wichayada suwanachun

The Fed recently raised interest rates by 50 basis points, emphasizing the importance of passive investors protecting their income streams from rising interest rates.

Rithm Capital Corporation (NYSE:RITM) is a diverse real estate investment trust (“REIT”) with significant exposure to Mortgage Servicing Rights. These can help passive income investors profit from rising interest rates.

Furthermore, given the mortgage trust’s 11.9% dividend yield, Rithm Capital provides passive income investors with an exceptionally low payout ratio.

With RITM stock recently reversing, I believe Rithm Capital is a screaming buy.

MSR Exposure Provides Interest Rate Hedge

A pullback is often a good time to buy a stock on current weakness, and I believe Rithm Capital, a mortgage REIT with diversified investments in Mortgage Servicing Rights, mortgage loans, real estate securities, and even single-family homes, provides such an opportunity.

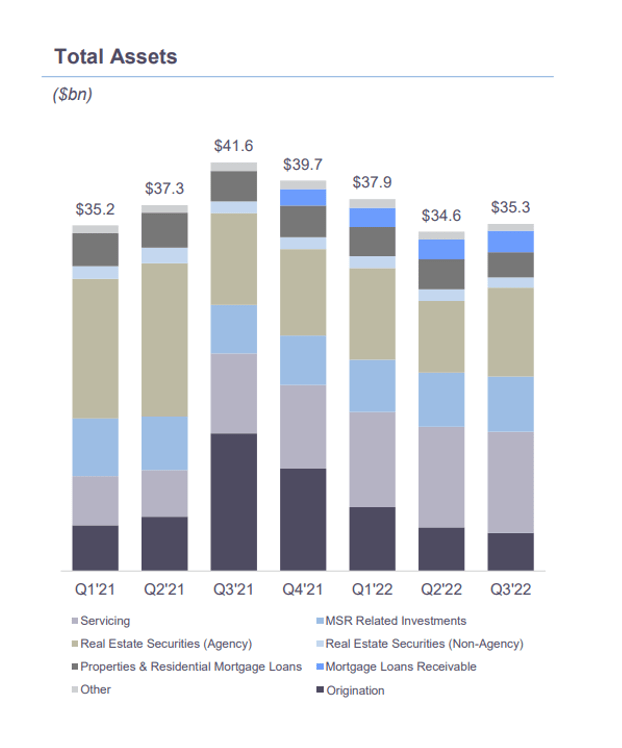

At the end of the September quarter, Rithm Capital’s mortgage investments were valued at $35.3 billion and consisted primarily of Mortgage Servicing Rights and Real Estate Securities.

Total Assets (Rithm Capital Corp)

Most mortgage investments (including mortgage trust stock prices/book values) tend to fall as interest rates rise. This is because rising interest rates raise the cost of debt-financed investments in mortgage securities.

Mortgage REITs suffered greatly in 2022 as the central bank raised interest rates, causing spreads on mortgage-backed securities to widen, borrowing costs to rise, and portfolio values to fall. This has resulted in significant declines in the book values of mortgage trusts such as Annaly Capital Management Inc. (NLY).

However, one asset offers relief: Mortgage Servicing Rights increase in value as interest rates rise in an economy, allowing existing MSRs to be sold at a premium in the market as they become more valuable.

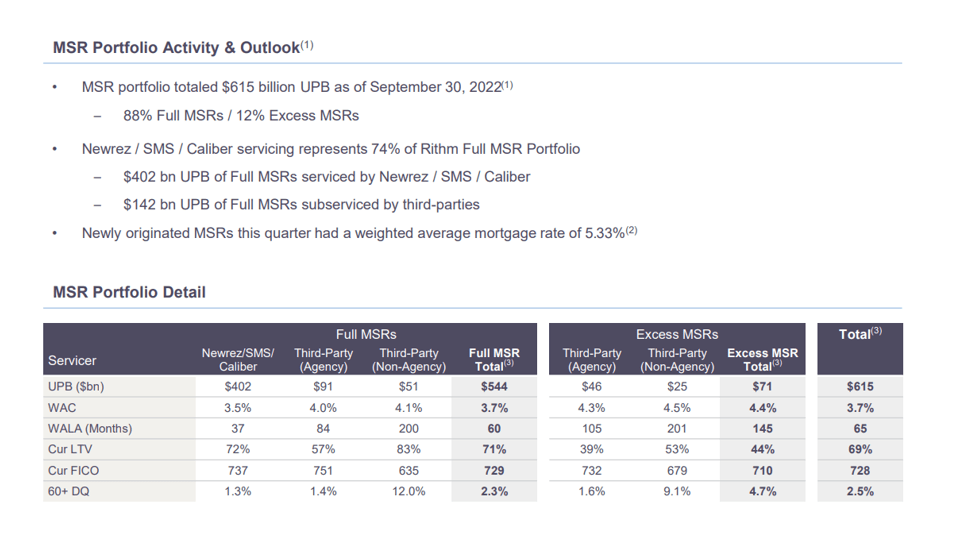

Rithm Capital had $8.9 billion in Mortgage Servicing Rights at the end of the previous quarter (based on fair value), representing a $615 billion unpaid principal balance. The total amount of principal in the underlying mortgages that has not yet been repaid to the lender is represented by the unpaid principal balance.

MSR Portfolio Detail (Rithm Capital Corp)

Another Reason To Buy Rithm Capital: Impressive Pay-Out Metrics

Rithm Capital earned $0.32 in distributable earnings per share, implying a pay-out ratio of only 78%, which is nothing short of impressive for a trust that pays a (covered) 11.9% dividend yield. Please see my summary of Rithm Capital’s payout metrics.

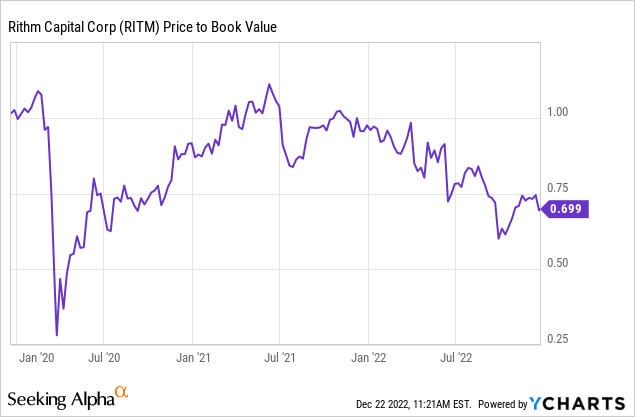

Now Trading At A 31% Discount To Book Value

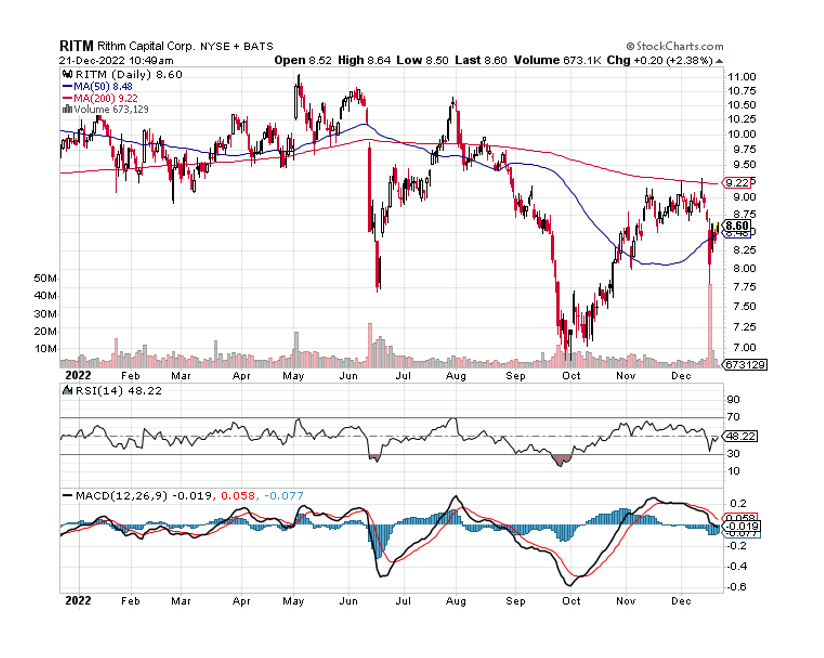

Rithm Capital’s stock price has recently declined, falling below $8 for a brief period before rebounding. Still, I believe there is a buying opportunity here.

While RITM stock is not technically oversold, the drop provides an opportunity to purchase RITM at a lower book value multiple and thus a higher margin of safety.

RITM Share Price (Stockcharts.com)

Given the diversified nature of Rithm Capital’s investment portfolio and the company’s hedge against multiple interest rate scenarios, the stock should not be trading at a 31% discount to book value, as it is currently.

Rithm Capital’s book value was $12.10 as of September 30, 2022, and it provides a reasonable estimate of the intrinsic value per share for mortgage trusts.

Given the degree of dividend coverage, the discount to book value is too large. So, why not take advantage of the recent pullback and add a strong mortgage trust with an 11.9% dividend to a passive income portfolio.

Historically, Rithm Capital’s discount to book value was much lower than 31%.

Why RITM Could See A Lower Stock Price

Higher interest rates hurt mortgage trusts, but Rithm Capital is not your typical mortgage REIT. Rithm Capital is far more diverse than other mortgage REITs, and the presence of Mortgage Servicing Rights, the value of which is positively related to interest rates, is a key differentiator.

Rithm Capital faces the risk of investment losses and a decline in the value of non-MSR mortgage investments such as Real Estate Securities if there is a major real estate recession.

My Conclusion

Rithm Capital is an excellent buy for a variety of reasons. These include a well-managed and diverse mortgage-focused investment portfolio with exposure to rate-sensitive Mortgage Servicing Rights. As interest rates rise, exposure to Mortgage Servicing Rights can provide investors with a hedge against further rate increases.

Another reason to own Rithm Capital stock is the trust’s strong core earnings and low pay-out ratio. With an 11.9% covered stock yield and an unusually large discount to book value, Rithm Capital Corp. is a great high yield stock to buy during the current pullback, in my opinion.

Be the first to comment