SpVVK/iStock Editorial via Getty Images

Investment Thesis

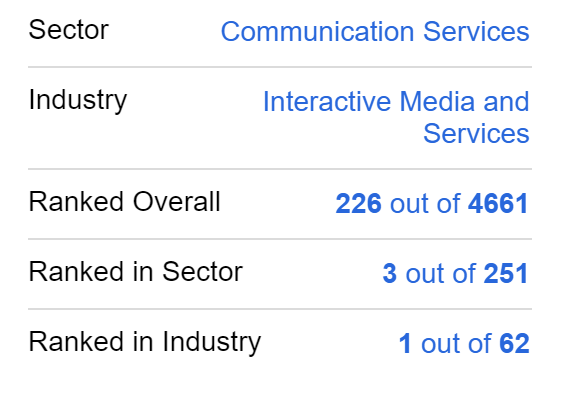

- The Seeking Alpha Quant Ranking shows excellent results for Alphabet (NASDAQ:GOOG) (NASDAQ:GOOGL): the company is ranked 1st (out of 62) within the Interactive Media and Services Industry and 3rd (out of 251) within the Communication Services Sector.

- The HQC Scorecard demonstrates that Alphabet is very attractive in terms of risk and reward: it receives an overall rating of 91 out of 100 points and is rated as very attractive in all categories (Economic Moat, Financial Strength, Profitability, Valuation, Innovation, Growth and Expected Return).

- I rate Alphabet as a strong buy: the company has impressive competitive advantages (such as its brand image, a history of successful acquisitions and integration of new businesses, as well as the ability to analyze and use its enormous amount of data), a relatively high free cash flow yield of 4.17%, high profitability (EBIT-margin of 29.65%) and strong financials (with a Moody’s credit rating of Aa2).

Alphabet’s Business Model and Competitive Advantages

The largest part of Alphabet’s revenue in 2Q22 was generated by the company’s business unit Google Advertising, which consists of the sub-units Google Search & other (which accounted for 58.40% of total revenue in 2Q22), YouTube ads (10.5%) and Google Network (11.9%). Google other accounted for 9.4% of the company’s total revenue in 2Q22 and Google Cloud for 9.0% in the same quarter. The business units hedging gains and other bets accounted for 0.5% and 0.3% of the company’s total revenue in 2Q22.

Alphabet’s results in 2Q22 show us that the Google Cloud business unit is becoming more and more important for the company. Proof of this is the fact that the unit’s revenue increased by 35% in 2Q22 as compared to the same quarter of the previous year. At the same time, Google Cloud accounted for 9% of the company’s total revenue in 2Q22 while it accounted for just 7.5% in 2Q21. The increasing share of the Google Cloud business unit compared to the company’s total revenue shows that Alphabet is getting more independent from its advertising business.

The increasing importance of Google Cloud is also underlined by this statement from Sundar Pichai, CEO of Alphabet and Google, who said:

In the second quarter our performance was driven by Search and Cloud. The investments we’ve made over the years in AI and computing are helping to make our services particularly valuable for consumers, and highly effective for businesses of all sizes. As we sharpen our focus, we’ll continue to invest responsibly in deep computer science for the long-term.”

Alphabet has several strong competitive advantages, which gives the company a wide economic moat over its competitors: it has a strong brand image, which is underlined by the fact that Google is currently ranked as the 3rd most valuable brand in the world as according to Brand Finance. Google’s brand value is estimated to be about $263,425M. The enormous amount of data and the ability to analyse and use it, provides the company with another strong competitive advantage.

Furthermore, Alphabet currently has $124,997M in Total Cash & ST Investments, which is proof of the enormous financial strength of the company. Moody’s credit rating of Aa2 is another strong indicator of Alphabet’s excellent financial situation.

In the past, Alphabet has successfully proven its ability to integrate new businesses into the company. One of its most successful acquisitions, for example, was YouTube, for which the company paid $1.65 billion back in 2006. Another successful acquisition and integration was Android, which Alphabet bought back in 2005 for $50 million. With a total of 22, Alphabet announced more acquisitions in 2021 than any other year in the past decade.

In my opinion, when investing in Alphabet, you not only invest in a financially strong company with a robust and well proven business model, but at the same time its acquisition and integration of startups enable it to maintain relatively strong growth potential. Alphabet’s Average Revenue Growth Rate of 22.88% over the last 5 year is an additional indicator of the company’s excellent growth perspectives.

All of these competitive advantages contribute significantly to my strong buy rating on the Alphabet stock.

Overview: Alphabet

|

Company |

Alphabet |

|

Sector |

Communication Services |

|

Industry |

Interactive Media and Services |

|

Market Cap |

$1.54T |

|

Employees |

174,014 |

|

Revenue [TTM] |

$278.14B |

|

Operating Income |

$82.46B |

|

Revenue 3 Year Growth [CAGR] |

29.41% |

|

Revenue 5 Year Growth [CAGR] |

22.88% |

|

Gross Profit Margin |

56.74% |

|

EBIT Margin |

29.65% |

|

Return on Equity |

29.22% |

|

Free Cash Flow Yield |

4.17% |

|

Dividend Yield |

0% |

Source: Seeking Alpha

Alphabet’s Valuation

Discounted Cash Flow [DCF]-Model

In terms of valuation, I have used the DCF Model to determine the intrinsic value of Alphabet. The method calculates a fair value of $162.61. The current stock price is $118.20, which results in an upside of 37.60%.

Alphabet’s Average Revenue Growth [FWD] Rate of the last 5 years is 19.53%. I have made more conservative assumptions and for my DCF Model have assumed a Revenue and EBIT Growth Rate of 10% for the company over the next 5 years. Furthermore, I assume a Perpetual Growth Rate of 4%. Due to Alphabet’s strong competitive advantages, I expect it to grow slightly above the United States’ Average GDP Growth Rate of 3%. I have used Alphabet’s current discount rate [WACC] of 8% and Tax Rate of 16.2%. Furthermore, I used an EV/EBITDA Multiple of 14.6x, which is the company’s latest twelve months EV/EBITDA.

Based on the above, I calculated the following results:

Market Value vs. Intrinsic Value:

|

Market Value |

$118.20 |

|

Upside |

37.60% |

|

Intrinsic Value |

$162.61 |

Source: The Author

Relative Valuation Models

Alphabet’s P/E [FWD] Ratio

Alphabet’s P/E Ratio is 22.59, which is 19.55% below its average of the last 5 years (28.08), thus providing an indicator that the company is undervalued.

Alphabet’s Free Cash Flow Yield

Alphabet currently shows a Free Cash Flow / Share [TTM] of $4.93. At the company’s current stock price of $118.20, this results in a Free Cash Flow Yield of 4.17%. This means that in theory, Alphabet would be able to pay a dividend of 4.17%.

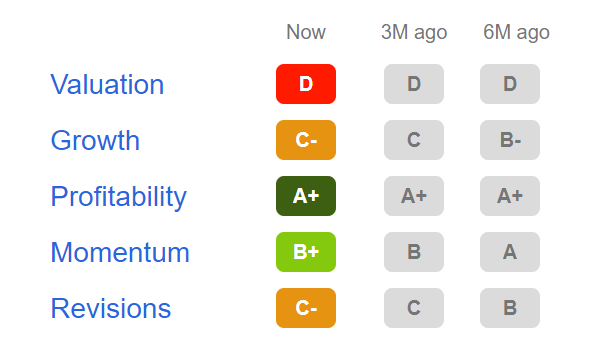

Alphabet According to the Seeking Alpha Factor Grades

According to Seeking Alpha’s Factor Grades, Alphabet is rated with a D in terms of Valuation. For Growth, the company gets a C- rating. In terms of profitability, Alphabet is rated with an A+. For Momentum, it gets a B+ and for Revisions, a C- rating.

Source: Seeking Alpha

Alphabet According to the Seeking Alpha Quant Ranking

The Seeking Alpha Quant Ranking places Alphabet 1st (out of 62) within the Interactive Media and Services Industry and 3rd (out of 251) within the Communication Services Sector.

Source: Seeking Alpha

Alphabet’s excellent rating as according to the Seeking Alpha Quant Ranking, strengthens my belief that the company is a strong buy and reinforces the theory of it being a very attractive option compared to its competitors.

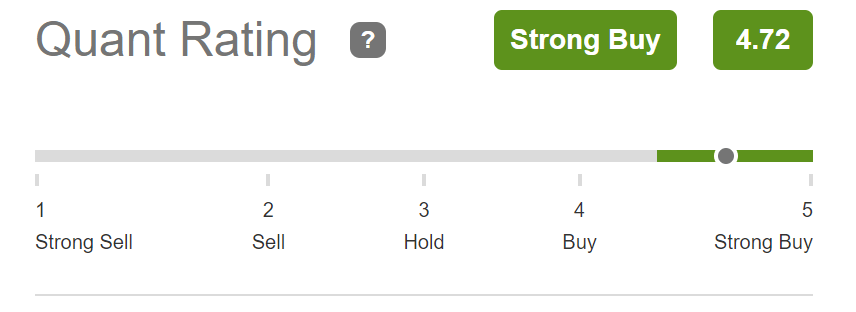

Alphabet According to the Seeking Alpha Quant Rating

According to the Seeking Alpha Quant Rating, Alphabet is rated as a strong buy, which once again underlines my own strong buy rating for the company.

Source: Seeking Alpha

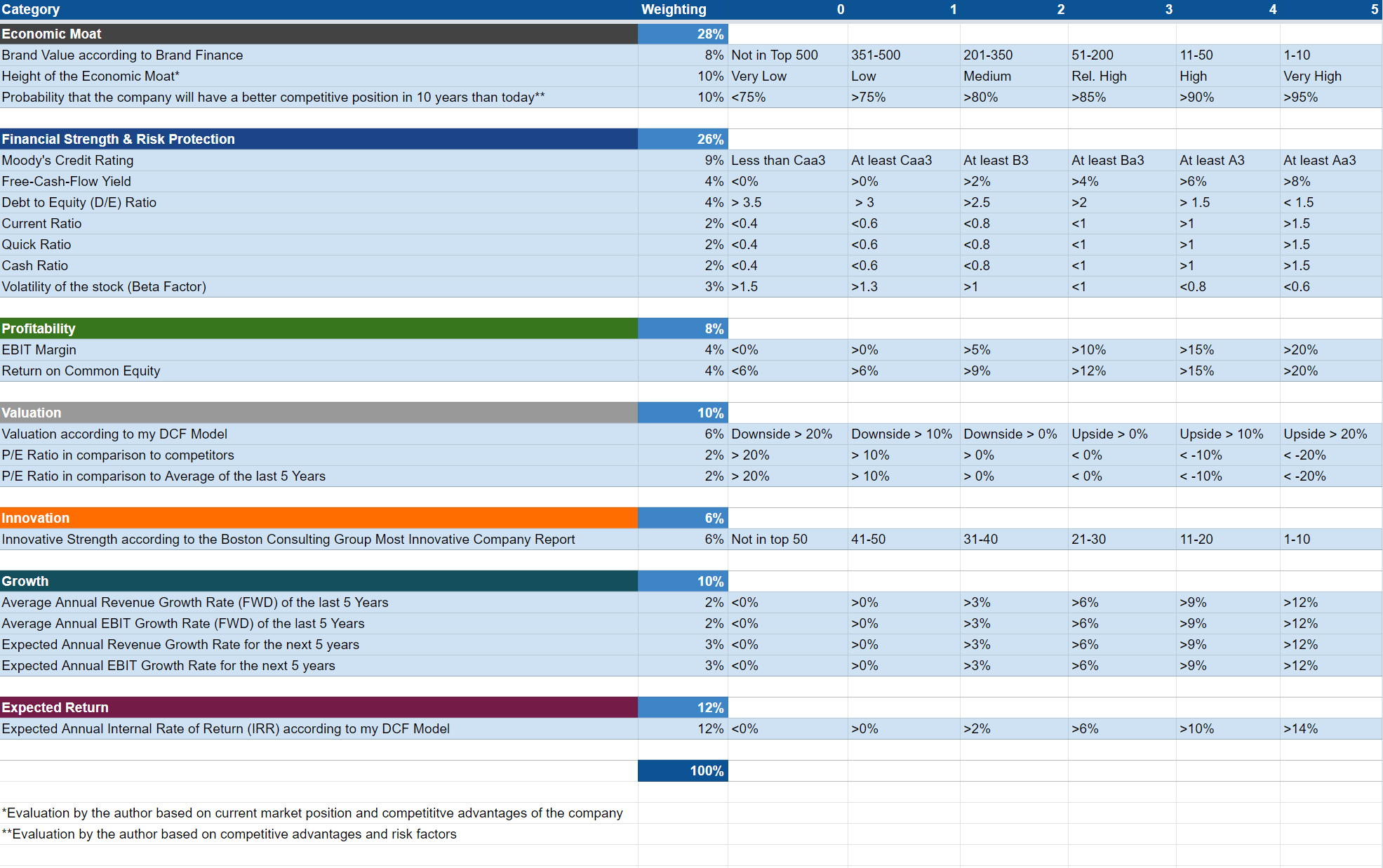

The High-Quality Company [HQC] Scorecard

“The HQC Scorecard aims to help investors identify companies which are attractive long-term investments in terms of risk and reward.” Here, you can find a detailed description of how the HQC Scorecard works.

Overview of the Items on the HQC Scorecard

“In the graphic below, you can find the individual items and weighting for each category of the HQC Scorecard. A score between 0 and 5 is given (with 0 being the lowest rating and 5 the highest) for each item on the Scorecard. Furthermore, you can see the conditions that must be met for each point of every rated item.”

Source: The Author

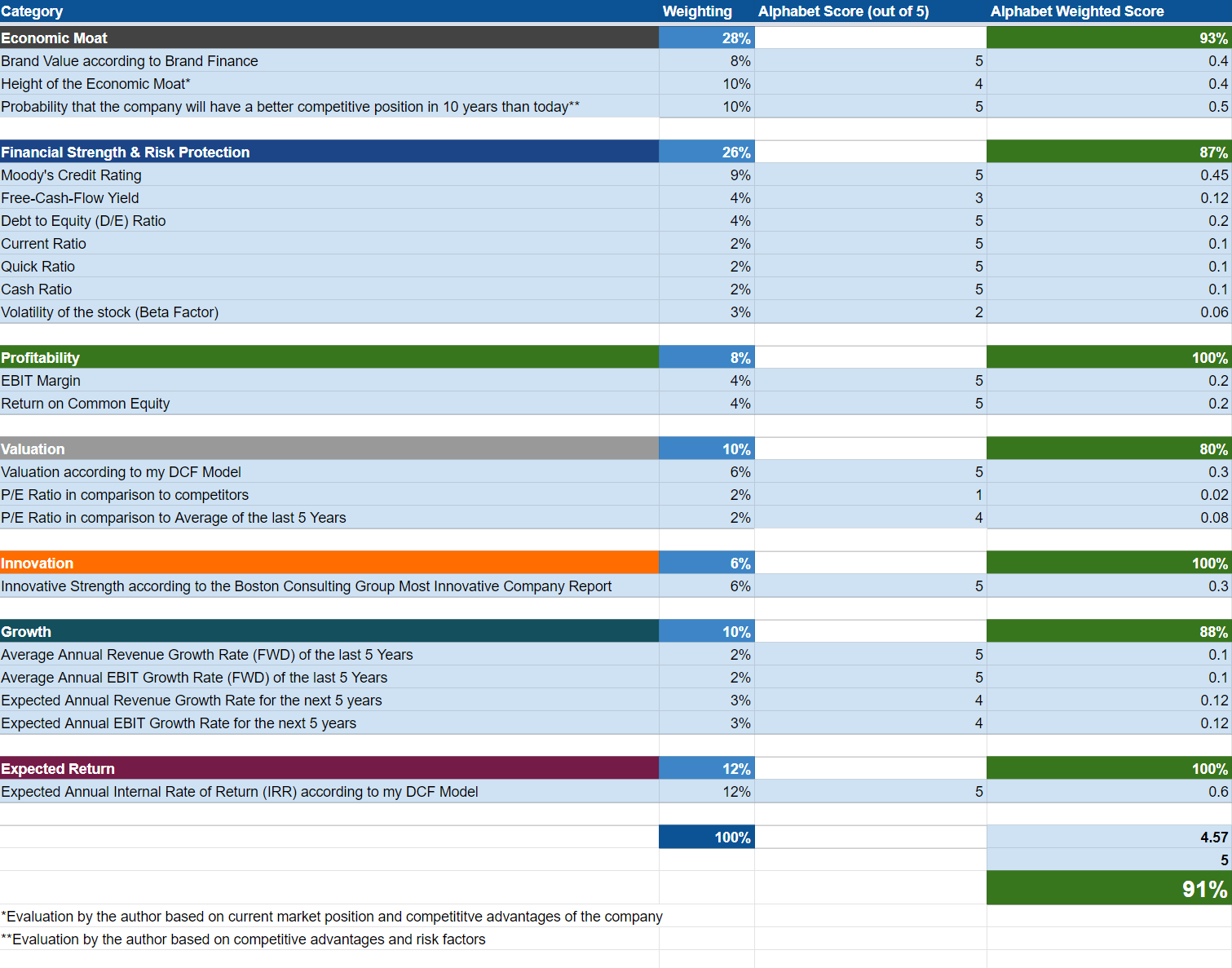

Alphabet According to the HQC Scorecard

Source: The Author

According to the HQC Scorecard, Alphabet has an overall score of 91 out of 100 points. In terms of risk and reward, this means it can be classified as a very attractive long-term investment.

The HQC Scorecard indicates that Alphabet is rated as very attractive in all categories. This includes Economic Moat, Financial Strength, Profitability, Valuation, Innovation, Growth and Expected Return.

This very attractive overall scoring strengthens my belief that Alphabet can be considered as a very appealing long-term investment.

Risk Factors

One potential risk factor I see for Alphabet is the fact that the largest part of the company’s revenue (more than 80%) is generated by its business unit Google Advertising. Reduced spending in advertising by Alphabet’s clients could adversely affect its business and therefore result in decreasing profit margins. However, as shown in this analysis, Alphabet’s other business units are becoming more and more important: proof of this, for example, is the fact that Google Cloud already accounted for 9% of the company’s total revenue in 2Q22 while it accounted for only 7.5% in the same quarter of the previous year.

Another risk factor I see regarding an investment in Alphabet, is the fact that the company faces intense competition in some of the industries it operates. Regarding YouTube, for example, the company competes with financially strong competitors such as Amazon (NASDAQ:AMZN), Netflix (NASDAQ:NFLX), Apple (NASDAQ:AAPL) and Walt Disney (NYSE:DIS).

Additionally, Alphabet faces increased regulatory scrutiny, such as antitrust complaints made against Google. However, the strong financial health of the company, proved by Moody’s credit rating of Aa2 and the high amount of cash it has available ($124,997M in Total Cash & ST Investments), are strong indicators that future penalties should not pose significant financial problems.

The Bottom Line

Alphabet has strong competitive advantages over its rivals: the company has a strong brand image, high financial strength (proved by a Moody’s credit rating of Aa2) and a high cash position ($124,997M in Total Cash & ST Investments). Furthermore, it’s getting more independent from its Advertising business unit. Additionally, the enormous amount of data and the ability to analyze and use it, provides the company with another long-term competitive advantage.

Alphabet’s strong ranking, according to the Seeking Alpha Quant Ranking, underlines the company’s excellent position within its sector: Alphabet is ranked 1st (out of 62) within the Interactive Media and Services Industry and 3rd (out of 251) within the Communication Services Sector.

According to the Seeking Alpha Quant Rating, Alphabet is rated as a strong buy, which underlines its very attractive rating in terms of risk and reward as according to the HQC Scorecard. The HQC Scorecard, gives an overall score of 91 out of 100 points and the company is rated as very attractive in all categories (Economic Moat, Financial Strength, Profitability, Valuation, Innovation, Growth and Expected Return).

These are all indicators that strengthen my belief that Alphabet is currently a strong buy.

Be the first to comment