregate to set the backdrop for what could be an 18% fall in real estate prices this year. Redfin is taking steps to steer its profitability back to the right path with 862 employees laid off, around 13% of their workforce. Around 264 of these cuts came from RedfinNow. The company anticipates generating positive adjusted EBITDA in 2023 and positive net income in 2024 as a partial result of these cost-saving measures.

These expectations come against cash and equivalents that ended the quarter at $475.8 million, down from $592.4 million in the year-ago period for net debt of $1.28 billion. Total revenue for fiscal 2022 is now set to be around $2.264 billion, down from $2.45 billion in 2021. I think the low multiple is justified against a business model in flux. The financials could decline further if the dreary forecasts for the US housing market in 2023 come true. I’m neutral on the stock but the current deflated price of the commons likely stands to persist through the end of the year.

Be the first to comment