narvikk

Container shipowners such as Global Ship Lease (NYSE:GSL) have been reaping the benefits of high post-COVID charter rates, putting up big revenue and earnings growth numbers. While those very high rates are expected to subside in 2023, recent rate declines have been mild for sub-10,000 TEU vessels, GSL’s focus area.

Company Profile:

Global Ship Lease, Inc. owns and charters container ships of various sizes under fixed-rate charters to container shipping companies. It owns 65 containerships, ranging from 1,118 to 11,040 TEU, with an aggregate capacity of 342,348 TEU. 32 ships are wide-beam Post-Panamax. The company was founded in 2007 and is based in London, the United Kingdom. (GSL site)

Charter Rates:

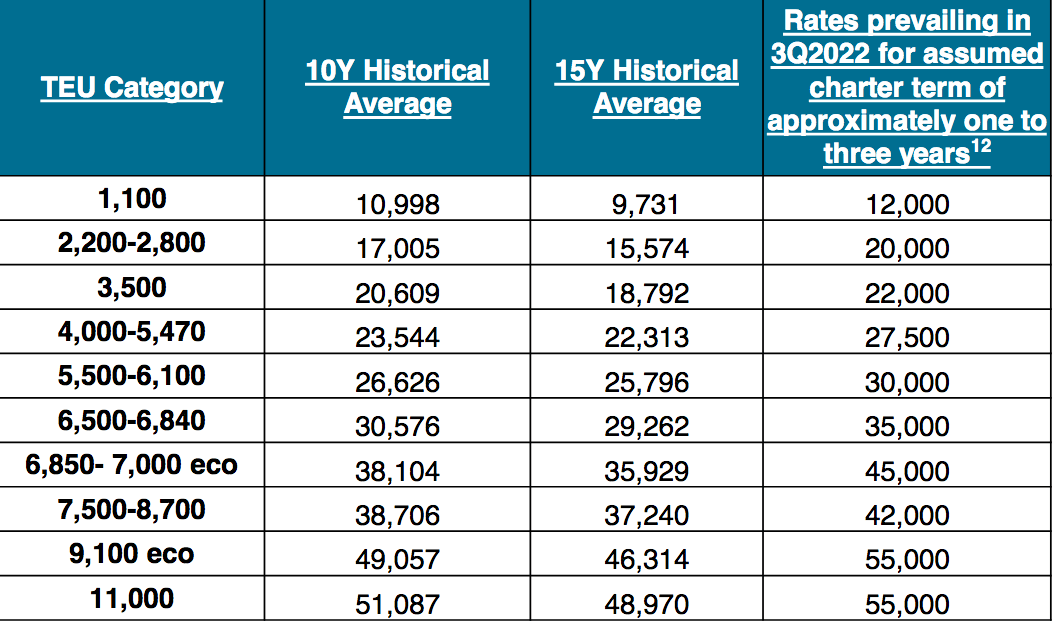

In its Q3 ’22 presentation, GSL listed prevailing October ’22 daily rates for sub-10,000 TEU vessels, ranging from $12K for 1,100 TEU size, to $42K for 7,500-8,700 TEU size.

GSL

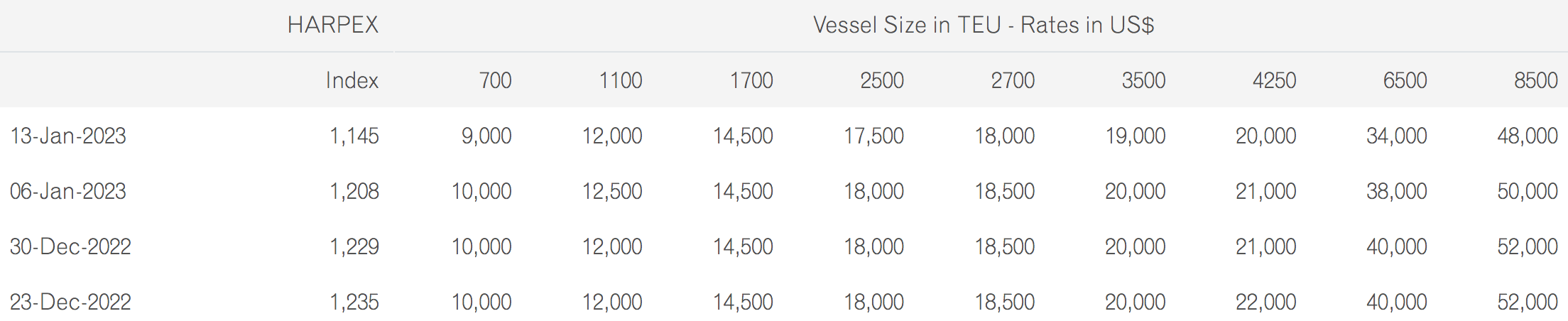

For the period of 12/23/22 to 01/13/23, the Harpex Index shows rates declining more for the bigger ships: ~8% for 8500 TEU vessels, ~15% for 6500 TEU vessels, 9% for 4250 TEU vessels, and 10% for 3500 TEU vessels.

The declines were much lower for 2500 TEU to 2700 TEU vessels, at ~3%, and were flat for 1100 to 1700 TEU ships. The smallest category listed, 700 TEU had a 10% rate decline.

Surprisingly, the 8500 TEU size category’s charter rates were roughly higher as of 1/13/23 in this chart, at $48K for vs. $42K for 7500-8700 TEU sizes in the October chart that GSL published. Most other rate categories were lower however, as of 1/13/23:

Harpex

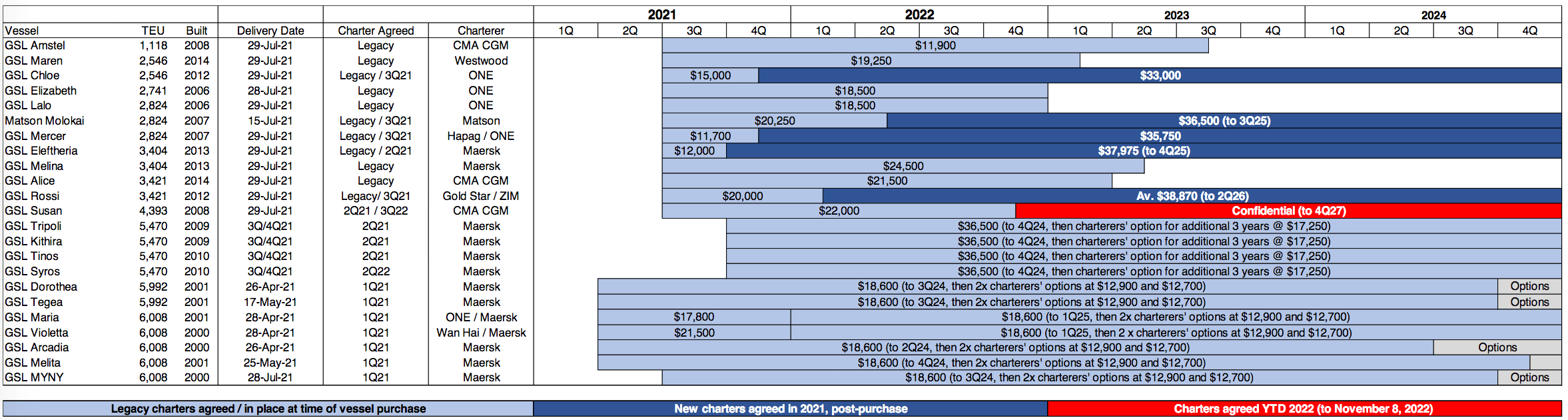

Between Jan. 1 and Aug. 3, 2022, management contracted ~$435.5M of additional revenues for its fleet, including five forward fixtures of charters of four to five years duration each, 1 one prompt fixture of just over three years, and three charter extension options of 12 months. These charters were renewed in a rising market, locking in increased forward cash flows even before the accretive impact of 2021 acquisitions.

GSL’s fleet had an average remaining charter length of 2.9 years, with $2.23B in contracted revenues as of 9/30/22. GSL had no exposure to the spot market in Q4 2022, with 91% of fleet ownership days in 2023 covered.

Management acquired several vessels in 2021, and chartered them at high rates, mostly into 2024, adding $920M in revenue, ($770M was added in the third quarter alone.) This gives GSL over $2B of contracted revenue spread over just under three years, which should support its earnings and cash flow in 2023 and 2024.

(Sorry for the tiny print in this table – if you double-click on this image, you should be able to read this date more easily.)

GSL site

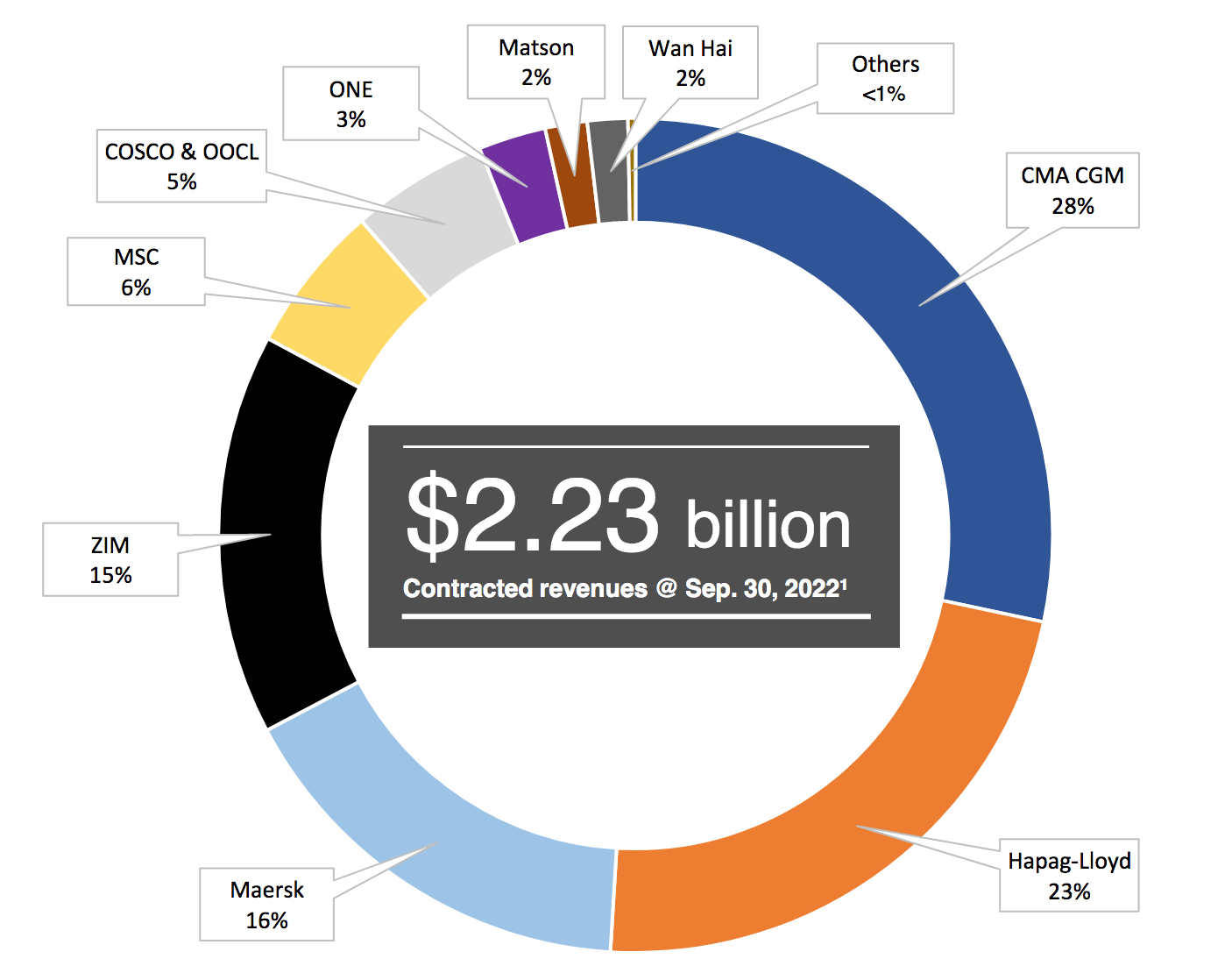

While GSL’s customer base has diversified over the years, there’s still 28% exposure to CMA CGM, its biggest customer. Hapag-Lloyd, Maersk, and ZIM are next in line, accounting for 54% of GSL’s contracted revenue:

GSL site

Earnings:

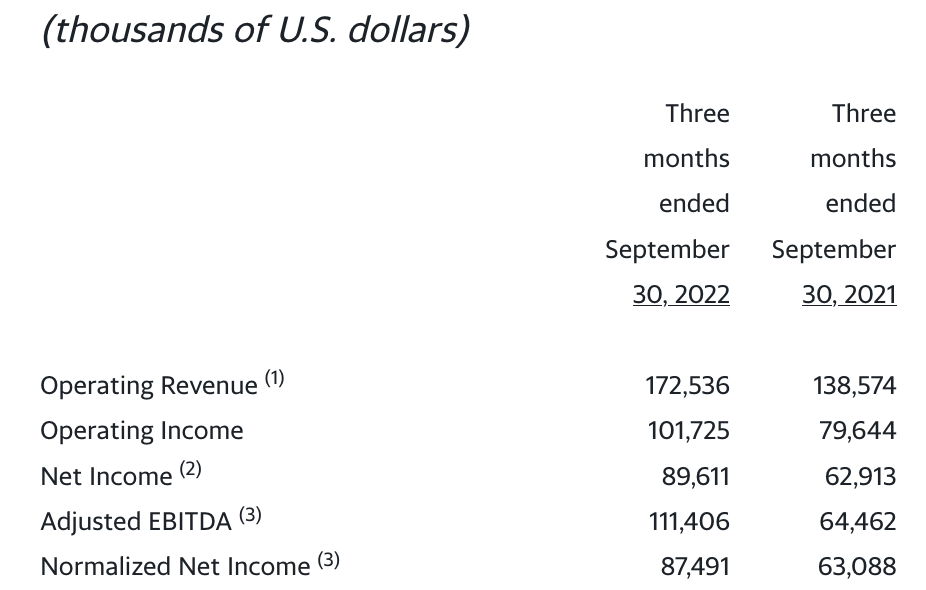

Q3 2022: Those additional charters at higher rates converted into strong revenue and earnings growth for GSL in 2022. Operating revenue rose 25%, net income grew 42%, and adjusted EBITDA jumped 73% in Q3 ’22, vs. Q3 ’21:

GSL site

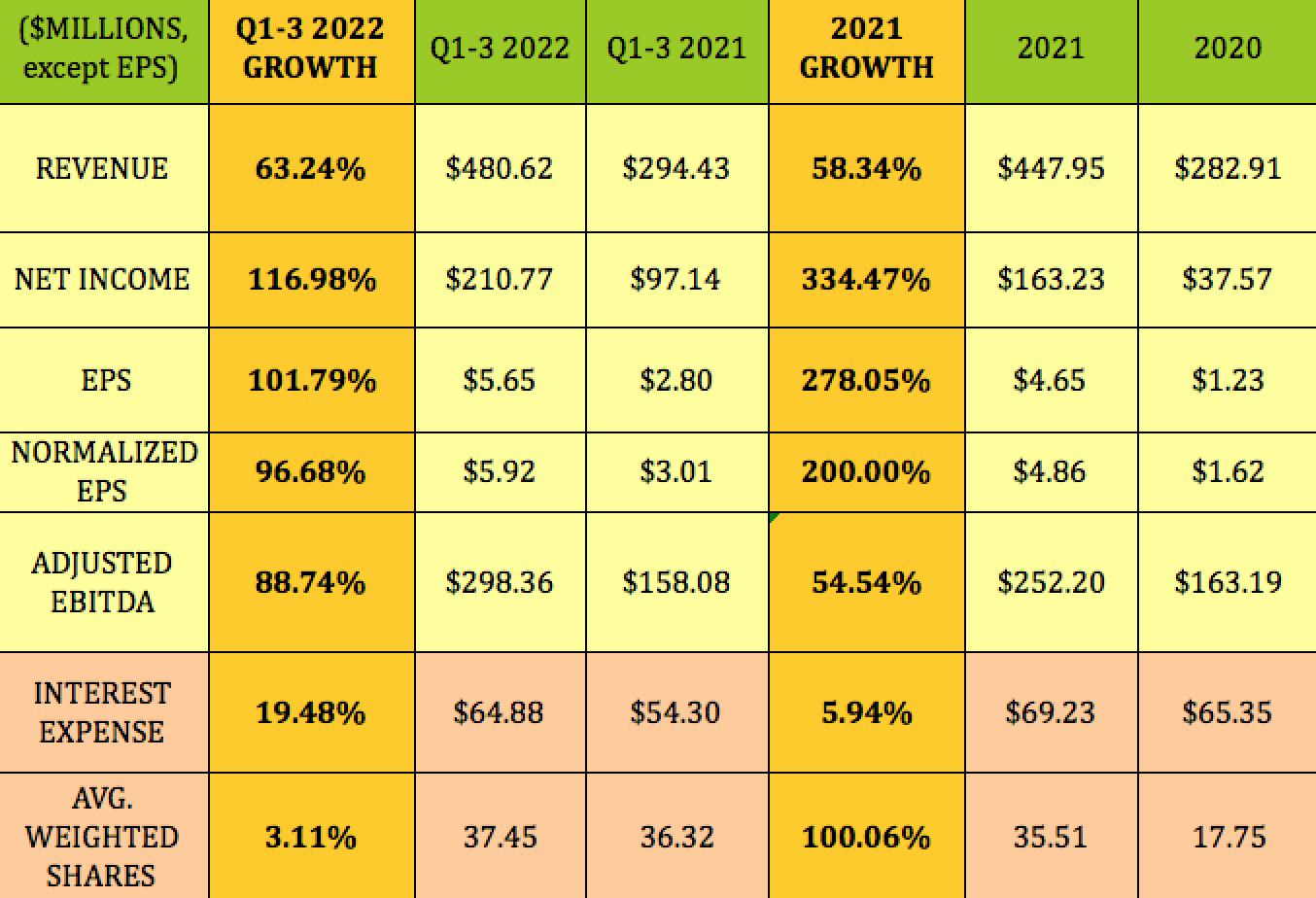

Q1 -3 2022: The larger fleet and contracted rates continued to boost GSL’s earnings in Q1-3 ’22, with three-digit net income and EPS growth, and 2-digit revenue and adjusted EBITDA growth. Interest expense grew 19.5%, due to the larger asset base, while the unit count rose ~3%.

2021 was a big year for GSL, as earnings bounced back from the pandemic’s effects in 2020, with three-digit growth.

Hidden Dividend Stocks Plus

Dividends:

After not paying a dividend in 2016 – 2020, management began paying a $.25 quarterly dividend in Q2 ’21. They increased the dividend by 50% in Q2 to $0.375/share.

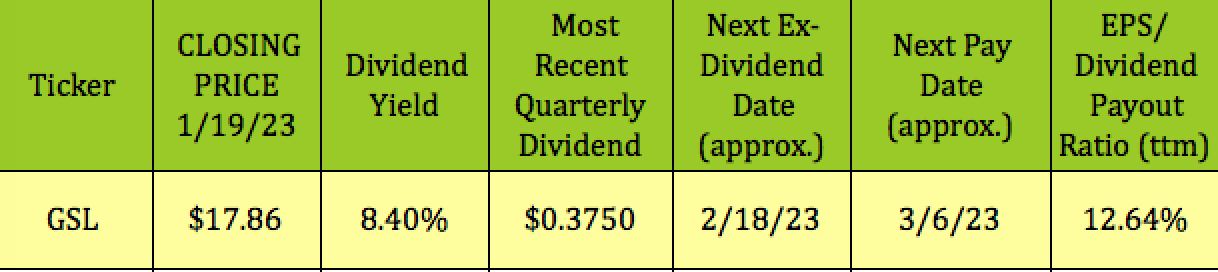

At its 1/19/23 closing price of $17.86, GSL yields 8.40%. It should go ex-dividend next on ~2/18/23, with a ~3/6/23 pay date.

Hidden Dividend Stocks Plus

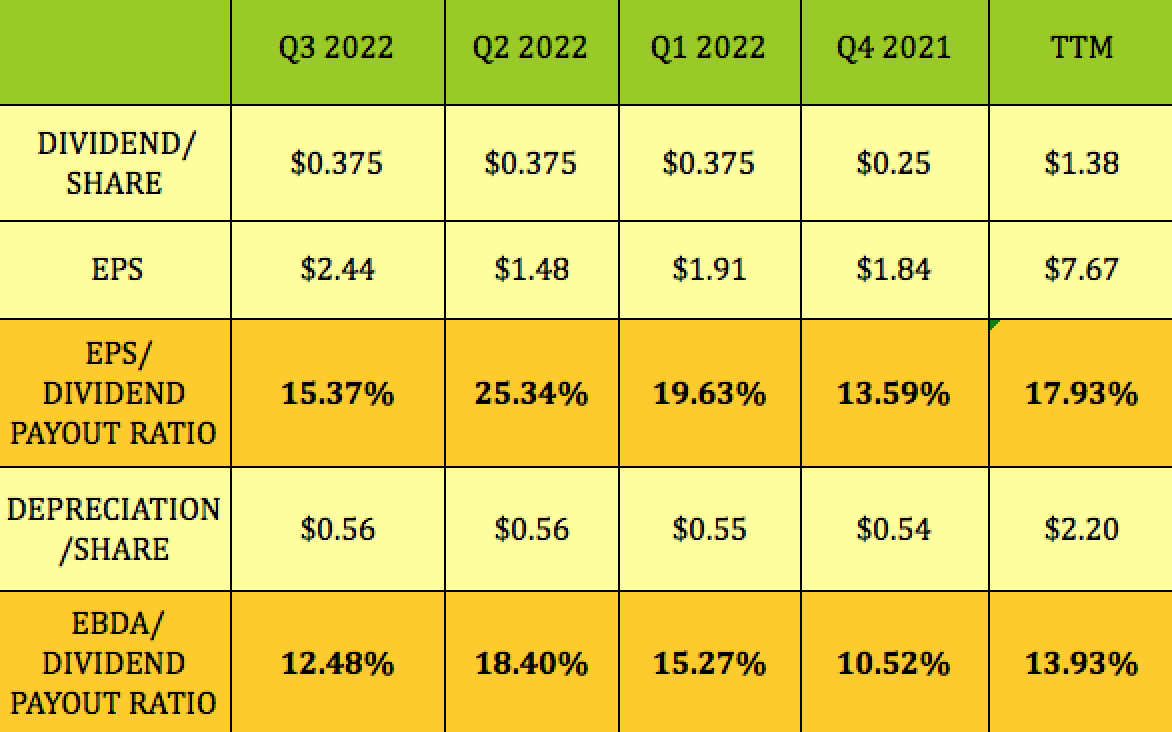

GSL’s dividend coverage has been strong, with low EPS dividend payout ratios ranging from 13.59% to 25.34% over the past four quarters. Q3 ’22 payout ratio came in at 15.37%, with a trailing EPS/dividend payout ratio of 17.93%.

However, EPS includes non-cash depreciation and amortization of $.54 to $.56/share each quarter. Stripping out those non-cash D&A expenses shows a very low 12.48% payout ratio on Q3 ’22, and an average dividend payout ratio of 13.93% over the past 12 months:

Hidden Dividend Stocks Plus

GSL also has a preferred B series with an 8.75% rate dividend, which was selling at ~$25.05 on 1/19/23.

Taxes:

“Distributions we pay to U.S. unitholders will be treated as a dividend for U.S. federal income tax purposes to the extent the distributions come from earnings and profits (E&P) and as a non-dividend distribution or a return of capital – ROC – to the extent the distributions exceed E&P.” (GSL site)

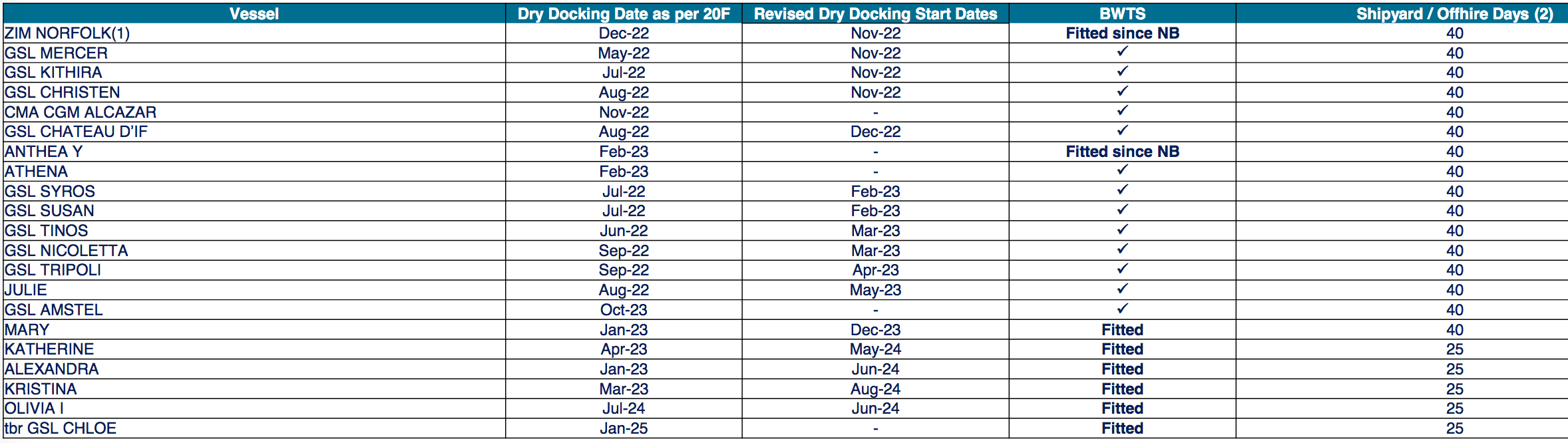

Drydockings and BWTS Fitting:

GSL has seven vessels scheduled for 40-day drydocking in 2023. However, they’ve all already been fitted with the required BWTS – ballast water treatment systems.

GSL site

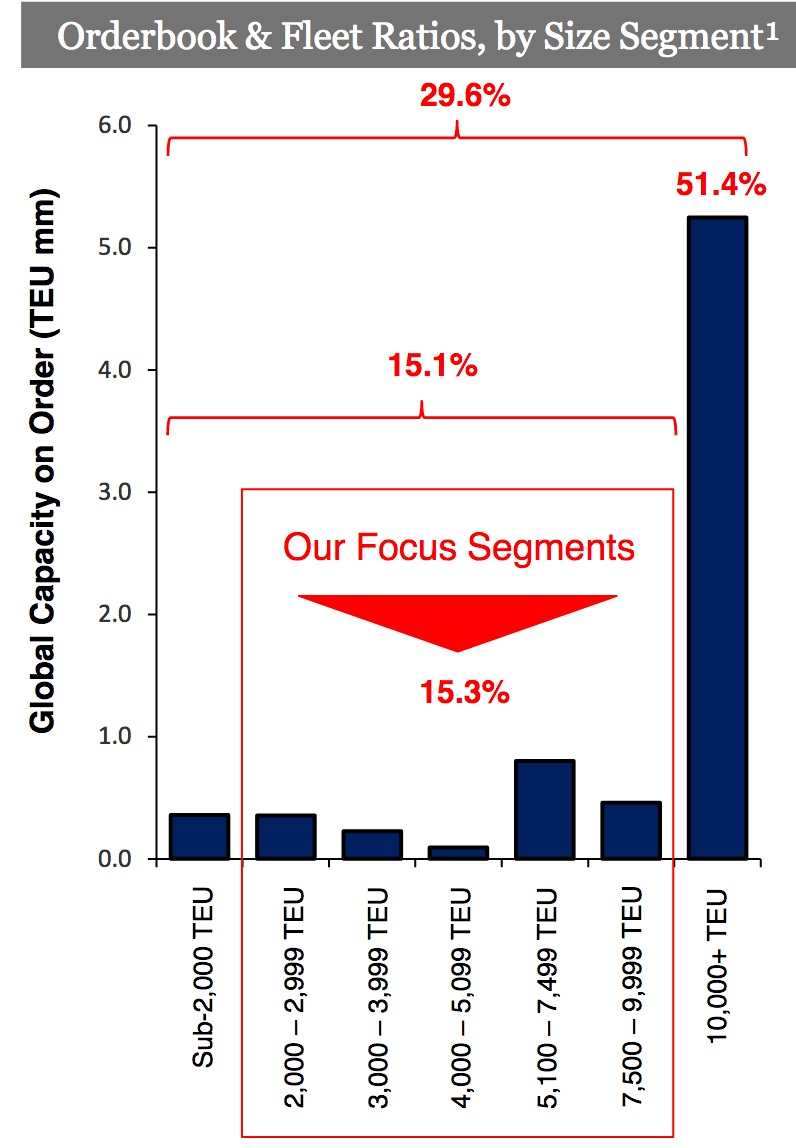

Industry Tailwinds:

The industry’s order book for new vessels is growing rapidly, up 51%, for larger, 10K-plus TEU vessels, but, fortunately for GSL, not as much for smaller, sub-10K TEU vessels, its area of focus, with those sizes up just 15%.

GSL site

Environmental regulations will also put pressure on vessels, effectively slowing them down, which creates more ton-miles, and subsequent demand.

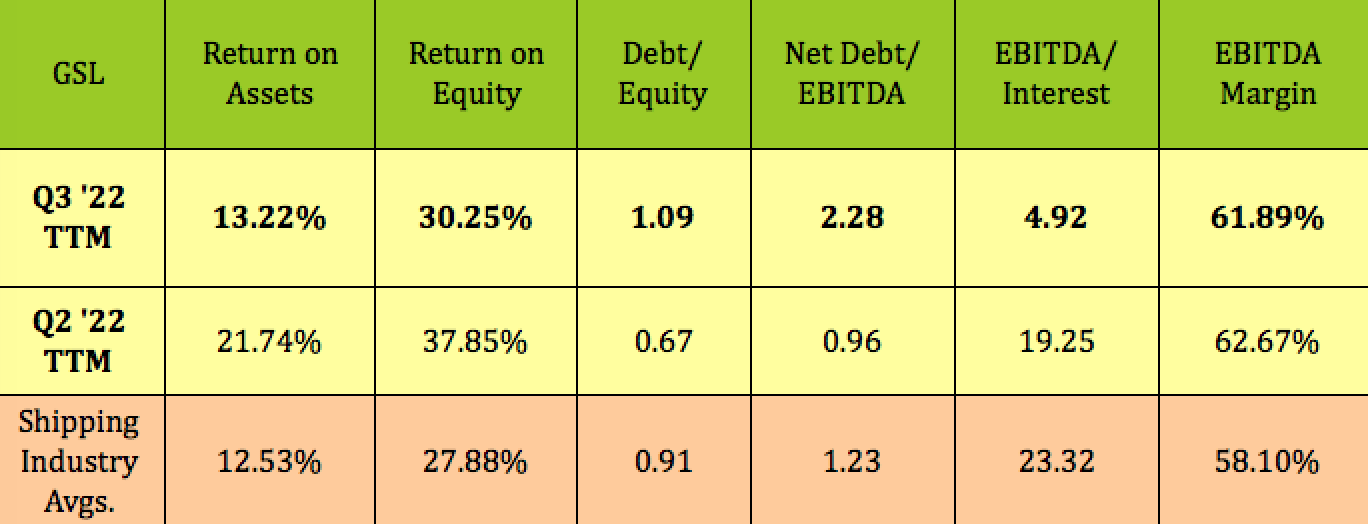

Profitability and Leverage:

The increased asset base required higher debt and interest, which raised GSL’s debt leverage ratios and lowered its ROA and interest coverage. However, as noted in the next section, the debt is fully hedged.

Hidden Dividend Stocks Plus

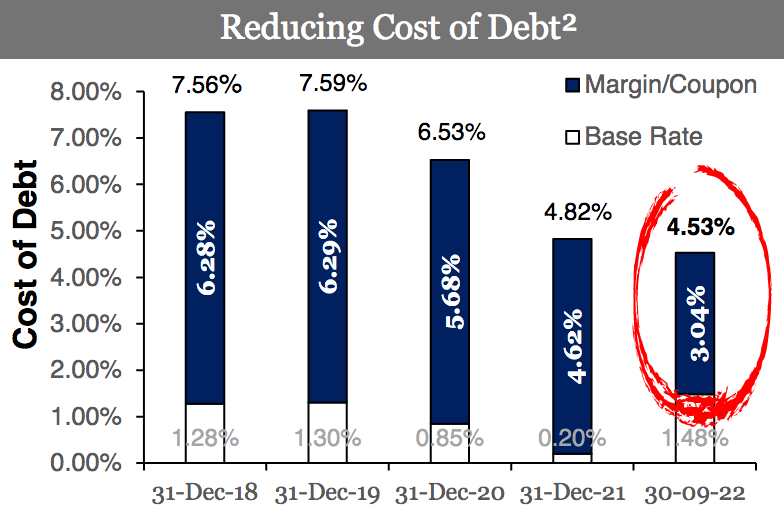

Debt and Liquidity:

GSL has no debt maturities before 2026, and an overall low cost of debt despite the global high interest rate environment, with all of its floating interest rates fully hedged, capping the floating rate at 75 basis points, with a weighted average cost of debt of 4.53%.

GSL site

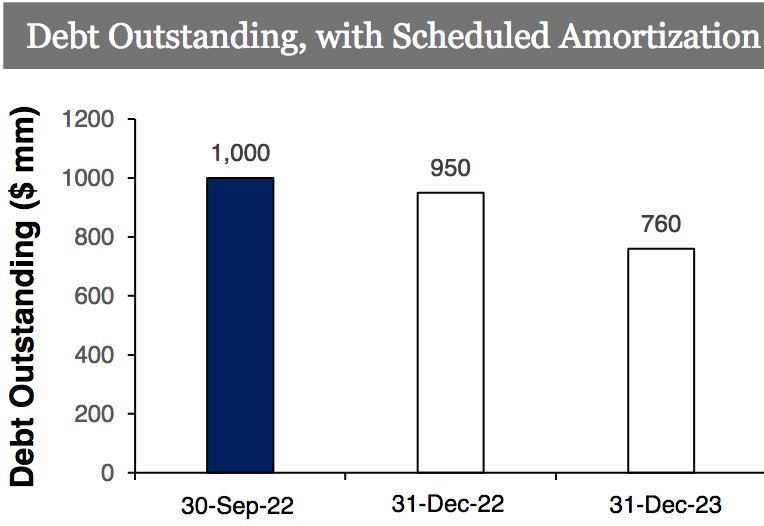

Management projects a ~24% reduction in outstanding debt by 12/31/2023, which will improve GSL’s debt leverage ratios.

GSL site

In the third quarter, management completed the U.S. private placement of $350M of privately rated investment-grade debt price at a fixed rate of 5.69%, which it used to fully redeem its more expensive 8% senior unsecured notes due 2024, the Hayfin credit facility due in 2026, and the Hellenic facility due in 2024.

As of 9/30/23, GSL had $97M in unrestricted cash. Its debt is rated BB Stable by Standard & Poor’s, and B-1 positive by Moody’s.

Performance:

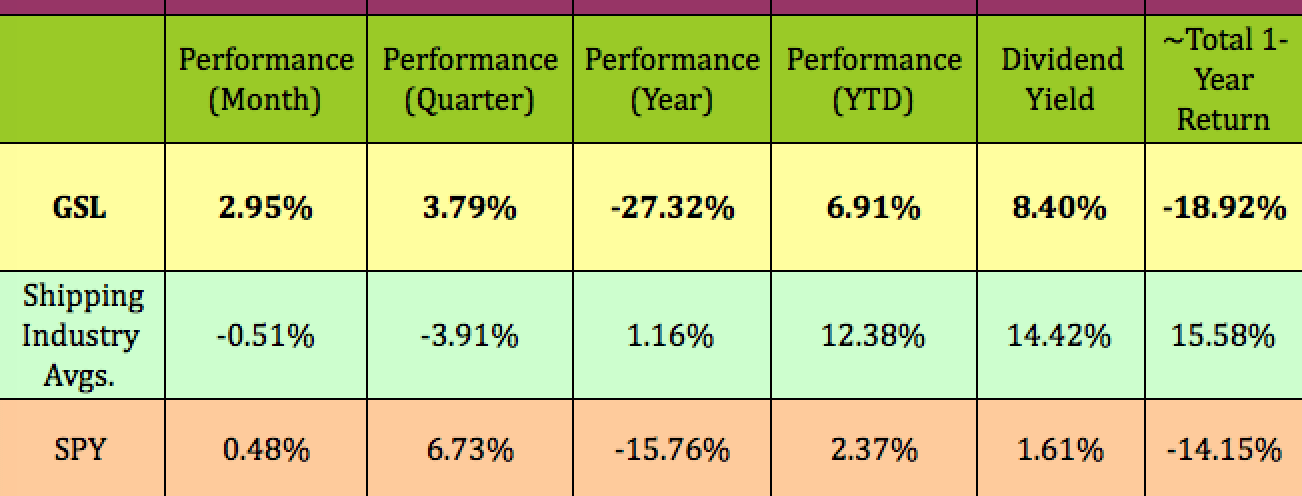

GSL has outperformed the S&P 500 over the past month and so far in 2023, but lagged it over the past quarter and year. It has outperformed the Marine Shipping industry over the past month and quarter, but has lagged over the past year and in 2023.

Hidden Dividend Stocks Plus

Analyst Targets:

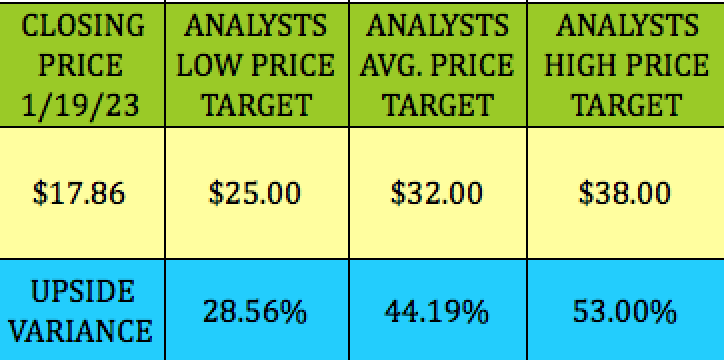

At its 1/19/23 closing price of $17.86, GSL is 28.56% below analysts’ lowest price target, and 44% below the $32.00 average price target. However, these price targets are old, from Q3 ’22.

Hidden Dividend Stocks Plus

Valuations:

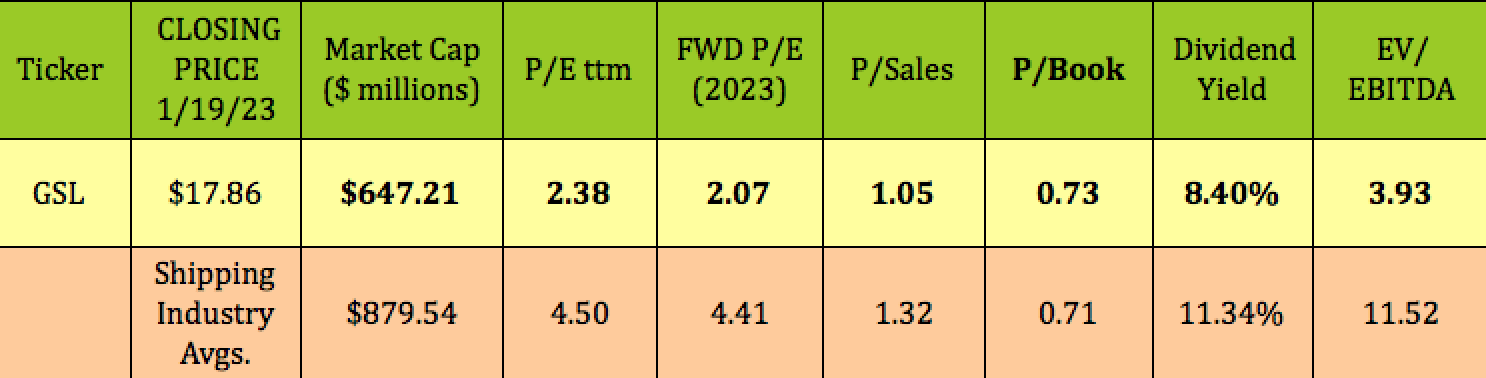

GSL looks undervalued on both a trailing P/E and forward P/E basis, with a trailing P/E of 2.38X, vs. the Marine Shipping industry average of 4.5X, and an even lower forward P/E of 2.07X, less than 50% of the industry’s 4/41X average.

GSL’s P/Sales is somewhat lower, while its P/Book is in line. Its EV/EBITDA is very low, at 3.93X, vs. the industry’s 11.52X average.

Hidden Dividend Stocks Plus

Parting Thoughts:

We rate GSL as a BUY. Although charter rates are falling, GSL’s contracted charter contracts will support further earnings growth in 2023, and stable earnings in 2024. Its balance sheet will continue to improve over the next year. With its strong dividend coverage, GSL’s attractive $.375 quarterly distributions should be ongoing.

All tables furnished by Hidden Dividend Stocks Plus, unless otherwise noted.

Be the first to comment