Vershinin-M/iStock via Getty Images

Investment Thesis

It is evident by now that the COVID-19 pandemic has been more than good to Trade Desk, Inc. (NASDAQ:TTD), given the massive growth in its revenues and gross profits by now. With the global digital advertising and marketing spending expected to grow from $350B in 2020 to $786.2B in 2026 at a CAGR of 14.44%, there is every reason for TTD’s success ahead indeed post-reopening cadence, since the global connected TV advertising market is also expected to expand from $16.56B in 2021 to $32.56B in 2026 at a CAGR of 14.48%. Its market share in the ad-tech segment has also grown impressively, from 8% in Q1’22 to 9.24% as of August 2022.

With the aid from increased political ad spending surrounding Mid-Term Elections in November, its long-term partnership with Disney (DIS) (and speculatively with Netflix (NFLX) in the future), and the massive growth in shopper marketing in the global e-commerce space, amongst others, we expect to see an easy upwards rerating of TTD’s revenue and profitability growth ahead.

Therefore, long-term investors should simply sit tight and enjoy the ride, since we expect its CTV segment to outperform despite the ad-pocalyse reported by Alphabet (GOOG) and Meta (META). Stellar indeed, due to TTD’s long runway for growth in the massive Total Addressable Market of $750B in global ad spending.

TTD’s Management Has Proven To Be More Than Stellar Thus Far

S&P Capital IQ

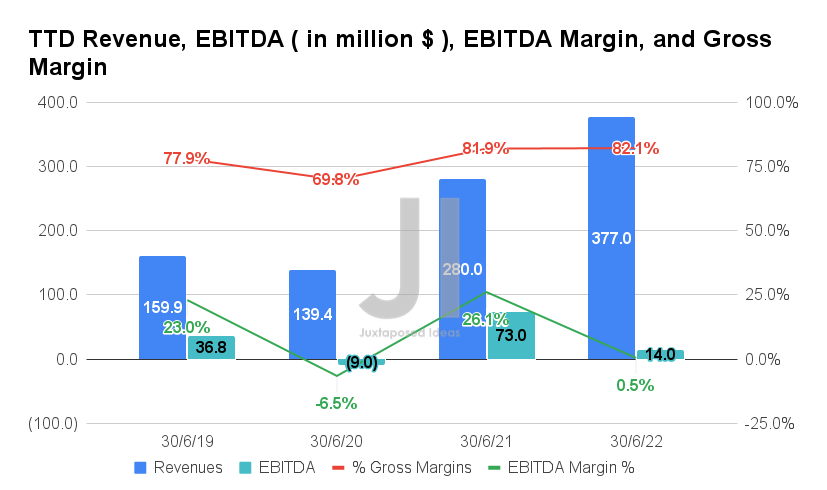

In FQ2’22, TTD reported revenues of $377M and gross margins of 82.1%, representing a massive growth of 34.6% though mostly inline YoY, respectively. Otherwise, a remarkable increase of 4.2 percentage points in gross margins from FQ2’19 levels, despite the rising inflation in current worsening macroeconomics. In the meantime, the company’s profitability has taken a hit, with an EBITDA of $14M and an EBITDA margin of 0.5% in FQ’22, representing a YoY decline of 80.8% and 25.6 percentage points, respectively.

S&P Capital IQ

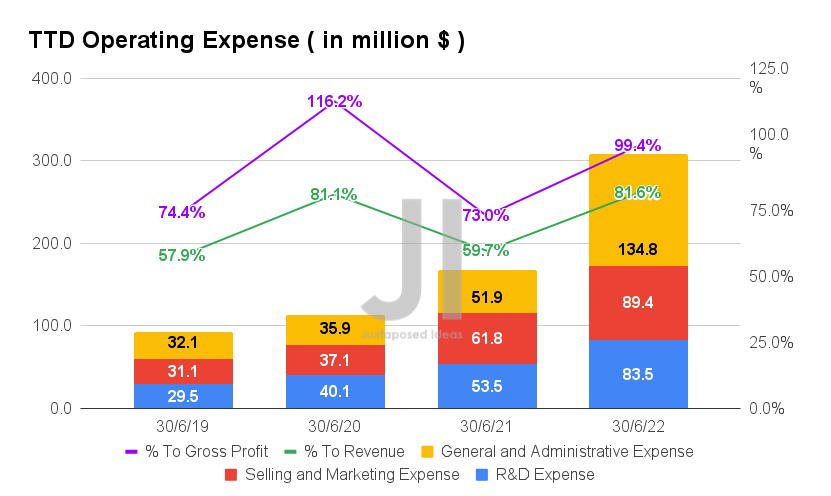

This is mostly attributed to TTD’s elevated operating expenses of $307M in FQ2’22, representing an immense increase of 83.6% YoY and 331.1% from FQ2’19 levels. This has directly impacted the ratio of its growing sales to 81.6% of its revenues and 99.4% of its gross profits in FQ2’22, compared to 59.7%/ 73% in FQ2’21 and 57.9%/ 74.4% in FQ2’19, respectively. Thereby, noticeably affecting TTD’s operating income by -97.1% YoY, from $61.95M in FQ2’21 to $1.74M in FQ2’22.

S&P Capital IQ

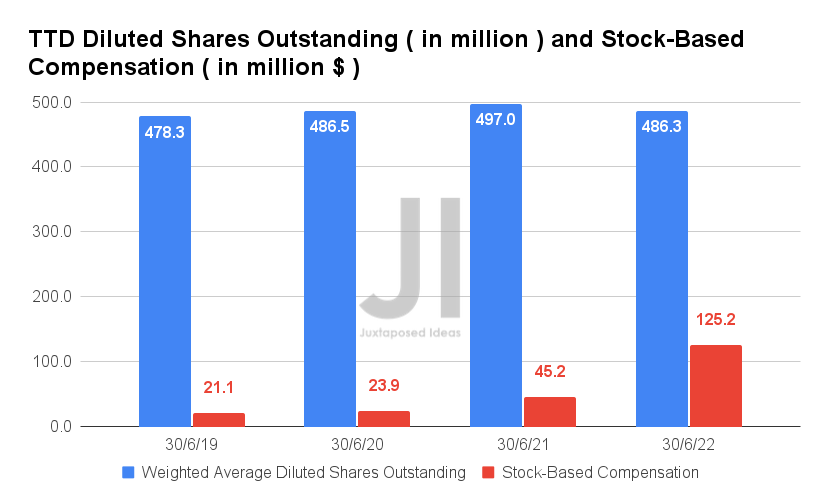

However, it is also important to note that part of the higher operating expenses was attributed to TTD’s elevated Stock-Based Compensation (SBC) expenses of $125.2M in FQ2’22, representing a massive increase of 276.9% YoY. In addition, the company reported $455.51M in SBC expenses for the past three quarters, up 345% from $132.01M three quarters earlier. Therefore, naturally impacting its profitability at the same time.

Nonetheless, it is also essential to note that despite the massive growth in its SBC expenses, TTD’s diluted shares outstanding have remained stable thus far, with 486.3M reported in FQ2’22. Therefore, asserting confidence in its long-term investors for now.

S&P Capital IQ

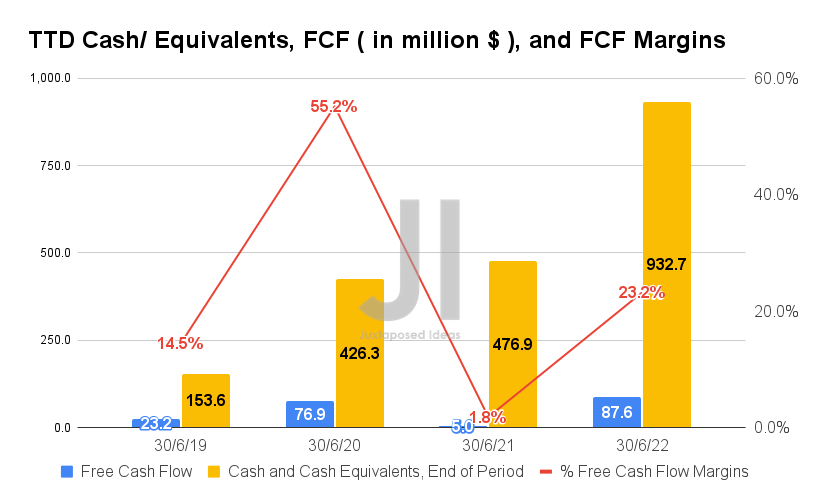

Fortunately, TTD’s Free Cash Flow (FCF) generation remains stellar after adjusting for its SBC expenses. By the last twelve months (LTM), the company reported $482.19M in FCF and 34.7% in FCF margins, representing a massive increase of 48.9% YoY and 31 percentage points from FY2019 levels, respectively. Thereby, contributing to TTD’s growing war chest of $932.7M in cash and equivalents on its balance sheet by FQ2’22.

Stellar indeed, since TTD reports $364.59M of net PPE assets and $48.85M of capital expenditure in the LTM, representing an increase of 53.5% and 36.8% from FY2019 levels, respectively, without the need to rely on any long-term debt at the moment. Therefore, TTD seemed well poised for growth and expansion ahead, despite the normalization in ad spending and global cost-cutting efforts from major tech companies. CEO Jeff Green of Trade Desk, said:

More of the world’s leading brands are signing major new or expanded long-term agreements with The Trade Desk, which speaks to the innovation and value that our platform provides compared to the limitations of walled gardens. This trend also gives us confidence that we will continue to gain market share in any market environment. (Seeking Alpha)

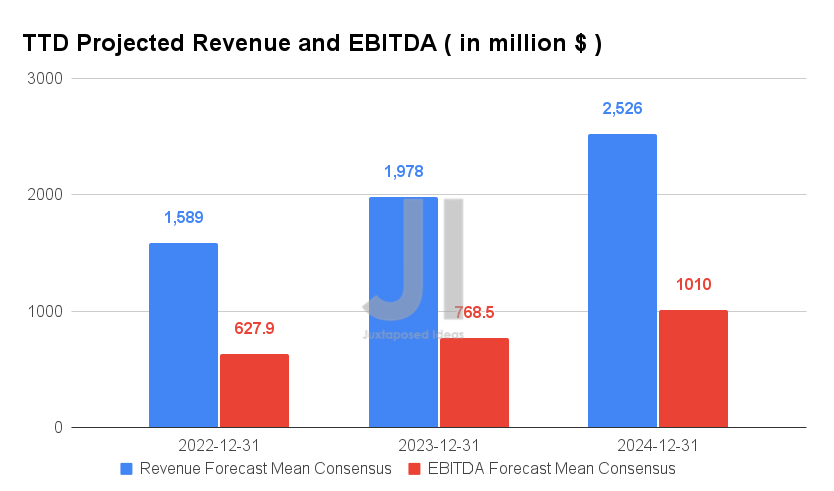

Mr. Market Is Very Optimistic About TTD’s Forward Profitability

S&P Capital IQ

Over the next three years, TTD is expected to report revenue and EBITDA growth at an excellent CAGR of 28.42% and 83.92%, respectively. These numbers represent an apparent acceleration in its EBITDA growth, compared to pre-pandemic levels of 31.11% and pandemic levels of 12.46%. Analysts are also highly confident about its profitability, given the massive growth in its EBITDA margins from 17% in FY2019 to 39.9% in FY2024.

For FY2022, consensus estimates that TTD will report revenues of $1.58B and EBITDA of $0.62B, representing a tremendous increase of 32.7% and 386.7% YoY, respectively. For FQ3’22, the company also guided a stellar revenue of $385M and EBITDA of $140M, representing YoY growth of 27.8% and 56.5%, respectively.

Therefore, given the outperformance witnessed thus far, it is no wonder that TTD has rallied by 38.3% post-earnings call, from $54.50 on 09 August to $75.41 on 15 August 2022. However, some gains are also digested by now, given the moderation of -12.1% to $66.23 at the time of writing on 25 August 2022.

So, Is TTD Stock A Buy, Sell, or Hold?

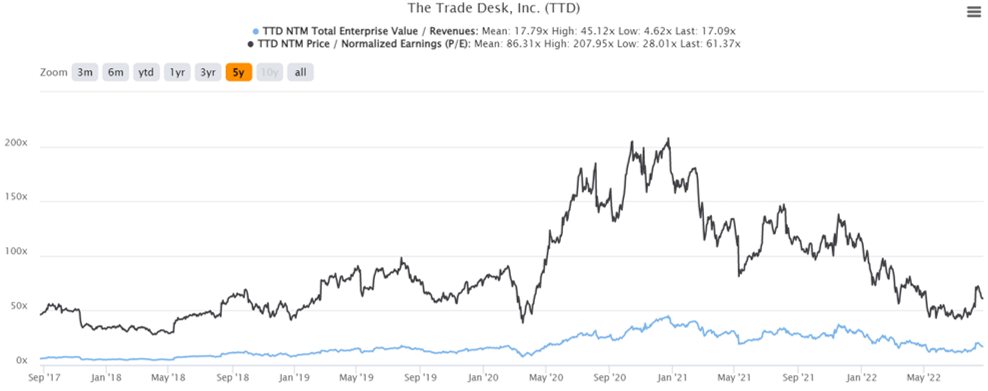

TTD 5Y EV/Revenue and P/E Valuations

S&P Capital IQ

TTD is currently trading at an EV/NTM Revenue of 17.88x and NTM P/E of 63.60x, in line with its 5Y EV/Revenue mean of 17.8x though lower than its 5Y P/E mean of 86.23x. The stock is also trading at $66.23, down 41.9% from its 52 weeks high of $114.09, though at a premium of 69.8% from its 52 weeks low of $39. Thereby, pointing to TTD’s current baked-in premium, given Mr. Market’s optimism on its forward execution for the next few quarters.

TTD 5Y Stock Price

Seeking Alpha

Consensus estimates still rate TTD as an attractive buy, with a price target of $75.20 and a 13.54% upside from current prices. However, given the apparent spike, we prefer to wait for a meaningful retracement before recommending a buy to this stellar stock. The time will come, if investors have missed the previous support level of $40s.

As a result, we rate TTD stock as a Hold for now.

Be the first to comment