hqrloveq/iStock via Getty Images

A Quick Take On Greifenberg Digital Limited

Greifenberg Digital Limited (GDLT) has filed to raise $15 million in a direct listing of its common shares, according to an F-1 registration statement.

The firm provides risk analytics services for fixed-income markets.

Given the firm’s lack of substantial revenue, thin capital base and management’s valuation assumptions, my outlook on the direct listing is on Hold.

Overview

New York, NY-based Greifenberg Digital Limited was founded to develop proprietary risk models for determining risk profiles of corporate borrowing entities in emerging fixed-income markets.

Management is headed by Chief Executive Officer David Goldman, who has been with the firm since January 2021 and was previously Business Editor for Asia Times and has written several books and widely published articles on international topics.

The company’s coverage area by country or region include:

Future:

-

South America

-

Southeast Asia

-

Australia

As of September 30, 2022, Greifenberg has booked fair market value investment of $2.1 million from investors including Integrated Media Technology Limited, Infa Premium Sdn Bhd and others.

Customer Acquisition

The firm’s business model will be to sell its research reports as a subscription-based service to ‘market participants in fixed income products including commercial, investment & global banking, governments and regulatory agencies, corporations, insurance companies, private equity, and investment management firms.’

GDLT intends to focus first on China and then expand its services to other countries and regions.

Employee Benefits expenses as a percentage of total revenue have fallen as revenues have increased from a tiny base, as the figures below indicate:

|

Employee Benefit |

Expenses vs. Revenue |

|

Period |

Percentage |

|

Six Mos. Ended September 30, 2022 |

316.1% |

|

FYE March 31, 2022 |

432.0% |

(Source – SEC)

The Employee Benefits efficiency multiple, defined as how many dollars of additional new revenue are generated by each dollar of Employee Benefits spend, increased to 0.3x in the most recent reporting period, as shown in the table below:

|

Employee Benefit |

Efficiency Rate |

|

Period |

Multiple |

|

Six Mos. Ended September 30, 2022 |

0.3 |

|

FYE March 31, 2022 |

0.2 |

(Source – SEC)

Market

According to a 2022 market research report by MarketsAndMarkets, the global market for risk analytics was an estimated $39.3 billion in 2022 and is forecast to reach $70.5 billion by 2027.

This represents a forecast CAGR of 12.4% from 2023 to 2027.

The main drivers for this expected growth are growing requirements for government compliance and increasing complexities across various markets.

Also, the financial services industry is a subset of the total risk analytics market and hopes to increasingly utilize AI/machine learning technologies to improve analysis of financial instruments.

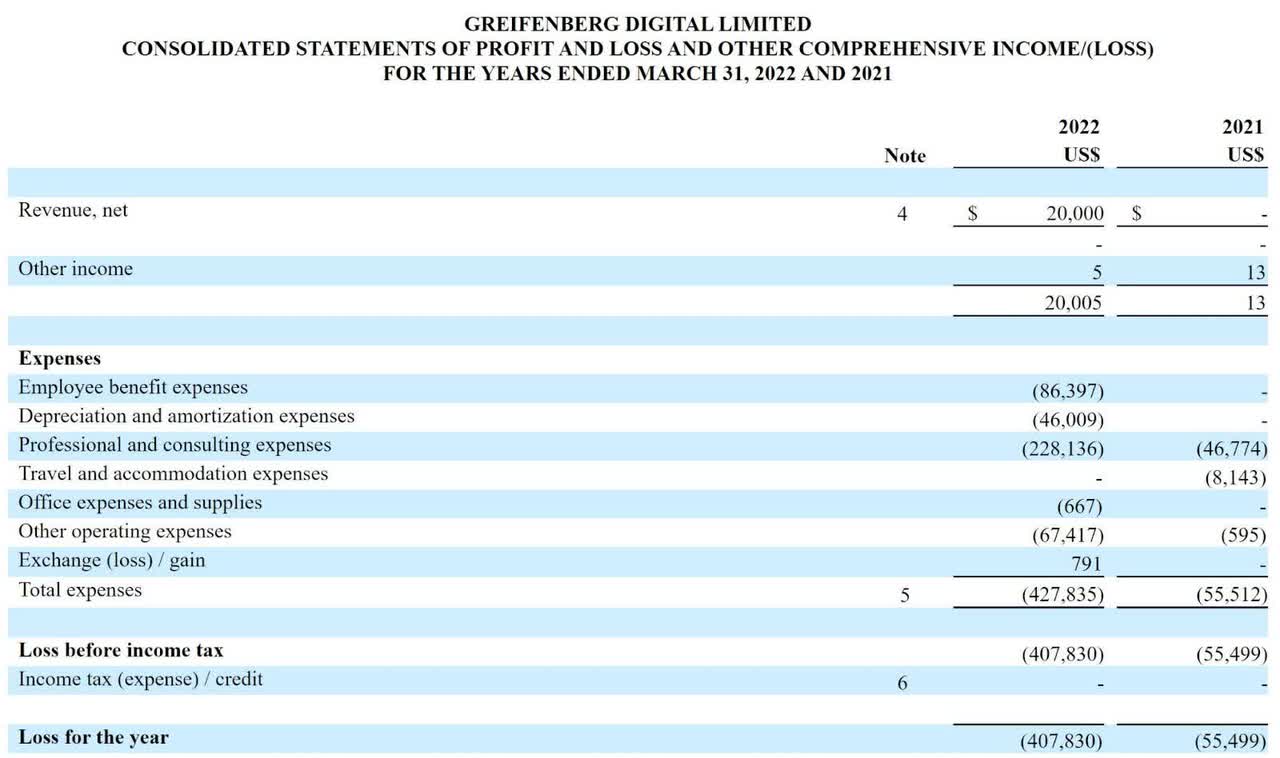

Financial Performance

Below are relevant financial results derived from the firm’s registration statement:

Company Statement Of Operations (SEC)

(Source – SEC)

As of September 30, 2022, Greifenberg had $25,467 in cash and $640,431 in total liabilities.

Free cash flow during the twelve months ended September 30, 2022, was negative ($112,041).

Direct Listing Details

Greifenberg intends to raise $15 million in gross proceeds from a direct listing of its common shares, offering 3 million shares at a price of $5.00 per share, on a ‘best efforts’ basis and with a $10 million minimum subscription floor.

No existing shareholders have indicated an interest in purchasing shares at the listing price.

Assuming a successful listing, the company’s enterprise value would approximate $27 million, excluding the effects of underwriter over-allotment options.

The float to outstanding shares ratio (excluding underwriter over-allotments) will be approximately 36.32%. A figure under 10% is generally considered a ‘low float’ stock which can be subject to significant price volatility.

Management says it will use the net proceeds from the listing as follows:

Continuous development and investment in IT technology for website and mobile App

Growth strategies – including development of financial models for mutual funds and other items

Development of financial models for other emerging markets

Sales and marketing – investment in media, marketing and promotion

Working capital

(Source – SEC)

Management’s presentation of the company’s listing is not available.

Regarding outstanding legal proceedings, management says the firm is not currently a party to any legal proceedings that would have a material adverse effect on its financial condition or operations.

Valuation Metrics For Greifenberg

Below is a table of relevant capitalization and valuation figures for the company:

|

Measure [TTM] |

Amount |

|

Market Capitalization at Listing |

$41,305,000 |

|

Enterprise Value |

$27,039,533 |

|

Price / Sales |

516.31 |

|

EV / Revenue |

337.99 |

|

EV / EBITDA |

-37.07 |

|

Earnings Per Share |

-$0.08 |

|

Operating Margin |

-911.85% |

|

Net Margin |

-911.85% |

|

Float To Outstanding Shares Ratio |

36.32% |

|

Proposed Listing Midpoint Price per Share |

$5.00 |

|

Net Free Cash Flow |

-$112,041 |

|

Free Cash Flow Yield Per Share |

-0.27% |

(Source – SEC)

Commentary About Greifenberg’s Direct Listing

GDLT is seeking U.S. public capital market investment to grow its technology and business in the fixed-income risk analytics space.

The firm’s financials show little revenue history and material losses.

Free cash flow for the twelve months ended September 30, 2022, was negative ($112,041).

Employee Benefits expenses as a percentage of total revenue have fallen as revenue has increased; its Employee Benefits efficiency multiple was 0.3x in the most recent reporting period.

The firm currently plans to pay no dividends on its common shares and to retain any future earnings for reinvestment back into the company’s growth initiatives and operating requirements.

The market opportunity for providing risk analytics is large and expected to grow substantially in the coming years, although its growth trajectory in the firm’s focus area is difficult to determine.

There is no ‘underwriter’ for the direct listing. As management writes:

The offering price of the shares has been determined arbitrarily by us. The price does not bear any relationship to our assets, book value, earnings, or other established criteria for valuing a privately held company. In determining the number of shares to be offered and the offering price, we took into consideration our capital structure and the amount of money we would need to implement our business plans. Accordingly, the offering price should not be considered an indication of the actual value of our Common Shares.

Risks to the company’s outlook as a public company include its tiny size, thin capitalization and lack of material revenue history.

As for valuation, management is asking investors to pay an Enterprise Value/Revenue multiple of approximately 338x, an astronomically high multiple.

Given the firm’s lack of substantial revenue, thin capital base and management’s valuation assumptions, my outlook on the direct listing is on Hold.

Expected Direct Listing Date: To be announced.

Be the first to comment