blackdovfx

Investment Summary

After an extensive analysis on Glaukos Corporation (NYSE:GKOS) where we set a target price on its stock at $52 with a hold rating, it has congested sideways and maintained range. Despite broad medical device indices attracting a bid into the new year GKOS has failed to catch the rally. Active investors are generating alpha again and seeking to position against strong profitability and bottom-line fundamentals, a potential headwind for GKOS seeing our comments in the previous note that “[o]perating performance continues to tighten on a sequential basis, particularly below the operating line”. We made a practical assessment of GKOS and subsequently re-rated it a hold [read it here]. Here I’ll share our additional findings on the company underpinning this thesis.

Data: Author’s previous GKOS analysis

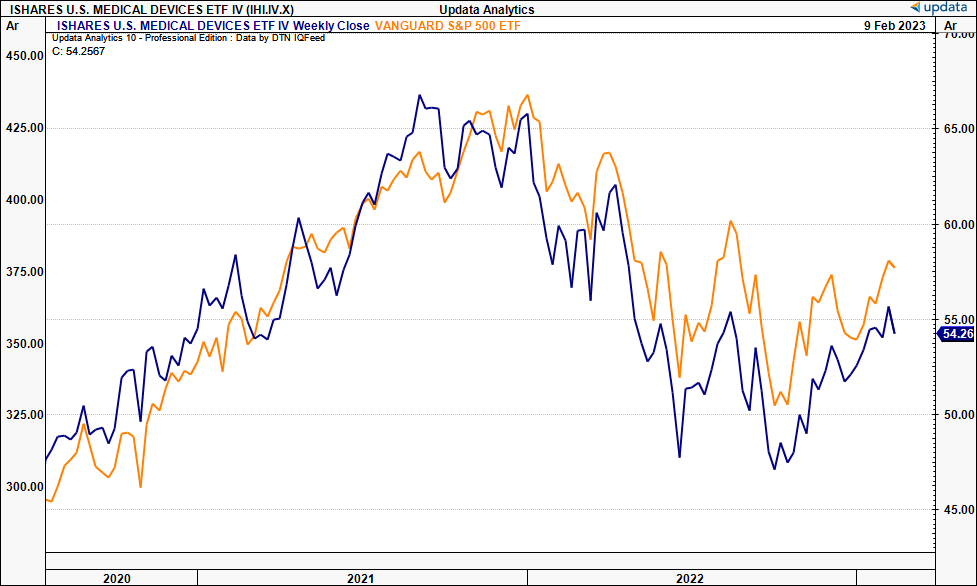

Exhibit 1. Medical Devices vs. benchmark

Data: Updata

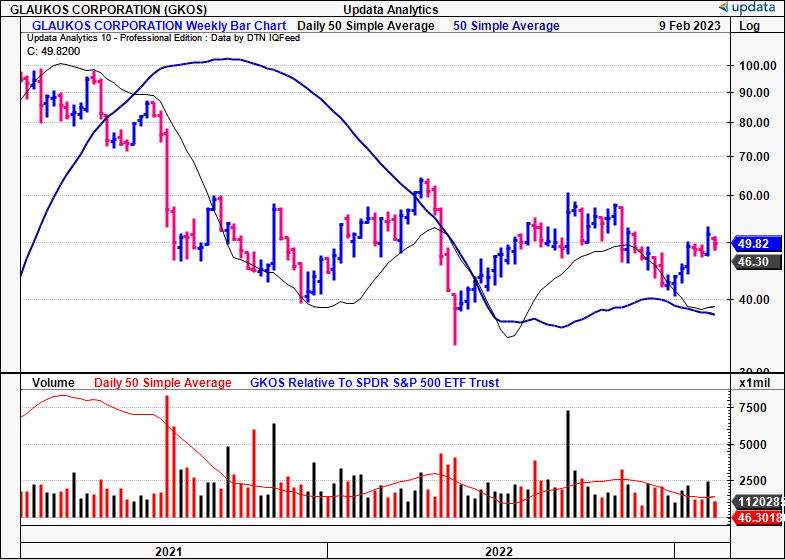

Before proceeding to the analysis, we should recall that it’s been a difficult period for GKOS’ stock price, and that it trades at more than 4x book value, and the book-to-market ratio on this is just 0.22x, suggesting management haven’t created value beyond the company’s book value of equity. Indeed, this is reflected in the price [Exhibit 2], despite clinical trial momentum and growing sales YoY since listing in FY15. Management also noted GKOS to be a $300mm OpEx company [R&D included], supporting our hold thesis via data presented later in this report.

Exhibit 2.

Data: Updata

GKOS recent developments

Indeed, it should be noted GKOS continues building momentum around its Corneal Health pipeline programs. Most recently, this included:

- Initiating the enrolment process for its 2nd pivotal Phase 3 clinical trial for Epioxa. As a reminder, Epioxa [Epi-on] is a transepithelial corneal cross-linking therapy for the management of keratoconus – where the cornea becomes cone-shaped, impacting vision. GKOS expects to include ~290 participants in the cohort, aiming to complete enrolment by this year.

- Subsequent to the above point, the FDA confirmed results of the company’s first Phase 3 trial, that met its primary endpoint, is sufficient to support the submission and review of a new drug application (“NDA”), along with the data from this 2nd trial.

- In addition to its keratoconus progress in the development of Epioxa, GKOS is gaining ground in its Photrexa [Epi-off] segment. We’d allude to investors Photrexa is the only FDA-approved treatment proven to slow and halt the progression of keratoconus.

- It announced top-line results from its Phase 2a clinical trial for GLK-301, a sterile ophthalmic topical cream for the treatment of signs and symptoms of Dry Eye Disease (“DED”). GLK-301 is part of the company’s iLution platform – patented cream-based formulations, versus eyedrops. It enrolled participants [n=218] across the U.S. and evaluated 3 dosage levels of GLK-301 administered bi-daily. Findings indicated improvement in the quality of tear film, measured by tear break-up time, and corresponding improvement in visual quality. This leads GKOS to plan a Phase 2b trial to commence this year.

Deeper look at fundamentals

In the current economic climate, profitability is a standout and able to generate shareholder value. With respect to an ‘earnings recession’, talked of by many, profitable names offer earnings resilience and propensity to maintain an upward growth route. Speaking of GKOS’ growth equivalent, it aims to continue its R&D investment, and capitalize on “big ideas” [Exhibit 3].

Exhibit 3.

Data: GKOS Investor Presentation

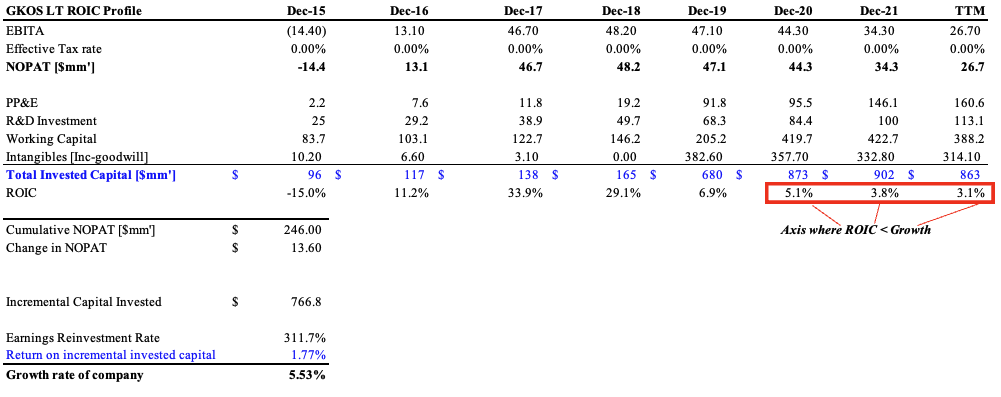

We unpacked GKOS and reformulated the accounting numbers to reflect a more accurate picture of its economics. Chiefly, capitalizing R&D as an investment to restate OpEx and operating income. GKOS’ R&D is strategic in our view, and we decided to gauge how this is pulling through at the economic level for the firm, leaving the accounting realities aside for now. Of course, this results in remarkable changes, after we recalibrated the annual figures from FY15–the TTM to Q3 FY22. Note, in Exhibit 3, the restated tax-adjusted operating income across the testing dates.

We should recall that a firm creates value when its ROIC exceeds the cost of capital. Moreover, a positive, and ideally growing ROIC is preferred. Where we recalculated R&D as an investment, the following observations were made:

- GKOS generated a cumulated $246mm in NOPAT

- Subsequent to this, the additional growth on this cumulative number was $13.6mm

- GKOS increased its capital investment by $766mm as part of this growth route

- Related to points 1), 2), and supporting our hold thesis, the incremental ROIC was just 1.77% on its investments over these dates

- In extension of this, the NOPAT growth rate exceeded the ROIIC at 5.5%

- To generate the growth, required >311% of NOPAT reinvestment, but not at high rates of return [1.77%, as mentioned].

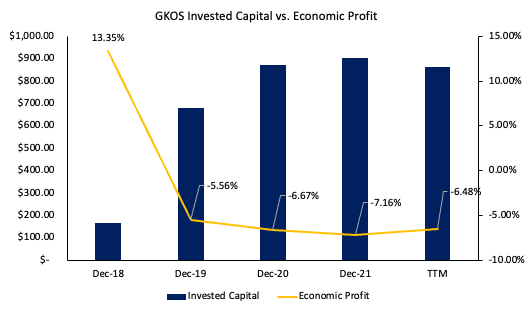

Exhibit 4.

Data: Author, using data from GKOS SEC Filings

A firm can grow faster than its ROIC, provided it has access to external financing [debt, equity]. In the analysis, after ROIC fell below the ROIIC in FY20 is when GKOS expanded its balance sheet on the liabilities side in obtaining long-term debt financing.

Typically, this wouldn’t be an issue, provided the financed growth was accretive to shareholder value. Recall, when ROIC>hurdle rate, is when growth generates economic value. This wasn’t the reality for GKOS – the ROIC prints have been underneath the cost of capital since FY19 [Exhibit 5]. Subsequently, the growth rates described above haven’t generated substantial value for equity holders, reflected in the 5-year performance of its stock price [January–December FY18′ inclusive].

Exhibit 5.

Data: Author

Valuation and conclusion

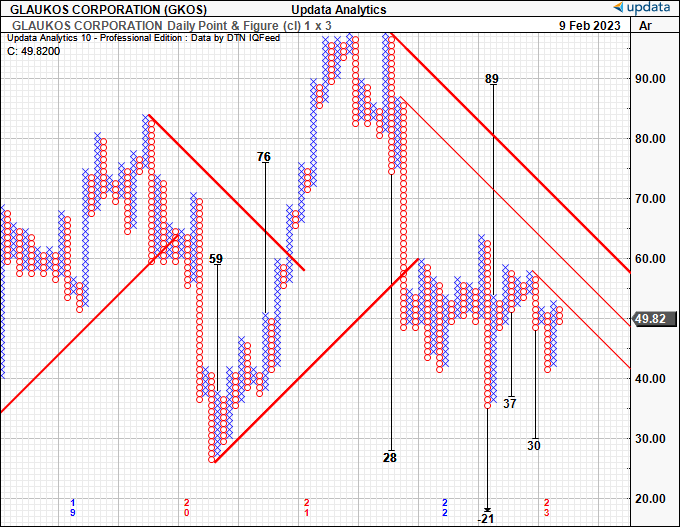

If GKOS were to warrant a 4x book value multiple, there’s to be more profitability driving this divergence. We therefore reiterate our neutral posture. There are multiple supporting points to this rating. As demonstrated, economic profit is absent from the investment debate just now, even when treating R&D as an investment. The stock is trading at 8x forward sales, meaning it must 8x its sales growth for investors to eventually realize this premium. We believe it has more to go in order to justify this as well. Moreover, the market data is pricing in further downsides, we have downside targets to $30 in our point and figure studies shown below.

Exhibit 6. Downside targets to $30, supporting view

Data: Updata

Net-net, we reiterate GKOS as a hold for now. There is plenty of activity building in its clinical trial domain, but we’ve yet to see this pull through for investors. That’s not to say it’s not possible on the horizon, and we remain constructive on its momentum in this regard. Rate hold.

Be the first to comment