Guoco Group Limited (OTCPK:GULRF) is a Hong Kong listed investment holding conglomerate that trades at a 10-year low valuation (price to book of 0.34x) and stock price (HKD63.80), and has had three privatization offers made by its majority shareholder during the company’s history. The company (ticker 53 HK in Hong Kong) has a market cap of HKD20.99 billion ($2.67 billion) presently and trades at 10.7x price earnings based on its FYE2022 net profit.

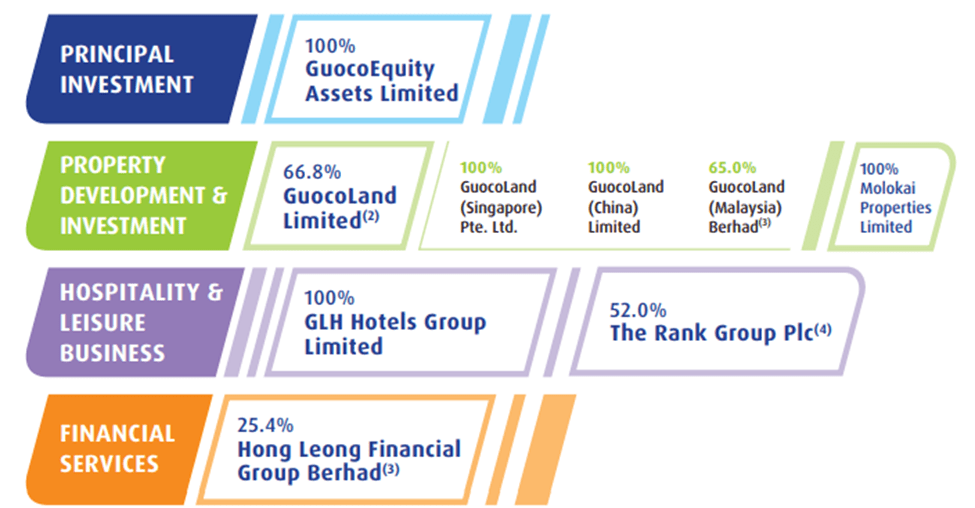

The main business segments of Guoco Group are 1) principal investments (investments made primarily into equity securities in major markets with a value-oriented focus); 2) property development and investment through its Singapore Exchange listed subsidiary GuocoLand Limited (OTC:GUOLF), a major Singapore property developer; 3) hospitality via its wholly-owned GLH Hotels Group Limited, the largest owner-operator hotel company in London, and leisure via its London listed gaming company The Rank Group Plc (OTCPK:RANKF); 4) financial services via its Malaysia listed associate company Hong Leong Financial Group Berhad (OTCPK:HLFBF), an integrated financial services group primarily in Malaysia.

The Group also owns other non-core assets, namely a Hawaiian island that had a previous price tag of $230 million, an oil and gas royalty, and a New Zealand honey business. A chart showing the company’s businesses and its shareholdings is shown further below.

There have been three privatization offers during the history of Guoco Group by its ultimate majority shareholder, Tan Sri Quek Leng Chan, the last unsuccessful offer being in 2018. With Guoco Group’s stock price at ten-year lows and several recent other corporate moves by Tan Sri Quek in his business empire that indicates planning for future legacy/succession, there is a high chance of another privatization attempt in the nearer future, in my view. The two largest minority shareholders in Guoco Group are investment titans Elliott Investment Management (9.72%), which supported the 2018 offer, and First Eagle Investment Management (7.97%), which appears to have rejected the 2018 offer.

Even if a privatization offer does not take place in the nearer future, the stock trades at one of its largest historical discounts to book value, making it a compelling long-term hold (despite the risk factor of unfavorable treatment of minority shareholders). There are also other potential catalysts to the company, such as a potential divestment/merger of Guoco Group’s indirect stake in Hong Leong Bank Berhad (OTC:HLFAF), one of Malaysia’s major banks.

My first section covers the company background, business segments and performance. The second section covers the history of privatization offers for Guoco Group by Tan Sri Quek. It also examines recent corporate moves, the possible motivations for the privatization attempts and why a fourth attempt may be likely. The third section examines the largest minority shareholders whose acceptance for an offer is required for a future privatization offer to succeed. The fourth section looks at the risk factors to an investment in Guoco Group stock.

Guoco Group is 75.55% owned by its ultimate corporate majority shareholder, GuoLine Capital Asset Limited (“GCAL”). GCAL is a Jersey incorporated private investment company of Malaysian tycoon Tan Sri Quek Leng Chan and family (Tan Sri is an honorific title in Malaysia bestowed by the King of Malaysia).

Tan Sri Quek, 80, is executive chairman and the largest shareholder of his privately held family company Hong Leong Co. (Malaysia) Berhad, which is a key holding company that is part of a diversified conglomerate known as Hong Leong Group Malaysia. Tan Sri Quek is ranked by Forbes as the no 2 wealthiest individual in Malaysia in 2022 with a net worth of $10.1billion. The younger brother of Tan Sri Quek, Mr. Kwek Leng Hai, is executive chairman of Guoco Group.

Tan Sri Quek holds 49.11% of GCAL whilst the other shareholders comprise his siblings and cousins, the Kwek family, in Singapore (Tan Sri Quek’s cousin, Mr. Kwek Leng Beng, is executive chairman of Hong Leong Group Singapore). Tan Sri Quek is the nephew of the late Kwek Hong Png, who founded Hong Leong Singapore with his brothers.

A summary of the business segments of Guoco Group is as follows:

Principal Investments

Guoco Group’s principal investments comprises their investing primarily into listed equities internationally, with a value-oriented focus. This segment registered a loss before tax of “HK$430.7 million ($54.86 million) for the year ended 30 June 2022, primarily due to unrealised mark-to-market valuations at the year end”.

Per annual report,

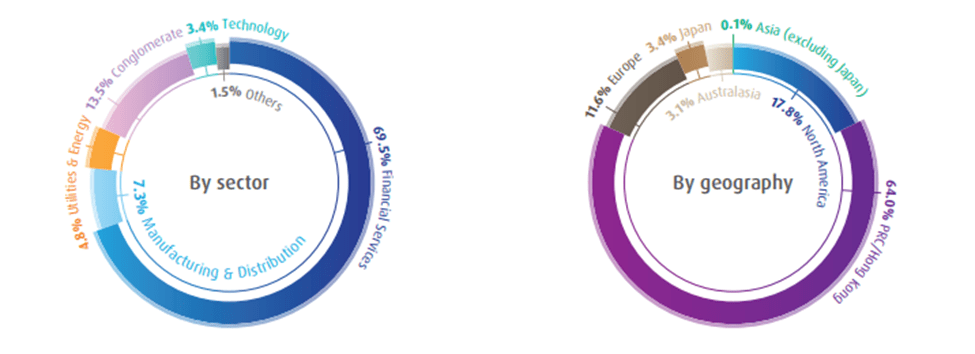

as of 30 June 2022, the Group’s total investments under the Principal Investment amounted to US$1,962 million. The investment portfolio consists of around 25 securities and no single investment accounted for a value of 5% or more of the Group’s total asset value as at 30 June 2022. Most of the investments are in financial services by sector (69.5%) and China by geography (64%). The breakdown of our investment portfolio (excluding The Bank of East Asia, Limited (“BEA”)) as at 30 June 2022 by sector and geography are as follows:

Guoco Group

It is not entirely discernable what has been the specific annual percentage return performance of the principal investments segment. Regarding total investment amount of this segment, only the amount of total investment assets as at the date of each financial year end is disclosed. However, using this year-end figure and reported annual profit/loss before tax, we can attempt a form of measurement of the annual percentage return. Under these assumptions, the annual percentage performance extracted for the last seven financial years looks underwhelming.

Under their property development segment, Guoco Group owns 66.9% of SGX listed developer GuocoLand Limited, translating into a stake value of SGD1.237 billion on a market cap basis presently. GuocoLand is a “premier property company with operations in the geographical markets of Singapore, China, Malaysia” per annual report, and has a strategic partnership in Australia and the United Kingdom. Amongst notable assets, it owns the Guoco Tower, a mixed-used development and the tallest building in Singapore.

At the end of Guoco Group’s recent financial year, GuocoLand’s stock price was SGD1.58 and at the start of this year it was SGD1.53. It is currently at SGD1.56, having reached a recent year high in September of SGD1.81 amidst a strong property market in Singapore before retracing. Therefore, in the context of the bear market internationally, GuocoLand stock has performed well by being up year to date and since Guoco’s previous financial year.

Under the Property Development and Investment segment is also 100% owned Molokai Properties Limited, which owns a third of the island of Molokai, encompassing 55,575 acres. Molokai was placed on the market in 2019 with an asking price of $260 million but there has not been a sale.

Hospitality and Leisure Business segment

Per annual report, 100% owned GLH Hotels Group Limited is the

largest owner operator hotel company in London with more than 4,700 rooms and over 120 meeting and event spaces across the capital city. Its portfolio comprises of four iconic hotel brands, including Guoman, The Clermont, Thistle and Thistle Express.

GLH Hotels Group was formerly under a SGX listed company, GL Limited, which was privatized successfully by Guoco Group in 2021 at a price of SGD0.80 per share, below the computed sum of the parts value per share of $1.14 to $1.32, by the appointed IFA. The IFA described the offer as being “not fair, but reasonable.”

The timing of the privatization offer was opportune as it came amidst the pandemic where GL Limited’s business was impacted and suffered a loss. There is significant upside to this valuation that may be realized in the future event of a sale or a re-listing of the business. GLH Hotels comprise some prime UK real estate. Theoretically, the successful privatization of GL Limited at the significant discount to book value is good for Guoco Group minority shareholders, assuming there is some future value unlocking/catalyst event for GLH Hotels that minority shareholders benefit from.

The Rank Group plc is 52% owned by Guoco Group and listed on the London Stock Exchange. Per annual report, Rank is a “leading European gaming company” and “offers a unique blend of gaming experiences through its three key iconic brands, Grosvenor Casinos, Mecca Bingo and Enracha, that operate from over 125 venues and complimentary digital channels in the United Kingdom and Spain”. Rank’s stock price is down 51.7% year to date amidst a challenging consumer discretionary environment. Guoco Group’s stake is worth GBP190.84 million on a market cap basis.

Financial services

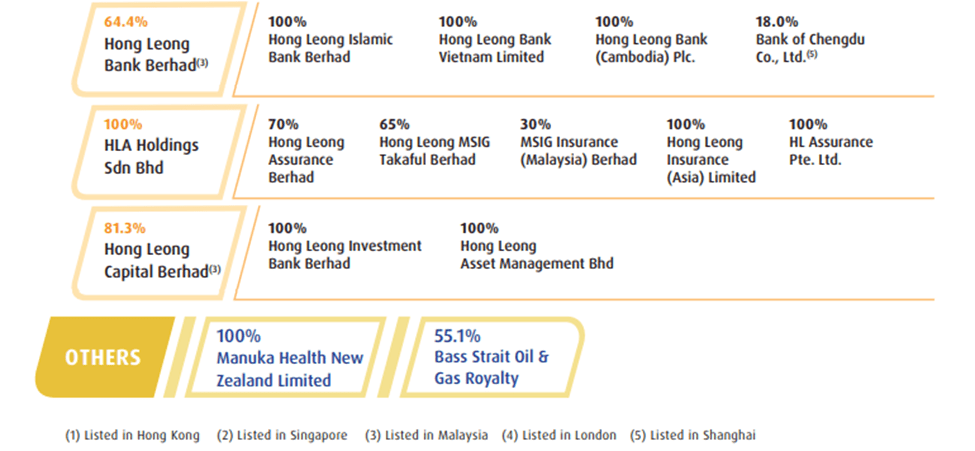

Guoco Group owns a 25.4% controlling stake in Hong Leong Financial Group Berhad. Hong Leong Financial Group is a holding company of several financial services companies in Malaysia and Asia. It owns 64.4% of Hong Leong Bank Berhad, one of the major banks in Malaysia. This segment may be a catalyst for a corporate exercise and Guoco Group’s stock price in the nearer future.

The Hong Leong Financial Group stake has been reported to being considered for a sale or merger by Tan Sri Quek. In August, Reuters reported that Tan Sri Quek was weighing options of his stake in Hong Leong Bank, including a merger.

Malaysia’s second-richest man Quek Leng Chan is weighing options for his stake in Hong Leong Bank Bhd, including a merger, two sources with knowledge of the matter said, in a move that could trigger wider consolidation in the sector. Quek, 80, is also exploring the possibility of reducing his stake in the Malaysian lender

Let us attempt to foretell how a future transaction of Hong Leong Bank might play out and the positive implications of this for Guoco Group. The most obvious acquiror and consolidator could be Malayan Banking Berhad (OTCPK:MLYNF), known as Maybank, which is the largest bank in Malaysia. A potential merger of Hong Leong Bank with Maybank could involve Hong Leong Financial Group receiving shares in Maybank as consideration. Note that Maybank has a market cap of MYR105billion presently, and thus shares in Maybank would represent a relatively easily monetizable holding. Post such a merger scenario, Hong Leong Financial Group could subsequently distribute the shares in Maybank to its shareholders, and thus Guoco Group could directly own shares in Maybank. Such a scenario may allow a monetization of the holding, and Guoco Group would then have a very significant boost to its cash pile. Remember, Guoco Group trades at only 0.34x its book value presently.

Malaysian business publication The Edge discussed a possible motivation for Tan Sri Quek to do a deal for Hong Leong Bank. Under the Financial Services Act (2013) in Malaysia, individuals cannot own more than 10% of a financial institution and approval is required to acquire control over a bank. This rule was “grandfathered” to allow individuals like Tan Sri Quek to hold his existing controlling shareholding in Hong Leong Bank. It is unlikely that such an exemption would apply on to his children in the future. The Edge quotes one analyst who suggests succession and estate planning may be behind the move:

“Quek, 80, may feel an increasing need to sell, given his age. “I don’t think the ‘grandfather-ing’ rule of allowing individuals like Quek to own such a high shareholding would apply to his children in the case of inheritance,” the analyst told The Edge.

Perhaps history can help provide an indication on how a future transaction might unfold for Guoco Group. Tan Sri Quek is known as a savvy dealmaker with a knack for divesting business assets at ideal valuations.

Of note, Guoco Group sold Dao Heng Bank to DBS in 2001 at a multiple of more than 3 times book value at the time. It would look opportune for Tan Sri Quek to divest/merge Hong Leong Bank soon. Hong Leong Bank trades at a relatively premium 1.39x price to book currently, and any transaction that adds a significant premium on top of this valuation would be an attractive valuation for Hong Leong Bank shareholders.

Considering the above, we may speculate that there is a good likelihood of a future sale/merger being done for Hong Leong Bank. Meanwhile, with Guoco Group’s share price at historical lows and one of the largest discounts of stock price to book value, there appears to also be a good chance that Tan Sri Quek may attempt another privatization bid of Guoco Group. This could take place before any sale by Guoco Group of Hong Leong Bank is made.

Manuka Health New Zealand Limited

Guoco Group acquired New Zealand Manuka honey products producer, Manuka Health New Zealand Limited, in 2018 from Australia private equity firm Pacific Equity Partners. The transaction price was not disclosed by Guoco Group. However, one media report at the time placed the transaction price in the “hundreds of millions of dollars”, whilst during the sale process, Reuters reported that the company had attracted a bid of $300million (about NZD447million at the time) from two Chinese firms. Therefore, we could presume that the consideration paid by Guoco Group for Manuka Health was at least NZD447million.

Pacific Equity Partners purchased Manuka Health in 2015 for a price of NZD110million. In 2015, Manuka Health had revenue of NZD70million, valuing it at a 1.57x sales multiple. In 2012, Manuka Health had a valuation of NZD20million.

In the last financial year, Guoco Group recognized an impairment charge on the value of Manuka Health. Per 2022 annual report: “Following a review, an impairment charge on assets of NZD104.0 million (approximately HK$552.1 million) was recognised.”

Guoco Group Net Assets

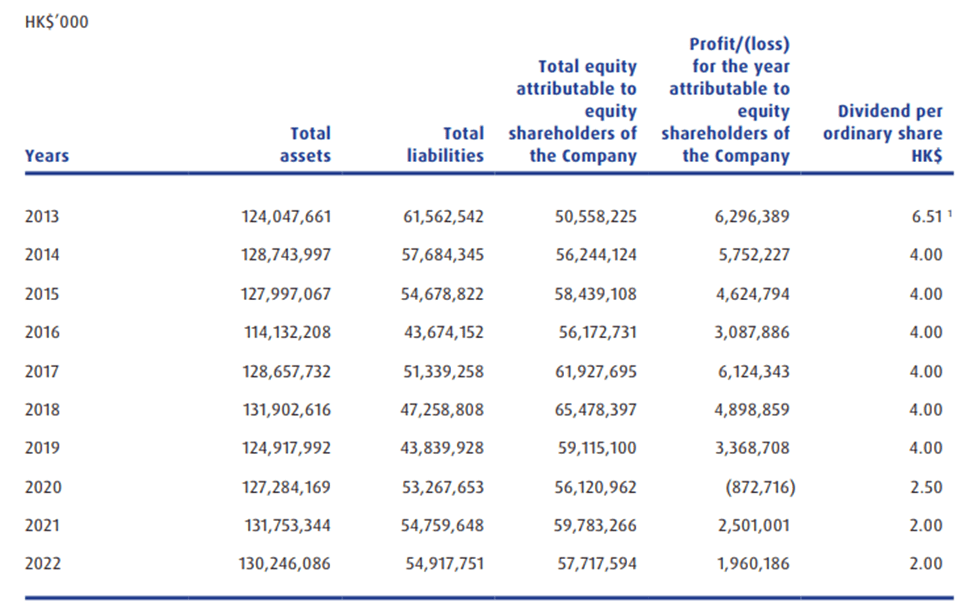

Guoco Group’s business segments have overall seen a somewhat resilient performance in the past year by measure of the consolidated net asset value. Net assets at HKD75.328 billion versus HKD76.993billion the previous year were only down by 2.16% at financial year end 30 June 2022 vs the previous financial year end. Net assets in FYE 2013 were HKD62.485billion. Therefore, consolidated net assets are up by 20.55% over the last nine years. At FYE 2013, Guoco Group’s share price stood at HKD90.55, thus its share price is now 27.6% lower than it was then.

Net assets in Guoco Group’s accounts are on a consolidated basis. Excluding non-controlling interests (in GuocoLand, Rank Group plc and Bass Strait Oil and Gas Royalty), Guoco has net assets of HKD61.179billion. With its current market cap of HKD20.99billion, Guoco Group trades at a price to book ratio of 0.34x. This is one of its widest historical discounts to its book value.

Guoco Group

Dividend History

We should note that after the privatization attempt in 2018, dividend per share declined from the HKD4.00 declared in FY2019 (the same dividend for six consecutive financial years), to HKD2.50 per share in 2020 before a further decline to HKD2.00 in 2021. 2020 saw a loss due to the pandemic, and profit in 2021 was lower than pre-pandemic years. Nonetheless, Guoco Group does have significant cash and investments, and the HKD4.00 dividend could have been maintained instead of cut.

The history of privatization offers by Tan Sri Quek for Guoco Group

There are a total of three privatisation offers that have been made by Tan Sri Quek for Guoco Group. Examining the history of the privatization offers and Guoco Group’s shareholder base will allow us to gauge the potential for a future offer.

In December 2012, Tan Sri Quek made an offer to privatise Guoco Group at HKD88.00. The offer was subsequently increased to a total of HKD100 in April 2013. Around this time, Elliott Investment Management (Elliott) emerged as a substantial shareholder and opposed the offer. The privatization attempt was unsuccessful, with only 32.82% of the total number of “Disinterested Shares” (shares of the company not owned by the offeror and its parties acting in concert) accepting the offer, vs 90% required for the offer to be successful.

In June 2018, Tan Sri Quek made a privatisation offer via scheme of arrangement at a price of HKD135 for the company. Presumably as a sweetener for the offer (the offer price was 32% below net asset value per share of HKD199), the offer included a choice between consideration fully in cash or in cash and a dividend distribution of stock in Hong Leong Financial Group. Elliott supported the offer this time and provided an irrevocable undertaking to approve the offer proposal. However, the privatization offer was not successful, with 64.78% of Independent Scheme Shareholders accepting the offer. This was short of the required 75% acceptances and not more than 10% of Disinterested Shareholders voting against the offer needed under a scheme of arrangement.

Apart from the two privatization attempts above, there was also a general offer to all minority shareholders made by Tan Sri Quek, following his buying out a 21.6% stake held by the Kuwait Investment Office in 2004.

Motivations for the privatization attempts and why a fourth attempt may be likely

Therefore, there have been a total of three privatization offers for Guoco Group by Tan Sri Quek since the 2000s. Clearly, Tan Sri Quek has had a determination to privatise the company, in view of the previous attempts. Let us consider the motivations for this and why a fourth offer may be likely.

The obvious motivation is that Guoco Group is deeply undervalued relative to its assets. There are also businesses under Guoco Group which would command a higher valuation if they were listed or divested in the future (such as Hong Leong Bank and GLH Hotels). Privatising Guoco Group would allow Tan Sri Quek to derive more of the benefits of this in the future. The privatization and the corporate exercises as a private company could be part of a possible several-step long-term exercise (therefore it would be better to privatise the company sooner than later).

Tan Sri Quek owns 49.7% of GuoLine Capital Assets Limited, the ultimate holding company of Guoco Group. The other shareholders are his siblings and cousins in Singapore. These are many shareholders in number and will become more in number when shareholdings are passed on in the future to the family company’s third generation of the Quek and Kwek families in Malaysia and Singapore. Tan Sri Quek controls this extended family company through his having the largest shareholding and being the driving force of the activities of Hong Leong Malaysia for many decades since its inception. One could surmise that having Guoco Group as a privatized entity may simplify for Tan Sri Quek his long-term corporate and legacy plans for the businesses and assets of Guoco Group.

There have been several recent moves that may indicate Tan Sri Quek is planning his business empire ahead for the time when it is passed over to his children.

Consider

In January 2021, Tang Hong Cheong, the then President and CEO of Guoco Group and a 40-year steward at Hong Leong Group, retired from his role. His position was taken over by the younger Chew Seong Aun (age 57), as CFO and Executive Director. Chew Seong Aun came from other roles in the Hong Leong Group and is a former banker and accountant. His background is also similarly suited for potential corporate exercises (potential privatization and subsequent unlocking of business subsidiaries value) that could be undertaken for Guoco Group over a longer-term period.

Per annual report, an internal restructuring was completed on 16 April 2021, whereby Tan Sri Quek’s Hong Leong Company (Malaysia) Berhad, the previous long-time holding company of Guoco Group, was replaced by Jersey incorporated GuoLine Capital Assets Limited. Malaysia incorporated Hong Leong Company (Malaysia) Berhad had long been the ultimate holding company of Hong Leong’s operating and investment companies, both public listed and private. After decades as the holding company of Tan Sri Quek and family/Hong Leong Malaysia’s business and investment interests, it is interesting that there is this recent restructuring. However, one could speculate that Jersey might have chosen as more suited for legacy planning purposes.

Together with the recent reports of a potential deal being made to sell Hong Leong Bank, the overall picture is that Tan Sri Quek may be legacy planning.

Guoco Group is at 10 year lows and continues moving lower on low trading volume. Global equity markets are in a bear market and bond yields have soared. The minority shareholders who did not accept the previous offer in 2018, may have more motivation now to accept a privatization offer.

The minority shareholders who determine a privatization offer’s success or failure

One of the requirements for a successful privatization via scheme of arrangement in Hong Kong is that there is not more than 10% of the Disinterested Shareholders who vote against the offer.

Tan Sri Quek’s indirect and direct shareholdings in Guoco Group are shown below, as well as those who would be deemed parties acting in concert with him in an offer (in this assumption, the parties acting in concert are his two brothers and the former CEO of Guoco). In total, there are 254,422,012 shares held representing 77.32% of the issue share capital of the company.

For a privatization offer to succeed, it must be accepted by 90% of the Disinterested Shareholders. Assuming the above figure, Disinterested Shareholders represent 22.68% of the share capital whilst minority shareholders representing 20.41% would need to approve an offer for it to succeed. A total shareholding of only 2.27% of the company could block an offer.

Issued shares

329,051,373

Tan Sri Quek Leng Chan

250,282,117

76.06%

Kwek Leng Hai

3,800,775

1.16%

Kwek Leng San

209,120

0.06%

Tang Hong Chong

130,000

0.04%

Parties Acting in Concert

254,422,012

77.32%

Disinterested shareholders

74,629,361

22.68%

90% of Disinterested shareholders

67,166,425

20.41%

Minority shares which can block an offer

7,462,936

2.27%

Source: Annual report

The largest two minority shareholders are Elliott Investment Management which owns 9.72% and First Eagle Investment Management which owns 7.97%, therefore these two shareholders own a total of 17.69%. Both of their acceptances in a new privatization offer scenario, would mean that Tan Sri Quek would only require an additional 2.57% of the company’s shares, or 53% of remaining minority shareholders to accept the offer for it to succeed.

Elliott supported the 2018 privatisation offer, as mentioned previously. Furthermore, Elliott has since closed its Hong Kong office, to focus on Japan and sold out of its stake in Bank of East Asia Limited this year. One could envisage that Elliott would support a new privatization offer again, since Hong Kong is no longer a focus market.

So, let’s look at First Eagle. First Eagle is a leading asset manager with $115billion of assets under management. They are principled, value-oriented investors – think modern day value investing that draws from Graham-Dodd style origins. First Eagle’s shareholding in Guoco Group is spread across several funds and managed accounts it operates and the firm has been a shareholder in Guoco Group since the early 2010s.

First Eagle disclosed on 29 December 2020 that it increased its shareholding in Guoco Group by the amount of 4 million shares, raising its ownership in the company from 22,849,466 (6.94%) to 26,849,466 (8.16%). First Eagle disclosed on 30 November 2021 that it had reduced its shareholding by 153,000 shares to 26,238,046 (7.97%). It is interesting that First Eagle has increased its overall shareholding significantly despite the stock’s low liquidity.

In the 2018 unsuccessful privatization offer, 24,338,637 votes were cast against the privatization offer proposals, which represented 35.35% of the Independent Scheme Shareholders. 44,519,382 votes were cast for the privatization offer proposals which represented 64.65% of the Independent Scheme Shareholders. As we can deduce, First Eagle would have had voted against the offer (its holding 22,849,466 shares at that time). Outside of First Eagle’s shares, there would have been 1,489,171 shares (2.16%) that also voted against the offer. If First Eagle had accepted the offer, the privatization would have succeeded. In a future potential privatization offer, Tan Sri Quek would need to have First Eagle’s acceptance to successfully privatise.

Consider why First Eagle may have rejected the 2018 offer.

In the 2018 offer, the offer price was at a 32% discount to book value. First Eagle is a value-oriented, long-term investor. One presumes that they will exit a position if it reaches fair value but otherwise are content to hold. Whilst First Eagle is a substantial shareholder in Guoco Group, the position represents a small percentage in its respective funds. For instance, it holds 12,748,580 shares in Guoco Group in its First Eagle Global Fund which represents 0.26% of the fund.

It also appears that First Eagle may be a representative “voice” for minority shareholders in Guoco Group. A general mandate for the directors of Guoco Group to issue, allot and deal up to 10% of share capital has seen a significant minority shareholder vote against it (28,683,350 shares voted against it at the recent AGM this month and 26,434,207 shares voted against it in 2021). This appears to include First Eagle’s shareholding stake that has voted against it.

Potential risk factors

Some potential risk factors to the stock investment, are discussed here.

1. Potential unfavorable policies to minority shareholders

There is a well-documented backdrop of policies unfavorable to the minority shareholder in Guoco Group specifically, that may be a potential risk factor in investing in Guoco Group stock.

The mentioned 2001 sale of Dao Heng Bank brought in a $4.1billion windfall to Guoco Group. Following the sale, minority shareholders of Guoco Group, including its then 2nd largest shareholder Kuwait Investment Office, wanted Guoco Group to distribute the gains from the sale as a dividend but Tan Sri Quek refused. Instead of distributing the gains as a dividend, Guoco Group used some of the proceeds to buy back stock in Guoco Group at a 25% discount to book value. This was met with strong resistance from minority shareholders. Eventually, Kuwait Investment Office divested their entire stake to Tan Sri Quek. A prominent academic paper studied these events affecting Guoco Group minority shareholders, and described it as being to “enhance the controlling owner’s grip on the group at the expense of the minority shareholders” and “eventually forced out the second largest shareholder“.

Since the 2018 unsuccessful privatisation offer, annual dividends have been decreasing although Guoco Group has significant cash and principal investments. There have also been a series of related party transactions whereby Guoco Group’s wholly owned subsidiaries have engaged related entities controlled by Tan Sri Quek, for the provision of management and investment management type services.

On 3 July 2020, two master service agreements were entered into by Guoco Group wholly-owned subsidiaries with related entities controlled by Tan Sri Quek, for the provision of services to Guoco Group’s subsidiaries, with fees payable being:

a monthly fee (the “Monthly Fee”) as agreed from time to time between such Service Recipient and the relevant Service Provider and is currently agreed to be approximately HK$613,000 per month; and 2. an annual fee (the “Annual Fee”) equal to 3% of the annual profit before tax of such Service Recipient as shown in its audited profit and loss account for the relevant financial year, subject to appropriate adjustment (for example, to avoid double counting of profit), if any…Total amount paid or provided for in respect of management fees to GGMC and HLMC for the year ended 30 June 2022 amounted to US$8,682,000 and US$298,000 (2021: US$4,457,000 and US$1,333,000) respectively.

Most recently, on 1 November 2022, there has been related party agreements for the provision of discretionary fund management services and investment advisory service being provided to Guoco Group. The annual fee, performance fees and staff costs payments for these agreements, is detailed in the announcement.

2. Risk of underperforming investment decisions

The historical performance of the principal investments segment appears underwhelming, per the previous estimates on its annual percentage performance. It is also uncertain whether Guoco Group’s procuring of discretionary fund management and investment advisory services from its related party entities will improve its principal investments performance. The engaged entities are related parties to Guoco Group, with the same ultimate oversight over investment decisions.

After years of avoiding making acquisitions based on a view of pricey valuations, Guoco Group made its acquisition of Manuka Health at a premium valuation, which has since seen a major write-down.

Although Guoco Group is 76% owned and operated by its majority shareholder, this does not preclude it from making sub-optimal investment decisions when it would have been better to distribute cash to all shareholders as dividend.

3. Liquidity risk

Daily trading volume in Guoco Group is low. Most days, there is low volume of a few thousand shares traded in the stock.

There are the occasional days where there are spikes in the trading volume, when there is determined selling and buying. The latest trading day has seen 42,390 shares of volume. We should note too First Eagle’s previous significant buying in spite of the low liquidity.

Nonetheless, investors who build a position in the stock, will likely be building it up over time and will need to view a future privatization offer as an exit or be investing with a view of the stock as being a long-term holding. Low liquidity risk should also be considered together with the described potential risks of unfavorable policies to minority shareholders.

Conclusion

Guoco Group represents one of the most compelling value stocks in Hong Kong, in my view. I am invested in the stock with the view that there is a good probability of a privatization offer again in the (nearer) future, for the reasons outlined.

Further, a future privatization offer would likely need to be at a suitable offer price to gain the acceptance of First Eagle’s deciding minority stake. The 2018 offer price of HKD135 is 111% higher than the current stock price of HKD63.8, whereas net assets have grown since. In any case, I view that a future offer will have to be at a higher price than 2018’s HKD135 and somewhat closer to the latest book value per share of HKD185.9 (which excludes non-controlling interests). In summary, the nearer-future potential catalysts are 1) a divestment/merger of Hong Leong Bank and/or 2) a privatization offer by Tan Sri Quek.

I am also prepared to hold the stock for the long-term for many years ahead, with a similar long-term time horizon view as that of First Eagle. There are potential risks to consider, as previously detailed. Nonetheless, price to book valuation at 0.34x is at a historically low valuation and one can view that the potential risks are priced in. Net assets of Guoco Group will continue to grow over time as it has historically, and ultimately its stock price will increase to trade at a lower discount to book value.

In the event that a privatization offer does not occur, I view there will eventually be more minority shareholder-friendly conduct such as higher dividends to come in the longer run, for those with a patient approach.

Please note that foreign exchange and other leveraged trading involves significant risk of loss. It is not suitable for all investors and you should make sure you understand the risks involved, seeking independent advice if necessary.

Be the first to comment