AleksandarNakic

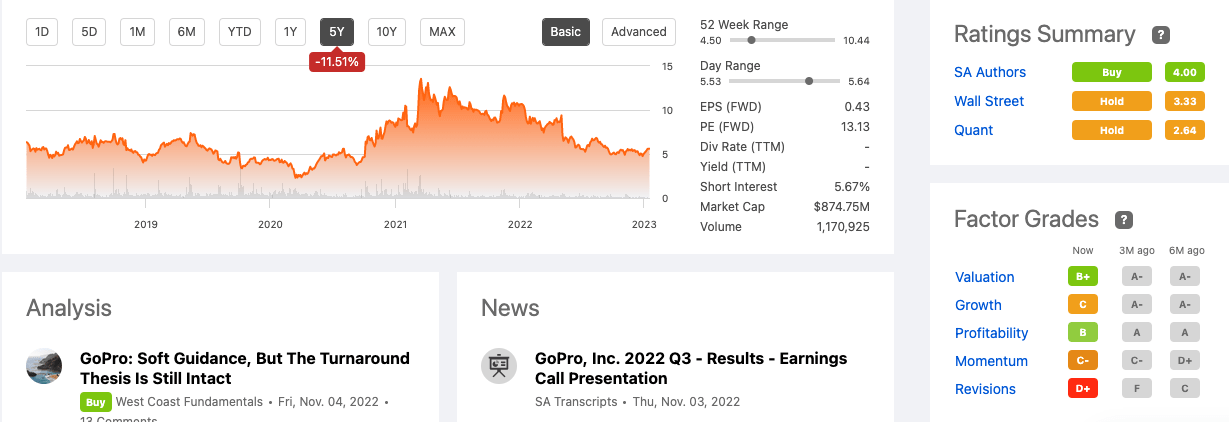

GoPro, Inc. (NASDAQ:GPRO) is a fundamentally better company than it was before 2020 for two reasons, it has grown its asset-light subscription model numbers by bundling it into attractive product offerings and increasing direct sales. The results have been annual recurring revenue quickly growing to over $100 million with over 2 million members and gross margins increasing. However, is this enough to earn back the trust of heavily burned investors who lived through poor management decisions, unsuccessful diversified business ventures, excessive spending and a general loss of business focus? Once upon a time, the stock peaked above $80 per share, nowadays and for the last five years, the price has barely broken into double-digit numbers and is currently trading well below $10.

Five-year stock trade (Seeking Alpha)

While the company has improved its top and bottom line results, growth has slowed this year due to strong headwinds and decreased camera sales. Furthermore, we are yet to understand how sticky the subscription model is. GPRO will soon release its historically high Q4 results with expectations set to earn less than the previous year. Although the company is generating good cash, it remains to be seen whether there is enough innovation and drive to keep it relevant in the long run. For this reason, the stock warrants a hold status.

Overview

GPRO was founded in 2002 by Nicholas Woodman, a Californian surfer looking for a better solution to record his outdoor travel lifestyle. The company successfully IPOd in 2014, gaining a loyal following of investors and delivering annual revenues exceeding the $1 billion mark. The good times turned sour as the business grew. It lost focus, increased spending, and attempted to diversify into media and other unsuccessful ventures. Failed product launches, recalled offerings, and production issues led to the company losing money quarter after quarter from the end of 2015 until the end of 2017.

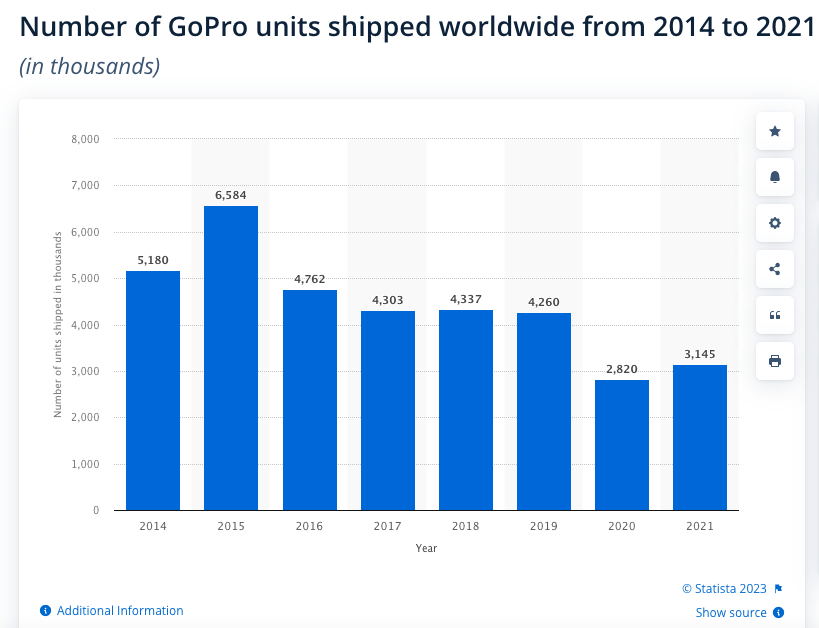

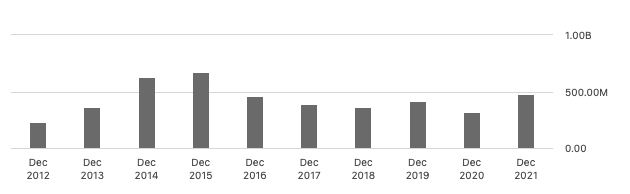

GoPro shipments (Statista)

COVID-19 pushed the company further into misery; however, it pushed it so far as to take on two cash-rendering strategies, betting on its asset-light subscription model that has grown 55% YoY to 2.1 million and increasing its direct sales through its website.

It has increased its subscription business, not because customers are proactively choosing the offering, but because it’s cheaper to buy GoPros with the subscription than without it. At $69.99 per year, the benefits are unlimited cloud storage, broken camera replacement at a discounted fee, editing tools, live streaming functionality and discounts. GPRO has not revealed churn numbers. Subscriptions will remain attractive only if they are sticky.

Offering with subscription (GoPro)

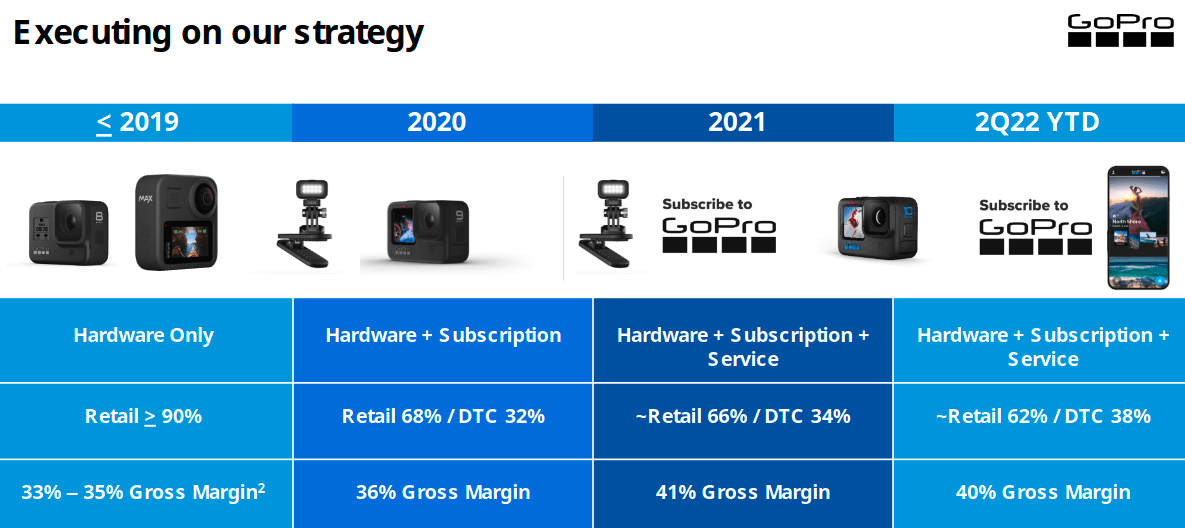

Secondly, the company has been funneling customers to their website and increasing its direct selling, which has helped grow the margin and allows the above bundle as GPRO does not have a retailer taking a cut of the revenues. This change took place over the last years in the slide below with retail at more than 90% prior to 2020 and decreasing to 62% while direct sales are at 38%.

Direct Sales and Subscriptions (Investor Presentation 2022)

Financials and valuation

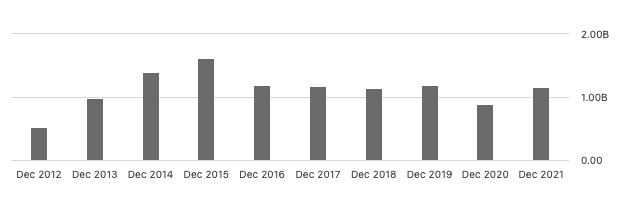

The financial performance has seen a boost from the company’s direct-to-customer subscription service business segment reaching $1.16 billion for FY21. However, revenue is less than in 2014, and fewer cameras continue to be sold. This past quarter revenue decreased by 4%, impacted by strong headwinds. We can expect the same headwinds to impact the soon-to-be-released Q4 financial report, which is historically the company’s strongest performing month due to the holiday season shopping.

Total annual revenue (Seeking Alpha)

Looking at the gross profit margin, we can see that the margin has reduced from 44.99% in 2014 to 35.40% in 2020. The company has increased its margin by introducing the recurring subscription model to 41.10% for FY21, and the TTM is at a slightly lower 39.84% due to solid headwinds for consumer discretionary products this year.

Gross profit margin (Seeking Alpha)

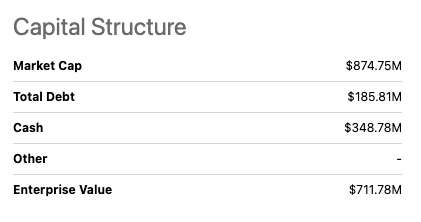

If we look at the company’s capital structure, we can see that the enterprise value is much lower than its market cap at $711.78 million due to its cash availability of $348.78 million and low total debt of $185.81 million. The company has reasonable liquidity solutions with a current ratio of 2.11 and a quick ratio of 1.47.

Capital structure (Seeking Alpha)

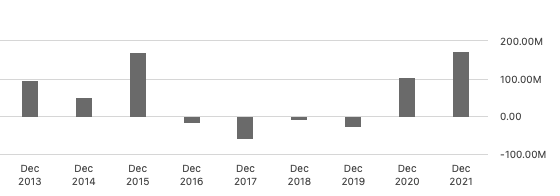

Looking at the annual trending cash flow, the subscriptions, which are asset-light, have positively impacted the cash flow at a positive $173.8 million for FY21 and $104.5 million if we look at the trailing twelve months.

Levered cash flow (Seeking Alpha)

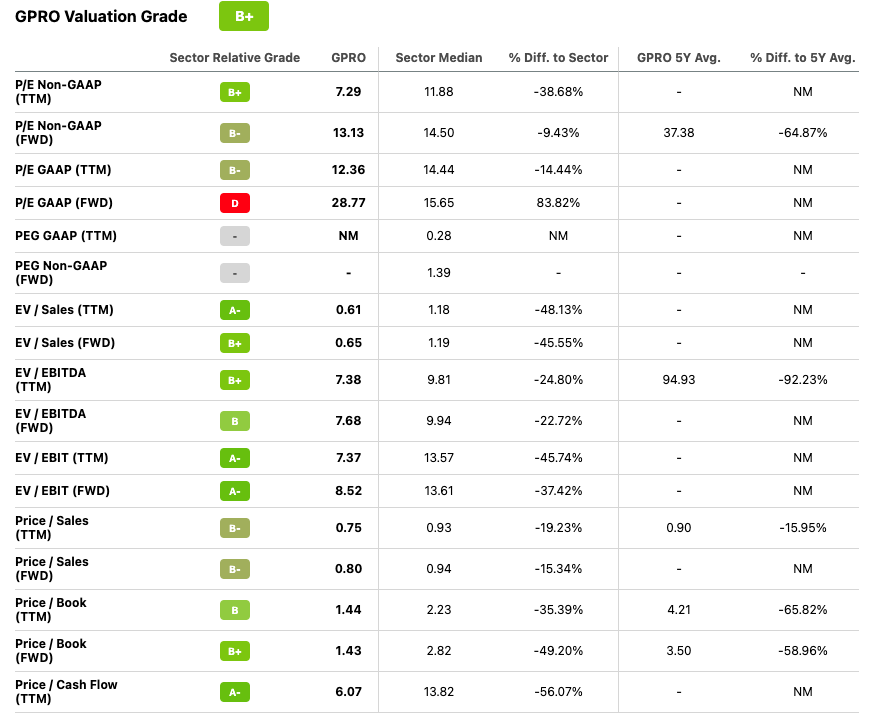

Taking Seeking Alpha’s Quant rating system, we see that GPRO performs well compared to the consumer discretionary sector with a price-to-earnings ratio of 7.29 compared to that 11.88. Price to sales is also indicating that investors are paying less than a dollar at 0.80 for every dollar the company earns in revenue, which is positive to see and may indicate the company is undervalued at this price.

Valuation (Seeking Alpha)

Risks

GPRO has seen more bad years as a publicly traded company than good ones; FY21 has been the first profitable year for GPRO since 2015. Although FY22 is en route to deliver a second consecutive year of positive earnings, growth has declined, primarily due to solid headwinds but also due to a decrease in cameras bought. While the company is benefiting from its direct sales and growth in paid subscribers, we have yet to see how sticky this business model will be. Most customers chose the subscription, not for the benefits but because it was the cheapest option. This is something we should be wary of. Furthermore, GPRO had a steep fall in the stock market due to significant missteps by the company and careless spending. The company’s fall was steep, with a lot of media coverage which has harmed the company’s reputation, and many investors may refrain from the stock for fear of getting burned again.

Final thoughts

GPRO gave a solid top and bottom line performance in 2021, and although its growth is slowing down, the company looks set to deliver another year of profitable results. It relies on recurring revenue with low costs and direct selling to increase margins. However, is this a compelling enough reason to believe the company will perform in the long run? Customers have chosen subscriptions because they are the cheaper option rather than for their perks. We will have to wait and see how sticky this recurring revenue will remain. For this reason, I recommend a hold status as we wait on the soon-to-be-released financial Q4 results.

Be the first to comment